Winston Peters’ dream of having a government-owned and operated KiwiSaver scheme is a step closer to becoming a reality.

New Zealand First MP, Fletcher Tabuteau’s, KiwiFund members’ bill passed its first reading on Wednesday. It will be considered by the Economic Development, Science and Innovation Select Committee, before having its second reading.

The 807-word long Bill establishes an independent working group of banking, savings and retirement sector specialists to advise on setting up a government KiwiSaver provider based on principles such as:

- lower and transparent fees;

- preferential treatment for New Zealand-based investments;

- social and ethical investment;

- the support of a government guarantee;

- keeping profits in New Zealand.

Speaking in Parliament, Tabuteau said the KiwiSaver scheme was a “roaring success” increasing the proportion of New Zealanders with a retirement savings scheme from 16% before its introduction to 75% today.

Yet he said fees were near static; his calculations showing the typical KiwiSaver member with a balance of $500,000 at maturity would have paid a total of $100,000 in fees.

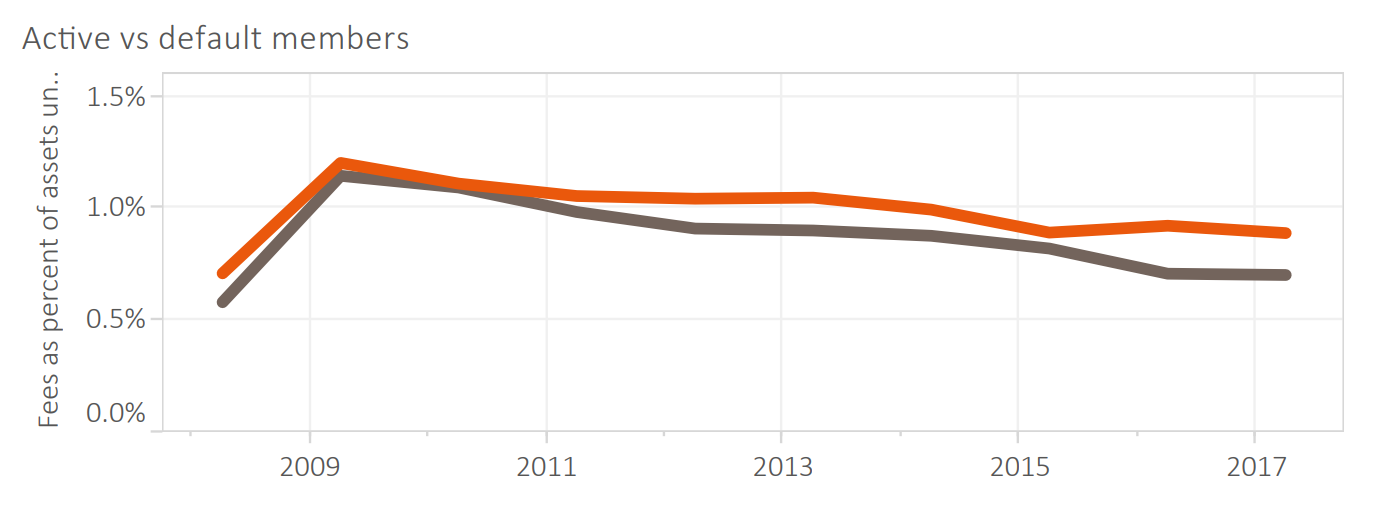

The Financial Markets Authority’s (FMA) latest annual KiwiSaver Report shows default KiwiSaver providers’ fees were stagnant between 2016 and 2017.

The orange line in this graph shows active members' fees as a percentage of funds under management, and the grey one, default members'.

Tabuteau also questioned the legitimacy of providers saying higher fees enable them to engage more with their investors.

