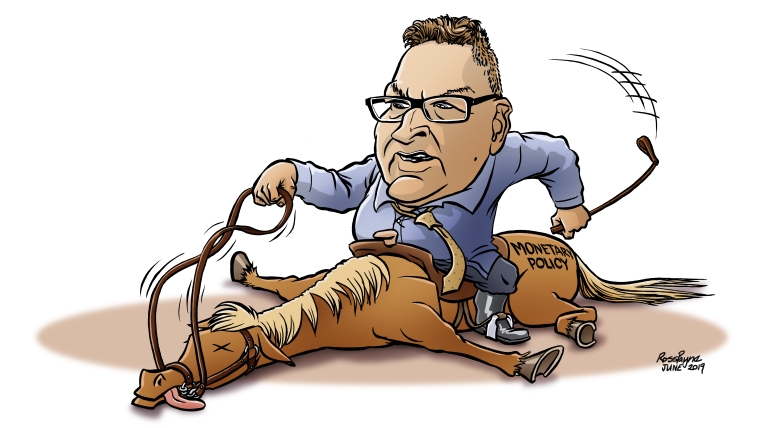

All sorts of metaphors involving horses came to mind when viewing the results of the latest ANZ Business Outlook Survey released on Thursday.

On the one hand I was thinking "well you can lead a horse to water but you can't make it drink" and on the other I was thinking of the expression "flogging a dead horse". And I was thinking of these two in tandem.

So mixing and mangling those two completely, I came up with "you can't lead a flogged dead horse to water" as a summation of where we are right now. Huh? What's that, you say? Well, apologies for the incomprehension. If I can put that all into context using plain english - it really is starting to look as though Reserve Bank Governor Adrian Orr is taking on a battle he may struggle to win to get the country spending money on the back of the 'shock and Orr' cut of the Official Cash rate from 1.5% to 1% on August 7.

If we look at the latest ANZ survey we see that apparently only a third or so of the responses to survey were completed AFTER the OCR cut was made. So, some caution is required in drawing conclusions. But by all accounts the responses of those third who answered the survey after the OCR announcement were not markedly different to those received before it. In other words nobody had been particularly cheered by the OCR cut. And they weren't suddenly in the mood to expand their business.

Perhaps Orr is starting to feel the weight of the task he has in trying to stimulate some activity.

I thought his decision to circulate "comments" in the aftermath of his visit to the high-power Jackson Hole talkfest involving the creme de la creme of central bankers in the US over last weekend was unexpected and noteworthy.

'Come on and spend!'

Reading heavily between the lines I could see a strong thread of frustration; a sense of 'look, I've given you the stimulus, come on and spend some money!'

The Orr comments were targeted at both the Government and the business sector, but there's no particular sign that anybody's biting. Perhaps the best hope is that the Government will loosen the fiscal straitjacket and start dishing out the sweeties, particularly as next year is an election year.

But business seems determined not to be cheered up, despite things not looking all that bad domestically, surely. Of course if you look offshore, well anything seems possible - in a bad way - and presumably that's where all business eyes are at the moment.

The financial markets here were certainly startled by the magnitude of the OCR cut. But it hasn't put anybody in a better mood.

Drifting expectations

Worryingly from an RBNZ perspective, the ANZ survey showed another tick down in inflation expectations.

The RBNZ watches that pretty closely. It got a sharp shift downwards in inflation expectations in its own quarterly survey of business views that came out just before the last OCR decision and I dare say that may have provided a final pervasive argument in favour of a double rate cut.

So, if inflation expectations generally start drifting well below the 2% midpoint of the RBNZ's inflation target then that will heap more pressure on our central bank to act further.

The RBNZ is running out of ammo though.

Unless there is a serious change in sentiment within the next month or few then I think we are heading for unconventional monetary policy territory.

It just seems likely that it will become clear that the conventional weapon of choice, the OCR, is not going to gain traction in terms of stimulating the economy.

Whether unconventional policies will carry any greater potency, well, who knows.

Stirrings in the housing market?

Strangely one ray of light, one potential avenue, might be if there are stirrings in the housing market.

Logic says that the disappearing 'safe' yields on bank term deposits might just encourage some investors back into the housing market. And that of course could spark things up a little in the market.

It won't happen though if the confidence is low. So, while logic says we could be in for more activity in the housing market, it ain't necessarily going to happen if people are feeling in the dumps.

