Well, that old spoilsport Grant Robertson 'showed us the money' in the past week but then displayed no immediate inclination to splash the cash in order to give the economy a lift.

In the meantime the business community is working itself into a gloomfest of epic proportions. The Reserve Bank is consequently going to be further leaned on to provide some support for the economy. Hence, therefore, the expectation that interest rates will be cut again by the central bank at its next review on November 13.

How much good that will do is open to speculation.

One thing I have touched on before in previous columns is the possibility (albeit seemingly remote just at the moment) of the housing market going into an upswing that will help support the economy. It's worth having a deeper dig, however.

Theoretically this could be a good time for the housing market. The ever-falling deposit interest rates are killing returns for term deposit investors. The falling lending interest rates are making borrowing money as cheap as chips. All things being equal, a lot of people you might imagine would turn to thoughts of owning an investment property and getting potentially a better yield from the rental return than would be available at the bank. But there's complications, which I go into further down this article.

So, the market may need a bit of a push. The RBNZ could actually help to do that - and help itself with its overall ambition of stimulating the economy into the bargain.

Some context: The Reserve Bank has two major functions - managing monetary policy and promoting financial stability.

To put that in easily recognisable terms, the Official Cash Rate is a monetary policy thing and the loan to value ratio (LVR) restrictions (one of the RBNZ's 'macro-prudential tools') are a financial stability thing. The RBNZ's next big 'financial stability' set-piece is the releasing of its Financial Stability Report on November 27.

Generally the monetary policy and financial stability roles don't overlap much - but one area of significant overlap of course is the housing market - it features prominently in the RBNZ's thinking in both the monetary policy and financial stability roles.

Lending a hand

And I think we are now in a situation where the RBNZ could use its financial stability weaponry to help out its monetary policy objectives.

There's no doubt this country hums along a lot better when the housing market is on an upswing. The 'wealth effect'. People feel like they have more money so they spend more and this turns the wheels of the economy around.

So, some rise in house prices and market activity now would arguably help stimulate the economy.

Okay, so, if we go back to 2013, the RBNZ introduced the LVRs in the face of a then raging housing market - particularly in Auckland.

I think it is often generally misunderstood that the RBNZ's actions were about controlling house prices. No. That's not the central bank's brief.

What the central bank does not want, however, is a lot of people getting into financial difficulty with their mortgages, banks reacting by pulling back sharply on credit availability, a subsequent big fall in the value of houses and resultant big risks to financial stability.

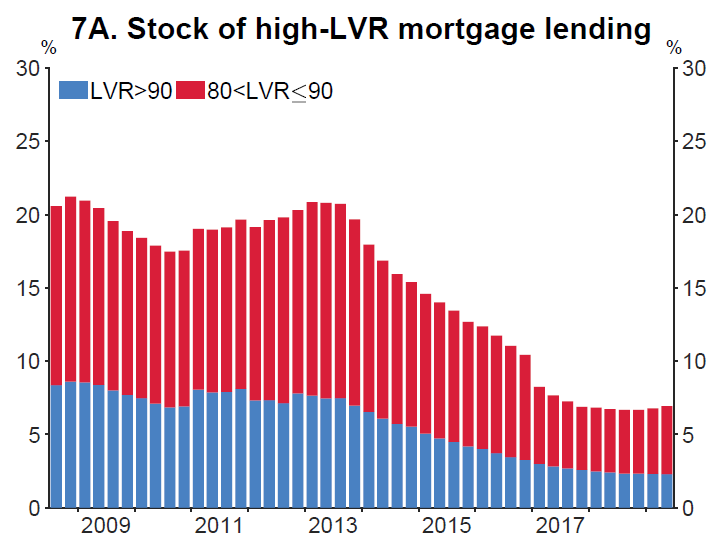

Back in 2013 the banks collectively were really ramping up the numbers and amounts of high loan to value ratio lending (lending of amounts above 80% of the value of the property) as they competed with each other for business. As the below graph from the RBNZ's September 2019 quarter 'Macro-prudential Chart Pack' shows, the LVRs have done a great job in reducing the numbers of high LVR mortgages outstanding.

The big reduction in numbers of outstanding high LVR mortgages has given the RBNZ leeway to relax the LVR rules. And it has already done this. The LVRs were relaxed from both January 2018 and again in January of this year.

Under current LVR settings banks can advance up to 20% (originally 10% in 2013) of their new lending in mortgages of over 80% of the value of the property. That 20% figure is often described as the 'speed limit'.

In 2016 housing investors had punitive 40% deposit rules clamped on to them. These have subsequently been eased to 30% deposits. Banks in theory have some, but not much, discretion to lend more than 70% on the value of properties. The 'speed limit' on this category is just 5% - which is effectively zero really.