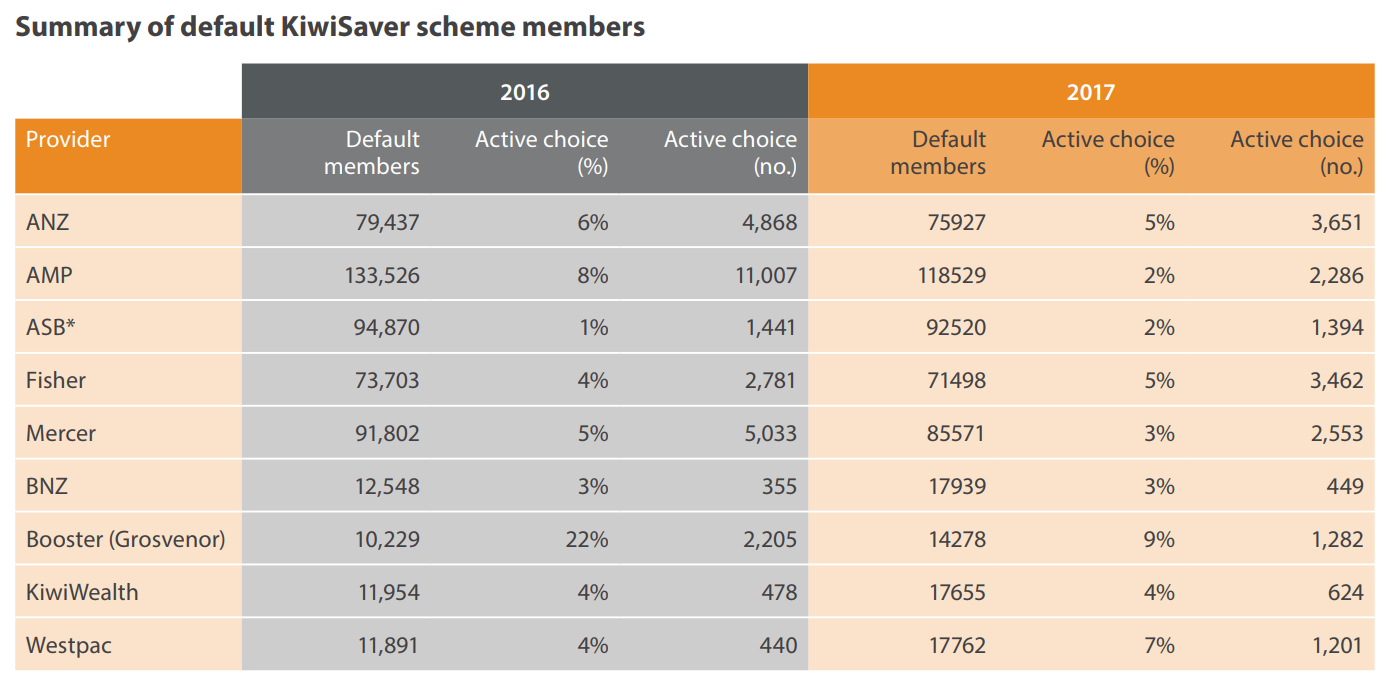

This FMA table shows the portion of members in default KiwiSaver funds who have actively chosen to be there.

Tabuteau likened KiwiFund to Kiwibank, saying: “New Zealand history is on our side in fact. Kiwibank tells the story of determination, of conviction. Everyone in this house knows that Kiwibank was the right thing to do.”

It is worth noting New Zealand already has a government-owned KiwiSaver provider - Kiwi Wealth. Like Kiwibank, it is a wholly owned subsidiary of Kiwi Group Holdings, which is owned by New Zealand Post, Guardians of the New Zealand Superannuation Fund and the Accident Compensation Corporation.

Despite being non-committal on the Bill when it was drawn from the ballot in December, Labour came in to bat for it.

Labour MP Michael Wood focused on the issue of KiwiSaver investors paying disproportionately higher fees than institutional investors, saying: “Why wouldn’t we look into that?”

‘Misguided’ and ‘unnecessary’

Yet the Opposition highlighted a number of flaws in the Bill, with National’s Associate Commerce Spokesperson, Andrew Bayly, saying it was a classic New Zealand First policy that sounded “popular” and “compelling” on a high level, but was “misguided” in reality.

He questioned whether adding another KiwiSaver provider to the array of providers we already have - including ones that prioritise low fees - would actually increase engagement and prompt investors in default funds to look further afield or make an active choice about being there.

