Assistant Reserve Bank (RBNZ) Governor Christian Hawkesby is dismissive of the view the Bank’s call not to cut interest rates on Wednesday paves the way for it to ease bank lending rules.

ANZ Chief Economist Sharon Zollner believes that the RBNZ’s decision to keep the Official Cash Rate (OCR) at 1% increases the likelihood of it loosening its loan-to-value ratio (LVR) home lending restrictions on November 27.

The thinking is that enabling banks to lend to more property buyers with smaller deposits, in an environment with even lower interest rates, could set a rocket off beneath the housing market. Yet with the OCR on hold, the likelihood of the housing market really taking off as a result of eased LVR restrictions, is lower.

What's more, interest.co.nz's David Hargreaves is of the view the RBNZ will give banks a carrot in the form of looser LVR restrictions, before announcing on December 5 that it'll be hitting them with a big stick in the form of robust capital requirements.

Speaking to interest.co.nz, Hawkesby recognised the RBNZ considers financial stability when setting monetary policy, but said: “We don’t really get into the fine tuning of how to move one lever so we can move the other lever. We just tend to take them each into consideration separately and we will do that later in the month.”

The RBNZ is due to issue its latest Financial Stability Report on November 27.

Hawkesby also made the point that while the RBNZ considers house price inflation when it weighs up what to do with LVRs, the resilience of the financial system, and the household sector to weather different types of conditions, are its main focuses.

Asked whether the financial system and household sector have become more resilient since the RBNZ last reviewed LVR restrictions six months ago, Hawkesby said: “We’ll sit down and look through the whole plethora of information…

“That sort of resilience question, and that question about financial stability, is a more slow moving one, and that’s why we tend to review it on a lower frequency [than the OCR].”

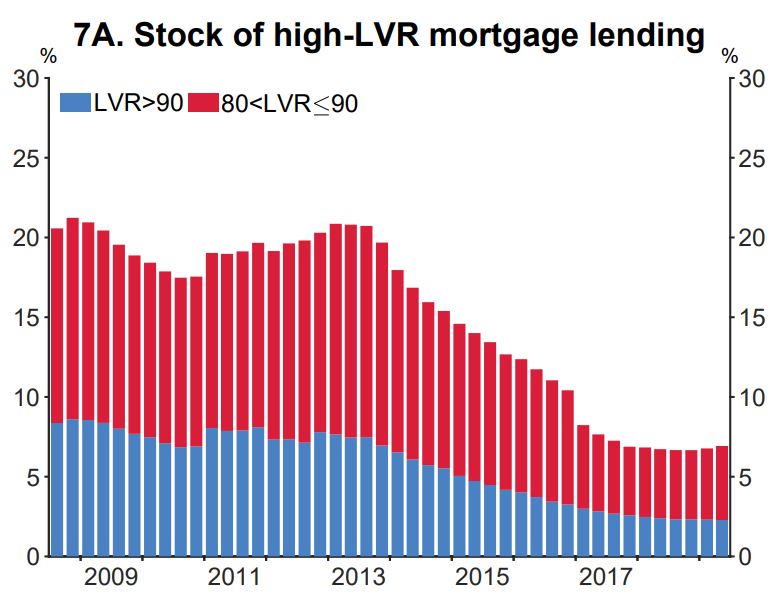

This graph, published by the RBNZ in September, shows how LVR restrictions have reduced banks’ exposures to riskier borrowers. In other words, borrowers with house deposits of less than 10% (blue) or between 10% and 20% (red).

The RBNZ imposed temporary limits on high LVR residential mortgage lending in 2013 and has tweaked these over the years.

Currently banks are allowed to make no more than 20% of their residential mortgage lending to high-LVR (less than 20% deposit) borrowers who are owner occupiers, and no more than 5% of residential mortgage lending to high-LVR (less than 30% deposit) borrowers who are investors.

Is house price growth doing too much heavy lifting stimulating the economy?