The Spring housing market is therefore going to be very significant this year.

There's no doubt that the New Zealand psyche, heavily influenced as it is by property ownership, is given a positive lift if the housing market is buoyant. And if that happens people start to spend more.

Doubtless the RBNZ and Governor Orr will be mindful of such things as well.

Overlapping roles

While the central bank's financial stability and monetary policy roles are seen largely as discrete, this is one occasion where we may well see some overlap.

I think it's almost a given that at its next Financial Stability Report announcement in November the RBNZ will further loosen the loan to value ratio (LVR) limits.

In the current environment would the RBNZ consider removing the extra limits (currently a 30% deposit minimum) on investors?

That could certainly stimulate some activity. But it might be risky too from both a practical and political perspective.

There's no doubt the first home buyers have been given more space to operate in with the knocking back of investor interest. Where they were crowded out by investors in the early days of LVR limits, the big deposit requirements for investors that were subsequently applied levelled the playing field and allowed the FHBs back in the door. To their own home.

Would encouraging investors back into the market by taking their handbrake off negatively impact the FHBs?

Take a risk?

I do wonder though if the RBNZ might be prepared to take the risk now.

As Governor Orr's comments this week indicate, he wants to spark up some activity.

This probably needs to be done one way or another and probably all things would be considered to make this happen - to stimulate economic activity..

To push the language at the start of this piece even further then, Orr needs to find a winning horse to back.

But it isn't looking easy at all.

The horses are all cowering in the stable.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

98 Comments

We've been spending to create work for years, so why isn't this working ?

As you say, we're on a dead horse.

But the reason its dead is that the life has been sucked out of it by its Foreign Owners.

Foreign Owners are embedded to the tune of taking $20 Billion profit from our economy each year (Banks $5 Billion p.a.).

1 year is 40 years Fontarra profits, the next decade $200 Billion would take Fonterra 400 years of working dawn to dusk to match the Foreign Investors.

Given Fonterra is our largest exporter, where do these Foreign Investors think their next decade $200 Billion profit is coming from ?

They're so embedded in the supply chain, they actually OWN NZ.

Tenants in our own land. Great work Asset Sales, now show me the money.

""where do these Foreign Investors think their next decade $200 Billion profit is coming from ?"" Answer: they intend buying Fonterra.

Leonardus - Truly, are you suggesting that the average NZer might one day become a saver and an investor such that NZ might not have to rely upon foreign investors to front up the $30bln in capital to run the NZ banking system for instance - fat chance unless you're happy with some third world banking system, and all the downside for business and individuals that goes with that.

One and a half years foreign profits from NZ is the $30 Billion bank capital done and dusted.

Do the math.

So Leonard explain who and how someone is fronting to lend the $30bln to fund the purchases whilst that $30bln is earn't ? Also since the banks profits are about $7.5bln over that period (that funds 95% of all the activity in NZ), can you please give me a link to the facts about the other $22.5bln over that period

Are the Kiwi banks third world?

Long and variable lags. Policy changes like cutting interest rates take 6 to 18 months to work through the economy.

Variable and unpredictable results. Central planning assumes predictable results based on assumed conditions which may or may not exist.

Mr Orr's scheme rather depends on more mortgage borrowing and more construction work to keep us all employed while the world has a slowdown. It's not a bad plan, but plans have a problem when they encounter hostile forces. Interesting times ahead. It could mean cheaper houses if construction continues apace, or even more ridiculous prices, or one followed by the other. Everything gets unstable during slowdowns.

Long and variable lags. Policy changes like cutting interest rates take 6 to 18 months to work through the economy.

The RBNZ has nearly cut the OCR in half twice since April 2015 and yet we are in need of more failed "stimulus" measures.

Low mortgage interest worked when they were lowered from around 9.5% to 4.5% after the GFC but have since become less effective. All they are doing now is making the huge mortgages over longer periods time more manageable. Those with savings don’t go out and spend when there are very low interest rates as this involves spending capital rather than interest.

Exactly. Well put

Exactly - Law of diminishing return.

Well articulated. I was thinking about this very issue yesterday. As a net saver/ +ve cashflow investor, I can assure anyone who thinks they’ll psychologically nudge me into spending more by reducing deposit interest: it’s not going to happen. If my secure money is growing more slowly, like hell I am going to go spend what’s left.

