The Reserve Bank (RBNZ) is seeking public feedback on a central bank digital currency (CBDC) to be used by the general public, which they wouldn’t need a commercial bank account for, and it says could lead to banks and other deposit takers losing profits and liquidity.

In a new consultation paper, Digital cash in New Zealand, the RBNZ notes it has still not yet decided whether to issue a CBDC, which it's referring to as "digital cash."

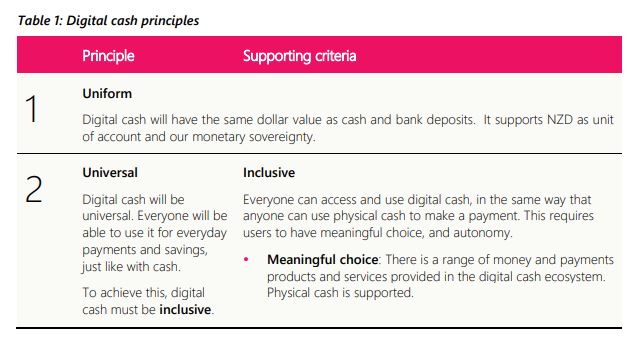

It says digital cash would be a new form of cash issued by the RBNZ to the public in addition to banknotes and coins, and the electronic money in people's bank accounts. It'd be; denominated in NZ dollars, it could be swapped 1:1 with physical cash, and other forms of NZ dollars, like money in your bank account. It'd also be private, secure, and able to be trusted, the RBNZ adds, noting "the Reserve Bank will not control how you spend your money." It'd also be "available to everyone and distributed by the private sector – but you would not need a bank account to use it."

The RBNZ is focusing on money it would offer to the public and business, not to wholesale markets. However, digital cash would be designed as a general-purpose CBDC and would be available for wholesale use, it says. Accounts would be held with intermediaries and service providers, not the RBNZ itself.

The level of digital cash issued would be driven by user demand, the RBNZ says. Demand could stem from deposits, physical cash or income growth. The RBNZ says it hasn't forecast how much digital cash people may want.

"But we can expect that if people want to use a lot of digital cash, then banks and other deposit takers will lose deposits. This could cause them to lose profits and liquidity," the RBNZ says.

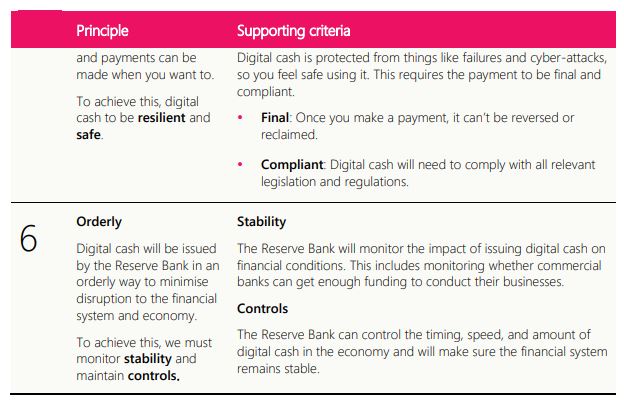

"We also need to consider the impact of issuing digital cash on wholesale funding [interest] rates [for financial institutions]. This is an important determinant for how banks would respond to fewer deposits. We will also consider whether we need to limit the amount of digital cash that people or businesses can hold. As well as what interest rate would be paid if any. We also need to test if there are any financial system stability impacts from issuing digital cash, including whether there are any transitional impacts on stability," says the RBNZ.

Preliminary scenarios of digital cash supply

It has developed preliminary scenarios of digital cash supply level, but says these scenarios aren't what it expects would happen because it has no evidence suggesting demand for digital cash would reach high levels.

However, two scenarios are modelled in the consultation paper. The first, the "high" scenario, sees $10 billion of digital cash issued. That's equal to the level of cash in circulation at the end of 2022.

"We swap cash and reserve balances to issue the digital cash. We assume digital cash doesn't earn interest and people can only hold $2000 each."

In this the scenario the RBNZ says its balance sheet stays the same size and there's minimal impact on commercial banks' deposit funding and profits.

Its "extreme" scenario sees $42 billion of digital cash issued. That's equivalent to 20% of retail deposits at the end of 2022.