The RBNZ has been providing an excellent data series, mortgage lending by borrower type, since August 2014 and we can track what the impact of the LVRs has been on the various buyer groups.

Sharing the spoils

In August 2014 owner-occupiers borrowed 59.5% of the total mortgage money advanced. This dropped to 54.7% in August 2015, rose to 57.7% in August 2016, rose again to 62.3% in August 2017, dropped again to 60.2% in August 2018 and rose to 62.9% in August 2019. In the past three months the owner-occupiers' share of mortgage money has been steady in around the 62%-63% area.

First home buyers, as the RBNZ has subsequently conceded, were "disproportionately restricted" by the first iteration of the LVR restrictions in 2013. This fact, and the subsequent recovery of their participation in the market, is very clear from the RBNZ figures.

In August 2014 the FHB grouping took just 9.7% of the mortgage lending, then 10.5% in August 2015, 12.4% in August 2016,14.5% in August 2017, 15.4% in August 2018 and 17.1% in August 2019. The FHBs have accounted for over 17% of mortgage borrowing in each of the past three months.

And so to the investors. They are the key in many respects in all this.

In August 2014 investors accounted for 29% of the total borrowed, followed by 33.5% in August 2015 (and the share got higher than that in subsequent months - up to 35%), 28.8% in August 2016, 22% in August 2017, 23% in August 2018 and then just 19% in August 2019. In the past three months the investor total has been in an around the 19% mark or just below. A quick dollar for dollar comparison: In August 2019 the investors collectively borrowed $1.023 billion. Back in August 2015 they borrowed $1.989 billion. Not far off double the amount.

So, the stepping back from the market of the housing investors has on the one had been very helpful for would-be FHBs, but on the other has undoubtedly been a big contributor to the overall market going much more quiet. Any uptick of investor involvement would undoubtedly put some buoyancy into the housing market.

But how affordable is the market?

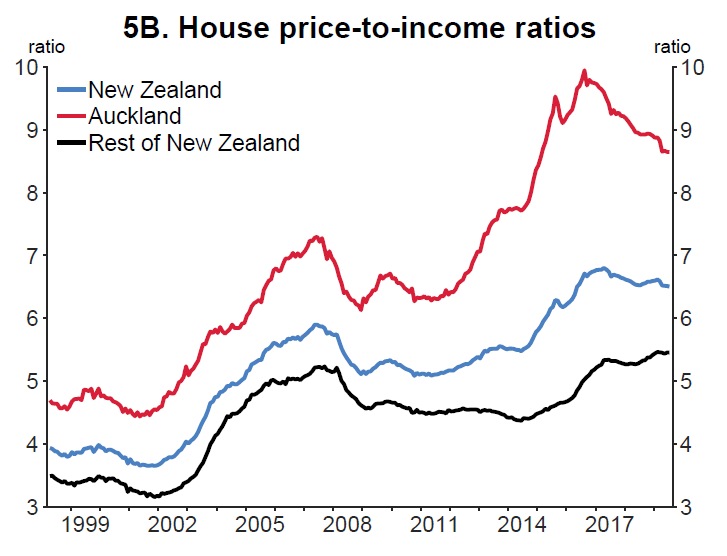

Affordability, as measured by price to incomes, is still high - particularly in Auckland. But it is coming down, as another graph from the RBNZ shows:

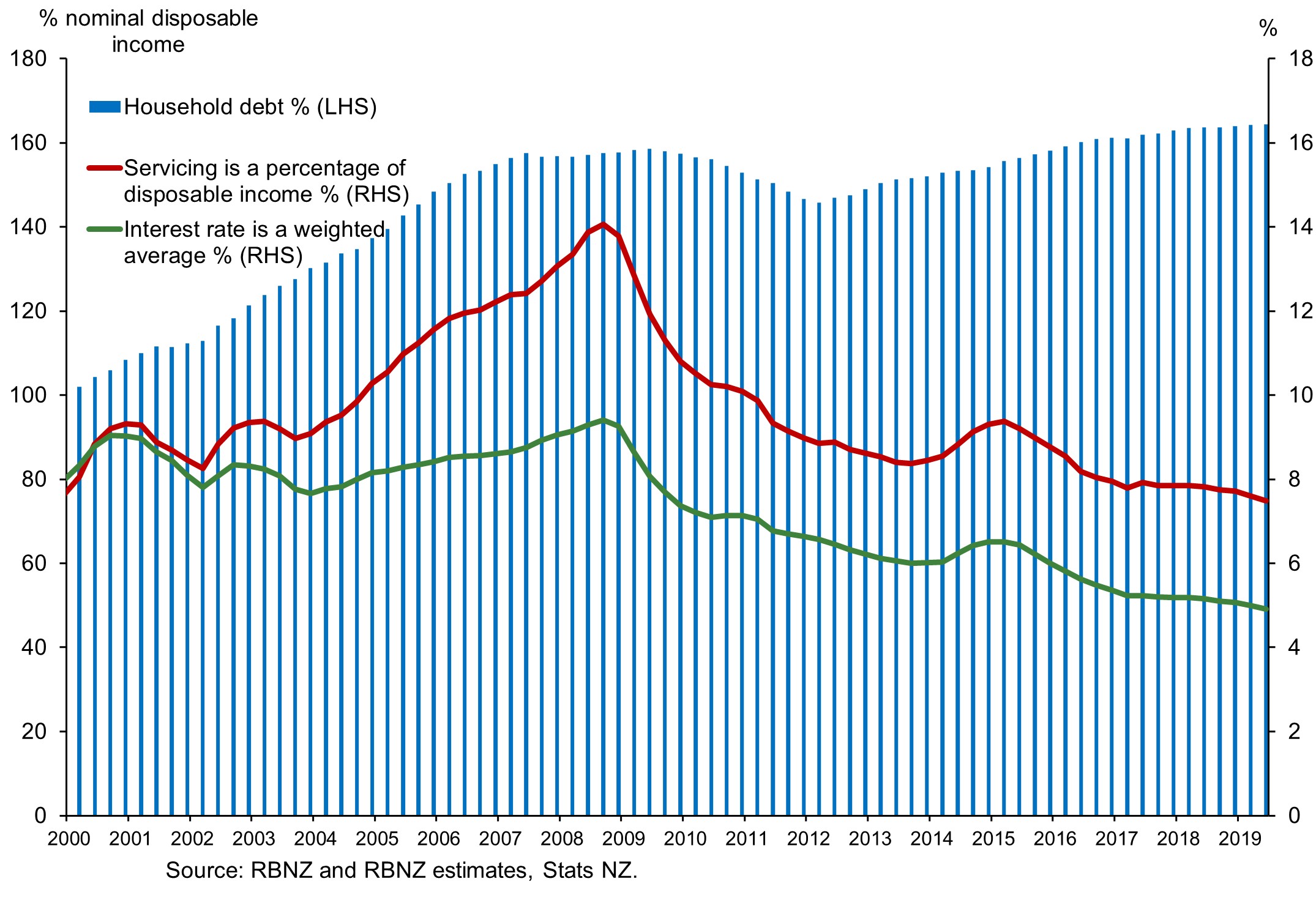

And more crucially still, as another RBNZ graph shows, while the size of loans has been getting bigger and bigger, the ability to service those loans is improving all the time - courtesy of the continually falling interest rates.

All of this says to me that the RBNZ can, and will, feel comfortable relaxing the LVRs further on November 27 - and just possibly giving itself a big hand up with providing some stimulus for the economy.

I honestly think the RBNZ may now feel sufficiently emboldened to 'switch off' the LVR settings for owner-occupiers, including first home buyers. Just to explain: We've already established that the LVRs will never now be 'removed' as such. But the RBNZ could just effectively 'switch them off' - meaning they are not binding for the banks any more. And if they are needed in future, they can be 'switched on' again. So, maybe there will be no official LVR restrictions for owner-occupiers and first home buyers, perhaps from the start of next year.

The bigger poser is probably what to do about the investors. It was the controls placed on the investors in 2016 that ultimately made the big difference to the housing market. Logic suggests that loosening up limits for the investors is therefore the key to allowing the housing market to heat up again. Would the RBNZ be bold enough to drop the deposit limit for investors down to 20%, in line with owner-occupiers and FHBs?

Well, it could do that, maybe. Of course another option might be to look at that 5% 'speed limit' referred to earlier. What say a 20% 'speed limit' for investors? That would mean banks able to advance up to 20% of the new mortgage money to investors for loans in excess of 70% of the value of the property. That would be a considerable loosening.

Surely such a loosening would get some would-be investors back into the market.

Would it be risky for the RBNZ to effectively allow the housing market the chance to heat up again?

Well, it would seem to me that an RBNZ seemingly struggling to get traction with its OCR cuts could do itself a favour by allowing the chance for the house market to heat a little.

And there's more...

There's another potential motivation here too.

In December the RBNZ is set to come out with its final proposals for banks to hold more capital. This issue has seemingly become more fractious as it has gone on.

We've seen dark suggestions about banks holding back on credit in the face of these new capital requirements.

Or that credit will be more expensive.

Or both.