Policy makers may think I should be nudged into taking on debt instead because interest rates on debt are low. But that’s the point; if they’re at all time lows, the return to mean would be even more painful.

I think I've seen studies from the US where cutting interest rates from already low levels actually made people save more and spend less. As the realisation sets in that their future income levels are dropping due to low interest rates, the only way to get them back up is to add more capital, thus they start saving harder.

Low interest rate is good for housing market and those who were already planing to buy will be more motivated but to expect anyone to buy just because interest rates are low is doubtful.

No interest in bank deposit or 2% interest will cover the inflation which in the falling market/ sentiment is better than losing deposit ($1500000 may get $3000 interest on deposit, which is hardly any but better than paying a deposit of $150000 for $750000 house and if in near future the value falls even by 5% - talking about minimum fall which happening will not be surprising if not 10% or 15% than are looking at $37500 loss from $150000). So low interest on deposit is still better than investing for short term and even for long term if one can get $750000 house for $715000 down the line, is it not better to hold on to deposit as $150000 will get more in future despite low interest on deposit.

If the reserve bank is jumping the gun that itself indicates the future of the economy.

Giving antibiotic in anticipation of sickness ( or may be already too sick and normal people are not aware except reserve bank - hence the decession) and if not than why give antibiotic before as now when needed in future will be ineffective.

Low, or even no, interest on a cash deposit in a bank is better than lashing out money on a depreciating asset. That's what low-interest rates are SCREAMING at us, and have been for some time! The lower mortgage rates go, the higher the likelihood of a fall in the resale price of the asset you've just bought or hold already.

And ultimately we know how destructive low-interest rates will be....or we should by now....

(Via Mauldin):

"... if Roubini is right then rate cuts aren’t going to help. Nor will QE. Both are simply ways of encouraging more debt which...is no longer effective at stimulating growth. They are, however, effective at blowing up bubbles. The closer yields are to zero (or below), the more impossible it is for both small savers and giant institutions to reach their goals with fixed-income assets. They will have to take on more risk and it probably won’t end well for them. But no matter who you are, you’re going to have a bumpy ride between now and next fall. Now is the time to get ready"

Yesterday was actually a 'better time to get ready', but today isn't too late. But tomorrow, it almost certainly will be.

As Shakespeare wrote some time ago:

" Better 3 hours too early, than a minute too late"

SCREAMING...is correct. Interest rates are falling and with the speed that they are falling indicates that future is not good for asset class and is the very reason that it is been done AND now we are entering unchartered teritory of zero interest or minus interest.

How long the Euphoria of low interest last as low interest is the norm now and after another round of fall than what ?

Encouraging people to borrow more and more and spend, Is it the right way specially for those who may end up borrowing more than their capacity to pay if by chance the interest rise.

'The lower mortgage rates go, the higher the likelihood of a fall in the resale price'.

Exactly, because future weakness does not have the same buffer available. Effectively if the ocr is cut to zero or lower, then there's not much ammo left to stimulate demand in the future.

I think many people fail to understand this point. Perhaps because they believe there be another boom, interest rates will rise again, and then be able to be cut again if there is a slowdown.

Well, this time there won't be a boom. Prices will probably slowly rise, but no boom.

RP, your quote of Mauldin states that it won't end up well for… SAVERS and giant institutions who hold fixed-income assets. He then goes on to say, quote:" They will have to take on more risk and it probably won’t end well for them"

Yesterday, Did mention : Giving antibiotic in anticipation of sickness ( or may be already too sick and normal people are not aware except reserve bank - hence the decession) and........

Today the article as below on same website :

CURRENCIES

"Rightly or wrongly, the RBNZ were signalling that they knew something bad was on the horizon for the economy that the rest of us were unaware of." by Roger J Kerr

Know a family who was contemplating a holiday to Europe but now are putting on hold as are worried about future and this is more to do with sentiments which is reflected by 0.5 fall in rate by reserve bank.

With absence of foreign buyers and money laundering very hard for FHB to buy house in Auckland on NZ wages and nothing can change it unless house price falls in line with NZ wages and that will take some years to come.

I think if mortgage rates drop to circa 2%, and lvr's are loosened, then we could see a reasonably significant lift in FHB activity. Not a boom, but a lift.