"We swap cash and reserve balances to issue the digital cash. We also need to use foreign exchange operations to increase reserve balances to issue the full amount of digital cash. We assume digital cash earns a competitive interest rate [paid by the RBNZ similar to retail deposit interest rates]. We also assume that people can hold more than $2000 each by balances over $2000 do not earn any interest," the RBNZ says.

Under this scenario, commercial banks would face reduced deposit funding and profits, it says, which they could choose to respond to by getting more funding from investors, reducing lending or increasing lending rates. The RBNZ's balance sheet would become longer, as it's issuing more liabilities than before.

Innovation & competition

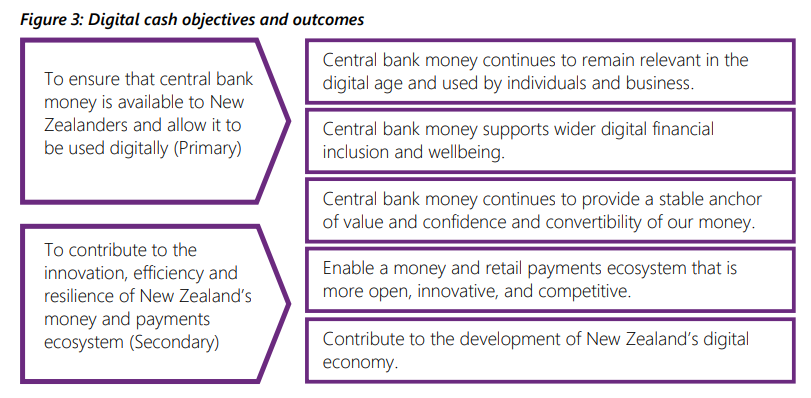

Ian Woolford, the RBNZ's Director of Money and Cash, says digital cash would ensure central bank money is available to all New Zealanders and able to be used digitally.

"It would also help enable a money and payments system that is innovative, competitive and contributes to the development of New Zealand’s digital economy. It would be the first digital form of New Zealand currency backed by the Government and available to the public. Physical cash in banknotes and coins would still be available, so people would have the option to use either digital or physical cash," he says.

"You would likely need a digital wallet, payment card or phone app to access your digital cash. You wouldn’t need a commercial bank account to use it."

"Innovations in money and payments are challenging New Zealand’s monetary sovereignty. Like crypto-assets, distributed ledgers, smart contracts, and digital currencies issued by global technology companies. New Zealand’s money must innovate to stay relevant and useful and ensure our monetary sovereignty," Woolford says.

"There is also a huge opportunity for digital cash to support competition and innovation by enabling our powerful fintech sector. Digital cash would be mainly used for payments by individuals and businesses, to pay online, instore, or even to pay your child’s pocket money in the same way you can use cash currently."

"You could use it to do new things like make an instant digital payment to anyone in New Zealand. Today, New Zealanders still cannot make instant payments electronically to other people, unless they are both with the same bank," says Woolford.

“It would also work via Bluetooth, so you could make payments without connecting to internet. This would be useful in an emergency, or when the power is out."

Many central banks overseas are also considering the introduction of a CBDC, whilst some are testing various concepts for one, and a handful have already introduced a CBDC. See more on this here.

The RBNZ previously consulted on the idea of a CBDC in 2021 as part of its Future of Money work. And in 2022 Woolford spoke on our Of Interest podcast, acknowledging the RBNZ considering launching a CBDC is in part a defensive move to protect the RBNZ's and NZ's monetary sovereignty.

Under threat

The RBNZ says the uniformity of NZ's money is being challenged by the decreasing use and availability of cash, and the emergence of new types of assets detailed by Woolford above. Additionally, CBDCs being considered by other countries could become a threat.

"If other currencies become more popular than the NZ dollar in New Zealand, then we could lose our monetary sovereignty," the RBNZ says.

"If a lot of people use them, it can pose a risk to our economy, the New Zealand dollar, and our monetary sovereignty. Monetary sovereignty is important because it means that New Zealand can independently manage its money, set interest rates, and make decisions without being overly influenced by external forces."

"We also have an opportunity to innovative central bank money. As well as to improve future efficiency and drive innovation in New Zealand’s money and payments. New Zealand’s payments landscape is dominated by a small number of large players. The barriers to entry are high and New Zealand’s payment services have become less innovative than other countries. Digital cash would help bring down barriers to entry to the payments system. Digital cash would also be a new piece of digital public infrastructure that supports digital transformation in New Zealand," the RBNZ says.

