Inflation expectations are likely to fall still further over the next year, making it even harder for the Reserve Bank in its "uphill battle" to generate a sustained lift in inflation, according to Westpac economists.

In a paper titled: 'I've fallen and I can't get up: Another look at inflation expectations' Westpac senior economist Satish Ranchhod says evidence of a downshift in inflation expectations can be seen "over a range of measures".

"And this isn’t just a response to the recent softness in oil prices. Expectations for inflation over the next few years have also fallen."

The paper updates an earlier one from Ranchhod in May last year and follows just two days after fellow Westpac senior economist Michael Gordon put out a paper closely examining the Reserve Bank's own measure of 'core inflation' and which concludes that it will be "difficult for the RBNZ to return core inflation to around 2% on a sustained basis, which is a strong argument for keeping the [Official Cash Rate] low".

The Westpac economists were first among the big four banks (subsequently joined by ASB) to state that they believed the Reserve Bank would be forced to drop the OCR to 2% this year. It's currently at 2.5%.

RBNZ Governor Graeme Wheeler, in a February 3 speech, said the central bank would continue to draw on the flexibility contained in the Policy Targets Agreement between Wheeler and Finance Minister Bill English in managing economic risks and assessing monetary policy. The Bank would avoid taking a "mechanistic approach" to interpreting the PTA.

And in a comment contained in the media release, but not in the published version of the speech itself, Wheeler said: "Some commentators see a low headline inflation number and immediately advocate interest rate cuts."

Subsequent to those remarks, a sharp fall in the two-year-ahead inflation expectation figure measured by the RBNZ's own survey has led to sharply divergent views among economists.

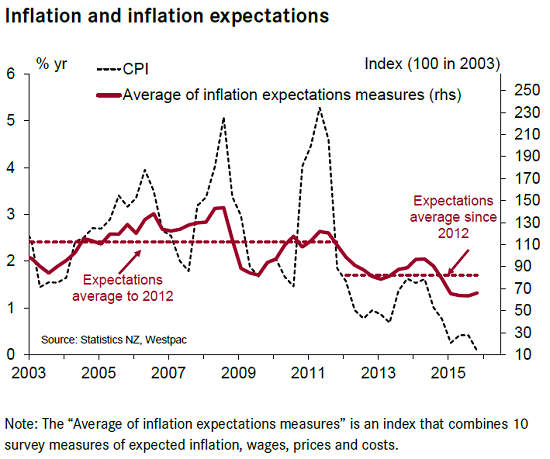

Westpac's Ranchhod said that Inflation expectations are a significant influence on wage and price setting decisions, and as a result play an important role in determining actual inflation. Looking across some of the main approaches to measuring inflation expectations, he said, three things stand out:

"First, there has been a marked downshift in inflation expectations.

"Second, this downshift does not simply reflect recent falls in oil prices and the related weakness in the near-term inflation outlook. Inflation expectations have been trending down for several years, including measures of longer term expectations.

"Third, this downshift has become more pronounced over the past year.

"The downshift in inflation expectations will be a major concern to the RBNZ, making the uphill battle they have been fighting to generate a sustained lift in inflation that much harder."

Ranchhod said against a back drop of persistently low inflation, if expectations had remained consistent with the inflation target, then the RBNZ could have taken a gradual approach when trying to get inflation back to 2%.

"However, measures of inflation expectations actually paint a more worrying picture. Across a range of measures and horizons, we have seen a downshift in inflation expectations. Some of the most reliable measures (including the RBNZ’s own medium-term two year ahead measure) are now well below 2%.

"This means there’s a real risk that inflation expectations are deviating from the inflation target. And given the continuing softness in inflation and likely downturn in growth further ahead, this downshift could become even more pronounced over the coming year."

Ranchhod said inflation expectations have been falling since 2012 – well before the recent oil-related weakness in inflation.

"This corresponds with an extended period of generalised softness in New Zealand inflation. It also corresponds with the start of Governor Wheeler’s tenure when there was a tightening of the Policy Targets Agreement to include an explicit focus on the 2% midpoint of the target range for inflation. However, as shown [in the graph below] the downshift in expectations in recent years appears to have gone beyond just bringing inflation expectations back to the target mid-point.

Furthermore, Ranchhod says, downward pressure on inflation expectations is likely to continue for some time yet.

"We’re forecasting annual inflation to linger close to 0% this year. On top of this, over 2017 and 2018 (i.e. the longer term horizons which are the key focus for the RBNZ) growth is set to slow as reconstruction in Canterbury eases back, and the current boom in migration dissipates. This slowdown in growth will compound the RBNZ’s difficulties in returning inflation to target."

