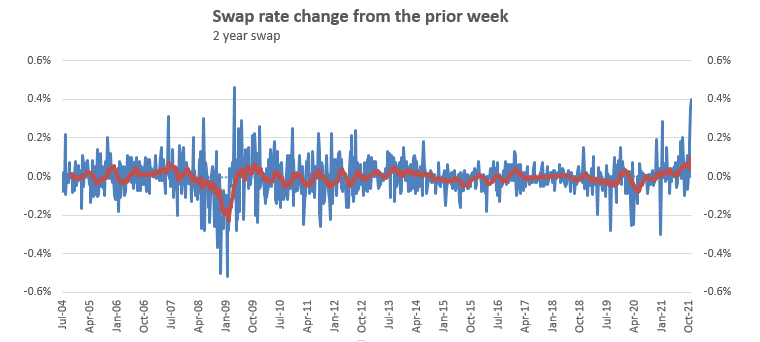

With higher than expected inflation revealed in the recent Consumers Price Index (CPI) as the catalyst, New Zealand wholesale interest rate markets are probably the most volatile they've been since 2009, Westpac senior market strategist Imre Speizer says.

As Speizer puts it, Statistics New Zealand's CPI release on October 18 "caused a kerfuffle in the market."

The CPI showed inflation rising to its highest level in more than 10 years, with the annual figure reaching 4.9% at the end of the September quarter. This was significantly higher than the 4.4% to 4.5% economists expected, and the 4.1% the Reserve Bank expected.

Off the back of this one-year and two-year NZ swap rates made their biggest one-day gains since the 1990s, rising 23 and 28 basis points respectively.

Now, market sources say that, as interest.co.nz noted late on Thursday, there's a shortage of receivers in the market who are necessary to make a deal. Without them, banks struggle to hedge their risk and if they remain exposed, the risks for bank treasurers heighten. As one market source told interest.co.nz; "It's not an easy time to manage risk."

Speizer says the higher than expected CPI meant some market speculators were caught out, having got their positions "the wrong way around." Having been burnt, these people aren't rushing back into the market.

At the same time rising interest rates overseas, notably in Australia, are rippling through to the NZ market.

Another market source describes a shortage of receivers through the short end of the yield curve out as far as three years with "woeful" liquidity. Liquidity refers to the ease with which an asset, or security, can be converted into ready cash without affecting its market price.

This source suggests some traders are in survival mode feeling battered and bruised, and isn't sure anyone knows exactly how and when the market will rectify itself.

Speizer says he doesn't recall things being as volatile since April 2009 when there was a "deluge of borrowers" wanting to fix mortgages and the market seized up. At the moment he says the market is still functioning and reckons we'll get to the point where people decide enough is enough.

"We might not be too far from that point," Speizer says.

But with home loan mortgage rates already on the rise, there's likely to be further increases.

"If swap rates rise mortgage rates will rise," Speizer says.

Nonetheless he suggests market expectations that the Official Cash Rate (OCR) could rise as high as 2.5% to 3% are overdone. The Reserve Bank last month increased the OCR for the first time in seven years, by 25 basis points to 0.50%. The OCR will next be reviewed on November 24.

In the meantime rising mortgage rates are encouraging home loan borrowers to fix before rates rise further, putting pressure on banks striving to hedge their risk in a market currently lacking liquidity, which means finding someone to take the other side of a deal may be challenging.

Daily swap rates

Select chart tabs

48 Comments

This source suggests some traders are in survival mode feeling battered and bruised, and isn't sure anyone knows exactly how and when the market will rectify itself.

This is the market rectifying itself.

Exactly. Forcing rates close to zero and funneling lots of cheap money to banks was always going to have impacts, and the current inflation and rising rates is the result.

Oh dear, tough times could be dawning for those who have got themselves donkey-deep in debt.

TTP

We can only hope. The irresponsible need to account at some point.

There'd also be the hope that some of those responsible for suppressing the risk over the last dozen years would be held to account.

Ok to much to hope.

Low tide soon

There is still plenty of room for being the deepest donkey...

Be quick.

Obviously, the bankers should be worried about this, who would buy their bonds when the sovereign is going to offer a better risk-free deal.

Banks should do some soul searching on the return-less risks they took, but they won’t as they know the game all too well. They party hard knowing that for the past 40 years reserve bank has always come in to mop up afterwards. I don't think it would be possible this time.

