By David Hargreaves

Reserve Bank Governor Adrian Orr now says the next official interest rate move will not be till 2020 - after earlier forecasting it would be next year.

Orr is still saying the next move could be either up or down.

The Kiwi dollar dropped after the 'dovish' announcement from the Governor, from about US67.5 just before the announcement to 67.1c shortly after. Then it continued to slide during Thursday to well under 67c.

As expected, the Official Cash Rate was left unchanged on Thursday at 1.75%, where it has now been since October 2016.

The bank's latest Monetary Policy Statement indicates that the timing of the next move in the OCR has been shifted by a whole year since the last MPS in May.

The first forecast rise in the OCR is now forecast to occur in September 2020, compared with September 2019 in the last statement.

CPI inflation is now tipped to be somewhat stronger through the rest of this year, while GDP growth is forecast to be somewhat slower.

However, the bank's GDP forecasts for next year are rather stronger than those in the May MPS and are pointing to 0.9% quarterly increases after the first quarter of 2019 and through the rest of the year.

Given recent low business confidence figures and indications of future activity, the RBNZ's forecasts for growing GDP next year are likely to be seen as surprising and may strike some credibility problems in a market that is seeing slowing GDP growth ahead.

Orr concedes that "risks remain" to the bank's central forecast.

"The recent moderation in growth could last longer. Low business confidence can affect employment and investment decisions.

"Conversely, there is a chance that inflation could increase faster if cost pressures can pass through into higher prices and impact inflation expectations."

This is Orr's statement:

The Official Cash Rate (OCR) remains at 1.75 percent. We expect to keep the OCR at this level through 2019 and into 2020, longer than we projected in our May Statement. The direction of our next OCR move could be up or down.

While recent economic growth has moderated, we expect it to pick up pace over the rest of this year and be maintained through 2019.

Robust global growth and a lower New Zealand dollar exchange rate will support export earnings. At home, capacity and labour constraints promote business investment, supported by low interest rates. Government spending and investment is also set to rise, while residential construction and household spending remain solid.

The labour market has tightened over the past year and employment is roughly around its maximum sustainable level. We expect the unemployment rate to decline modestly from its current level.

There are welcome early signs of core inflation rising. Inflation will increase towards 2 percent over the projection period as capacity pressures bite. This path may be bumpy however, with one-off price changes from global oil prices, a lower exchange rate, and announced petrol excise tax rises expected. We will look through this volatility as appropriate, and only respond to any persistent movements in inflation.

Risks remain to our central forecast. The recent moderation in growth could last longer. Low business confidence can affect employment and investment decisions. Conversely, there is a chance that inflation could increase faster if cost pressures can pass through into higher prices and impact inflation expectations.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

73 Comments

“The Man” stated that interest rates for mortgages wouldn’t be hitting 6% again a year or two ago despite all these people on interest.co and economists saying they were going to go to 9%.

If you want to get ahead financially you need to take accurate advice from people that have been very successful financially.

You can listen to the Dooom and Gloom merchants on here but you should not follow their advice.

The property bulls on here are generally positive people who have taken control of their lives financially and therefore you should be taking more notice of their words of wisdom rather than the negative property bears.

I don't recall seeing anyone on here saying that Interest Rates would hit 9%. Anyone can make up their own set of facts in attempt to strengthen one's narrative.

There were many that were stating that the floating rate for mortgages was going to 9% a couple of years ago.

The Man said that they wouldn’t ever see 6% again and it certainly looks like that is the way it is going to be.

Of course things can change and there is a possibility that they could go over 6% and if that is the case there will be A lot of carnage but I seriously doubt it.

But the floating rate for mortgages is currently around 6%. If there were many making this claim then you'd be able to cite a couple of sources?

The floating rate for any one with sense is about 5.2%. The rate most investors will be paying will be about 4.2% on various fixed terms.