Turning back to the whopper August OCR cut, RBNZ Governor Adrian Orr on Wednesday recognised the housing market is a “big channel” for stimulus to come through.

But he said it wasn’t a “one pony show”, as lower interest rates should also prompt businesses and the government to borrow and invest more, as well as keep the New Zealand dollar low, making New Zealand exports more attractive overseas.

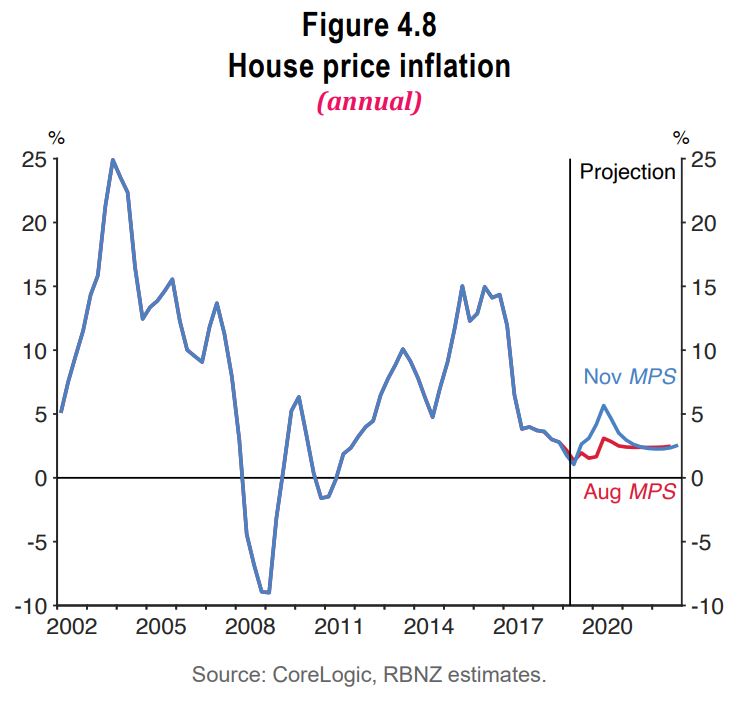

Nonetheless, the RBNZ now sees house price growth picking up more in the short-term than it did in August.

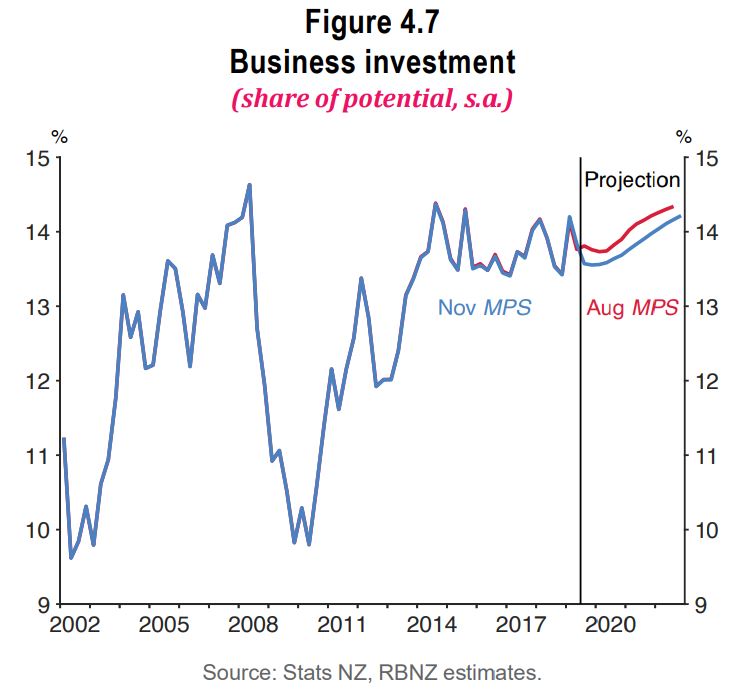

Meanwhile it sees business investment as a share of GDP only increasing slightly due to low business confidence, uncertainty and subdued growth domestically and globally, and capacity constraints.