A lot will depend on the wider economy. Will the development and infrastructure sector fall away significantly? Or will the government step in to steady the ship? I think they will, but it will be election policy which means we don't see a real lift for the economy till 2021.

So how I see it:

- another 2-3% fall in Auckland house prices

- IF the ocr is cut to zero and over is loosened, then over 2020 we will see a 5% rise in Auckland prices

- then similar in 2021

I think the bust of this bubble won't be until some time in 3-5 years time when there is a real economic shock and we don't have the monetary ammo left to prevent the bust.

Question to be asked, how many can buy million dollar house in Auckland at least not FHB and so called investor are reluctant to buy in absence of fast money/CG.

Domino effect is in place so do not see any rise in house price. How much will it fall and how fast have to wait and watch because of low interest. Speed of fall may be slow or delayed for low interest but is inevitable and the process is well underway atleast in Auckland.

Valid point.

Then a key question is to what extent FHBs will buy in the 700-800k range?

That’s going to get you a 2 bedroom place, maybe a three bedroom place further out.

Many FHBs I know are adamant they need a 3 bedroom place. Buying a home often coincides with starting a family.

There’s not a huge pool of FHBs who can afford 700-800k.

So we are still coming back to the key issue - prices are too high.

I think cuts to interest rates will lift effective demand, but not hugely. There will need to relaxation of lvr’s to see more meaningful change. If FHBs can buy with a 10% deposit at a mortgage rate of 2% then I think we will see prices push up in that 700-800k range. But a lift in the median may be cancelled out by further drops in house prices in the $1 million - $2 million range.

Agree that come what may, Economy Cycle has to run it's course so has to fall to bottom out before starting the upward trend, again.

All efforts though needed will only lead to more blood.

Wait and Watch.

Also just because FHBers can borrow enough to buy a house in the $700-$800k range, it doesn’t mean they will. The ability for FHBers to borrow x amount will not necessarily prop house prices up.

Potential FHBers can just sit tight until the right price comes along, carry on doing what they’re already doing. Somebody who needs to sell on the other hand.....

I know a family who is going to Europe for 4 weeks in 2 weeks time

... we're heading back there next year ... couldn't give a toss about the exchange rate , business sentiment or anything else...

Just pack the passport, clean gummy undies.... AND GOOOOOOOO !

What about your carbon offset; unfortunately voluntary??

https://www.airnewzealand.co.nz/loyaltymodule/form/carbon-emissions-off…

The answer is quite simple. The government needs to spend more. But with a big caveat.

No more wasteful spending please. Focus on the spending that addresses several issues at once. Probably the best example of this would be to ramp up the house building programme. As per the original policy intent, Kiwibuild should be about the GOVERNMENT building affordable homes.

If done en masse in the right locations this will:

- create lots of employment

- stabilise the housing market

- address the housing crisis

- bolster spending in the economy.

- support public transport, making government investment into PT a better investment

No, not kiwibuild. Housing nz rentals.

Housing Nz, too, yes. But why not Kiwibuild? At least with Kiwibuild they can get an immediate return on their investment when they sell.

If govt builds them they don’t need to make profit. In which case delivering 3 bedroom townhouses in Auckland for 650k becomes realistic. They could also do leasehold under Kiwibuild too, and sell 3 bed townhouses for circa 450-500k

"If govt builds them they don’t need to make profit."

I'm fine if they break even, but i'm not going to support selling them at a loss. Yet another bunch of subsidies to distort the market, and make winners out of some, and prop up developers profit margins and once again leave the poorest segment of the community screwed over in favour of those that have wealthy parents to give them a deposit.

Agree

If the Govt is undercutting normal developers who do need to sell at a profit, why would normal developers even invest their capital and build them? If there is a significant difference in price FHB will simply sit waiting for a Kiwibuild, and developers will have no buyers. However, as the current Kiwibuild scheme sits, the Govt is buying houses off developers at above market prices, which is why they failed to sell in the first place.

Let's hope they come up with something substantial on Wednesday

Is that when the ‘reset’ is announced? Will be interesting...

Yup, if they stick to the date

There's rumors that there might also be an OSM announcement

Pardon my ignorance, what is OSM?

OffSiteManufacturing

And about bloody time. They should be cranking that up big time. The government is the only entity that builds enough housing in a small country like NZ to be able to drive this.