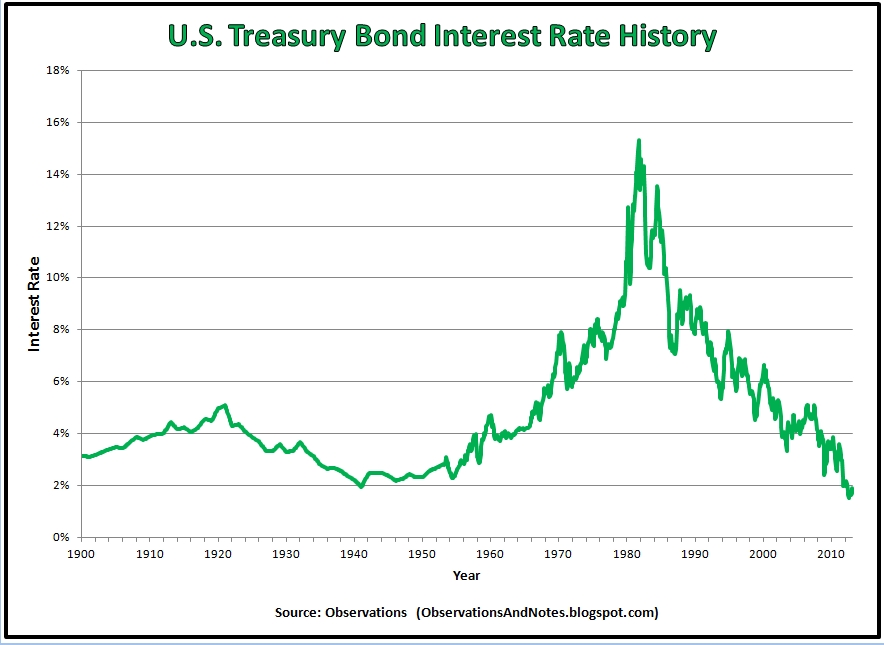

I dont know if anyone specifically said 9% but lots of people use the term 'normalise' implying a return to rates pre 2008 which would be about 9%.

A host of comments have referred to rates rising off the back of things like US inflation and for years now people have been calling rate rises as imminent with reference to international funding costs or the reserve bank wanting to shore up risks.

The statement from the reserve is an enormous rebuke to the armchair non-investors that infect this board and a huge validation to some of the investors who have been making statements for over a year that rates would likely persist at reasonably flat levels and the market would likely prove resilient.

Not all bears have been making such strong comments but a sub set has been persistently incorrect now for years, with some been wrong for over 5 years. Outrageous calls like 50% drops or rates returning to pre-2008 levels circulate on these boards frequently with claims of eminent enormous corrections on the scale of Ireland, Spain, Greece or parts of the United States.

Post of the week, hands down.

Fair call thanks for replying, I forget my tenure on this site is less than a year so I don’t have as good a gauge on this. I’ll have to look up a few of Houses Overpriced’s comments over the last 7 years.

I've never made the call myself that a big crash is coming. I think most people are aware central banks are spinning QE out as long as possible. Interesting though, that sentence at the end of your post...

"...claims of eminent corrections on the scale of Ireland, Spain, Greece or parts of the United States."

While I haven't called a crash definitely coming, it's another thing entirely to say that what's happened in so many other housing markets with massive price growth and a seeming disconnect from local fundamentals could never, ever happen in New Zealand.

That's a big call.

As Australia is experiencing, mortgage rates are not being determined by the Reserve Bank but by the cost of overseas borrowing, which is rising. So while the RBA/RBNZ keep rates on hold, or even cut them, the cost of mortgages will still rise.

I would have to broadly agree with your statement .. educated positive minded people tend to do much better in life. It's far too easy to read to the negative comments on here and not act as it supports your underlying fear of whatever you goal is, where it be property or other vehicles of investment.

Well said, I would add that it is much easier to criticise others than to take action oneself, therefore I would add the latter (minority) group to your people who do better in life.

Leaving rates low is a telling sign of what is yet to come. They don't want to be raising rates into the storm and offshore forces may even push up our rates a bit higher anyway.

I doubt we would see them return to 9% levels though so whoever spoke about that on here was way off the mark. 6% rates would still have quite a significant impact on a lot of people though as so many people are leveraged to the eyeballs with debt in NZ. Household debt is at record levels and our household savings are now in negative territory.

Many property bulls try to stay upbeat on here because the last thing they want is for their property values to drop. So many people with invested interests in the market always talking things up, even in the face of a lot of local and global risk.