The RBNZ says digital cash wouldn't see it provide digital cash services directly to users. Rather, there'd be digital cash service providers offering digital cash services, with the public able to choose which provider to use.

"You could also change providers or use several providers depending on the services you want. These may include banks, payments companies and new providers," the RBNZ says.

"There would be a range of devices that people can use to access and make digital cash payments. The Reserve Bank would own and operate a digital cash payments platform. This platform would facilitate all digital cash payments."

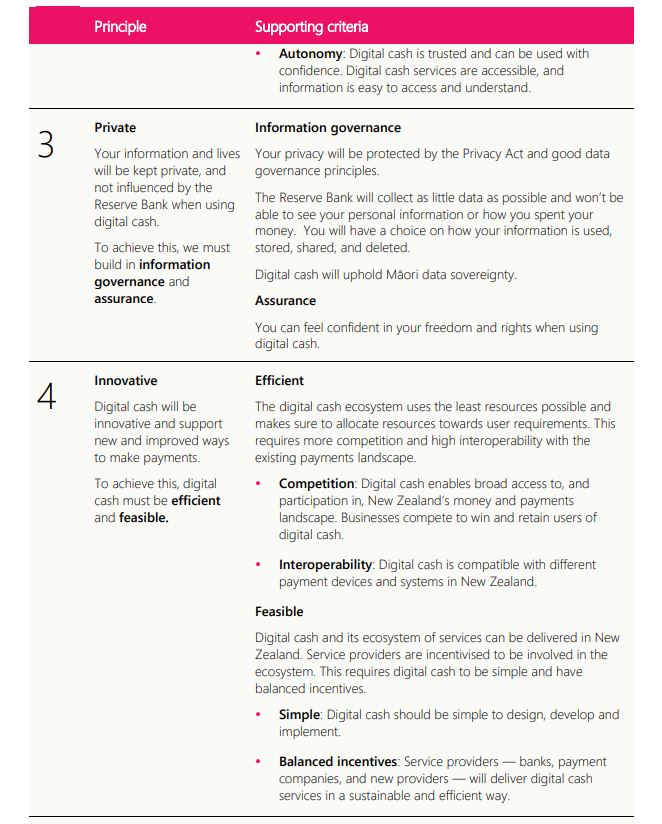

"Digital cash service providers would not be able to touch your digital cash. That means, even if a service provider failed, you would not lose your digital cash," says the RBNZ.

Digital cash payments would be available 24/7, and would be sent and received instantly. People could use digital cash to make payments without internet access by downloading their funds to a local device and use Bluetooth technology to make a transfer to another device.

"There is also the possibility that digital cash can support wholesale uses such as cross-border payments."

The RBNZ says digital cash would be private and secure, with people free to use and spend it as they want to.

"The Reserve Bank would not be able to, nor want to, place any limitations on how the digital cash can be used. The Reserve Bank will set rules on how third parties can collect, use, share and delete your information."

When might a CBDC actually be introduced?

The RBNZ argues digital money could provide new entry points to NZ’s payment landscape for new service providers by providing an open, interoperable, and safe payments platform that can be accessed by banks and other third parties to provide a wide range of digital cash services. Additionally it could improve digital financial inclusion by offering more consumer choice such as basic money and payment services and offline payments.

"We are considering a delivery approach that allows the market to deliver many different services, in the digital cash ecosystem. The Reserve Bank would provide a digital cash platform that has built-in functionality to encourage a diverse and rich ecosystem. The Reserve Bank would also set the guard rails for how the market can operate in the digital cash ecosystem. This approach prioritises open competition and a dynamic market, while ensuring the remaining digital cash principles are achieved," the RBNZ says.

"We want your feedback on our judgments and design options for digital cash. This will inform our future work on whether digital cash is right for New Zealand. Digital cash will not replace physical cash," the RBNZ says.

It's seeking submissions by July 26, and says it's undertaking "multi-stage exploration" of a CBDC until about 2030.

