The USD continued to retake ground against heavyweights EUR and JPY on Friday, as policymakers failed to rule out the prospect of a September Fed Funds Rate hike.

NZD consolidated in its new sub-0.65 range.

The Fed’s Jackson Hole symposium on Saturday, and the multitude of media interviews conducted around its fringes, did not leave us much more informed on policymakers’ inclinations regarding US rates lift-off.

Fed Chair Yellen wisely chose not to attend this year, in an attempt to deflate the reputation Jackson Hole has recently developed as a venue for significant policy announcements. But instead, investors simply scrutinised Vice Chair Fischer’s comments, as a gauge of which the way the committee is leaning.

Fischer struck a very balanced tone, in an interview with CNBC as well as on his scheduled panel appearance. In the former, he said, “I wouldn’t want to go ahead and decide right now what the case is, more compelling, less compelling,” with regard to a September lift-off. As a panel participant, Fischer reaffirmed his view that inflation would move higher, supporting the case for removing what remains extraordinarily loose monetary policy.

Most of the Fed’s decision-making body continue to hold that belief, despite inflation remaining extremely subdued at present, in the face of an improving labour market. On Friday, the Fed’s preferred measure of inflation, the core PCE deflator, logged deceleration in July, to 1.2% y/y.

Investors seem more inclined to play the man (optimistic policymakers), rather than the ball (low inflation), and bid the USD higher on Friday night. The market continues to unwind the sharp gains that EUR and JPY saw through last week’s equity market plunge.

We remain constructive on the USD into mid-2016, though we have pushed back our expectation of first US rate hike from September to December.

NZD effectively traded sideways on Friday, but is exhibiting an increasing reluctance to rally materially.

A look above 0.65 on Friday was very short-lived, and NZD failed to close above that level every day last week, despite attempts to do so. We remain bearish on NZD, and forecast it at 0.62 by year’s end.

The US employment reports will dominate the week, more so than usual, as this is the last set before the 18 September Fed meeting. A strong reading, coupled with a period of market stability, could well see the Fed lift rates then. We’ll also be keeping an eye on China’s PMI readings (Tue), Australia’s GDP print (Wed), and the local dairy auction (Wed, early am).

Get our daily currency email by signing up here:

Daily exchange rates

Select chart tabs

Raiko Shareef is on the BNZ Research team. All its research is available here.

1 Comments

Fischer reaffirmed his view that inflation would move higher, supporting the case for removing what remains extraordinarily loose monetary policy.

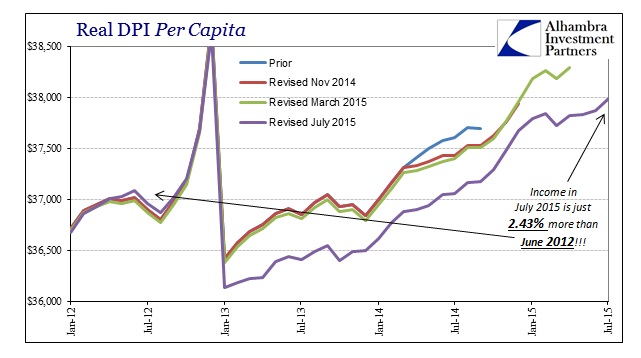

How else is 2.4% income growth total supposed to bring about all this unquestioned recovery? Graphic evidence

{kind=link}

Belief is not enough. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.