The concept of risk has not been understood by this generation of money managers because it has been so comforting to believe in the big central bank put. I suspect this time it would be a greater fool game, and these bonds would have to be sold off to the dumbest of the dumbs.

New Zealand is the first developed market to experience this, Canada, the UK, and Norway aren't far behind. So we don't have the luxury of leaning on their experience. I'd say it's probably the start of the end of the current credit cycle, a pivot to more naturally occurring rates rather than manufactured rates. If I may steal the phrase from 2020 - buckle up for 'unprecedented times!'

Heard nature takes its own toll.....here economy is and will take its own toll.....

What has reserve bank done till now.....in garb of helping have printed and supplied cheap and easy money...If this is the solution why not keep printing and supplying to solve problem as this what like of Orr's have been doing.

What do you mean the RBNZ doesn't control interest rates?

RBNZ can only control rates temporarily, as long as the market believes in their narrative. Anyway NZ debt market is functioning quite well, we're moving toward a more naturally occurring rates environment. But we're a drop in the bucket when you look globally.

The fact is NZ is offering better returns than some of the equally safe debts of the world, and that has put a self-correcting brake on the NZ rate lift-off, but think of the time when rates lift in the bigger and better economies, our bonds would drop and rates would lift off quite a bit.

The banks will cry, as there could be some serious mark-to-market losses in coming quarters

The fact is NZ is offering better returns than some of the equally safe debts of the world

What? NZD has been a 'risk on' currency for as long as I can remember. To think any otherwise is delusional and not attentive to history, particularly the GFC.

I'm talking about the attractiveness and safety of debt, not the FX play. The point is about the safety of principal and coupons

The comparison made here is with other AAA-rated and comparable sovereigns

I'm talking about the attractiveness and safety of debt, not the FX play

You look at debt markets and FX independently? Why?

Not shedding any tears for the rates traders.

If they are even remotely competent they should be doing well.

Another market source describes a shortage of receivers through the short end of the yield curve out as far as three years with "woeful" liquidity. Liquidity refers to the ease with which an asset, or security, can be converted into ready cash without affecting its market price.

The fixed-rate payer receives floating interest, and is said to be long or to have "bought" the swap. The long side has conceptually purchased a floating-rate note (because he receives floating interest) and issued a coupon bond (because he pays out fixed interest at periodic intervals). On the other hand, the floating-rate payer is said to be short or to have "sold" the swap. The short side has conceptually purchased a coupon bond (because he receives fixed interest) and issued a floating-rate note (because he or she pays floating interest).

The principal or notional amount is never physically exchanged (hence the term 'off-balance sheet') but is used merely to calculate the interest payments.

So an IR swap is an agreement between to parties to exchange a stream of cash flows calculated as a percentage of a notional sum calculated on different bases.

Liquidity in this case means lack of market maker commitment to engage balance sheet capacity to execute the price making function. If balance sheet capacity (the real money in the system, therefore liquidity) is systemically impaired, as in a crisis, or a crisis that doesn’t really end, then to get dealers to give up their precious balance sheet capacity and engage on the other side of a swap someone would have to pay a hefty premium to make it worth it (risk-adjusted) for the dealer to do so.

Audaxes... I know very little about swaps etc.

Do you think that the decline in term deposits from $190 billion in 2019 to $153 billion , has played a part in the volatility in the swap mkt.

https://www.rbnz.govt.nz/statistics/s40-banks-liabilities-deposits-by-s…

Im thinking Banks have been relying more on the swap mkt to fix their borrowing term.. ( 1-3 yrs ? ), since they have lost almost $40 billion in fixed term borrowing , in the retail mkt.

If so... then this is a consequence of the RBNZ financial repression strategy..?

Audaxes... I know very little about swaps etc.

Same here- but I know the basics because my trading desk live priced semi annual bond equivalent.synthetic swaps using 3mth futures strips (eurodollar FRA stacks) out to four years. (many years ago)

I think the IR swap market is to exchange fixed to floating in respect of mortgage payment types (floating vs fixed) This asset class has largely grown in a one way trajectory.

Bank liabilities (so called deposits) have to match outstanding mortgage $values until the borrowers extinguish that liability. Deposit terms are irrelevant because bank deposits (records of what banks owe) cannot be cashed out except for tiny amounts of legal tender.