Labour's future hopes could depend quite strongly on this announcement. They've taken their time, so hopefully they have used it wisely to come up with a coherent and achievable plan.

Absolutely agree.. it was one of their biggest election promises..

This could be the quickest way in the current environment to get money into the economy.. there has been a lot of ground work, time for action..

OSM = one square meal , a Kiwi company concocting snack bars and mini meals ...

Yes that was what I equate OSM too as well Gummy! One of my favourites, given I am often on the run and unable to sit down for a proper lunch!

... yes .. and this has been my refrain for 20 years .. the country needs lots of innovation, small start ups ... OSM's , Kapitis , A2's , Lewis Road Creamery , Kaikoura Cheese Factory .... we need many many more of them...

Instead ... we got one Fonterrible ... 80 % dominance of the dairy market... no innovation , no creativity ... just lots of million $ salaries for the boys at HQ , and $ billions of failed investments .. and they closed the unique Kaikoura Cheesery ...

SIGH !

mmmm food and .... good wine :) NZ does these things so well.

Apparently we have the world's number one supplier of sea anchors in New Zealand too.

For the immediate fix that Orr is looking for, the only solution is helicoptering money, by way of cheque sent to each citizen/permanent resident, or direct credit to their bank a/c, say $1500 each. I am sure most of that will be spent very quickly. The Aussies did it, The Yanks did it, why not he Kiwis too ?

Getting money back into the economy, in simple terms, cannot be sustained by printing money anymore than it is viable by subsidies, such as the power hand out. But you can get money into the hands of consumers by the way of tax cuts. The much maligned President Harding made that effective. Anybody else agree?

In the case of the US I don’t think it really worked as planned.

https://www.thebalance.com/bush-economic-stimulus-package-3305782

“Tax rebate checks are not an efficient way to stimulate the economy.”

Well it did avert a looming slump which was highly undesirable given overhang of WW1 in particular. These were permanent tax cuts, not rebates. Both Presidents Coolidge& Hoover continued with it. Then of course 1929 undid everything. And indeed some historians claim that these measures contributed to that, but equally it is argued that the great depression was unavoidable.

Demand deficit solution is not to do things again which boost asset prices whilst bottom half get further behind. Debt is not alternative to higher pay

This is my complaint about the OCR cut, I don’t see how it helps.

If we all borrow to consume that is just a sugar rush that digs the long terms hole deeper. Has anyone considered that one of the reasons our economy is so stodgy is perhaps that we are all so indebted and housing costs are so high (forcing frantic deposit saving at the other end) that nobody has the disposable income to stimulate the economy?

Arguably borrowing to fund capital expenditure would be more helpful, houses, factories and motorways, but the problem with that theory is the economy is already at capacity. We can’t build any more stuff without generating unhelpful inflation in the inputs to those processes.

So I defer to the reserve bank in that their models show this stimulus is needed 18 months out but I don’t believe this will help. We are overleveraged and addicted to debt. This change will only make us more dependent and make the future reckoning more severe.

More dependency is not a flaw, it is an objective. Government in general, big business and especially banks all like well behaved dependents who know their place. We scrabble about borrowing more, trying to escape.

In all honesty there is a far bigger scope of factors at play in our little economy than I think a single article on this site can address.

Chief amoung my list would be the underlying failure across 40 years of consecutive neoliberal economic policy from both political parties. They failed to establish an industrialised, high tech manufacturing sector with which to boost the country's gdp and everything that flows from it. Infact, every economic crisis that has affected this country sees more policy put in place that simply panders to the entrenched easy money makers propping up our increasingly frail economy. A good example would be signing away water rights and ignoring runoff issues so that dairy farming could expand unsustainably instead of investing in, for example, a nationwide natural gas reticulation network that could improve productivity and reduce pollution in our industrial and residential sectors. Its derivatives could even become a high value export!

I believe it was Labour in at the time that just let F&P whiteware manufacturing walk away from New Zealand. We have never had the right focus on developing a number of large high tech companies in New Zealand. When you factor in the population increase, we have really been going backwards for a very long time.

