Will the Covid-19 crisis and subsequent economic recovery lead to rising inflation, turning the tide on three decades of deflation?

Yes, according to Morgan Stanley economists.

In a nutshell economists at the investment bank argue because the public health crisis has galvanised policy-makers into a quick response, for the first time in a decade there's coordinated monetary and fiscal policy easing underway. This combination, they say, is essential to get out of the low-growth, low-inflation loop of recent years, and will disrupt the three key deflationary forces of the past three decades, being technology advances, trade rules and corporate titans.

When will this inflation emerge? Morgan Stanley's estimate is 2022.

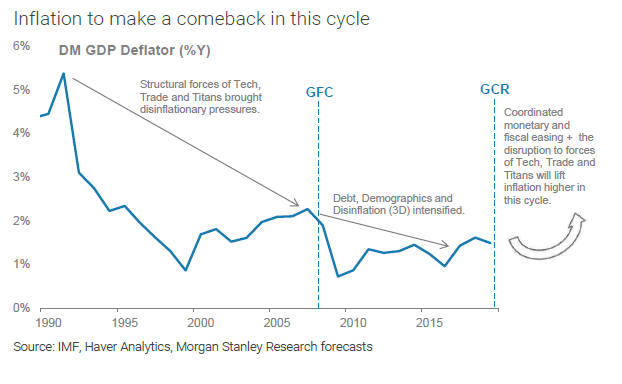

"For the past six years, I have written a good deal about how the 3Ds of debt, demographics and disinflation are the key structural challenge for the global economy. Pick up a long shelf-life report from this period and you will probably find a comparison of the global macro backdrop to that of the US in the 1930s and Japan in the 1990s, and how macro policies post the global financial crisis (GFC) were unlikely to effectively bring us out quickly from the debt and disinflation trend. Those who are still in the disinflation/deflation camp will argue that the Great Covid-19 Recession (GCR) is a supercharged version of the GFC and will only exacerbate the debt and disinflation trajectory that we have been on," says Chetan Ahya, Morgan Stanley's Chief Economist and Global Head of Economics.

Ahya suggests there are two reasons why the tide is turning in favour of higher inflation.

"First, the GCR will be a sharper but shorter recession than the GFC. The trigger this time is an exogenous shock in the form of a public health crisis, rather than the classic, endogenous adjustment triggered by rising imbalances. The GCR also did not start out as a financial crisis, and the banking system is in better shape today than prior to the GFC. We expect global and DM [developed markets'] output to reach pre-recession levels in four and eight quarters, respectively, compared with six and 14 quarters during the GFC," Ahya says In a report entitled The Return of Inflation.

"Second, and more importantly, the public health crisis has galvanised policy-makers to respond swiftly. For the first time in a decade, we are finally getting coordinated monetary and fiscal easing – a policy dynamic that we have viewed as essential to get out of the low-growth, low-inflation loop. The scale of easing is also unprecedented during peace time. With the economic shock driving an even deeper wedge between low- and high-income workers, policy-makers are scrutinising what I have called trade, tech and titans more closely, given their role in driving the wage share of GDP lower and widening the income divide. Disturbing this trio will also mean disrupting the key structural disinflationary forces of the past 30 years."

The GCR, as Ahya puts it, has unleashed forces that will make it a turning point and start "a regime shift" towards higher inflation.

"We see the threat that inflation emerges from 2022 and will overshoot the central banks’ targets in this cycle."

"The consensus remains in the disinflation camp. Just as the consensus underestimated the disinflationary trends of the past 30 years, it is at risk of under appreciating the inflation threat. In response, I would argue that the driving forces of inflation are already aligned and a regime shift is under way. The near-term disinflationary trend will quickly give way to reflation and then inflation," says Ahya.