Ranchhod says there are signs that the softness in inflation expectations is passing through to conditions in the economy more generally. Over the past year business expectations for wage growth over the next one to two years ahead have fallen back to the levels seen during the financial crisis. "This could exacerbate the current softness in inflation."

And Ranchhod says the downshift in inflation expectations is also evident in financial markets pricing.

"Such measures are unlikely to be affected by temporary volatility in inflation due to their very long term focus (over ten years). Consequently, they are often viewed as an indication of the credibility of the inflation target."

Financial market expectations for inflation over the coming years have been trending down, and are now at very low levels, he says.

26 Comments

Financial market expectations for inflation over the coming years have been trending down, and are now at very low levels, he says.

Exactly, hence financial risks have elevated sharply - few of the indebted can liquidate their debt without the crutch of inflation. Foreign wholesale lenders recognised as much and hiked funding costs by one third year on year according to Kiwibank executive Paul Brock.

I get it. If you buy a house in AKL, with inflation at %7 in 10 odd years it's doubled in value and everyone is happy, except the silly old bugger who sold it to you. Get no inflation the house is the same value, minus some maintenance, a new roof some rates,insurance and general wear and tear. You have been working your butt of to meet the payments, what the hell for?

Suddenly it looks like a terrible investment but it could have been worse you could have bought a farm, or it could be worth less than you paid for it.

...hmmm, you may want to reconsider your understanding of inflation or be more careful with your usage of the term.

Inflation does not necessarily imply capital/real gain.

If, as you say (arbitrarily), AKL housing inflation is at 7% p.a, there is only a real economic (personal welfare) gain if your effective cost of capital and outright costs average out to lower than that figure. In the case that your cost of capital is higher, that 'silly old bugger' who sold you the house may have indeed realised a better real gain than you.

That is exactly the risk when you buy with capital gain expectations. There has been plenty of advice out there explaining the risk, but some choose to ignore it.

I don't understand why the RBNZ is such a reluctant OCR cutter

My theory is that they fully understand the hellishness that's coming and want to have something left in the tank.

It won't make a difference though. Do you really think dropping the OCR from 2.5 to 0 will spark any kind of recovery if it all goes horribly wrong again?

Yeah, I think it will Jimbo, a "recovery" in Auckland house prices to levels similar to Sydney where global hedge funds are currently debating the best way to short the Australian housing market that they describe as "the biggest housing bubble in history". Always good to join a party isn't it ?

house prices going up is not "growth" and is not what the RBNZ needs. a 0 or less inflation rate means that the RBNZ is willing to provide funds to the retail bank to stimulate growth. To take this step it will need to define how that money is used, when ordinarily it probably wouldn't have had to, but houses are too far out of step with the rest of the economy. Commercial loans from banks usually start somewhere north of 8 - 10% as banks factor in their risk (might be a little dated), which is a fairly steep price. But for the RBNZ to achieve what it needs to, then it has got to be prepared to make sure that money is available for a lot less, and to accept some higher risks, knowing that some will default. The question is how much are they prepared to pay?

The question is what should the money be used for? Buying houses does not create jobs or money movement in the economy, but building them will. Manufacturing and other businesses that create jobs and pay wages and causes the money to flow out into the economy is what is needed. the problem is how to achieve this? There are plenty of rules and regulations that get in the road too.

So shorting the banks? whose shares look to be currently dieing on their feet?

NZ must be on their radar as well, the ratios are close to as insane as OZ.

not really....it needs to go down now.

Smalltown

What's in the tank is water I'm afraid; what we need is something (not water) between the ears.

Dropping interest rates has proven to be risky (inflates house prices and share markets artificially) and it does not encourage the money to be invested in productivity (although that is the theory). What is needed is structural change and more disincentives to property speculation.(Why a brightline test of 2 years, why any limitation on years, a good speculator/investor has a longer time frame)

Because low interest rates destroy capital, just ask the Japanese.

https://housingjapan.com/2011/11/10/a-history-of-tokyo-real-estate-pric…

I am beginning to wonder if this so called necessity for positive inflation is just to suit the ever increasing bank profits and the so called investors who simply want to farm inflation as opposed to adding something creative.

The imperative that inflation remains positive means that productivity improvements that result in lower prices must be offset by price increases elsewhere. Housing and capital assets appear to be one of the sectors where the price increases are directed. This seems to be having the effect of being very good for the banks and supper wealthy investors. In other words all of this seems to be channelling the benefits of increased productivity into the pockets of the super wealthy while holding back or diminishing the position of the bulk of the population. The following link illustrates how something like this has been going on for three and a half decades.

http://www.nytimes.com/imagepages/2011/09/04/opinion/04reich-graphic.ht…

Would a prolonged period of deflation be a good thing and redress the lopsided sharing of wealth.