I was bullish for a lot of years when I knew there was growth potential. Now the risks are high and I am a lot more bearish in the short to medium term.

Watch this space as there is a lot of turbulence ahead. Those that can't see it coming are living in a dreamland of blind optimism.

I remember before the last GFC when so many property bulls were talking things up.

Adam, agree with most of your sentiments.

However, property bulls do very well when the market is slow as the opportunities are abundant and it is generally when the financially comfortable bulls make their money.

Turbulence ahead for the slecuvestors and not the professional property investors.

Always plenty of renters around and interest rates affordable and positive returns on property purchased right!

Agree. That's what we are positioned for but wont be buying for a while as there is a lot of downside to come.

Adam, from your last comment I understand that you own some property, given your own bearish outlook, are you looking at selling some?

Cheers

Already sold...

...nice timing! ;-)

I'm out too. Uncle John's exit was the signal that should have alerted everyone that the game was up, albeit I sold up a couple of months before he did.

Could have been better timing if I had of gone with my instincts back when the boom was still going in 2016. I was telling everyone the peak of the market was coming and 99% of people were denying it would happen and that prices would continue upward due to supply and demand. Well look at things now!

..interest rates are gonna be the least of your worries. Tightening credit, falling prices, increased costs, more rules and regs. But what the heck eh...ppty only goes up.

"The property bulls on here are generally positive people who have taken control of their lives financially..."

The delusion is strong in this one. Its called fake growth and leverage.

Interest rates are going lower and lower to deliver more of your financially successful growth. Real money is continually losing its buying power...

If you understood the drivers, it should worry you.

Which means you dont.

ham n eggs

I agree with you.

As a long term property investor and member of the association I used to chuckle at the profiles featured in the PI magazine (especially 2000 to 2010).

There was always featured stories of investors doing great things. Sadly within a year these successes were bust.

Any man and his dog couldn't help but fail to do well over the past decade. However, in the changes in the market suggest that blood rushes and a sense of invincibility being expressed are both naive and very foolhardy.

I think that yields under 5% on current values (less all those expenses and all that risk and work) without increasing house prices suggest conditions are very much unlike those of the past decade.

ham n eggs,

Your posts intrigue me and when you write,"if you understood the drivers',i assume you are referring at least in part,to the cost of energy.

i would love you to spell out your vision for say,the next 5/10 years in the energy and financial markets.

In other news, I put $100 on red at the casino and it came up red, which makes me an investment expert, don't listen to those doom and gloom merchants that say otherwise.

It was only a few weeks ago that the blood sucking Vampire Squid (Goldmans) were pushing their early 19 first RBNZ hike call. Thankfully I was here to call BS on that

pump and dump. Their clients will already have exited their NZ dollar positions.. In fact Goldman has such confidence in NZ that their NZ operations have been moved to Australia. Except for 2 members of staff in Auckland and the cleaning lady.

Squid's macro calls are surprisingly bad. They will have left NZ because the funnel isn't sucking enough blood to warrant being here. The first sign of any state asset sales and they will be back

"The Man"

Your response to the OCR announcement seems overly full of exuberance.

Me thinks that there is a great, great sense of relief on your part which could be typically expected from someone heavily mortgaged.

I am one who said for some time that there was upside risk to an increase in mortgage rates; however, I have only ever talked about 1 to 2% increase being significant (and crippling to many) and like other respondents I don't recall anyone mentioning 9%.

I am pleased at the OCR announcement especially for recent FHB that there is a stable outlook.

However, the OCR is only one factor in determining mortgage interest rates. In a global economy experiencing uncertainties there is a likelihood that banks will find funding costs are higher as risk goes on.

I again restate my view that those with large mortgages should not be complacent. A 1.5% increase on a $500,000 mortgage is $7500 p.a or $288 a fortnight (after tax). I suggest that this could stretch many with large mortgages - especially those who may find themselves on one income rather than two when they purchased.

This is especially of concern for those on interest only payments as there is no surety that this facility will continue especially in a flat housing market with some possibility of downside. Lenders will want to be protecting themselves in such conditions.

So if one is heavily mortgaged, some relief for today, but not a time to start feeling complacent.