If the RBNZ chooses to greatly free-up the bank's ability to lend on November 27, through a big relaxation of the LVR rules, this will remove one layer of excuses the banks might have why they shouldn't lend to someone. It would put public pressure back on them to keep lending - even if they might be more inclined to claim the new capital requirements are contstraining their ability to lend.

So, therefore, the RBNZ might find the idea of freeing up the LVRs doubly attractive, if indeed the final release of the capital proposals does turn out to be something of a battlefield.

It's therefore well worth keeping an eye on all this as it develops.

Look, maybe the Finance Minister will finally at some stage unveil some goodies through some new infrastructure projects to fire up the economy. Next year IS election year after all.

But in the meantime, the humble housing market could be used to help the RBNZ out a little.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

95 Comments

The RBNZ doesn't need to do anything. They have the property clock up on the wall, so they can see the market will be booming, regardless of any outside factors, in the next couple of years.

*chuckle*

I know, right? Can’t help but chuckle when people talk about “market cycles” like they actually exist!

As long as we agree the RBNZ shouldn't fiddle with it!

The housing market could be in for a "hot summer".......

Let's wait and see.

TTP

People forget that the future doesn’t always look like the recent past. Often it does but you can get really caught out when it doesn’t.

I’ll give you big time respect if you can give me one single example of someone unsarcastically stating or suggesting that the future always looks like the past or recent past when it comes to property. It is far more common that people fail to learn from historical trends and convince themselves that “this time is different”.

I’m keen to hear what you mean by “recent past”. My opinion on property market cycles is based on looking at over 55 years worth of property ups and downs, since records began.

Does Ireland count?

https://www.independent.ie/opinion/analysis/property-markets-no-house-o…

"As one who has been involved in the Irish property market for 40 years and has experienced every type of market scenario, I am totally convinced that the market is currently in good shape and that anyone buying now will do extremely well in the years ahead. There is no better investment than Irish property at present, and I believe that I will be proved right in this conviction."

Guess the year!

Where is the part that he states/suggests the future always looks like the past or recent past?

Examples of optimistic (or pessimistic) predictions that turned out to be wrong are a dime a dozen. If I looked hard and long enough I could probably find examples of people predicting good times in NZ property before the mid 70s and late 00s downturns.

It is a common DGM misconception that spruikers on this site think that “property only ever goes up”, or that property will only ever perform like it has performed over the past 10 years. This is very different to taking the view that property is a sound long-term investment, with ups and downs along the way, and long-term patters are very relevant.

He extrapolated what he saw in the previous 40 years to what would happen in the few later years. He didn't use the exact words you were looking for in that exact order, but it's difficult not to infer that is what he meant.

Obviously property is a sound long-term investment with ups and downs along the way. If that's all we're talking about, there is no need for any argument. As long as it's clear that long term can be very long indeed. From what I can see, if you bought property in 2007 in Ireland, you are still a little bit down even today.

He said that he is a seasoned expert, pointed to his 40 years of experience to emphasise that point, and then made a prediction that turned out to be incorrect. He didn’t say or suggest that the future will be good because the recent past was good. I’m not after those specific words, anything along those lines will do.

But once again, you’ve managed to find a point that we agree on - property is a sound long-term investment with ups and downs along the way.

DD, top of these comments “they can see the market will be booming, regardless of any outside factors, in the next couple of years.” Many assume the market will return to boom times after a short period of flatness or plateau. It will surprise many if it doesn’t, as this has been the history of the past few decades.

I disagree with two aspects of this statement.

Firstly, I think "boom" is too strong of a word. On this site I've seen expectations of property price growth in the coming years, but I don't actually recall any predictions of a "boom" or a repeat of what we saw during 2011 - 2017. On the other hand, baseless claims of a crash based on feels (because China, because Sydney, because Ireland, because Trump, because income to value ratios aren't fair, because I really want a cheap house), are prolific on this site. Personally, I'm picking the bottom of the cycle at 2021/22, strong growth after that.

Secondly, I think the claim that expectations of growth are made "regardless of any outside factors" are unfounded. The predictions I've seen are based on the same market fundamentals that have driven previous cycles (immigration, land and housing supply, interest rates, credit availability, global economic cycle etc.).

DD, I think the credit cycle will have the biggest impact this time. It’s way out of hand, although the banks don’t want anyone to think so. The “boom” has been a cheap, loose credit boom which hasn’t ended yet, which led to speculation (the countless flippers). I think there will be outsized consequences because of it. It was kept rolling in Australia and NZ through the GFC, but eventually the music will stop. Fine with me if it doesn’t, as I own debt free property in NZ, but odds are it’s coming.

Is it more than one debt free property VOR? If not then probably that's something to do, buy another either debt free or with leverage. Because even then you will be low debt levels and low risk.