Asked if he was worried about a disproportionate amount of stimulus coming from the housing market, versus business investment, Hawkesby recognised the OCR is a “blunt” tool.

“The challenge we have is that we don’t have control over which channel is going to be the strongest. So we monitor how things are playing out.”

Hawkesby said he's watching to see how house price inflation feeds into consumption growth. IE people feeling wealthier and spending more.

29 Comments

Good article, thanks. Has improved my understanding.

So the current LVR settings are really pretty restrictive, especially on investors.

27 November is an important day, although as noted in the article the decision on 5 December may mitigate the potential impacts of the decision on 27 November.

Agreed, a great article.

Of concern to me, was that the discussion of OCR and LVRs was largely about their effect of influencing financial stability and stimulus; sadly, there was no discussion on the consequences for housing affordability.

It would seem - as was reflected in REINZ data out today - the Auckland market may be firming (in response to a variety of factors but including the stimulus effect of August OCR cut) - so we need to see how the Auckland market does pan out. A cut to LVRs - or a further OCR cut - would result in a price stimulus at the expense of affordability.

The regional markets appear to be slowing but currently are still showing relatively strong growth well above the rate of inflation, and in a number of instances, considerably above the rate of inflation.

So for affordability issues and no immediate need to provide stimulus to the housing market, both LVRs and OCR should both be held at at current levels.

With the OCR currently being so low, it doesn't provide much room to move in future (without approaching zero or negative which would be interpreted as sending an alarming signal) so the RBNZ need to keep what little powder they have left both intact and dry.

While the future outlook is for "global headwinds and uncertainties", the true effects of these are yet to be seen. As Robertson often repeats at Question Time - the state and nature of the New Zealand economy is well poised to withstand these threats. OCR and LVRs can be adjusted as and when required.

Rbnz goal is stability in banking sector, not creating affordable housing.

In fact if capital requirements increase dec 5 our banks would be safest in world and very robust able to weather big storms. That's what rbnz cares about along with inflation and employment targeting.... not house prices being affordable for whingeing millennials (I'm a millennial so I can say that :)

Affordable house prices.... such an *unreasonable* thing to whinge about.

RBNZ setting interest rates at all time lows to stimulate house prices given its correlation to consumption. Central Banks globally killing the natural business cycle with loose monetary policy. But RBNZ putting in additional capital requirements to stem the risk & moral hazard they created... so *reasonable*.

(I'm a millenial AND a home owner, so I can say that)

Although much of their powder has already been used, with the increasing global economic headwinds, central banks seem to be of the exact same mind of applying yet again the same actions used in response to the GFC.

Whatever one thinks of this action by central banks actions; the outlook is likely to mean stimulus - in our case through further OCR cuts and loosening of LVRs - in the short to medium term and the reality of increasing house prices (despite FHB concerns) and falling TD interest rates for those (e.g. retirees) with cash. FHB and retirees with cash are going to be the casualties.

On one level we can be critical of central bank actions, but at a personal level we need to accept the likelihood and the consequences and react accordingly.

Those who post expecting falling house prices - especially in Auckland - are going to be sadly disappointed.

"Exact same mind of applying yet again the same actions used in response to the GFC."

They have never stopped responding to the GFC, that's why we're awash with liquidity.

On *many* levels we can be critical of Central Bank actions.

They've not only kicked the can down the road... they've paved more road so they can keep kicking the can.

So, let's accept for a moment your position that Central Banks are going to be able to continue this course ad infinitum and, as you think, this means house prices can't drop. Therefore we must accept that:

i) FHBs will increasingly be priced out of the market and ultimately completely priced out because they will never be able to build the required deposit;

ii) Same FHBs who are unsuccessful in will be paying more(?) in rent - cause rents go up ad infinitum too amirite?;

iii) Retirees will cease to consume because they will have no income;

iv) Actual growth in the, you know, real economy will continue to be muted/stagnant (why else do we have this stimulus?);

v) Not-FHBs/Renters will increasingly constitute a larger proportion on the population (see i & ii) and they'll have decreasing disposable income because a) no growth (see iv) and b) increasing accommodation costs (see ii)

vi) The stimulus will be successfully transmitted to wholesale money markets... despite the fact the 2 year swap rate has already rebounded to where it was *before* the 50bp cut.