TM2

Keen to understand your thoughts on this.....What impact do you believe a lower NZ dollar will have on bank interest and lending rates in New Zealand?

TM2,

If you want to get ahead financially you need to take accurate advice from people that have been very successful financially.

in my experience,really successful people don't boast about it. Those who do like you,are often very insecure and not nearly as successful as they want you to believe. That said,i think you may well be right that interest rates will remain lower for longer than some assume.

I wrote a piece on this over 4 years ago in which I said;"but I am strongly suggesting that it will remain very subdued by historical standards.I have a quote here from Shamubeel Eaqub in Aug.'16 to the effect that interest rates would be low for decades to come.

Lots of ppl have stated interest rates are going no where for years myself included, nothing special in seeing that one, but our reasons almost certainly odnt line up.

Classical mistake some make, just because someone made a profit historically does not mean they will do so projecting out into the future.

Funny thing but people like me who said a stagnant global economy and interest rate for years where described as the doomsters and gloomsters , now it seems the ppl expecting 7%+ are.

weird.

TM2, "Next move as either up or down" - Right now, several plausible downside/upside inflation scenarios exist that are simply beyond our control.

(Rates upside), a return to the 70s hyperinflation where property failed to keep pace with inflation and in real terms fell big time. Mortgage rates rise putting further pressure on the 10% of speculators who hold 40% of the debt.

(Rates downside) - another GFC, property prices fall.

Right now, property valuations are riding on stretched fundamentals. Whether one is a bull or a bear, doesn't alter fate.

Agree. Only one this is for sure, policy from any Govt in NZ will have nada to do with the outcome as we are but an ant under the global elephant of finance. If said elephant changes direction and you have bet the farm in the opposite direction, you are flatter than a possum on a state highway.

Bulls, still waiting for you to confirm your loading up on property debt until your ears are bleeding. Anything else is just comes across as Real Estate Agent like pom pom cheer squad.

Im still bearish BTW. Math's is broken and two many external factors were promoted under the last govt to pump the NZ market.

"You can listen to the Dooom and Gloom merchants on here but you should not follow their advice.

The property bulls on here are generally positive people who have taken control of their lives financially and therefore you should be taking more notice of their words of wisdom rather than the negative property bears."

Congratulations you have proven his point yet again.

Ha-ha-ha-ha :)

I forecast for 2019 that inflation will be above 2% but GDP growth will be sluggish at under 2%. This will leave the RBNZ with a tough choice: prioritise inflation and hike the OCR or prioritise business activity and employment and leave the OCR as is

.....more stringent bank lending along with Inflation has already strangling one of NZ's largest growth engines - the Construction sector. Stagnant house prices are already affecting consumer spending too.

In the absence of a global shock, are we about to experience a prolonged episode of Stagflation?

Note that the NZ and Aussie sharemarkets have soared today.

Orr's announcement might also spark some renewed interest in the housing market. It's good news for the tide of young people intent on purchasing their first home. (-:

Term deposits become an even bleaker prospect. )-;

TTP

TTP, you seem a little aggrieved about others having term deposits at this juncture. Why? If it's such a bad medium term investment choice, why are you so tichy about it? Auckland based FHB's are witnessing falling house prices and therefore, the upfront value of their house deposits are increasing. Why do you have a problem with FHB's waiting on the sidelines? In your Feb 2017 forecast, you were actively encouraging buyers to wait and argued it as common sense :)

RP, not sure you understand what stagflation is.

"Stagflation, a situation where the inflation rate is high, the economic growth rate slows and unemployment stays steadily high" Wikipedia

NZ inflation has been persistently low, so has unemployment...

Hi Yvil,

Re your comments on stagflation (above) you are absolutely correct.

TTP

Yvil, you say "I forecast for 2019 that inflation will be above 2% but GDP growth will be sluggish at under 2%" youvé just forecasted stagflation - right?

Are you sure you know what stagflation is? Checking Wikipedia to reassure yourself?

Just quoted Wikipedia to educate you

I would've said that they would prioritize price stability but now that the RB has a mandate to manage unemployment, it would seem it could go either way.