Bayly pointed out that concentrating a fund by giving New Zealand-based investments preferential treatment would increase its risk profile, which would affect returns.

He also said having a government guarantee would create a “moral hazard”, as other providers wouldn’t have the same backing.

Also speaking in Parliament, National MP Lawrence Yule questioned why New Zealand First was wasting time and resources introducing legislation to review the KiwiSaver scheme, when it could do so through an inquiry into fees, transparency or whatever else it was trying to fix.

Furthermore, he raised the point: “There is nothing [in law] to currently prevent anybody, including the Rt Hon Winston Peters, setting up a superannuation fund himself, with very low fees, without a government guarantee, to actually support the people he’s claiming he wants to support.”

He questioned why yet another “working group” needed to be set up.

‘The last thing it needs now is more political tinkering’

The Financial Services Council - an industry body that represents a number of KiwiSaver providers - likewise questions whether the Bill is necessary.

Its CEO Richard Klipin said there is “real transparency” around fees, with investors able to choose funds on a spectrum from low fee passive funds to high fee actively managed funds.

“The fee debate is an important one to have. However the fee discussion in the absence of value is only considering half the issue and does not give the full picture,” he said.

“KiwiSaver has just entered its second decade and is beginning to mature and have New Zealanders starting to properly engage with it. The last thing it needs now is more political tinkering and another working group.

“Instead we think industry and government resources would be better focused on improving New Zealanders' understanding of KiwiSaver, and to build on the range of advice and resources that are already available.”

More political pressure than regulation

The Financial Markets Authority (FMA) has in recent years put notable effort into providing the public with more KiwiSaver resources.

For example, in November last year it released a ‘KiwiSaver Tracker’ - an online tool that presents the information KiwiSaver providers give investors through their quarterly fund updates in an interactive tool.

The Tracker provides granular information about individual funds returns after fees.

The FMA has also required providers from this year to start disclosing fees in dollar terms on members’ annual statements.

Its CEO Rob Everett has in the past said the sector is now large enough for fees to fall. He has also put pressure on default KiwiSaver providers to better engage with their members so they move to the most suitable fund for them.

However this pressure Everett has applied hasn’t translated to regulation.

Commerce and Consumer Affairs Minister Kris Faafoi earlier this month said he wanted to see default KiwiSaver providers cut their fees, yet in November told interest.co.nz he would take a “considered approach” so wasn’t keen on capping fees.

Is further research and a ‘working group’ really necessary?

The other Government agency that has done extensive work on KiwiSaver is the Commission for Financial Capability.

In its latest three-yearly Review of Retirement Income Policies, it recommended the following changes be made to KiwiSaver in the short term:

- Increase employer and employee contributions from 3% to 4%.

- Automate the option to increase member contributions up to a certain level.

- Add 6% and 10% to increase the range of employee contribution rates options.

- Decouple the age of access to KiwiSaver funds from NZ Superannuation and discuss appropriate eligibility age for access to KiwiSaver funds.

- Allow people over 65 years to join KiwiSaver.

- Change the name of ‘contributions holiday’ to ‘savings suspension’ and reduce the maximum time to one year.

- Require KiwiSaver providers to disclose the total dollar cost of all fees on annual statements.

The last recommendation is the only one that has been enacted.

59 Comments

Been in Kiwisaver since the beginning and haven't had any interaction, except standard emails.

Hence the real issue is advice - schemes should be engaging with their investors to advise them on the right fund (conservative/aggressive etc). Choosing the right fund is more important than choosing a scheme with no fees but selecting the wrong fund

But look at the Plethora of Posidives, peeps:

- Employment opportunities, as the HQ could conceivably be in Kaitaia, Waitara, or other shovel-ready hubs of financial expertise, because discrimination

- Top salaries payable, because inequaility

- Low fees, as the aforementioned salaries will be subsidised by WINZ, TPK, Ministry for Women and the Regional Development Fund, because we can

- Investment opportunities, because 1 billion trees and 0.1 million houses

Or, just possibly, because ya just can't make this stuff up....

