It doesn't matter how you choose to view the New Zealand's latest inflation figures - they were shockers from all angles.

While the official Consumers Price Index issued by Statistics New Zealand on Monday showed 'headline' inflation at a 10-year high of 4.9%, the Reserve Bank's own model showed things were even worse.

According to the RBNZ's own 'Sectoral' measure, inflation as at the end of September was at its highest level since June 2009, albeit at a somewhat less spooky-looking 2.7%.

But it has risen sharply. It's up from 2.4% as of June, 2.2% in March and 2.0% as of December 2020.

The Reserve Bank describes this model as "a dynamic factor model that estimates the common component of inflation from all the CPI classes for which data is available. Ninety-six of the 105 classes currently in the CPI are included. The data excludes GST."

The latter point is quite key - because of course the last time the official CPI was above 5%, in June 2011, this was due to the effects of the last rise in GST. Before that the previous time the CPI was above 5% was in 2008 just prior to the Global Financial Crisis.

The other key thing to look at with inflation is how much of it is locally-generated, IE within New Zealand and is not subject to international ups and downs, such as global oil prices.

In terms of this 'non-tradeable' inflation, the RBNZ model has it running at 3.5% - the highest level since March 2009.

So, we are not just importing inflation. We are making it ourselves.

And this figure has risen from 3.3% in June, 3.1% in March and 3.0% in December 2020.

Remember, the RBNZ aims for inflation within a 1%-3% range with an explicit target of 2%.

It has already increased the Official Cash Rate (OCR) from 0.25% to 0.5% on October 6. Everything in the latest inflation figures suggest it will - if it is to be consistent with its inflation targeting - increase the OCR again when it next reviews it on November 24.

ASB senior economist Mark Smith says the RBNZ "will be very wary of the lift in core non-tradable inflation from its measure".

"We expect annual headline CPI inflation to move above 5% by the end of this year reflecting a perfect storm of higher costs/commodity prices, intensifying capacity pressures and demand-driven inflation," Smith says.

"While the RBNZ will likely ‘look through’ a transitory lift in inflation, the risk is that high CPI inflation outcomes persist well into 2022 as pressures on capacity broaden and tighten further."

Smith noted that Monday saw "a large pick-up in NZ yields and upward revisions for OCR rate hike pricing".

"NZ swap yields were up 15-35bps across the curve, with similarly-sized jumps for NZ bond yields. Swap yield increases were the largest in the fixed mortgage belt, with circa 27-35bp rises in the 1- to 5- year swap rates and a close to 60bp increase in the 2-year swap rate (at 2.00% a 3-year high) since the start of this month.

"If these increases stick, and we expect they mostly will despite a worryingly high number of Covid-19 cases reported yesterday, further rises in mortgage interest rates we earlier warned about will be sooner and more sizeable."

Consumer prices index

Select chart tabs

34 Comments

It seems obvious to me that consumer prices will rocket when the productive capacity of nearly half the country, including our largest city, is impaired by lockdowns. There's lots of money looking to hoover up goods and services but business has one hand tied behind its back.

The longer lockdowns go on the worse inflation will likely get and the higher the probability it triggers a recession.

And then there is also the post lockdown where everyone has excess cash to spend, also inflationary

Covid wage and resurgent payments, add on Nat Super and benefits and bloated govt and councils.

That's a big pile of cash giving purchasing power to those producing nothing. So we have those producing nothing being given purchasing power to bid up the fewer services/goods being produced.

And they are surprised by inflation figures?

Orr just pretending to be surprised?

Feels like watching the start of a Train Crash in slow motion. What will Orr the highly intelligent Train conductor do now? Probably time to base any response on facts rather than RBNZ & Treasury forecasts.

What part of this was not predictable prior to Christmas? Why in heavens name did they carry on with their foot hard on the economic stimulation pedal? In doing so they have completely wiped out the last vestiges of hope that the majority of young Kiwis have of ever owning their own home. The consequences from here on are ugly. A god almighty house price crash, a dispossessed generation of young Kiwis, wholesale loss of our brightest and best young Kiwis overseas of a horrible combination of the lot. Multiple heads need to roll over this.