Where inflation's at

To put the Morgan Stanley prediction of a "regime shift" in context, inflation in the United States, the world's biggest economy, fell 0.8% in April, the biggest monthly decline since December 2008 led by falling petrol prices. Projections in the International Monetary Fund's latest World Economic Outlook, from April, suggest inflation of 0.5% in advanced economies this year, and 1.5% next year. The IMF sees inflation of 4.6% in emerging markets and developing economies this year, and 4.5% next year.

Australia's latest annual inflation rate, released in March, came in at 2.2% its highest level since 2014, and New Zealand's March year inflation rate came in at 2.5%, the highest it has been in more than eight years. However these figures predate Covid-19 lockdowns. The Reserve Bank of New Zealand's Survey of Expectations has since shown inflation expectations plummeting.

And the RBNZ's latest Monetary Policy Statement (MPS), issued on Wednesday, predicts inflation will be much lower by the end of this year, possibly below the central bank's 1% to 3% target range. The RBNZ baseline economic scenario from its MPS is for annual inflation to trough at -0.4% in the first half of 2021, and remain below 1% until the second half of 2022.

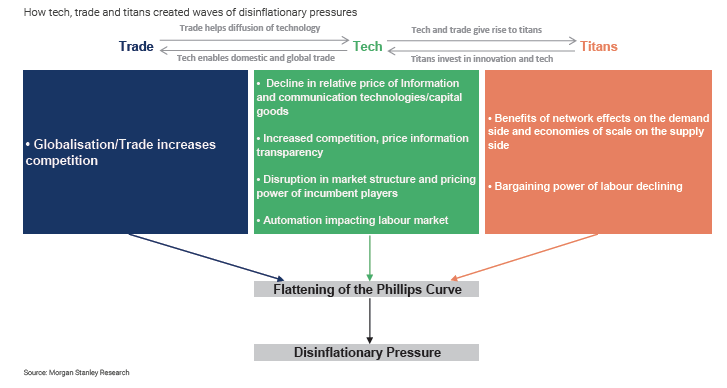

The impact of 'tech, trade & titans'

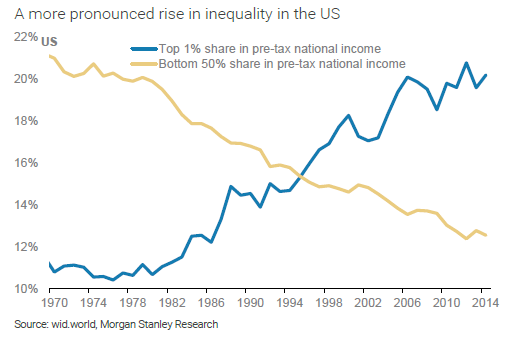

Morgan Stanley points out "tech, trade and titans" have been the key disinflationary forces over the past 30 years. But the three have also contributed to a lower wage share in GDP and rising inequality.

"The discontent about inequality has risen, triggering policy action. Cracks are emerging in global supply chains and slowbalisation trends are being accelerated by geopolitics," says Morgan Stanley.

"The emergence of trade tensions was partly motivated by rising inequality and has already led to scrutiny of the tech and telecommunications sectors. Trade now faces even closer scrutiny after the outbreak of Covid-19, given the need for more resilient local supply chains, especially in areas such as pharmaceuticals and medical equipment. Fears have risen that continuing technological change combined with workplace automation will widen the skill and income gap."

Morgan Stanley says the US is the most exposed developed country to the risk of higher inflation in this economic cycle, because its monetary and fiscal policies are the most expansionary and inequality is most extreme in the US.

'Underlying political pressures to address inequality will rise further'

Morgan Stanley lays out the startling details of where the US deficit is at, and where it's heading.