National would get rid of kiwisaver, the nz super fund and probably even public schools and hospitals if it could. Sign me up.

Yes, that is why National reversed the welfare state when it first came to power in 1949.

Oh no wait, that didn't happen, you are just making stuff up.

Nope, i'm not. National stopped paying into NZ super, opposed Kiwi-saver and made considerable changes to it as the previous government including removing the sign up incentive and taxing employment contributions.

I know the idea of ordinary kiwis having considerable wealth going into retirement and contributing to a considerable source of capital for local businesses scares you. But rest in the knowledge Australians and Singaporeans are doing just fine.

Of course you are.

You claimed National would get rid of Kiwisaver. But it never did.

You claimed National would get rid of nz super. But it never did.

You claimed National would get rid of public schools. But they never did.

You claimed National would get rid of hospitals. But they never did.

You are putting words into their mouths and/or predicting the future - talking complete rubbish.

You have no idea what scares me, you don't even know me.

Read what I said. I said they would if they could. Not they would. They have underfunded or negatively impacted all the areas mentioned.

Your taking the Winston Peters rejection a bit too seriously. There are plenty of fish in the sea.

I could have told you he wasn't going to pick you by the way. But you can't reason with the smitten.

I did read it - look up and you will find these words in your post "National would get rid of .."

Now you say "if they could" -- as if they haven't just been in government with every opportunity.

You said something silly, I called you on it. That is all that happened here.

National would get rid of kiwisaver, the nz super fund and probably even public schools and hospitals if it could.

I know your hurting. Winston's a player, it's time to pick yourself up and get back in the game. I hear Joyce is looking for love.

Still pushing drivel I see.

It could have and it didn't.

I suppose I should give credit where it due. National could/would/did introduce a weird hybrid beast named charter schools under the guidance of a irrelevant little man named Seymour. A type of Freudian slip suggesting a move towards privatization of our schools.

But that's gone now. Within 100 days no less.

With National is was always a slow death by a thousand cuts, then privatise to their friends in the private sector to profit from the scraps.

Exactly, National knows full well that being up front and honest with its policies would make it un-electable.

That is a big assumption, ie we have not seen this stated as National policy. In terms of how that would work out for a party wanting to do that I suggest you have a look at ACTs vote % for the last few elections...or just trust me when I say its about 0.3%. ie un-electable.

Sounds like you support good social policies .

To be fair there is getting rid of, and starving the service to death so ppl are forced to move to a private service.

National chose the latter, insidious course.

.

Nice. At least you said something that is true.

I predict this will happen because I suspect Mr Peters wants a personal legacy and that we all have to pay for it probably doesn't feature in the thinking.

"KiwiFund Bill to establish a committee .."

I recommend that we set up an interdepartmental committee with fairly broad terms of reference so that at the end of the day we'll be in the position to think through the various implications and arrive at a decision based on long-term considerations rather than rush prematurely into precipitate and possibly ill-conceived action which might well have unforeseen repercussions.

I'm a big fan of Kiwisaver. But there is no great reason to do this given the existence of a government owned provider anyway (Kiwiwealth).

Anybody can set up a scheme, and then folk will vote by joining or not. Power to the people on that one.

As for the fees thing, yes they are ridiculous. But it's as much the fault of those paying them as those charging them. Kiwi's are suckers and the opposite of smart when it comes to purchase decisions.

Sure anybody can set up a scheme - but - this way Mr Peters can take all the credit if it's a success but it won't cost him a cent and with the added benefit is he can blame someone else (management) if it fails.

He is an experienced political operator you know.

Given the commentary here today, on Interest.co.nz, re the first rate success of the NZ Super fund, and comments asking why this ability cannot be made available for Kiwi Savers too, well it would appear that WP’s iniative here is sensible and a good fit.

This is precisely the point, the ideologically driven disgruntled National voters here do not want to acknowledge.

If nothing else the existence of a government scheme will drive the costs of other providers down.