An RBNZ spokeswoman told interest.co.nz a decision to actually issue a CBDC would be made following discussion with and agreement from the Government. The RBNZ expects to make recommendations in 2026 on whether to proceed to the next stage, and would then develop prototypes to test how a CBDC could work in the real world, during 2028 and 2029. A CBDC could then be introduced around 2030.

"We are now sharing our latest thinking on what digital cash could look like in New Zealand. We describe what we mean by digital cash and how New Zealanders could use it. We also describe why the Reserve Bank is investigating it, and what it would bring to New Zealand. We want your feedback on our judgments and design options for digital cash. This will inform our future work on whether digital cash is right for New Zealand," the RBNZ says.

Figure 3 from the RBNZ's consultation paper, below, summarises its public policy objectives for a CBDC.

Table 1, below, sets out the outcomes a CBDC needs to meet to achieve the RBNZ's public policy objectives.

50 Comments

We're about as close as you get to a cashless society as it is. Why bother reinventing a 'digital' cash that requires third parties and service providers to hold on an individual's behalf.

By the sounds of it, you won't earn any interest. Fair enough, it's cash. But really, why bother? Just to take some deposits away from the banks?

This isn't a CBDCurrency it's a CBDCash and I don't see the point.

Exactly. Let's reinvent the wheel..

No "Its" not Cash.

It is a Programmable Finance. Think Totalitarian Control of how you spend "your" Finance.

It is disturbing how naive kiwis are to the implications for our Society.

Think: Loss of Freedom, Liberty and Justice.

Refuse, resist.

"the Reserve Bank will not control how you spend your money."

After the freedoms we lost and control the government placed on us during covid do we really believe that.

David Seymour is already talking a similar cbdc for payments to beneficiaries that could not be used for certain things like smokes or alcohol.

Once implemented and we are all on it the government can easily control what you spend your money on. Limits on fuel and energy, subscriptions, petrol vehicles.....

"David Seymour is already talking a similar cbdc for payments to beneficiaries that could not be used for certain things like smokes or alcohol." Source ?

He did in the past raise cutting benefits to those who didn't get vaccinations. What people called creating a second class of citizen, mandated, dictatorial yada yada yada.

3 years ago...ok, that explains a lot

Sounds an excellent suggestion on appropriate use of taxpayers welfare with good results from the Oz experience in the article, I hope they resurrect it into current policy

The real issue is how this controlled spending could be implemented in future. It’s only been 3-4 years since the govt restricted access to most shops etc for those unwilling to take a newly developed vaccine. Could a similar well intentioned but mis-informed set of politicians decide it was appropriate to limit the use of funds by a group of their choosing?

The consultation indicates the CBDC would run in parallel with the existing coins and bank notes. Continued use of cash would be required to ensure the RBNZ didn’t decide that cash could be ‘phased-out’ in future.

Your personal information is valuable and should be protected, and while I appreciate IRD can access your bank accounts under certain legal statutes if needed, I would much rather have an extra layer between me and government organisations for good reason. One has to consider, if this were introduced, and the public jumped into it head-first, the real question would be what would they do with all of this information? Spending habits, travel habits by means of spending location etc. Or, maybe the govt could simply focus on better regulation of the banks.

A CBDC will potentially be the biggest threat to our freedom in my lifetime.

Your freedom to dodge tax in your retail store?

Big assumption there. I mean freedom to buy what I want without potential control of my money by a government. Government already controlled my potential to earn over covid so they can potentially decide to pass any laws to control spending if a cbdc is introduced.

Be interesting to see if it drives a return to more bartering in the economy. Favours and returns.

I think it will. Societal exchanges will just go under the table. Tax free of course.

As a deterrent/ next stage of control for that, maybe facial recognition comes along to shame and divide you from associating with friends and acquaintances- just look at China for that as a real world example. Of course, we all have nothing to hide.

Makes you think, it might not have been the best idea to give the person from dirty politics power over the country's surveillance apparatus...

Agree...

But, imagine we're going off a rather large cliff and you can choose to flap your fist full of fiat, or take the cbdc hand glider...

Destination is same.

Unless you're already paying cash for everything, that freedom is already gone. Even then, with cash, the freedom is gone. Locally I can buy or sell whatever I want using whatever I want, ultimately NZD is convenient for settling tax and interest payments. There is already a digital record of all of your transactions. What freedom are you talking about here?