Houseworks, I do not see good value around right now in NZ property: expensive prices, a lot being built. Happy to wait. Same with the NZ sharemarket in general. With a value investing approach, I've got a list of great stocks that are overvalued right now, that will become undervalued in time, during the next correction. It has been about 10 years since the last big opportunity like that, which lasted a few years but has faded as the cycle has progressed. I look for good assets at bargain prices. I did buy some gold (and gold stocks) last year and early this year, and a significant amount of US dollars before the NZ dollar dropped recently. I have bought some US financial stocks in the past year, as well as some undervalued (I believe) China tech stocks, all well below PE of 10. In general I think now is a time for caution, and patiently waiting. Keeping busy with deep research.

"resurgence in the housing market and therefore a boost to the economy" Why would you want to perpetuate a false economy? See here's the crazy thing, the more you prop up the housing market which was massively inflated by Overseas Speculative Investors to maintain prices the more you kill off our real economies by keeping the cost of living sky high in our main cities. To lower living costs and help real sustainable economies to thrive you need to reduce the cost of living.

Well said CJ099

Thanks Oreo, It just seems so ridiculous to keep our cost of living so sky high here in NZ. When I'm watching business regularly fold here since they can't maintain such high salaries to maintain that cost of living. Particularly in the Tech sector but this effect everything else from Education to exports.

We'll continue to prop up our economic growth with house price inflation and low value industries by bringing in more people who are willing to work on lesser wages despite nationwide high costs and low living standards.

This may be a horrible deal for those used to the opposite but for the majority of our migrants, our rapidly falling living and pay conditions are far better than what they leave behind when moving here.

That's just a mirage. Our lax immigration guidelines stimulates population growth there by creating a housing demand. But the population boom papers over a really sluggish economy and real per capita GDP growth has started to vanish. Go and look at the data. See how our largest city and immigration hot spot Auckland is dragging it's feet along with it's housing market.

https://www.interest.co.nz/opinion/101984/kiwibank-economist-jeremy-cou…

correct. We have a fundamentally weak economy. It's just being propped up by the housing and immigration ponzis.

Some day, I don't know when (I guess 2021/2022) the fundamental weakness will catch up with us, we won't have any OCR 'ammo', and we'll be in deep S##@

Very true. Countries like Singapore, Germany and Sweden are fighting to elongate their economic grace period in the face of an existential threat to their high wage, productive industries. What chance do we have coming out of the next crash as an “advanced economy with a developed market”.

As noted above, if 'this' is all New Zealand has left to support itself, well.....

Well said. I couldn't believe what I was reading from David, actually.

Very much a false economy, that in addition to some' benefits' has a wide range of economic and social costs,

Seems a pretty warped perspective indeed. Too many years of housing being treated as an investment vehicle for certain folk who inherited affordable housing from preceding generations and their governments. Little regard for its role in the wellbeing of society across generations and versus other investment that is needed more - i.e. productive business.

Yep. More class warfare against renters, that'll definitely save the economy.

Nothing brings out the commie strain in me like this kind of shallow, counterproductive stupidity.

"I honestly think the RBNZ may now feel sufficiently emboldened to 'switch off' the LVR settings for owner-occupiers, including first home buyers."

It isn't April Fools Day.

How about the RBNZ just buying each of us a powerball ticket on Wednesday, I'm sure that could be parlayed into a GDP boost.

That might keep the music on for another year or so but the house of cards are doomed to collapse inevitably.

.. nope ... " this time is different " ... aha haaaaa ...

RBNZ there are simple answers to stimulating NZ economy without pushing us in to deeper debt.

So how to revers a false economy created by Speculative Overseas Investors - Easy! Tax the by product!

Step 1) Almost 40,000 empty homes are now situated in the central and main commuter districts of Auckland. If we were to adopt the very successful Vancouver Empty Homes Tax model this could generate $460,000,000 in tax revenue each year and probably at lot more! This is based on the average unoccupied home value being $1,170,000 due to most of these homes being in the more expensive parts of Auckland according the the latest census figures, - 1% tax on home value = average yearly tax of $11,700 per vacant property x that by 39,393 unoccupied homes = $460,898,100 in tax revenue. Main advantages: -

1) Huge tax revenue generated that can be used to build homes and improve services for NZ.

2) You are mostly taxing Speculative Overseas Investors vacant property who can't vote in this country.

3) Reduces the overall cost of living in Auckland by freeing up more rental property.

4) Helps business to thrive since they can attract and retain staff more easily with reduce cost of living in AKL.

5) Deters money laundering.

More info on the Vancouver's empty homes tax : Opinion: What Vancouver’s impressive Empty Homes Tax revenue tells us. https://www.vancouverisawesome.com/2018/11/30/empty-homes-tax-vancouver…

That sounds way too bold, innovative and effective for our muppets...