So who TF exactly is going to be the ones paying ever increasing prices into perpetuity??

Unless they're eventually successful in spurring wage inflation.

It seems to me that the best/desired outcome is for high wage inflation (in NZD), which would require low NZD for businesses to remain internationally competitive. So - debase the currency through low interest rates. The only problem is that everyone else is doing the same thing.

If they're successful in spurring wage inflation then that's a double-edged sword.

You spur inflation then guess what, you've got to start raising rates on the Himalayan-sized debt mountain you created.

That was my thinking from a few weeks back, leave the OCR put to lower the LVR's a little

Looking at the graph, it appears the banks are already lending well less than the 20% limit for owner occupied low-LVR mortgages anyway? Assuming that graph is a showing new lending in each time period, currently they're only dishing out about 7% of their total loan book to low LVR borrowers.

Seems like the only change the RBNZ would make here is to increase the proportion of high-LVR borrowers for investment properties from 5% to 10%, but since it looks like the banks are voluntarily well under all of their limits anyway, would this actually result in any material change in lending standards whatsoever?

Unless that graph is showing all outstanding mortgage value, not just new mortgages drawndown in each time period.

Exactly. The previous relaxation of the LVR limit had little impact, I suspect any further relaxation will have similarly very little impact.

Why? RBNZ capital requirements hanging over the banks are a game changer. The big four only went bananas lending to high LVR borrowers because their internal models allowed them to treat them as low risk borrowers and allocate minimal capital to make those loans. Once banks are using the standardised model these types of loans will no longer be profitable.

Kiwibank and other NZ owned banks never lent excessively to high LVR borrowers simply because it wasn't profitable as it required high allocation of capital. The big four will be behaving similarly in the future.

Irrespect of what anyone may say but the fact is that RBNZ has given themselves a room to reduce LVR on 27th Nov (Carrot) before 7th Dec announcment

Even Labour government has realised that in NZ only ecenomy

is Housing economy.

Take it in writing that LVR will be reduced despite sign that housing market is starting to move up - end result has been decided by RBNZ and now just have to find reason for the same - justify their decession - which will be a piece of cake.

Asked whether the financial system and household sector have become more resilient since the RBNZ last reviewed LVR restrictions six months ago, Hawkesby said: (Pretty much nothing! He certainly didn't answer your question. Maybe he's going into politics?!)

And then there's:

Asked if he was worried about a disproportionate amount of stimulus coming from the housing market, versus business investment, Hawkesby (said) “The challenge we have is that we don’t have control over which channel is going to be the strongest.

Of course, you do! That's' what this conversation re LVR's is all about. But 0% OCR and 5% LVR deposit it will be...and mark my words Mr Hawkesby, it's going to be a disaster of your making....

and looking at the bigger picture, surely the fact that he doesn’t answer these questions indicates to me that the Banks will get into difficulties if they don’t start to lend at the previous high levels. This is a problem across all major Western countries and certainly not limited to New Zealand. Look at how much the Banks exposure now is in the derivatives market with these low interest rates compared to 2007 when interest rates were much higher. Detivatives do not appear on bank balance sheets!

https://www.macrobusiness.com.au/2018/06/australia-sitting-ticking-deri…

And whose mortgages with LVR over 80% have been rising most last 2 years? Yep FHB. Great idea as their exposure to neg equity is highest. Regulator asleep as usual

One channel where low interest rates are pushing on a string is business lending. Hard to induce businesses to 'invest' (i.e. borrow heaps and spend that) when their daily sales are static or decreasing, DSO increasing, and COGS increasing at least partly by fiat (minimum wage....). And neither Orr nor Hawkesby strike me as being competent communicators/salespersons for That effort - pace Michael Reddell.....