If all we have is a government controlled cbdc they can stop you buying whatever they want. Yoir fuel, petrol car whatever. Imagine a green labour govt with only cbdc.

I suggest you read what's written on a banknote.

So....more ticket clippers then?

I'm a fan as long as CBDC can be used anonymously in transactions (perhaps up to a given limit). I do think RBNZ are coming at this from the wrong angle though - as if, somehow, our monetary sovereignty is under threat? As long as taxes are paid in NZD, Govt spends NZD into the economy, and debts are settled in NZD, we will have sovereignty.

The bigger opportunity for me is getting $10bn per year of bank profits into the pockets of kiwis - and bringing Govt finance into the 21st century.

For example, I could swap $10,000 of cash for CBDC that is 'locked for spending' for 12 months, and when it is released from that lock it would be worth $10,550 (interest at OCR). This approach could be used for a 21st century version of 'war bonds' - allowing Govt to spend big on infrastructure while RBNZ offered higher rates of return to slow consumption (making space in the economy for the investment). Govt 'debt' would then be a mix of privately held CBDCs and Govt Bonds.

The other big opportunity, which I know RBNZ are looking at is, free payment systems to get banks of the necks of small businesses. I suspect that a lot of the CBDC publicity is actually about applying pressure there.

In an interview on RNZ this morning, the representative of the RBNZ commented - from memory - that transactions would be private but not anonymous.

Not quite sure how that tautology works, but there's too much value in the record of transactions for them to be left anonymous.

I wonder if that was what I heard. I didn't catch who the chap was who was being interviewed but one of the statements he made to justify the need for a CBDC was post Gabriel, only cash could be used to buy things. I coughed at his comments because it suggested he didn't understand the concept. Post Gabriel only cash could be spent because there was no power or internet. A CBDC is most certainly not a solution in this situation. Only cash is, and more of it!

Not a fan, not needed. But it does indicate that the RBNZ looks afraid of the banks and doesn't want to have to regulate them to take away their power.

For example, I could swap $10,000 of cash for CBDC that is 'locked for spending' for 12 months, and when it is released from that lock it would be worth $10,550 (interest at OCR). This approach could be used for a 21st century version of 'war bonds' -

OK. There's a use case. Not for me. But I would imagine that some people might find it attractive.

Can one pay a mate to sort one's plumbing with a digital cashie?

Asking for a friend.

yes just use reference "Trademe Purchase"

$850 for 'two pineapples'

Maybe it's a gift. More favours will be done, more gifts given.

Just as we currently make a whole lot of money from completely accidental capital gains we never invested for.

There's another good question here about the application of deposit guarantees and OBR: RBNZ accounts should be Govt guaranteed.

The biggie is security of personal fund accounts. "Yesterday's conspiracy theory is today's spoiler alert": after eg. Trudeau's freezing the bank accounts of striking truckers a couple of years ago, nobody has reason to trust any Govt.

1. Digital discussion goes straight to 'rules'. eg. upper limit $2K. Jfoe above talking of 'locking'. Why?

We have none of that with our physical cash now. It's great that it's entirely up to us how and what we do. Let's keep it the same.

2. I read about phone payment systems with incredible uptake in places like Kenya and Brazil. Super cheap or free.

Never figured out how they worked. Let's look at those

I mostly agree that CBDC should be genuinely equivalent of cash. The 'locking' comment was about replicating the macroeconomic benefits of term deposits (eg postponed consumption, insured savings etc).

... the RBNZ adds, noting "the Reserve Bank will not control how you spend your money."

Interesting that they thought they needed to say that....

But they will know how you spent it...

Gold to the moon

Economy grows on creation of money via loan creation. What are they going to replace that mechanism with when banks cannot make deposit profits?

Deposit profits? Banks pay money on deposits. The profit they make is that the interest they collect is higher than that they pay. The concern for the population is the high amount of deposits sitting in cheque accounts for daily transactions. This is essentially a free liability for the banks, who can balance those deposits with interest paying assets. CBDC would constrain that, banks would need to fight for deposits by paying (dun, dun, dunnnnnnnnn) higher interest.

Everyday we use and trust the money which the banks create as credit, and why is that? Because it is convertible into the governments own currency on demand and even the banks themselves will only accept payments from each other made in the governments own currency.