I agree; current upward pressures in prices from falling NZD and inflation resurgence in China won't lead to higher CPI for NZ until early-to-mid next year.

Expect China to continue exporting inflation as producer prices continue to trend up at around 4.5% and tariffs on fuel and raw materials from the US start to push input prices even higher.

Looks like BNZ's Stephen Toplis has an answer my question above:

"The question going into it [the MPS] was would the Governor be more concerned about the weakening growth indicators or would he be more bothered by the upward trend in both core and headline inflation? The answer is now there for all to see - weak growth won the day. Inflation forecasts were, on balance, little changed but this was not enough to prevent the RBNZ lowering its interest rate track," said Toplis

"The scenario analysis in the MPS also reveals the [Reserve] Bank’s dovish biases. Under the Bank’s higher inflation scenario it raises the cash rate by 50 basis points more than its central scenario. However, was growth to surprise on the downside, the door is open to a 100 basis point cut."

The Fed is signalling 2 more hikes this year and 4 next year. Can we really be in a position where the US interest rates are more than 1% higher than ours? Interesting times ahead.

If there were 6 hikes in FED rate then they'd be closer to 2% higher than ours.. so in answer if that happens, no.

The message that I'd take from Mr Orr today is that he is postponing execution as long as he can to buy a bit of time for households to get their finances in order. What I would also suggest is that when they do rise they will go faster and higher. 12-18 months to get the sails tied to the mast so it can brave the storm.

Weaker dollar and inflation on the way before then.

Just because the OCR is unchanged does not mean the banks interest rates wont change !!!

Yes.

True. Thanks to ours low net savings, banks will continue to fund a portion of our debt from overseas money markets. Also, as growth slows, households will be forced to deleverage and banks will be forced to cut down on risky lending.

So CPI is the metric you look at when you’ve got house price hyperinflation, but when house prices look like they’re going sideways then it’s easy money time. Looks like a one way ratcheting mechanism to me. Interest rates are in exponential decay.

{kind=link}

fat pat, you say

"So CPI is the metric you look at when you’ve got house price hyperinflation"

House prices are not included in the CPI

Yvil, exactly. If house price inflation runs far higher than core CPI rate, this must surely signal they're out of kilter with historic fundamentals. It presents strong argument they'll underperform core CPI rate for some time into the future.

Hi Retired-Poppy,

Please note that, historically, house price changes have not tracked closely with the CPI - or producer price indices (PPI).

There has been no strong correlation.

Your argument that house prices will underperform the CPI "for some time in the future" is mere (uninformed) conjecture.

TTP

......feeling less peeved now you've offloaded your myopic interpretation?

Ouch, not liking people setting you right RP?

Yvil, TTP, happy to admit fault were it exists :) lately, it seems you hang on every word I say. Should I feel a little creeped out or flattered? Pick one.

seems like 4.19% is pretty much the norm for 1 yr fixed with the major banks. Do folk see this dropping much more given RBNZ dovish mood?

ASB just posted record profits due to high margins. So if our banks were actually competitive, it should drop. So probably not.

Small drops yes, not because of the RBNZ but because the banks will trim their margins to get more business

Forward guidance is part of the job of a governor and also to not spook the masses. Adrian is doing a good job on both. It's too early for any cash rate movement at this stage and business confidence needs the certainty that the RBNZ isn't going to go fiddling until necessary. Lots can change in a short space of time though as we know with NZ history and if the world decides that our dollar isn't worth supporting at such low rates then that will influence policy again. Up rather than down is the next move and my guess would be earlier than 2020 without stepping on the toes of Mr Orr.

David is the monetary statement pdf available thru your website, cannot download from RBNZ maybe gremlins and pixies my end

We'll just keep treading water and pretending that keeping our heads above the waterline is progress? What rate do we expect to enter the next recession at and what options do we have if that's before 2020?

Are these very competent people at the RBNZ asking themselves the right questions (let alone the journalists)? Here is another great summary by Michael Pettis. To me it explains the cause of the New Zealand Problem With House Prices - excess capital inflows. I have lightly edited the conclusion, substituting NZ for US:

What Can New Zealand Do?

So what are the policy implications if New Zealand is serious about reducing the current account deficit? It depends on which underlying conditions apply.