I'm not sure if it's possible perhaps someone could enlighten us, but the NZ super fund benefits from special tax treatment being a sovereign wealth fund. If the NZ run kiwi saver scheme could take advantage of such treatment it would be hard to argue its potential upsides.

Agreed, the best way to deal with high fees is to vote with your feet. If anyone is keen to pay a 1%+ fee and throw away 10-20% of their annual expected gain, they are welcome to. The government has a role in making sure fees are transparent and I think have already taken steps on that.

Given that fees have not reduced as scale has increased this suggests regulation is needed. I don’t support a government option. The best option is probably a maximum fee, something under 1%.

I guess it wouldn't be allowed to invest in weapons and defense stocks. I'm not against investing in NZ companies but shouldn't the focus be 100% ROI?

To be honest, I don't know what the heck this bill is all about ... and Fees? ..What fees?

Not sure which Kiwisaver fund is charging 20% ($100,000) in fees over the life of the average $500,000 fund as the NZF member claims ?? ...

My provider is one of the top Growth Funds and is making me an average 13% pa over the least 10 years ... year in year out !!... they charge me $36 pa in fees ... that is not a miss print ... it is $3.00 a month for a fund greater than $500,000....and there are no other charges whatsoever, they will charge bonus fees when they achieve over 15% pa in any given year ( and that incentive is fair) ....

Surely, providers need to charge something for the efforts they put in achieving such returns - especially active fund managers looking after local and o/Seas equities etc.... or is that another pound of flesh the gov sees necessary to dissect from this industry ?

Surely, The super fund executives and custodians are being paid big packets for achieving these returns, aren't they?

Again, The good samaritans just love to regulate instead of educating people and let the free market correct itself - if fees are getting overboard, then make an enquiry and whisper few words in the right ears to get it right - the Gov does not have to be first and last resort if people cannot think for themselves and shop around !! ...

Good points Eco & agree there are obviously funds out there with sensible fee structures. All it takes is a bit of effort to ask around. Only sour grapes is that, from our previous dialogues, I had you down as bit older than that, like me. Guess though no reason not to savour the single malts at a junior age.

Indeed :) ... No reason whatsoever ...

I guess you're referring to Simplicity, they do look pretty good. I just did a quick compare to my own fund Kiwi Wealth growth. Simplicity Growth vs Kiwi Wealth Growth net fees : 0.57% vs 1.18 %. But comparing the yoy returns Kiwi Wealth won, Simplicity Growth vs Kiwi Wealth Growth yoy_(2017): 11.65% vs 15.47%. Need to keep these guys on their toes.

.

Hmm, I think you're right. looks like you need about 10K in simplicity to give 0.57% pa! The rate gets better the more you have. I was just taking the sorted website at face value. On the simplicity website it clearly says the fee structure is $30 per year + $3.10 for every $1000 under management.

As far as I can tell from my own Kiwi wealth Growth fund I'm paying about $600 management per year but I only have a small kiwisaver of 63K. looks like 0.95% which doesn't quite tally with the sorted website either (but agrees with the graph in this article). Need to look into this in more detail.

.

.

Expecting ANZ to come out first soon with KS fee reduction, like they did with the ATM fees. Let the music begin. The government is on the right track in pressuring the Banks with initiatives like this...Way to go, Winston.

Super Gold Card holders having KS accounts should be completely exempt from any fees.

They already did earlier in the month.

Cool, must have missed that. Why other providers have not followed suit though ?

They have. Kiwi Wealth did as well. I recall doing a rough calculation of the $ impact of the ANZ reduction had it at a bit less than $1 mln per year. But given their high membership, it does not translate to much per member.

So, it was just cosmetic ? Very underwhelming..

Surely the government can just instruct GMI (which is now a subsidiary of Kiwibank/NZ Post/NZ Super etc. as I understand it) to do this. They just need to scale the staff and come to an agreement on a low fees approach (index funds or whatever). Very low risk and little upfront investment aside from changing the letterhead.

anyone know what would happen if one of these kiwisaver funds became insolventt? I presume they'd be bailed out like South Canterbury Finance was.