Yet if you warn about the consequences of the reckless monetary policies and lending to the housing market over the last 10 years, you get abused, dismissed and silenced by New Zealand's 'winning culture' as a doom, gloom, merchant - yet they have only done this to exploit a bad situation to benefit themselves at the cost of others.

Very true - these stupid reckless ultra-loose monetary policies have only benefited a parasitic minority of self-serving housing speculators.

And now the whole of NZ will have to pay the price for it - with the RBNZ forced play catch-up and to tighten monetary conditions much more aggressively than otherwise would have been necessary, therefore punishing the real economy and productive people too. You did not need to be a financial Nostradamus to foresee it - and I have been saying this for almost 2 years now. The incompetence demonstrated by the RBNZ has been eye-watering, and of extreme negligence.

Well, at least if this tightening of monetary conditions has the effect of bursting the housing bubble and finally kicking a few housing specuvestors out of the market, I will not lose any sleep on it for sure.

And it wasn't Christmas 2020 when it became apparent.

A conspiracist might tell you, this has nothing to do with Covid19, but the virus was used as the excuse to pump tens of trillion worth of dollars, yen, euros and yuan debt into the global economy, - all in the name of what we see about us today. "Mission Accomplished", so to speak.

The RBNZ was just doing as it was told.....

(NB: As you suggest - it isn't going to work, and we will be left with the consequences you detail)

I wonder if Orr reads this site, or checks out the comments.

No. He reads comic books.

I think that it was pretty obvious by Nov/Dec 2020 and I posted several times on this site predicting the mess that we are now facing.

Me too. It was so clearly obvious to anybody who just wanted to see.Orr's incompetence is of epic proportions - and now the NZ economy and society is left to pick up the pieces.

Among the illusions encouraged by every speculative bubble is the idea that wealth is embodied in the prices of securities – that higher prices inherently represent greater “wealth.” The fact is that every security is, at base, a claim to some future stream of cash flows that will be delivered into the hands of investors over time. The wealth is in those cash flows. Yes, any individual can obtain the market price of a security by selling it to someone else, but the buyer, and ultimately the whole string of people who own the security until it is retired – ultimately has a claim on only one thing: the cash flows that the security will deliver over time. That’s where the wealth is. Every other transaction is simply a transfer of wealth between a buyer and a seller. At extreme valuations, that transfer typically favors the seller. At depressed valuations, that transfer typically favors the buyer.

When the prices of securities become extreme relative to their underlying fundamentals – the revenues, GDP or other economic engines that generate deliverable cash flows – there’s only one way to bring the ratio of price to fundamentals back into line, and that is for prices to grow at a slower rate than fundamentals do.

In general, that implies a long period of dull or negative investment returns.

What about rapid growth in fundamentals? Well, over the past two decades, S&P 500 revenues and U.S. nominal GDP have grown at just 4% annually. Unless profit margins expand indefinitely from already-record highs, that’s the baseline for nominal growth. There are two ways to bump that up: higher real growth, or higher inflation. Given that real structural U.S. GDP growth (the sum of demographic labor force growth and trend productivity) has gradually declined over the past three decades to only about 1.6% annually, real GDP growth is unlikely to meaningfully contribute to the realignment. It’s certainly possible for inflation to drive nominal fundamentals higher (in which case investors could still expect negative real returns), but as we’ll discuss below, inflation-driven growth tends to benefit nominal stock market returns only after valuations have been crushed. At present, the CPI would have to roughly triple before the “benefit” of inflation would offset the drag of extreme valuations.

For the S&P 500, we expect a long period of negative returns, both real and nominal, but with more than enough volatility to provide regular opportunities for a value-conscious, full-cycle investment discipline. What makes this cycle “different” from previous cycles is not that valuations don’t matter (they do, and will), but that Fed-induced speculation has not been constrained by historically-reliable “limits” that were useful in previous cycles. So we’ve adapted, to tolerate and even thrive in a world where even Fed-induced speculation without “limits” can still be gauged by the level of valuations and the condition of market internals.