Cynicism to one side, totally agree!

Thanks Fritz, I really hope that Labour don't drop the ball on this issue, it's such easy revenue that could be put to good use for NZ. And it's been tried and tested around the world in cities where Overseas Investors liked to park this money. Surprising how much the overseas wealthy and money launders are willing to pay extra tax for that privilege.

Have you written to any of the ministers on this CJ099? If you haven't please do.

I wrote to Woods asking her why a mass government leasehold ownership scheme isn't being progressed.

Yes, Also put forward the current evidence, would advise everyone to voice their opinion on the subject to help our real economies. :)

Good on you. That's all we can ever do. Helpful to provide good evidence. Fingers crossed.

Did u cc the Greens? If not, forward it on to them

Fritz did with his mass government LOS (Leasehold Ownership Scheme)

... as much as it seems a waste to have houses lying vacant ... it is the owners prerogative to do so ... we're still a free and democratic state ....

On the other hand , introduction of a land tax over and above regular rates would stimulate owners to get an income from their houses and swathes of undeveloped land ...

.. the perfect way to pick the pockets of absentee and foreign owners . . Land Tax !

There's no doubt this country hums along a lot better when the housing market is on an upswing. The 'wealth effect'. People feel like they have more money so they spend more and this turns the wheels of the economy around.

by Audaxes | 26th Sep 19, 8:20am

The cruel hoax of government sponsored central bank monetary policy is being exposed for what it is.In March 2017, former Treasury and Federal Reserve (Fed) official, Peter R. Fisher, delivered a speech at the Grant’s Interest Rate Observer Spring Conference entitled Undoing Extraordinary Monetary Policy.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

'People feel like they have more money so they spend more and this turns the wheels of the economy around.'

If housing was affordable, or a lot closer to affordable, people wouldn't need to 'feel' like they have more money, they would actually have more money!!!!

I'm honestly a bit sick and tired of the housing debate. We all know there are meaningful policy responses, but there's no real appetite for them.

Personally, I don't think Labour are that serious about it from what I have seen and heard. Twyford is, to give him credit, but he's got other issues (like - he's dogmatic, over simplifies the issue, and has a superficial understanding of the issue, the old 'a little bit of knowledge is dangerous'. HE's also arrogant and only listens to the advice he wants to listen to )

So, some rise in house prices and market activity now would arguably help stimulate the economy.

by Audaxes | 13th Aug 19, 12:12pm

Is this analysis based upon all lending or that which is restricted to productive investment which is eligible to be counted for GDP calculation purposes? Because:

The majority of bank credit creation in the UK [and NZ] is not even used for transactions that contribute to and are part of GDP, but instead is used for asset transactions. They are not part of GDP, since national income accountants require a ‘value added’ for inclusion in GDP, not just the shifting of ownership rights from one person to another. When bank credit for asset transactions rises, asset prices are driven up, because the loans do not transfer existing purchasing power, but instead constitute an increase in net purchasing power: money is being created and injected into asset markets. When a larger effective demand for assets is exerted, while in the short-term the amount of available assets is largely fixed, the price of assets must rise. Link-section III.

The article is apparently about housing activity, not a singular mention of housing sales volumes. However,in summary, I have a property that David can purchase from our family trust for 10 percent more than we paid 6 months ago , Jenee can buy it from you after a further six months for 10 percent more , no need to use Barfoots, , I'm sure Greg will need an investment property six months after. He should be able to give it indoor outdoor flow and flip it for 20 percent more to Sally from overseas . Sally however is not interested in a large mortgage. She has a set of chairs and enjoys music

Umm, I see a slight blockage to the ponzi chain. That all depend on whether Sally can get her money out of her mother land. ;)

Article: South China Morning Post: China Economy - China’s capital outflow controls have gone to the ‘extreme’, former central bank adviser says.

https://www.scmp.com/economy/china-economy/article/3012312/chinas-capit…

Again CJ099 well said,

Housing has been treated as a commodity ...but it is much more than that. Last info I could find was that 33,000 houses in Auckland were vacant. Where did you get your figure?

Cheers, Here you go Shawking: If you take a look at the chart, it highlights Auckland's unoccupied dwellings 2018 total is 39,393. Though I don't think this takes in to account vacant lots, where long term vacant homes have had to be demolished due to disrepair, squatters etc. It does provide an interesting break down of regions and where most of the vacant homes are in the more expensive areas of AKL.

https://www.interest.co.nz/property/101855/2018-census-shows-191646-hom…

You are always banging on about this topic CJ its your hobby HOARSE

At least he is banging on about something in the interests of wider society, rather than in his own selfish narrow interest.

