Central bank digital currencies, using an electronic record or digital token to represent the virtual form of a country's fiat currency, could offer a range of benefits, according to a research report by money management firm Bernstein.

The report argues that in an environment where more than half all payments already happen digitally, the modernisation of the global payments system is inevitable and essential for many reasons including financial inclusion, payments stability, efficiency, and monetary policy implementation.

"This becomes even more important as the blockchain technology unleashes a new wave of value creation and industries which are powered by their own native digital tokens. In the absence of a central bank digital currency, which can provide easy on-ramps to crypto, stablecoins will continue to grow. If unregulated, stablecoins pose many risks for monetary policy, anti-money laundering/ know your customer, and consumer protections," Bernstein says.

A stablecoin is a type of cryptocurrency that attempts to offer price stability and is backed by a reserve asset.

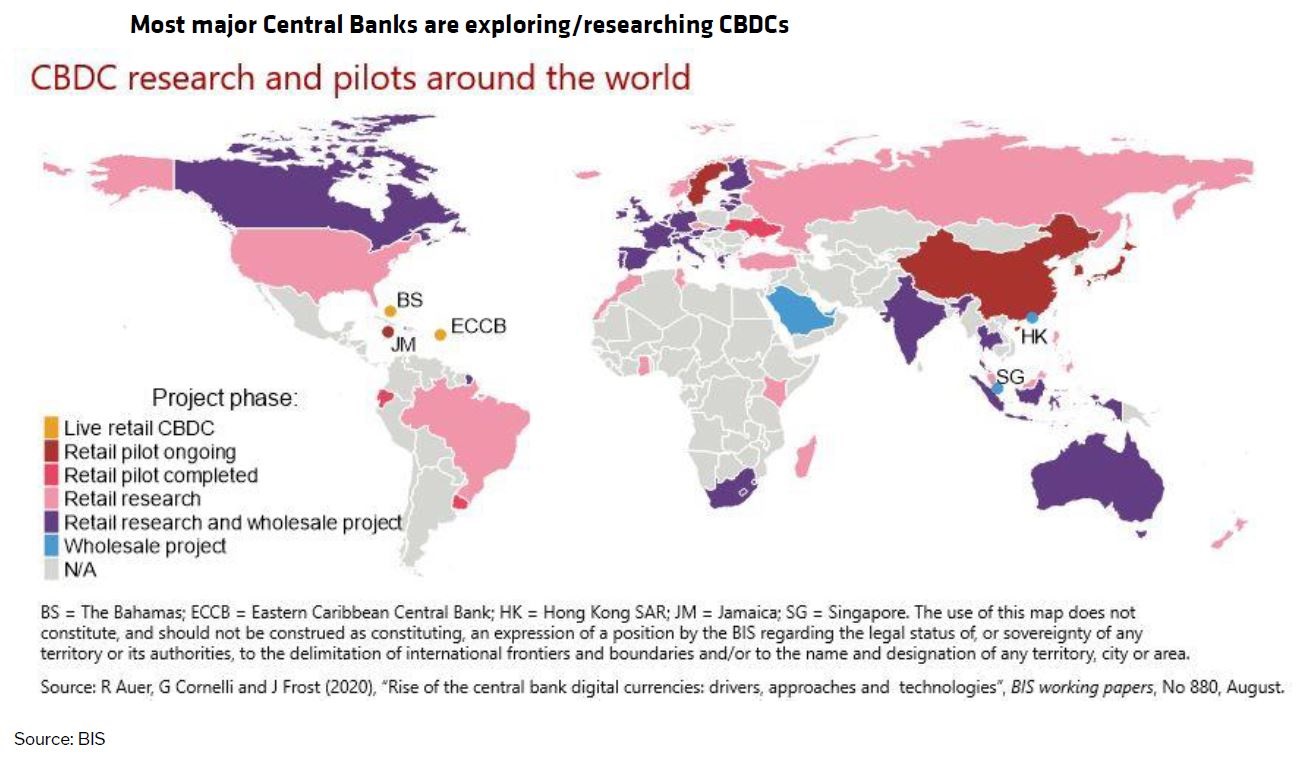

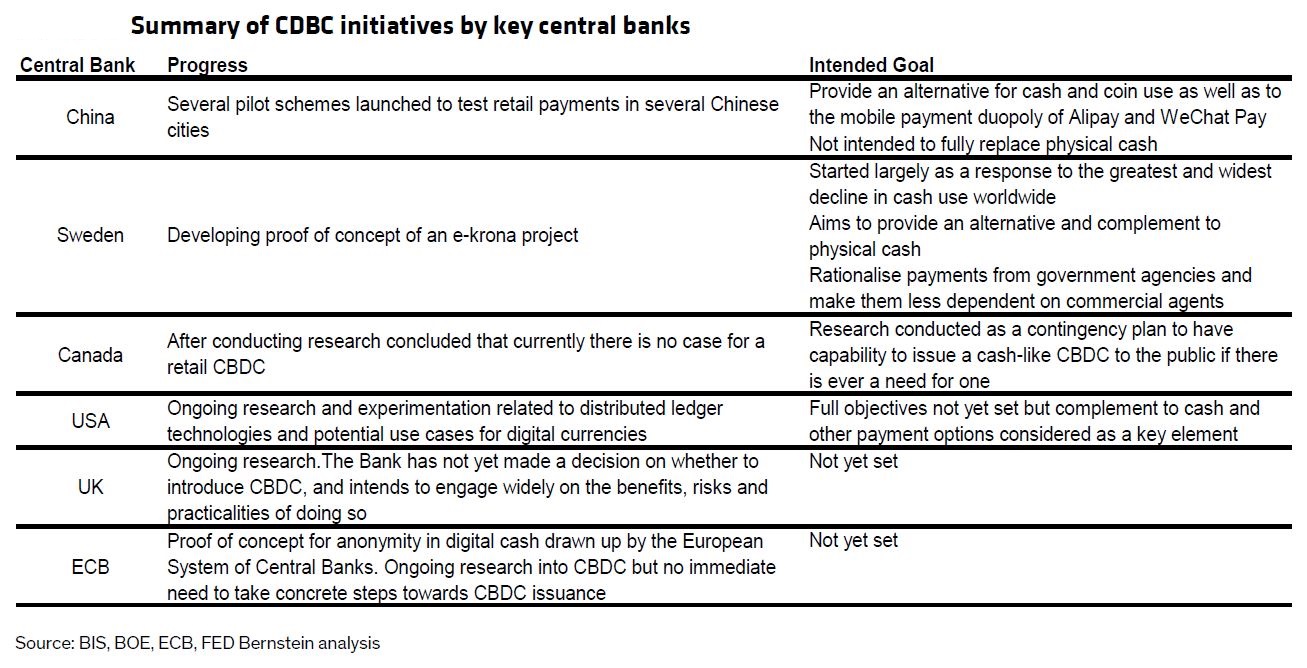

"It is not a coincidence in our view that central banks only began to take CBDCs [central bank digital currencies] seriously after Facebook announced its Libra project, which catalyzed an arms race for CBDCs. As per a Bank for International Settlements survey, over the last four years, the percentage of central banks interested in a CBDCs project increased from 65% to 86%. Only central banks in very small countries are currently not looking at CBDCs as per the survey."

Speaking at a press conference last week, Christian Hawkesby, Reserve Bank of New Zealand (RBNZ) Assistant Governor and General Manager of Economics, Financial Markets and Banking, said the RBNZ is among the central banks actively researching CBDCs.

"We have a money and cash department which is in part dedicated to thinking about things like that. So we're working on it and we're planning to say more about it through the course of this year," Hawkesby said.

Meanwhile in its report, Bernstein asks the question what can a digital currency do that a fiat currency can't? It notes that we're in an environment where most consumer-to-business, business-to-business, and bank-to-bank payments are already electronic.