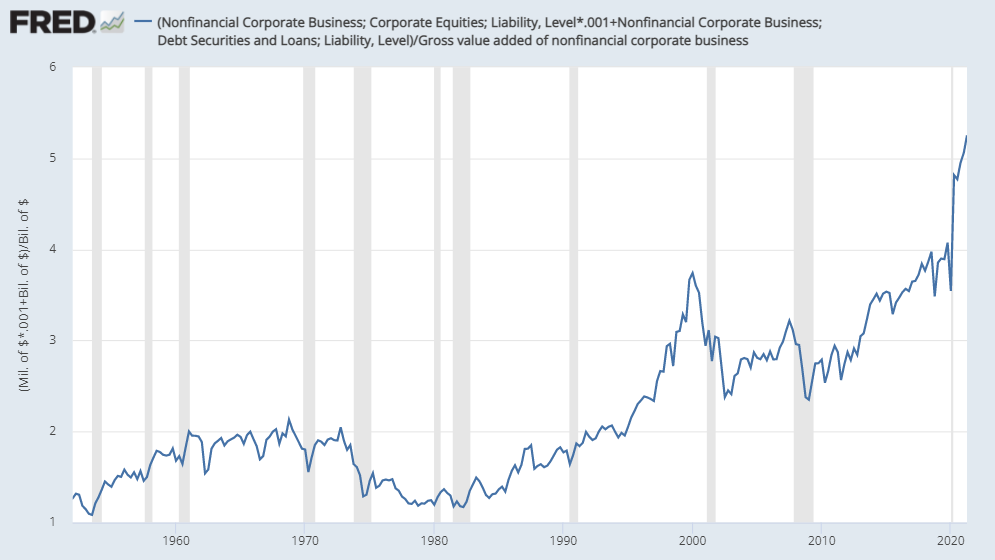

What investors view as “wealth” is actually just the current price of their future wealth. Except for individual investors who sell into the extreme valuations that are periodically offered by Mr. Market, those prices are just blotches of ink on paper and flashing pixels on a screen. For long-term investors, the wealth is in the cash flows, and those cash flows are in the denominator. When you divide the market capitalization of the liabilities (the market value of stocks or debt) by the value-added production that generates the cash flows (GDP or corporate gross value-added), you get a useful picture of the extent to which investors are likely to enjoy outstanding long-term returns or dismal ones. Indeed, as I’ve often detailed, valuation measures based on these comparisons are also the ones best correlated with actual subsequent market returns.

At present, that picture has never been more extreme. The chart below shows the sum of equity market capitalization and debt for U.S. nonfinancial firms, divided by the gross value-added (essentially revenues) of those firms.

{kind=link}

"The data excludes GST."

Whew! That's a relief. I mean, it's not as thought retail consumers have to pay the end result of GST or anything.....2.7% is so much more consoling that 4.9%...

I think you will find that GST makes no difference to the percentage increase unless the GST rate changes.

I know. But have (your) purchases gone up by 4.9% or 2.7% - IF those figures, in themselves, can be believed at all?

I don't really keep track, probably about 2.7% as all I buy in lockdown is food and that hasn't gone up much other than fruit and veg.

I noticed some big price movements at Bunnings though with an online order.

Obviously if I bought a house I would see a big difference, but unlike some I don't buy one of those very often.

The ONLY inflation that the central bankers really give a damn about is salary increases. Anything else, can, and will, be excluded, ignored or "looked through". This systemic bias is why the cost of living in this country keeps getting worse and worse.

You guys are going to run out of images of an array heading upwards soon

Nothing new incompetency at it's best, thanks Orr no thanks..

Just going to put this out there: Anyone who thinks that Govt spending, quantitative easing, or monetary policy is behind the current swathe of price increases is letting their passion for state-bashing cloud their judgment.

Sure, low interest rates have contributed (a bit) to rising house prices, but energy prices, shipping constraints, disruption of just-in-time supply chains, raw materials, the price of broccoli? Really?