New Zealand-incorporated registered banks are also subject to a minimum core funding ratio (CFR). The basic notion underlying the CFR is a comparison between an estimate of the funding of the bank that is stable and can be assumed to stay in place for at least one year (‘core funding'), and the core lending business of the bank that needs to be funded on a continuing basis. Core funding is defined as retail deposits plus wholesale funding with maturity of more than one year.

Is COVID-19 real? Absolutely.

Is it any worse than H1N1 - Swine Flu? We'll never know. We've handled it differently.

And part of that 'handling it differently' has been to create and disseminate tens of trillion of dollars, Yen, Euro , Yuan and NZ$ debt into The System; a System that was in strife before Covis-19 hit. And one way or another, that debt is going to haunt a System that was already overextended before the current virus.

For those that saw the virus as an opportunity to 'inflate the debt away'; inflate asset values, and so the price of everything, to create more wage demand, to pay off the existing debt, the problem is - The Existing Debt to be paid off hasn't remained static. Massive New Debt has combined with huge 'old debt' and we are right back to where this all started - a System in strife - except now - it's even bigger; even worse.

I understand that the RBNZ is 'just doing as it's told' as part of a wider Central Banking effort to use "Inflation!" as a heart starter, but at what stage do they have the courage to look after wellbeing New Zealanders instead of going over the debt-falls with everyone else? We know the answer. Sadly, at no stage. We are all too far gone, and 'they', and probably we, know it.

"Is it any worse than H1N1 - Swine Flu? We'll never know. We've handled it differently."

We have put an awful lot more effort into fighting Covid, and it has so far killed 5 million vs swine flu's 284K (and swine flu has now been around for five times as long as Covid). I think one could safely suggest Covid is worse.

But what if we hadn't put that effort in? Would it still have been 5 million dead? We don't know. We can assume; that's all.

The point I'm trying to make isn't medical, but economic.

What we do know is that the World now has something like $300 trillion of debt; untold tens of trillion of dollars worth more than we had before, much courtesy of 'fighting the virus' in all of it's supposedly well-intentioned guises. Whatever financial 'vaccine' some very frightened global regulatory think is going to magic that away is unlikely to be "let's do lots more of what already failed so miserably"

(NB: If what 'they' had done, works, then why is Global Productivity on the precipice of contraction - again?)

You aren't doing your argument any favours by doubting if covid is worse than other flu's. Of course it is, just look at any of the mortality statistics and R numbers for both.

This has nothing to do with covid, as it could have been any of 100 different black swan events that exposed the massive debt build up that was never addressed during the GFC. It is true that the "economic stimulus" is just all part of the financialization of the economy and transferring increasing amounts of wealth into the hands of a very small minority, but that has nothing to do with covid.

You could be right! But my intention was to highlight 'what we are told' as opposed to 'what might be' Anyway. I come from a time when Pox-Parties were still a thing :) ( NB: I, and all of my wider family, are double Covid vaxed)

"So are pox parties a good idea? That’s hard to know. Whether you prefer to vaccinate or prefer the naturally gained immunity there are risks involved. As a parent it's difficult know which is the best course of action to take. Many parents are now opting for the varicella vaccine because it’s promoted as a safer option and it solves the issue of taking time off of work to look after sick children. However there is little data to show that vaccine gained immunity for the Varicella vaccine lasts for a significant period of time, with immunity levels decreasing even after the first year and no consistent figures on immunity after 5 years or more. This raises questions about people having immunity in their formative years but becoming at risk of infection when they are more vulnerable in their adult years. Choosing the vaccine may put you at risk later on, unless you remember to take regular booster shots."

Worse? Depends on the measure really. I'd much rather catch Covid than any of the other flus prevalent over the last decade.

Of course it is worse. Nz has been insulated from its effects, resulting in some crazy opinions on it and questioning how bad it really is. It would overwhelm any health system is it was let to rip. Nz will have many deaths next year even though 60% plus of the total population will be vaccinated.

And if we get 100% of New Zealander vaccinated, and it still rips though, then what?

The point I am trying to make is that in the grand scheme of 'Never let a good crisis go to waste!" the monetary luminaries of the World haven't.

Covid has been a God-send for them; it gave them an opportunity to try to 'do a 70s' and blame "Covid!".