"A digital currency can perform a variety of functions including:

1) Driving financial inclusion (especially in an environment with lower cash usage and lack of bank account access for everyone) – CBDCs could essentially act as a replacement for cash in the digital world,

2) Increasing efficiency through programmability features (e.g., automatic execution of certain transactions on pre-defined conditions),

3) Better implementation of monetary policy (e.g., potential to charge negative interest rate which is impossible with cash),

4) Modernization of domestic payments infrastructure which could operate on 24x7 architecture vs. fiat dollars which are tied to legacy infrastructure," says Bernstein.

In a deflationary environment CBDCs could allow central banks to impose deeply negative interest rates, Bernstein says, adding this would also require broader policy decisions such as wealth transfer from savers to borrowers.

"A second macro consideration, though one firmly in the camp of politicians rather than central bankers, is wealth taxes. A negative interest rate can be thought of, in a sense, as being a wealth tax. A post pandemic environment that is set to see starkly greater inequality is likely to see greater calls for wealth taxes. By limiting the ability to withdraw cash CBDCs could enable such wealth taxes, though we note that a negative interest rate is only a wealth tax for investors who hold very short duration assets – i.e. cash – while it potentially boosts the value of equities."

"But this brings in other policy concerns that go far beyond the narrow topic of just digital currencies. There would have to be a huge debate about what this does to the relative wealth and power of savers vs creditors. There has already been a debate about this in Germany, it would likely only intensify if CBDCs were created. Before people get too excited about the technological possibilities this policy debate needs to happen," Bernstein suggests.

In terms of cryptocurrencies, Bernstein says the launch of CBDCs could make them seem more mature and accepted. But there is also potential for a clash.

"For example, if central banks wanted to force rates deeply negative then bitcoin would become very useful as a way to shield capital from such a rate. However, it would be so useful in that it could get in the way of the implementation of monetary policy and therefore there might be a call for its use to be restricted."

Then there's geopolitics, with the dominant role of the US dollar since World War II, and "existential questions" of monetary sovereignty.

"The dollar is pre-eminent in international payments. However, the ability of the US to 'weaponise' the dollar, the pick-up in demand for gold from central banks such as China and Russia in the last decade and some of the growth of use of cryptocurrencies point to a demand for alternatives. This could force G10 [Group of 10] countries, especially the US, to pre-empt such a move, e.g. by China, and establish their own digital alternative. There could also be a more general concern here of the need to maintain monetary sovereignty in the face of competition from cryptocurrencies or foreign digital currencies," Bernstein says.

The report goes on to suggest that although modernisation of global payments infrastructure via CBDCs poses threats to almost all incumbents including the payment networks, central banks may ultimately partner with these networks to get scale, ubiquity and utility, and to avoid the cost of creating a new payments infrastructure. In terms of payments networks, Bernstein's talking about tax minimisers Visa and Mastercard, plus the likes of PayPal and Square. In fact some central banks are already working with payment networks, with Visa and Mastercard having a long history of being adroit about partnering with threats to their business.

"Mastercard recently announced a collaboration with the Central Bank of the Bahamas to instantly convert their digital currency into traditional Bahamian dollars for usage in retail payments. Both networks are proactively engaging with the governments on design considerations for the digital currencies. Visa recently published a technical paper outlining an approach for offline payments on CBDCs. Mastercard also recently launched a CBDC testing platform."

"Interestingly, both Visa and Mastercard have recently announced capabilities to settle stablecoins on their networks – a suite of capabilities and partnerships, which might come in handy if/when CBDCs are widely launched," Bernstein adds.

The report also suggests that on balance CBDCs are positive for digital wallet providers such as PayPal and Square, suggesting they will likely position themselves as CBDC retail distributors.

"If successful, this will further solidify their positioning as financial super apps, with huge implications for revenue and value per user. Being large distribution platforms of CBDCs could be a big deal for user growth, engagement, cross-sell of financial services, and reduction in legacy payment costs, which eat significantly into gross margins. In its recent investor day, PayPal said that it is looking to engage with governments on CBDCs."