Yes take note Fritz. As for me I am keeping the economy humming by employing staff and contractors as well as buying materials. Is that what you call selfish narrow interest?

ha ha, the old appeal to 'the charitable businessman or landlord'. That's an oldie, but a goodie.

Presumably you are not doing that as a charity, but as a way to make handsome profit. Not that there's anything wrong with that at all.

But to dress that up as charitable...

Hi Fritz,

Houseworks does a lot of good for the economy and society.

CJ099 is merely shaking with anxiety. He's been banging away at his keyboard all morning - achieving absolutely nothing.

TTP

LOL, So Ttp have YOU come up with or even put forward any plan what so ever that would help generate over $460,000,000 in tax revenue each year? I think not! We have. I see you're the one doing nothing - Go on make a suggestion, what's your plan to help NZ? :)

Yep let's hear it from the guys...what's your vision for NZ?

The number of responses so far is indicative of the expected tax revenue that would be generated from your "scheme". I think you will find that most of the houses were not actually vacant CJ

Well feel free to disprove the 2018 Government Census HW. Do you have and statistics to back up your claim that Auckland's empty homes are actually all occupied? Please send us the evidence. If you can't then we know that you're just telling porkies.

Evidence is there online, either you dont know how to look it up or you're wilfully ignoring the truth. I think its the latter CJ. You will continue to disagree of course, that is why you should cc the Greens. If taxinda is not in favour then there is still hope with the Greens

LOL, wow is that really the best you can do HW! Nahh if that was any evidence to disprove the statistical evidence of the 2018 Census you would have post the links. Clearly you have tried and come up empty to support you very empty claim. Ahh well too bad, try again.

Obviously you dont hold much faith that others believe you, as you say you "hope that Labour don't drop the ball on this issue"

Taxing "Empty Homes" is on their radar hence why they had to be so very thorough with the recent census data. As you have found, it's very hard to pick holes with taxing Overseas Speculative Investors; It's a Win win tax and a huge revenue gain for NZ.

Aren't you being a Doom Gloom Monger HW, look on the bright side. :)

That's bullshirt, "cc the Greens" and tell them you and Fritz are friends, that will get some action

Hi CJ099,

Suggest you take a hint from all your DGM mates.......

Bugger off - just like they’ve done.

TTP

Charming. That's abusive. Editors - will you ever do something about this ?

It wouldn't be so bad if the likes of these property trolls actually provided an actual informed opinion from time to time.

I honestly can' be bothered with it anymore, I'm sure there are others who feel the same.

Maybe the Editors won't miss us.

Only if it affects ad revenue.....

LOL Is that the best you could come with TTP! Well that just proves you're a TROLL. With no credibility to back up your claims. Here we are; Fritz, Oreo, Shawking and the other helpful and positive commenters actually putting forward beneficial good ideas that could add millions to support our NZ economy, and all you can do is huff and puff and be abusive. Not very sporting of you is it. :)

Sporting or not it does expose the weakness of their arguments if they have to resort to ad hominem attacks. I do wonder if deep down they know it is all to good to be true and are scared that it could all be taken away from them if the predicted market crash / recession does happen.

EDIT : spelling

. . there is a school of thought that we're currently experiencing a deflationary depression ... hence the poor business confidence ( it's not all your fault , Taxcinda ... not 100 % , anyway ) ...

Which makes me wonder why house prices are still creeping up ...

... too much immigration ? .. yes Taxcinda ... that is 100 % your fault . .

I very much doubt it would cause a market crash, it hasn't caused other cities to crash where an Empty Homes Tax is in operation. It would allow more rental properties to be added to the market in cities such as Auckland. Another main benefit would be the huge revenue stream generated form Overseas Investors actually having to pay a bit more tax on their empty homes. :)

Maybe his DMG mates have somewhere to be on a Sunday afternoon, rather than being a troll on the internet.

I've long held the view that LVR's were nothing to do with financial stability at all. In light of the evidence that has accumulated since they were implemented i.e. the trapped generation of renters denied the ability to borrow to buy and who now are paying some rentiers mortgage instead...I think the LVRs were absolutely a tool designed to kneecap prospective owner occupiers from taking housing stock out of circulation so investors and developers could have their speculative forays unopposed and be delivered a handy, captive segment of the population as tenants. Cause and effect. It wasn't till a thunderous uproar broke out about how developers and speculators were rampaging unchecked through communities that they too got the LVRs applied that had some how been conveniently overlooked. Cause and effect. Disgusting and Key and English were neck deep in it. I bought my first home in the mid naughties with something like 90% debt yet still made the payments. Mind you that was prior to the gfc and the mass casualisation of employment that Key's government allowed so I guess risk was lower?