Perhaps if various commentator of this site hadn't been warning for many years now, where contemporary Government/RBNZ would take New Zealand (pretty much exactly where we are today) then, No. And guess what? It's going to get worse.

There is no painless way away from where we find ourselves today. It's just a matter of who loses, when and how much. (NB: Those who find themselves at the bottom of the economy haven't got much left to lose, So it will be those who think they are insulated from loss)

Okay jfoe..explain this. If we don't increase the money supply and have the same amount of cash...how can you have inflation?

Sure a price of good A goes up, so you have less to spend on good B. They balance each other out.

Inflation is the result of increase in money supply. It is a form of tax/theft created by the central Banks.

Around 90% of the money supply is credit money loaned by banks to consumers and businesses and around 10% is from Govt spending. Thus the money supply is primarily driven by people appetite to borrow and ability to pay back. More importantly, saying that money supply leads to inflation is seriously flawed. If you are up for finding out why... https://www.forbes.com/sites/johntharvey/2011/05/14/money-growth-does-n…

Federal Reserve Bank of St. Louis

To summarize, the money supply is important because if the money supply grows at a faster rate than the economy’s ability to produce goods and services, then inflation will result. Also, a money supply that does not grow fast enough can lead to decreases in production, leading to increases in unemployment.

Money and Inflation, Feducation | Education | St. Louis Fed (stlouisfed.org)

Nobody believes this rubbish any more - it just lives on in the text books and on daft sites like investopedia. See also the idea that banks lend out the money you deposit (or multiples thereof), or that Govts go into debt when they swap bonds for cash in bank settlement accounts etc etc.

All I’m reading here is further attempts to downplay the inflation I see everyday at the grocer.

As if the sham that is CPI wasn’t enough. I’m pretty angry to be told inflation is 3-4% when everyday essential expenses like food, power, fuel, housing are clearly up at least 20%. It feels like a bare faced lie and does little for my confidence in our institutions.

My confidence in the current management of the RBNZ is ZERO, given their track record of at least the last three years.

Take a look at the inflation in the USA here.

https://www.dailymail.co.uk/news/article-10103413/US-recession-bad-2008…

I think you are wrong. Yes, inflation is rising and will do so for a while yet, particularly for some things like petrol and quite possibly food. However, you are ignoring the fact that global GDP has been slowing for decades-despite globalization and the technological revolution.

When the sugar rush of pent up demand falls away, a truer picture will emerge with GDP continuing its decline, a growing realisation that it's getting ever more expensive to dig up all the metals and minerals we need to transition to a Green economy (EROI), a gradual realisation that the age of rampant consumerism is coming to an end(must end) and oh yes, the small matter of an ever worsening climate.

I don't have a mortgage, but if I did I would fix for 5 years. After that, they may well be in retreat again.

Lower growth may be deflationary... BUT

not until there has been destruction of asset prices. While the accepted market value of financial assets is sky-high, it just means there is more money chasing fewer (less growth) goods.

In a sane world, people would look at real growth rates and realise that many financial assets are not worth anything like what they're marked at because they'll never return a profit. Then the bezzle shrinks and there's a chance for deflation. But that hasn't happened yet -- so long as your unprofitable tech stocks and your cryptocurrencies can be exchanged for lotsa money and then used in the real world, there's inflation.

David Hargreaves points out the RBNZ's sectoral factor model to measure consumer price inflation. And 'apparently' this is the measure that the RBNZ prefers to use over the CPI (no doubt they look at both).

If you look at the SFM over the long term, you can see far less volatility than in the CPI.

Why does the RBNZ keep the public in the dark about the SFM? You never see it referred to in their media releases nor does the mainstream media ever refer to it.

Given that the SFM always seems to hover around or below 3%, does this make the RBNZ less effective in responding to 'real inflation'?

It would be a dark comedy if interest rates passes its inflection point; the more the raise it, the higher the inflation.

Yet they sat on their hands and did nothing.

We need a sensible government again that will change the mandate of the RBNZ back to what it used to be, and we need a sensible RBNZ that can think for itself and not cower to Labours whims.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.