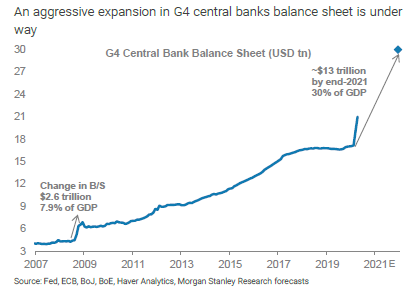

"The US fiscal deficit is projected to reach 19.2% of GDP this year (and will still be relatively high at 14% next year), and there are reports of a further US$1 trillion of fiscal easing, which would lift the 2020 deficit to 24% of GDP, its highest level since 1942, when it stood at 27%."

Additionally the Federal Reserve’s balance sheet will expand by 38% of GDP by 2021, more than the 20% during its GFC era quantitative easing 1, 2 and 3 programmes combined.

"Recessions tend to hit the lower-income population the hardest, but the impact of Covid-19 on lower-income workers has been outsized. As a result, we believe that the underlying political pressures to address inequality will rise further, and see both fiscal activism and continued action to check tech, trade and titans continuing for longer. We see the US as being most exposed to the risk of higher inflation in this cycle, as the monetary and fiscal policies are the most expansionary and the issue of inequality is the most pronounced," Morgan Stanley says.

"The forces that will bring about inflation are aligning. We see the threat of inflation emerging from 2022 and think that inflation will be higher and overshoot the central banks’ targets in this cycle. This poses a new risk to the business cycle, and future expansions could also be shorter. Central banks are now more tolerant of inflation and will be keen to make up for some part of the lost inflation during downturns, in particular for the Fed, given its focus on the symmetry of the inflation goal."

The forces that will determine the speed and magnitude of inflation

Morgan Stanley's economists argue the speed and magnitude of inflationary forces will be determined by; firstly, the size, duration and spending mix of expansionary fiscal policy; secondly by the extent to which tech, trade and titans are disrupted; thirdly by the pace of recovery and normalisation post-Covid-19; and fourthly by the reaction of central banks.

"We would view policies that boost spending on infrastructure, education and the public healthcare system as more beneficial to productivity growth and less distortive than transfers to households. Severe disruption to tech, trade and titans could also create a regime shift in the outlook for corporate profitability."

The Morgan Stanley report argues a precise timeframe for a return to inflation is challenging to predict because it hinges on the evolution of the virus and the pace of economic normalisation/recovery post-Covid-19.

"Private sector confidence (AKA animal spirits) has clearly been dented by the outbreak, but our base case is for a fairly quick recovery. The trigger for this recession is an exogenous shock in the form of a public health crisis, rather than the classic, endogenous adjustment triggered by rising imbalances. Indeed, prior to the GFC, non-financial private sector debt/GDP had risen by 36 percentage points in the US from 2000 to 2007. But prior to the GCR, private debt remained flat after a 23 percentage point decline."

"We see the shock as more akin to a natural disaster than a financial crisis, hence the GCR should not trigger the big balance sheet recession dynamics that we have seen over the past decade. This also did not start out as a financial crisis, and the banking system is in better shape today than prior to the GFC. Financial sector debt/GDP has been declining persistently since its 2009 peak. Moreover, this recession has prompted the most coordinated and aggressive monetary and fiscal easing that we have witnessed in modern times. We expect global and developed markets output to reach pre-recession levels in four and eight quarters, respectively, as compared with six and fourteen quarters during the GFC," Morgan Stanley says.

"We expect inflation to emerge from 2H22 [the second-half of 2022], but we caution that expectations may precede the re-emergence."

A two pillar inflation framework

Morgan Stanley says its "inflation framework" rests on two pillars being the new-found activism in monetary and fiscal policy, and collective action to address inequality, which will disrupt the disinflationary forces of tech, trade and titans.

"Hence, the key question for us is when but not if we get inflation in this cycle."

"We see three phases in the journey – a shift from disinflation in the near term to reflation and finally to inflation. The timing of this sequence depends on the pace of the economic recovery post the Covid-19 shock," Morgan Stanley says.