I was in the manufacturing sector at the time. F&P plus countless left NZ or simply surrendered as china started getting its manufacturing momentum up after joining the WTO. In my view it was disinvestment and poor leadership by owners of capital that led to most of those closures. They could have modernized and carried on but chose not too. Case in point, the F&P factories were really old and despite having government subsidies right up till they left NZ the owners had maintained a relatively undersophisticated assembly line. The factory they opened in Mexico, was I believe, brand new and highly automated in comparison. The operation I was involved in made and exported native timber furniture but was so poorly led by the executive team and investors that they couldn't move fast enough in response to the changing market. The chinese product was coming in for sure but a better run LOCAL competitor took their market share and seeing the writing on the wall, I left 6 months before the doors closed.

Depressing.

Vs. for example Sistema who managed to export goods manufactured here out to markets across the globe, despite the oft-repeated refrain that we're too far from all these markets to be able to do such manufacturing.

I thought his decision to circulate "comments" in the aftermath of his visit to the high-power Jackson Hole talkfest involving the creme de la creme of central bankers in the US over last weekend was unexpected and noteworthy.

LOL: -

Curiously short on star power, the Jackson Hole gathering this year has already taken an odd turn. It’s been practically subversive. Usually when the Kansas City Fed gets together for these things each and every August, the main attraction is the top central bankers in the major economies. Outside of the Bank of England’s Mark Carney, this year there’s only Fed Chairman Jay Powell. Link

Surely the question you should be asking is not whether I want to purchase New Zealand assets , but whether you should be holding NZD denominated assets. In simple USD pricing , the median Auckland home has fallen 19 percent peaking in March 2017. August 2019 monthly close NZD/USD at ten year low ( Roger needs to change tack), against JPY 7 year low, CAD and CHF 4 year low. With current OCR settings we no longer differentiate ourselves. If a housing market is all we have, and unfortunately the past two decades bear testament to that economic path, what will happen to the NZD if the ( Auckland ) housing market cannot reignite.

Just in case, gold is at recent record high prices in NZD terms - graphic evidence.

Monetary stimulus does not work and the theory supporting it is nonsense.

- It creates bubbles

- It disrupts the market’s pricing mechanisms, distorting risk pricing.

- It will ultimately weaken financial institutions, and so reduce lending.

- It directs funds toward unproductive investments, so productivity growth collapses.

The economy is going to be killed by this bizarre theory.

Perversely, the RBNZ lowers interest rates intending to lift optimism to invest, but it actually signals major difficulties and troubles ahead.

Another metaphor comes to mind..One act Pony. Housing in the case of Aotearoa.

Its going to be a very interesting election next year if our economy hits rock bottom, which at present looks to be perfect timing for an official global recession. One could have argued it would have been the COL's to loose but the opposition are going to have all the ammunition they need if the current lot cannot turn it around. No point blaming National either, it will not be enough to get re-elected.

Agree. If the economy continues to weaken it could be a very close election.

In my opinion, the government should have initiated more fiscal stimulus this year. If they are keeping it up their sleeve for the election then I think there is a big danger they have left it too late.

I recon that Labour will come out guns blazing with the soon to be released 2018 census statistics to drive National back in to the hold they dug themselves in to by doing nothing to stop foreign buyers. The problem is that markets need to re-balance and that's not going to happen overnight considering the amount of damage that was done.

Plus there's the global market shakeup that's currently being caused by Mr Trump. Agreed Labour need to be a bit more proactive in helping to grab opportunities, such as taking up market share where the Americans have locked themselves out.

Here's an example; NZ Wine Industry could step in more to fill the gab left by the US tariff ware for the Chinese markets which apparently is huge.

BBC article: https://www.bbc.com/news/av/world-us-canada-48454123/how-the-us-china-t…

National will have all the ammunition? If they do, it is not the govt they should be aiming it at.

It will not be surprising for me to see National criticising Labour for problems that National themselves created or carefully nurtured.

Gold Reminds Governments That They're Still Not In Control

It is the debt itself which has become gold. It’s a hard concept to grasp, I know, but that’s what’s behind what otherwise appears to be a hard and irreconcilable contradiction.

Though repurchase agreements had been in practice since the time of Keynes and Edison, it was only later that what we now call repo-[tab4] would take its primary monetary form. At its center is a form of liquid gold, highly-prized collateral that is bandied about as if it was money itself. To put it simply, a bank’s liabilities can best be managed by its stock of collateral. Elasticity has today almost nothing to do with currency as it was once known.

The greater this perception to hoard collateral, the more valuable the utility of ownership becomes. That simply means, as always, when a currency is inelastic its price can rise sharply as demand for it surges. In this case, since the money or currency is UST collateral, the rising price is perversely denoted by falling interest rates.