Despite all the potential, Bernstein says it's possible that most CBDCs could never see the light of day, with central banks pursuing different options.

"Most central banks haven't yet decided whether they will launch CBDCs. Central banks may also simply look at improvements, e.g. on digital identity, universal access, speed, 24x7 availability, on ramps to digital markets to existing fast/real-time payment systems around the world. It is possible that many central banks may eventually choose to create a better/more stringent regulatory framework for stablecoins which, when better regulated, may help achieve similar policy goals."

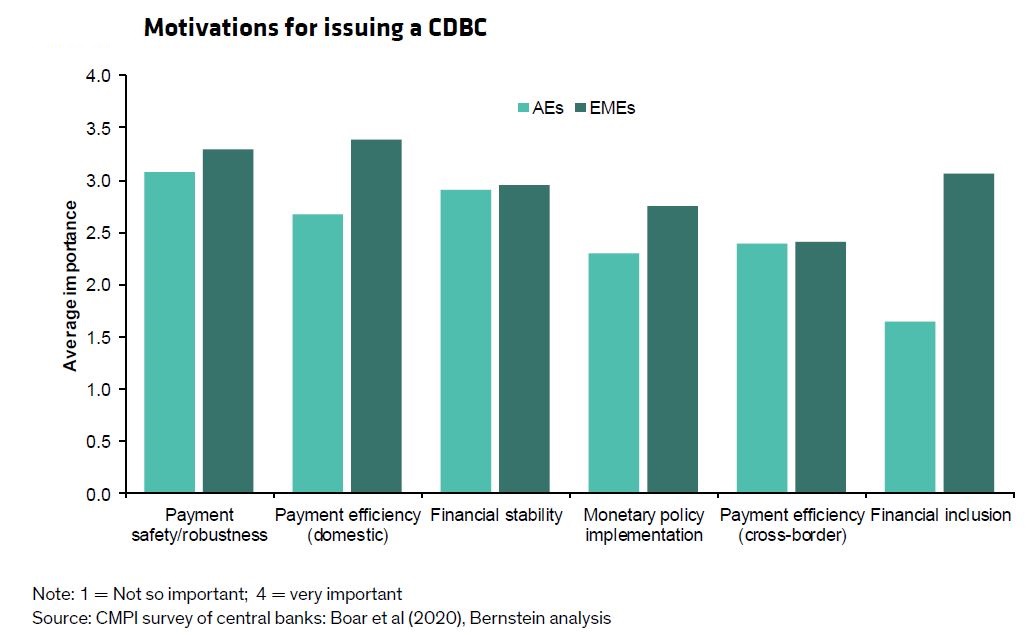

(Note, AEs stands for advanced economies, and EMEs stands for emerging market economies).

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

20 Comments

For many people, the point of digital currencies to get away from the crooks and thieves at the central banks.

And who can blame them.

Exactly my main thought after reading this.

"If unregulated, stablecoins pose many risks for monetary policy...". ie. Central Banks want to talk about improving payments and digital features that matter a bit, but the bottom line is they are the purchasing power thieves of govt, and how can they do that if the plebs escape their grasp to non-sovereign cryptos?

It’s a much easier read if you replace any mention of regulation with ‘manipulation’.

CBDC = state super surveillance technology.

CBDCs would be the end of traditional banks. Taxes will be taken directly from your central bank account. UBI/stimulus deposited directly to you. Every purchase and every transfer made being available for state scrutiny. Oh, you said something anti-government? You just got locked out of your account. No food this week, sorry, pleb. Stay in your pod and eat your remaining bugs.

Get the god damn state out of the money, please!

Exactly. And the biggest reason is negative interest rates. These will not work if one can still withdraw cash and store it under the bed.

The thieving central bankers wet dream of full control of our lives is on course.

Please do some reading on how blockchain works before posting these inane comments. Especially the part about DECENTRALISED consensus which is literally the point of the technology. It's embarrassing.