This looks like a solution to a problem that doesn't exist other than in the minds of bank strategists who want to remove or externalise their current costs of cash handling and get rid of something that can't be monitored. So, we're expected to:

- Trust the RBNZ and others won't monetise even more of our transaction details.

- Be prepared to surrender the privacy the anonymity of cash brings.

- Take it on faith that the organisations who will process the transactions won't gouge: is anyone willingly paying 50 cents to use a card for a three dollar parking meter payment, when a few coins are so much simpler?

- Believe that digital currency can be made secure in light of the billions being stolen by digital currency hacking, or lost to our own personal errors.

- Credit that the infrastructure will work and won't add costs - a big leap of faith in light of how badly we run infrastructure, and how immune to things like power and data outages cash is.

Anything that cuts banks out of the picture is a no-brainer. Why should I be forced to have a trading account with a bank when I can have one in my pocket? A $NZ blockchain ledger for peer-to-peer transactions makes sense to me. Stand up an exchange into the banking system for financial services and just get on with it.

A $NZ blockchain ledger for peer-to-peer transactions makes sense to me.

Makes sense to you but it's the last thing that the payment ecosystem wants. It's not just the ticket clip that's important for the payment providers, it's also the data. They perceive that data as having saleable value.

And what 'when' the government overspend and need to claw back money, they can decide to implement negative interest rates on your CBDC? Spend it or lose it, the fact that the government could do whatever they want with our hard earned money, it's a NO from me.

Have they mentioned it will be tied to your social credit score, no that will come later, don't scare them off. You can dismiss this but to introduce this they will need a digital identity that's tied to you and what better way than tie it to your money, once they have that they can do exactly what China has done, maybe not this government but what about the next or the one after that. Why do they need so much control over us?

Lets face it none of them are fiscally responsible enough to be trusted!

Sure from a privacy view point they may know what you purchase but a CBDC would mean they decide IF and on WHAT and WHEN you can spend your money.

Edit: Removed some comments after thinking...

And what 'when' the government overspend and need to claw back money, they can decide to implement negative interest rates on your CBDC? Spend it or lose it, the fact that the government could do whatever they want with our hard earned money, it's a NO from me.

How is this any different from what is currently happening with fiat? With ~1-2% ticket clip on the way through the commercial banks.

One thing, the ability to reach in to accounts without a middle man, currently the banks sit in the middle and that does hold the government to account to some degree. Also the speed at which sweeping changes can be made, it's programable money.

Is there going to be an onbudsman?

I don't see what problems it's really going to solve, it's still centralised, backed by nothing, can be printed to infinity, valued against the USD globally.

What am I missing?

Exactly

I don't know if I am missing something, but what is the positive uplift of this?

Isn't tech awesome? Once CBDCs are in place they can get rid of cash and force everyone to use the new digital currency, then it will be easy to set up digital IDs (linked to the growing network of CCTV cameras with facial recognition), connect vaccine passports to the system to make sure we're all up to date with our injections, and then set up a social credit system. That means we'll have a nice healthy and obedient society with no more crime, because our perfectly trustworthy government with its perfectly reliable IT systems will be able to track absolutely everything we do, naughty or good, give us a ranking, and punish or reward us appropriately. If we're really naughty, they'll be able to just stop us accessing our own money, or buying certain things like plane tickets, just like in China. Happy days!

So. If the RBNZ remains as the 'Clearing House' and by default removes the need for banks, the big four will no longer exist. All you would need is an electronic wallet for the 'Clearing House' to direct all that is yours to you, your wallet. From there you sort out your own payments yourself by having absolute control. But, you will still be restricted access to your cash by the 'Clearing House' right?

Eliminating the 'middle-man' is a good thing, no more ticket clipping but there still is a 'Policeman' the Clearing House.

I'm 50/50 on it so far but ....

Innovative that, innovate this.... it's all just a buzzword and everyone's practically brainwashed by it...

Real innovation would be addressing the existing imbalances and structural flaws in the monetary/banking system and everywhere else... Innovative would be remodeling what we already have... digital, electronic, paper tokens, makes no difference if the underlying foundation is broken.

Nice to see they're realising monetary sovereignty is important but, we gave that away when private banks began creating money.

A nice fluff piece full of psychological and emotional manipulation tactics..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.