There is something wrong with this inflation target management, how it reacts to productivity driven price falls, the distribution of wealth and how the banks operate. We need a long term careful think about what is going on and how it needs to be changed.

thats a great link chris-M...

My understanding is that nominal GDP growth needs to be higher than nominal interest rates in order for deleveraging to occur..... OR... If there is no deleveraging, then simply a continuation of the last 40 yrs of "creditism"...( GDP growth generated thru credit growth..) So..yeah... it suits the current " system"

That link shows how it is wages which have been and are lagging..... and because of this, metrics like house price/income ratios have become, somewhat, meaningless in regards to determining whether house prices are overvalued...

Global FX reserves have gone from $1.3 trillion in 1993 to over $12 trillion in 2015. ( almost 1000% in 20 yrs )

Currency debasement has been rampant... because of that the full benefits of productivity gains don't lead to an increase in the average persons standard of living ( I think Keynes expected that we would be all working only 30 hr week and enjoying life , by now )

Central Banks response to any kind of liquidity issues has been "money printing".. ( metaphor )..

I'd make 5 points:

1/ productivity gains get captured in land values.....

2/ Fiat money debasement transfers wealth.

3/ PAYE tax is a very inequitable form of tax .

4/ Globalization.... Global Capital Flows.... wage rate arbitrage..etc

5/ Credit...One persons spending becomes another persons income... ie.. credit is a very important function in the supply/demand equation... ( especially so in regards to the locational value of Land , which has a fixed supply )

Those 5 things have contributed to what u mention and to the article you link too.

For me ... the irony is that it might well be inflation that brings the house of cards down... ( If workers start getting decent wages rises and general prices start rising.... Central Banks will be between a rock and a hard place ).

This is Just my own view on things..

Floating mortgage rates have stayed high at around the 6% mark since 2009 despite OCR cuts, so no deflation there.

This a very good observation MortgageBelt.

The big Aussie banks are gouging us big-time.

NZ sold out NZ-owned banks, BNZ and ASB, to the Aussies after Rogernomics. Both Labour and National are guilty of flogging off NZ - silverware.

Governments in NZ have mostly been too lazy to govern; and it has been getting worse under National ( think AirNZ and power companies ). If there's effort involved to turn some institution or government entity around then the easiest path is to flog it off for peanuts. Tell me a NZ-richest who didn't get his start by swilling at this trough.

This is why we need someone like Trump. A true leader

Uh no, he's not. He's only after looking after himself.

The world is still trying to dig itself out of the hole created when the yanks last elected a moron for a President. Trump will be another W and that is really scary!

Actually I think Trump would be considerably worse! hmmm....though less honest and more corrupt, anti-science, anti-democractic, anti-poor, racist and sexist is hard to imagine.

:/

why? because he wants to kick 11million "mexicans" out? he's just a racist bigot.

David, the headline of your article is just wrong: the RBNZ has not been fighting any battle let alone an 'uphill-battle' against anything to do with inflation !

Its had an uphill battle to remain credible in face of the data and state of our economy!

All the bankers and Hedge funds are desperately hoping for inflation.

WHY

Simple explanation

They want to inflate your pension funds away. That is the only way they can hide their ponzie scheme.

With inflation

You get $1 million from your pension fund

Real value after inflation $100k

With deflation

You get $100k

Real value after deflation $200k

Read the W'pac article.Having done so,I can't help but wonder how it is that someone as far down the ladder as me,a mere financial foot-soldier,figured this out ages ago. In late 2014,I wrote a piece on "Why the Reserve Bank is Fighting the last War" . It is obvious to me that low inflation rates represent a profound structural change and our RB is well behind the curve.

Go and look at long-term inflation graphs for NZ, OZ, UK and USA and you will find the same overall picture.Inflation has been declining for over 25 YEARS,not of course linearly,but the trend is clear. Why? Globalisation,technology,the decline of union power,increasing inequality and,it must be said,the role of central banks in inflation targeting.

Our OCR will move lower and should be done aggressively to get the exchange rate lower,BUT,at the same time,accompanied by a more hard-hitting approach to the property market. the Bank/government could prevent overseas investors from buying existing properties,prevent the banks from lending on investment properties,introduce stamp duty, penalise developers for land-banking etc.

We should also amend the RB's mandate and find a new governor!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.