The low and even negative yields are effectively the expense of this new form of money reflected in the opportunity cost lost by being forced to hold more of the best collateral. In that way, it shares the same driving agency as with modern gold.

As interest rates on UST’s and the like fall, that’s the banking system paying more for these money-like reserves while at the same time it reduces the opportunity cost of hedging via gold. And both for the same reasons; a monetary shortage brings with it all the dangers investors seek to avoid by holding gold.

{kind=link}

'Come on and spend!' In regards to NZ property, that's a "Nope we're not investing"! Not on your Nelly until property prices re-balance and fall to wage earner levels. After almost ten years of the blatant money laundering/ foreign buying facilitated by the National Government, particularly for Auckland. There's no way any Property Investor would take the risk of buying in a still heavily over bloated and distorted market, even with low interest rates. Remember market distortion has also effected the region areas too!

Many people I know up till 2017 were dying to buy a second/ investment property( They already had a family home/one house) but now even with low interest low rate and house value dropping slightly (Better values for buying than what they were willing to pay earlier) are not interested in buying.

Because earlier, everyone wanted to make fast buck as everyone around them were making heaps even news headline ( Headlines like House earning more than wages of $2000 per week) were motivating them to buy asap as had the fear of missing out but NOT any more as they know thatthey have already missed the bus (last boom) and now price may or may not fall ( most probably will fall) but one thing is clear that are not going up in near future.

Also not many in power admit but know all that happened was because of money Laundering - NZ was safe heaven and what better place to park the unofficial unaccounted money than in property.

For few who do not understand the concept why money laundering - Suppose someone had 2 million unaccounted money in China - that money had zero value as were not able to use or will be caught so besides zero value also had the fear that if caught by authorities will be behind bar for life. So they transfer the money through unofficial channel overseas and may lose 5% to 10% in the process and than once the money comes to NZ can buy property even by paying 10% to 20% more as have to park their money and ends up buying a house 20% or 30% more than the actual value of the house ( Net result they loose 20% to 30% but now 2 million that had zero value is 1.4 million offical). Side effect of all this was that the house in that area went up immediately by 20% or 30% in that area and chain reaction started (Average kiwi did not have or had that type of money but people in power or rich with vested interest were benefiting by all this speculation and we expected national leaders to stop all this - Just check how many national leaders have more than one or few proprties and how many made fortunes by selling during the peak and judge for self).

With money laundering law those activities or hype can never be recreated. House price will go up but in a rather rational manner and will still be good long term investment.

I hope you're not suggesting that the Chinese buyer of John Key's Auckland residence was laundering money; or that the ANZ affiliated buyers of his Omaha Beach bach, that was flipped some relatively few months after purchase, at a loss, was laundering money? Golly, no! Our ex-Prime Minister, or even one of his new employers, wouldn't be a party to any of that...That might trigger An Enquiry...

Were it to trigger an inquiry the terms of reference would be very carefully set to ensure a bad result could not be found.

Heard a good story the other day. Some Chinese buyers were driving around a town in regional NZ, knocking on doors of lifestyle block holders, saying they wanted to buy the owners properties. One guy answered the door, laughed, said "I'd want at least $4million" and shut the door. Next week the Chinese buyer knocked on the door and presented a cheque for $4.2m. The property was valued at $1.8m. The owner took the cheque, and promptly retired.

After almost ten years of the blatant money laundering/ foreign buying facilitated by the National Government,

Wrong. "Facilitated" by govts (would have been no different under Labour) and institutional support. Capital inflows into NZ are not about National and JK (even though they're not going to address the negative implications of the phenomenon). This has not been peculiar to NZ, but the impacts may have been greater in places such as Auckland.

Reality is that govts like asset bubbles like the world has seen post-GFC. It takes the heat off them to some degree. And the reality is that housing bubbles are secondary to consumer spending. Bubbles support consumer spending for the obvious reasons. High house prices also support small businesses for caollateral. I could go on and on. National, Labour, and particularly the Aussie ruling party absolutely love bubbles.

In order to spend or invest you need something to do it with.

Yes the majority of New Zealanders are already up to the eyeballs in debt. Years now of record new car sales and people using their house as an ATM. To try and ask Kiwi's to now spend even more to get us out of a hole that spending up large got us into in the first place is great idea....not.