Let's hope for all of our sake that, just like vaccinating 100% of us, it works. Because just like the medical vaccination, if it doesn't.....(possible answer: Mortgage rates at 25% pa, here we come!?)

Of course its bad, I don't think anyone argues this. I think the point though is that our particular response, is out of proportion.

2 deaths in this current outbreak at a cost of what 5 billion? (someone will correct me). That's not logical. Particuarly when the average age of deaths from ''letting it rip'' would be 80+

Letting it rip is not the option either (obviously), though all that does is just decreases health system effectiveness, not overwhelm it. Its not like it ceases to exist. Health systems still function, they just need to triage more and results are less effective.

Its possible that we could have gone for (still go for) some middle road, where borders are open, face to face transactions still occur, kiwk business dont need to rely on monopoly money and we just live in a moderately restricted environment.

Our current approach (zero deaths ever!) cannot go on forever. That is unless you want to live in lvl3 & with massive inflation for the rest of your life.

Its a shit burger either way. Time for a stiff upper lip.

This is what I pretty much posted in other thread...

I guess we live in a global economy and are not immune from big boys playing god... It's disappointing RBNZ didn't try to temper the flood sooner.

Time to float?

Wait for the double dip.

I have no sympathy for the 'traders' or 'macro economists'. When mediocrity meets ignorance, this is what you get.

They were sleeping on the wheel when inflation data started surprising in June, when bounceback in the economy was better than expected, when LSAP was terminated, when RBNZ said that the trajectory of rates is up?

Failure to read data is 'gross incompetence' in my books

Especially if data reading is someone's job.

Add 'arrogance' to mediocrity and ignorance.

"It's not an easy time to manage risk."

Those who do not understand risk in its true nature cannot control it. Whoever you're quoting here needs to forget about liquidity, they should hold on to maturity.

It is in nature of these traders they think they'd always be able to sell an instrument, sometimes you can't and perhaps we're entering the stage in the market when the excess liquidity might remain trapped in these bonds, indirectly removing the excess liquidity problem we have!

"If swap rates rise mortgage rates will rise," Speizer says.

That's what I call scaremongering. A trader doesn't need to worry about mortgage rates, there are other institutions who have a full-time job monitoring and controlling all that

Yet the statement is fairly self evident, is it not?

What risk?

Central banks have destroyed risk.

The central banks now seem to have assumed the responsibility of making money for the market. Apparently, there has not been any serious scrutiny of their role, but there should be, so next time when there is a serious crisis, the property market does not go through the roof!

I think RBNZ is probably doing fine in comparison to some of its peers - but that is not to say they're innocent

Plenty of short-end liquidity in the form of deposits looking for a half decent return. I'm just waiting for a reasonable deal...

Short end in this context is 2yr-3yr. History shows that retail deposits don't go longer than a year no matter how attractive the rate being offered. I'm talking some banks have <1% of total deposits that are >1yr.

You’ve got (smart) investors looking to ditch their TINA faves for safety, you may be surprised at how many would be enticed by a decent 2 year rate. Maturing just in time to mop up the blood spilled by a falling knife.

Volatility and a lack of liquidity in the wholesale markets aren't all doom and groom.

On a positive note, this is pay day for smaller private lenders and shadow banks.

Parents would be wise to provide their children with the liquidity required to seize pockets of golden opportunities in an uncertain market.

The payoff could well exceed any risk premium implied by the general wholesale. Family wealth aren't built based on wholesale markets.

Be quick.

Yeah.... how to send a whole family broke,.... dad, son and daughter

Why be concerned when Orr has assured that he will solve everything by distributing money - feel rich till ......

Not to worry about Inflation nor fundamental as has managed to convert economy into housing ponzi and will support till his last breadth with support of empathy Queen, who having taste power will too not let it go easily and will use every manipulation.

The realisation that defaults are a very real option hits home...better late than never(or not).

Tony Alexander was calling for people to fix long months ago. Smart guy. Lock it in and smash the principal. 5 years at 2.85 was like winning lotto... and so many people turned it down because they wanted to get the powerball too.

He has a very good track record. I remember his advice around January was : not sure what’s going to happen and nearly every economist over the last two years had been wrong. So locking in a very low rate of say 2.99% for five years is a great way of controlling the uncertainty.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.