Funds like this don't become 'insolvent'. Insolvency is when you can't pay your debts, and money market funds only have assets, no liabilities. But those assets can go up and down in value, and in theory go to zero value. That an investment asset loses all its value is just means there would be no payout. The fund managers can't borrow against the fund value. They could become insolvent but that would not directly affect the value of the assets in the fund. All that would happen is that a new manager would need to be appointed. I think you are mixing up the position of the fund manager, and the legally separate position of the fund and its investors.

Thanks for clarifying. These funds aren't like Hanover or SFC are they. I was thinking of a scenario like that involving Bernie Madoff where serious fraud was involved. That's not totally inconceivable is it? I suppose there are checks and balances to make sure the assets match the liabilities.

Yes Fat Pat. I too have thought of what happens if some scheme goes the "Full Madoff". A solution for that is that you would be allowed two have more than one Kiwisaver scheme - even several - thus spreading the eggs into different baskets.

Maybe a requirement that you have to have $10K Plus (or 50Kplus) before you get an additional scheme.

well that's an alternative to a bailout. I guess there’s no risk of a “run on the bank”, so to speak, because the funds are locked until age 65, but that probably increases the likelihood "full Madoff" it because the chances of detection would be low. As mfd says money can be held in trust but that doesn’t fill me with confidence. Also if the fund had an insolvent parent.. say bank with covered bonds...

In the case of my provider (simplicity), the funds are held in a trust. From their website:

"When you invest in any KiwiSaver Scheme, the manager does not get any of the money (apart from any fees it charges you)"

"If for any reason Simplicity were to run into difficulties, your investments would not be affected. The Scheme’s investments would be transferred to another manager."

Simplicity is essentially holding cash and Vanguard funds in my name, if the provider falls over then the funds still exist and still in my name.

I presume other providers have the same kinds of arrangements but obviously check this before signing up.

Just put a limit on the fees that the greedy Kiwi Saver fund managers charge - should be half what they are now

Why not take action yourself? You don't need 'someone else' to do that. Just move to where you think you get a better deal. Its quick and easy. Fee disclosure is easy to find and there are a very wide range of fees being charged. Your problem will be that there is virtually no relationship between fees and net returns. Many of the better returns come from higher fee funds, many of the lower fee funds are underperformers. We will have gritty detail on this in an upcoming article. Focusing on fees is a complete red-herring. You should focus on future long run after-all-taxes, after-all-fees returns and positioning. KiwiSaver has been going ten years now so there is a track record.

I was thinking the same thing David - it's the return after fees and tax that is the most important number. By regulating fees I think we could end up in a position where there is no innovation and competition in KS and all we have is passive index funds. KS has been going for 10 years and Interest's comparisons show who are decent and who isn't. I focus in the growth/aggressive funds and it seems there about 5 fund providers who are generally there or there abouts.

Yes, you've hit the nail on the head.

It's already hard enough for boutique/startup money managers in New Zealand. Do we want a "winner take all" situation where cheap and vanilla is all that there is in the market? It's effectively the government making a value judgement on what sort of investment strategies people should be undertaking - not their role IMO.

Go Milford

Excellent David.mAin point there is no free lunches, you only get what you pay for. Low fees low performance a no brainer really.

Would like it if the Kiwisaver funds were only taxed when the funds are paid out. Would help the pie grow bigger

Present system is like three steps forward and one back.

But heh that is why the Govm changed the tax status because it had run out of money.

"Low fees low performance a no brainer really."

Ask John Bogle if you're right.

I say, good idea, make it the default fund for employees, and make it index-tracked or ETF, then you will see fee`s going down, and the commercial banks starting to cry.....

Fees are a red herring. Net return after fees is the real measure of success!

Just look at the latest Morningstar reports showing Simplicity in 8th (out of 9) place for total returns in the Aggressive fund. Well done to all those chasing low fees, you missed out on the performance element!

I like this idea from Winston & I would be more than happy to switch to this fund. Because currently all I know of my chosen funds is the fees & the returns plus the risks.

Knowing where your money is invested & which

country it is benefiting along with the Government backing is what ALL current Kiwisavers are lacking!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.