Do you remember back in the 80s, and even 90s, quite few people had flash European cars

... yesssss ... so funny ... many of them sold at an eye watering loss after the owners faced the reality of how unreliable those European cars were , and the extortionate price of parts ... that is , if you could locate a specialist mechanic to work on them ....

The Gummster's cheap and cheerful old Toyota Corolla just keeps on trucking , never misses a beat ...

Cannot beat a Toyota, have owned mine for over 20 years now.

Don't you think there are a lot more flash European cars on the road now than in the 80's & 90's?

... the newer European diesels are getting an impressive 65 mpg ... nevertheless , you pay $ 70 000 for one ... the Gummster's Toyota from Turners Auctions only does 41 mpg on 91 ... but the bashed up little 1.3 L bugger only cost me $ 1200 ....

There is something green about keeping old cars going; saves the ecoterrorism costs of building a new one and recycling the old one.

Just don't hit anything or do too many kays

I just got a Peugeot diesel for a steal, from a dealer and all! It is getting 60mpg once I blanked the EGR. Even fits my 9'6" surfboard inside. Reckon I won't need parts for a while as the miles are low, and if I need them it should be able to buy them online. Go the pug!

Those Q7s and other Hitlerwagons are flashing by you on double yellow lines

If OCR drops below zero that would change how a bank thinks about finance. Although mortgages will retain the same profit from interest they will suddenly be far less enthusiastic to have the principal repaid. Will they be pushing interest only mortgages? What happens in Japan? Am I missing something obvious?

Banks are not keen to get their principal repaid now either, their business is to lend (and make a margin on the lending) therefore principal repayment = less lending = less profit. The only case when banks are keen to see some principal being repaid is if they think the borrower is financially weak

Private debt in New Zealand is sky high, and houses still a ridiculous multiple of income.

The tree god can call for a reinflation of the housing bubble if he wants, but that would seem stupid from my perspective.

The government should spend a bit more and return cash to citizens in the form of a general tax cut. But this lot will probably prefer cash to special interest groups.

I think we have been stimulated to much. Money lost all it's value when they just keep printing money. We have to go back to gold standard. Just listen to Max Keizer and Stacey Herbert, not say they right but got feeling their view is bang on.

No the gold standard is not a good idea, the economics cases/examples , abd data against it are pretty compelling. "lost value"? how so? we have virtually no inflation. The entire globe's financial system is on life support of constant $ injections weighed down by too much debt and too expensive energy stop it or go to gold and we get the 2nd Great Depression, not where anyone sane wants to go.

Lower interest rates and lack of confidence in the outlook for the overvalued housing stock may finally tip the balance to more people investing more effectively.

Offshore owners of Nz equities are not the problem, but net dividend flows are - and they result from a low Nz savings rate and a widespread inability to invest in diverse assets. Banks for instance are much better to be owned by shareholders other than just NZers, and no reputable AFA would suggest an investor would confine themselves to residential property and Nz equities.

I’m thinking that’s what Orr is after - more savings which don’t automatically go into housing, but strengthen

Perhaps you can lead a flogged dead horse to water......

It all depends on what mind-bending drugs you've been taken that make that happening 'real'; like say imbibing in more QE or, worse, MMT?

To scramble a Groucho Marx metaphor "My dear, in the morning I'll be sober, but you... will still be in debt"

The problem with being the last country to go to zero is that foreigners & the carry trade have already priced up all the assets. If the NZD goes low enough though, parts of the economy like tourism and exports will fly.

Oh, what the hell, let's add another Metaphor to the ungainly beast depicted.

'You cannot push on a string'.

Elfin safety alert, but, this might be the metaphorical straw that breaks the - oh, wait, let's just stop right there....

It's rope, not string that's being put on sale. Rope to hang themselves with.

So Orr wanting us to spend borrowed money. I'd argue that too many people are simply tapped out of cash or ability to take on more debt even at 1%. Then if you understand the fear in the financial markets right now that seems to be building for a recession and probably a big one (if not even a depression) encouraging ppl to take on debt is plain awful of him.

https://www.youtube.com/watch?v=3WclYu5l4G0

Anyway I am out of debt. So congrats people you kept the game of musical chairs going long enough for me to be clear of the ball and chain, the feeling is amazing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.