1 If foreigners export capital to New Zealand mainly to finance the New Zealand trade deficit, Wellngton must implement policies that force up the domestic savings rate if it wants to reduce the trade deficit.

2 But if foreigners export capital to New Zealand mainly to dispose of their excess domestic savings, Wellington must implement policies that make it harder for foreigners to dump excess savings in New Zealand or policies that make it easier for Kiwis to send these flows abroad. Only by reducing net foreign capital inflows will Wellington be able to drive down the trade deficit.

If I am right, then it is not the case that New Zealand runs a current account deficit because Kiwis save too little. It is the reverse: Kiwis save too little because New Zealand runs a current account deficit or because it runs a capital account surplus: foreign capital inflows automatically depress New Zealand savings.

As counterintuitive as this conclusion may seem, this is the implication of very plausible assumptions about how the world works. The reason most economists are not aware of this is simply because they have not made explicit the assumptions that underlie the models they use. Consequently, they have not recognized how changes in global markets have made their models obsolete.

https://carnegieendowment.org/chinafinancialmarkets/77009?utm_source=rs…

Er, ok, but how does that work, you ask?. Well, the crux of the issue is whether, as a nation, we spend more than we earn because:

1 We are a bunch of hopeless spendthrifts who just can’t resist bidding up house prices by bidding against each other to borrow the most money from our friendly Aussie banks, aided by the RBNZ helpfully modulating interest rates to make the repayments affordable and thereby enabling maximum indebtedness at all times (very helpful to the Aussie banks too). The mechanism being our rabid appetite for debt.

2 Capital flowing into New Zealand in excess of our needs, thus pushing up the exchange rate so our exports become less competitive and exporters' profits are reduced; the excess being force fed into household mortgages like corn down the gullet of geese being fattened for pate de foie gras, aided by the RBNZ reducing interest rates so the excess causes greater indebtedness rather than higher unemployment. The mechanism being less profits (ie savings) because the exchange rate is too high.

https://rogerwitherspoon.wordpress.com/2018/08/08/its-the-capital-inflo…

Printer8, I am not full of exhuberance because of the interest rates staying the same at all!

Fortunately we are positively geared on every property and returns on purchase prices is approx 9% on average over the whole portfolio.

As for being heavily mortgaged it depends on your own viewpoint!

Yes we will owe the Banks a lot of money in many people’s eyes if they are not used to having debt or just the one mortgage.

Our equity is a lot larger than what we owe the Banks and as I have said previously our Business Bank Manager has stated that we are his safest customer that he has, so maybe that is something to take note of.

We are extremely comfortable in what we are invested in and the fact that the Auckland housing market is in a quiet slump at the moment only validates our reason for investing in the extremely stable Christchurch market!

Each to their own and you can have money in the Bank, shares etc. but at the end of the day it is the investor that has to be comfortable with what they have invested in.

The ones that have talked negatively in regards to property for the past 10years have got more than enough egg on their faces!! !

For all you Guys who almost gloat over the fact that interest rates won’t go UP

It’s a rip off. Everyone knows that there has been transfer of wealth from savers to borrowers. Its officially known as Financial Repression. This wealth transfer has blown asset prices up.

I was taught that Rf is the risk free rate and that was typically the USA 10yr . And all govt rates used to be generally priced off this based on Country risk vs an interest rate that was considered “risk free”

With all the Central bank collusion the WORLD has been in emergency Financial Repression for 10 YEARS!

Savings are the result of thrift and the competition for that thrift was real interest rates. Think about this; if mortgage repayment P+I interest rates go up by 2.5% then some borrowers will pay 50% more on their monthly payments than they are paying today. I don’t think Orr et al can afford for that to happen that’s the real story here. Plus he’s setting Savers up for a negative rate of return. Well done Adrian

As I said it’s a rip off

What now? does this all end in deflation? is that the elephant in the room?

Deflation is when inflation falls below zero, inflation is on the rise, so no, it does not look like deflation in the foreseeable future

Banks don't need to raise rates. Anyone borrowing has to be able to service 7.5%. If they can do that the banks will lend at 4.5%. So in a way its as if the rates have already risen which makes things different to past cycles.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.