“Affordability ... is still high”, so highly affordable?

As bizarre as it sounds, due to super low interests rates affordability is increased, despite high prices of houses. Unlike the days of Alan Bollard at the helm of the Reserve here in NZ where houses were cheaper yet interest rates went up so steeply that they actually caused a recession!

Yeah but as we all know it's hard to get a deposit together

There's quite a good lead article in the latest North and South on millenials staying at home with their parents. Eaqub reckons it has increased from 23% of households having an adult child at home, to 26-27%. That will be increasing average occupancy, a further factor in the exaggeration of the housing shortage.

Coming to a family near us all!

New York parents sue 30-year-old son who refuses to move out. Court documents say he does not pay rent or help with chores, and has ignored his parents' offers of money to get him settled. It was becoming clear their son had no intention of leaving.

It's called failure to launch ......

.. or , a failure of the parents .. if he feels no compunction to chip in some money for food & power ... not the need to do any chores ...

Spoilt brat ... but he learned to be spoilt by whom ?

Change the locks

Wow those are some terrible ideas.

First of all the wealth effect - note the work the word ‘feel’ does in your sentence. Most people don’t gain wealth from house price rises, they just ‘feel’ wealthier. Therefore rising house prices just encourage people to take a more myopic approach to financial decision making which therefore just transfers spending from the future to now. This in part explains why our economy is so anemic now.

Second - the economy needs to learn to operate without the sugar rush of housing. We want lower interest rates to encourage investment in the factors of production not housing speculation. They’d be better off introducing a DTI and doing a big cut to rates at the same time. That would make it harder to take on housing debt but lower the cost of debt across the board. This would challenge banks to find some businesses to lend to.

Well if the price of their house rises, they make a capital gain they can then use to acquire more cheap debt, be it for a rental, a new car etc.

But I agree housing speculation has severely hamstrung our economy and also household spending and confidence

Absurd.

The continuous focus on the property market is nothing more than a symptom of:

a) an unsustainable immigration rate

b) an inelastic RMA

c) a tax system favouring the most unproductive use of capital bidding up land prices

Its no wonder NZ continues to slide in gdp/capita rankings vs other countries

... so true .. we have had 2 successive governments who foolishly thought that rising house prices were a good thing ( Helen & John ! ) ...

Nothing was deemed amiss as $ 200 Billion was borrowed by the private sector to bid up & up house prices....

... but try to get the central government to borrow just a fraction of that amount to put into renewal and upgrades of our country's infrastructure ... and it can't be done ... no sirree Robbo ... it's all too hard , or it will upset Julie-Anne ... SIGH !!!

In fairness to John Key, he thought it was a terrible crisis...until he got elected, at which point there was no such crisis and only a good problem to have. A betrayal of younger Kiwis, that.

For property investors, LVR's may be a lower priority

measure now, and less of an issue.

A few mortgage brokers have stated there has been an increased focus on debt servicing criteria by banks, and applying stress interest rates - this seems to be the key constraint to borrowing capacity. This may be due to Responsible Lending Guidelines - if the banks have breached these then the borrower may have some legal recourse against the bank.

There is a property mentor who has an LVR of 50%, yet he was unable to borrow more due to debt servicing criteria constraints.

Also refer here : https://www.landlords.co.nz/article/976515716/servicing-test-changes-li…

Sounds like unofficial DTI policy's.

https://ourfiniteworld.com/2019/09/12/our-energy-and-debt-predicament-i…

Note the divergent graph: What could possibly go wrong.

Then read Steve Keen's 'Can we avoid another financial crisis?

We need more financial scribes who aren't wedded to conventional economics, and we need to be beyond a belief that ever-more debt can be entered into. The whole planet is heading Japan's way, whether it likes it or not. Even below zero interest-rates won't solve that dilemma - although they might soften the landing for some

Have you been to Japan , Mr PDK .. and seen first hand what it is like there ? .. when it's not typhoonicating , I mean . . .

Where is Retired Poppy? I miss his negativity.

..probably following the "I don't waste time arguing with people who are stupid' approach.

Reality dawned more like

If the Governor wants to win his battle against the Aussie Banks, he should actually tighten the LVR rules, so some sense continues to prevail in propping up the bubble housing market and give a breather to FHBs.

It is time the NZ economy is gradually weaned away from the lopsided dependence on the housing as a only investment game in the country.

All the problems in housing...and the answer come up with is:

"Get the young Kiwis to take on lots more debt!"

Where is Mike Kirk, the ex agent?

Probably out door knocking even though he isn’t selling real estate anymore!

He's an ex commenter too THE MAN :))))

Very good article David (as evidenced once again by the multiple squeals of the masses)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.