Also have your quarterly 'free' jab produced by a company that had paid 4 trillion in fines for health and safety breaches and false advertising (and bribery)

[ Please don't repost or link to conspiracy babble. We are better than that. It is only aimed at the gullible. Ed ]

OK thanks. I'm totally buying more gold.

I thought this was just a 'conspiracy theory' just like vaccine passports are/were

A currency needs faith

if the masses lose faith then its of little value

but wet dreams about democratic crypto replacing sovereign currencies are just that

there wont be a global trading platform & working supply chains unless sovereigns powers are involved

otherwise we will trade in eggs, not crypto

which is why the US$ holds it power ... the petrodollar

its backed by OIL

stuff that makes stuff, moves stuff and gets stuff done

backed by bloody big guns I would add.

indeed

its not the accent everyone is falling for

So remember how the IRD spent $1.2B on MyIR and produced a steaming pile of crap? Now apply that to blockchain development delivered by the likes of IBM. Laughable. Bitcoin will be at 0.01NZD/SAT by the time the rbnz get their act together and the big players will no longer be shelling out for junk bonds at -1% in the face of real hard money like that. As for CBDCs in general, the only utility fiat has provided in crypto markets undergoing massive price discovery is as a stable coin. As soon as something more reliable does a better job there's zero reason to use them. So best keep in mind, BTC will stabilize as it gets closer to 21M tokens minted because that will be it.

CBs are far better to regulate and create frameworks as described. Canada are onto it. The separation of currency and state will underpin the next seculum IMO. Keynesian economics is useless to describe what will happen as we move back to a standard backed by a real store of value. Better to read up on the Austrian school.

As for little old NZ, we should be doing everything in our power right now to get BTC on the government books. For just a few 10s of our printed millions, we could use our FTA with China, hire in some mining experts, import a few thousand ANT miners and really get Tiwai going as a BTC mine. If we did that, I guarantee in 10 years we'd be one of the richest countries in the world.

Further to this, CBs are far better to leave the transactional layer of currency to one of the many smart contract solutions jostling for dominance. ETH is the most established, but there's several looking promising where ETH has shortfalls right now, namely transactional cost, scalability and throughput. As we saw just days ago with the EIB testing out a bond issuance for the EU via ETH, it's far more likely IMO to see a smart contract platform become the go to for governments, where they can borrow hard money like Bitcoin from liquidity providers, who make a guaranteed rate of return. There's actually dedicated token platforms already specifically for the purpose of providing liquidity like this, AAVE being a notable example in the top 100. It's quite imaginable in this scenario for governments to raise capital directly from retail, as there's really no minimum amount someone can stake in a liquidity pool, the size of many pools is already in 100s of millions heading for billions, and the standard protocol is one of openess making a private issuance more complex. With a blockchain based smart contract in place there's zero need for custody, and settlement is baked in. That means bonds can be issued then settled without any need for wholesale settlement custody. In effect, CBs would only need to operate in a tech oriented role to issue and validate the tokens, less about monetary policy and governance, and more about code management and software delivery via blockchain based on government capital requirements. At the moment this all sounds a bit SciFi, but with blockchain it's completely within the bounds of reality. Governments are about to fear their citizens again, by way of their collective non-custodial monetary might, and be forced to be fiscally responsible and accountable. About bloody time too.

You say high transactional costs; I say security.

"Keynesian economics is useless to describe what will happen as we move back to a standard backed by a real store of value"

As mentioned before, what you are describing is UN-leverage

Which destroys wealth claims , incomes and all economies to scale

Not sure if Canada has this in mind

The holy church of BTC.

So much wrong with it I can't be bothered. But keep praying and preaching, there are believers out there - and of course you need new believers to keep a ponzi alive.

More banking inclusion... And banking exclusion if you are disagreeable to the state

"Inclusion" is a new control word brought to you by the same people at the Bank of Imternational Settlements who plan to have us "own nothing (but you will be happy)" by the arrival of 2030.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.