“Asked whether the financial system and household sector have become more resilient since the RBNZ last reviewed LVR restrictions six months ago”

We’re still creating credit/money and we are still relying on ever increasing credit/money creation to pay off the former (dependency cycle) so we’re not more resilient in the grand scheme. Just tinkering around the edges.

"Has the RBNZ given itself enough room........?"

Question in it self is the answere... The writer Jenee too knows and is just a way of putting it for reaction and feedback.

If nothing else, it will squeeze the big bank margins and corresponding profits; which are obscene at $5 billion annually.

Put in context, ANZ by itself generates four times the profit of NZ's next biggest listed company. Fonterra would take four years to generate this profit, and we all know Fonterra contributes more to the economy than just one bank; which are just parasites.

The only conclusion you can come to here is banksters profits are grossly excessive, and need regulation to reign in their abuse of power. Does anyone else see the conflict of interest with Jonkey being chairman of ANZ, when while being PM resided over (and facilitated) the biggest growth in household debt NZ inc has seen in history? .

Not to forget that NZ also honoured him with SIR.

Basically everyone who makes it to PM eventually ends up with that honorific, don't they?

God help me Good Samaritian, do you not understand investment at all - you compared a bank to an underperforming NZ corporate. But take any NZ corporate and tell me how much capital that their shareholders employ to produce their lower profit number that they are menat to feel proud of - alot less. Understand return on equity. The banks employ around $30bln of capital in NZ, but they dont have to and if they aren't getting a 12-15% return just watch it go elsewhere in the world i.e. not as readily available to NZ businesses and individuals, and if you think thats a good thing, you really don't understand the consequences of a credit crunch

The simple rule : If the Banks are asking for something, then it is bad for the customers.

Dismissive or not : Stage is set to reduce LVR to give momentum / push to housing market that has just started to move.

Decession has already been made and announcement on 27th November is a matter of formality - Just have to find and give reason to justify the already drawn conclusion.

'Asked if he was worried about a disproportionate amount of stimulus coming from the housing market, versus business investment, Hawkesby recognised the OCR is a “blunt” tool.'

LVR Can be used effectively to control the housing bubble and rising debt in housing sector BUT everyone has realized that if any sector helps ecenomy in NZ, it is only Housing sector

Interesting couple of comments from CoreLogic's head of research, Nick Goodall, on Twitter:

Nick: "I tend to agree there's a good chance of LVR restrictions loosening, however I'm not so sure it'll set the market alight. The banks already have room within the current limits and aren't using it. I believe it's serviceability rates doing the restricting so an easy move for RBNZ."

Me: "Interesting. Thank you. Are banks being more risk adverse/imposing tougher serviceability requirements themselves, or are requirements the same, with house price inflation simply making it harder for people to buy houses they can afford to service the mortgages of?"

Nick: "The serviceability requirements have actually been slightly loosened recently but only seem to be having a minor impact which could be due to potential borrowers not being aware. Greatest change in last few years has been stricter expense testing, as well as house price inflation."

Very interesting indeed.

I suspect the impending RBNZ capital requirement changes are having a very big impact. Lending to high LVR borrowers is profitable if your internal model allows you to allocate relatively small amount of capital. They won't be as willing to lend to the same borrowers if using a standardised model.

Interest rates are so low at present because:

1. The high costs of living; namely essential items (housing, food, petrol prices, etc)

2.

The masses are maxed out on debt

LVR's will be relaxed in November. Very few people would be looking at transacting in December or January. But it will get many potential FHB's thinking about buying in the new year.Enquiries at the Bank of Mum and Dad head office over Christmas or if your lucky the Coromandel branch office. Follow that up with OCR cut on 13th Feb and we are off. A nice little bump. Just in time for November or maybe earlier if he goes full Shane before then.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.