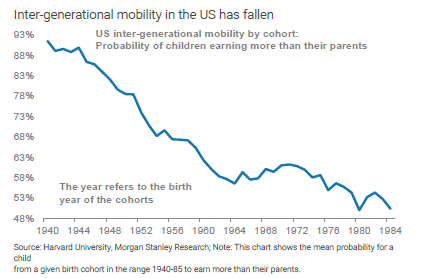

The sluggish cyclical recovery since the GFC has exacerbated the long-term trends of rising inequality and reduced inter-generational social mobility, as the US labour market didn't reach full employment until 32 quarters after the economic expansion started, Morgan Stanley says.

"Across the OECD, median incomes have grown by only 4.6% over the past decade, while the pace of income growth for wealthy households is much higher at 10.3%. In the US, real mean household incomes for the bottom quintile did not recover to pre-recession levels until 2017. The discontent over rising inequality has already affected election outcomes in several economies and has been receiving more attention from policy-makers in recent years, typified by the rise of the progressive political movement."

*The charts and diagram below come from Morgan Stanley.

*DM = developed markets.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

31 Comments

I don't think we will see the inflation risk as early as 2022, unless it really is a V shaped recovery.

Scarcity will set in perhaps even more quickly than that to my mind.

In what areas do you foresee scarcity in NZ?

Jobs.

Stuff. People dont work. Stuff doesnt get made. Stuff gets scarce. Stuff gets expensive. Already 13wks/52, behind the play here in nz. 7 weeks lockdown. 4 weeks xmas. 1/2 week public holidays. 1/2 week getting reorganised.

I follow Morgan Stanley's argument, however don't see the recovery as soon as they see it.

How is the US expected to recover so quickly when they have 20% reported unemployment, and probably more unreported.

The large majority of business customers are mired in debt, with declining income and reduced equity in their homes. Some probably negative equity in their homes.

Sure, the authorities will require these tech companies to pay their past due taxes. All governments are in the same boat, and will be forced to take out the wooden spoon on the abuse of these tax havens. Alot of current and ex politicians will be running for cover, as there pile of ill gotten gains will be exposed. As these tech giants are in on the same sham, I dont see how its going to play out any other way. Here's hoping anyway.

I've always questioned what these technology companies bring to the economy, apart from increased operating cost and more unemployment. The wider cost benefit has never added up to me. I just look at the organisation I work for, where the IT numbers have growth from 10% to 15% of the work force in ten years; bringing on more software which only a fraction ever use. Certainly hasnt driven efficient here, and with the extra training probably less.

Its a giant con job, where companies are hooked into small software upgrades and maintenance just to keep these software giants revenue going. The question one has to ask is whether the the 10% of costs (on average) these impose on business delivers the same gains with extra business. I suspect not, which suggests the software revenue generated from these upgrades should be taxed at a higher rate than other businesses. They might then have to think about how they deliver these upgrades, if any.

"We see the threat of inflation emerging from 2022"

Quite probable.

But that's two years away.

In the meantime, prepare for the opposite.

Those who are still in the disinflation/deflation camp will argue that the Great Covid-19 Recession (GCR) is a supercharged version of the GFC and will only exacerbate the debt and disinflation trajectory that we have been on

There has been no "disinflation" since the GFC. In fact, inflation has been ramped up. The debt trajectory has also been heading for the stars, particularly among h'holds.

This crisis is far worse than the GFC in many respects and it's not unreasonable to expect deflationary forces to take center stage before inflation inevitably appears.

Agreed. Central bankers just keep firing money at everyone. Looks like they their final belt of ammunition unless they start paying you to take debt. Popcorn...

I've seen economists forecasting a return to an inflationary environment for years.

Judiciously, if any substantial rate of inflation where likely to return by 2022 I don't think banks would be lending at less than 3% for 2 years because that's within RBNZs target band.

Hahaha. Squishy an excellent point.

Judiciously, if any substantial rate of inflation where likely to return by 2022 I don't think banks would be lending at less than 3% for 2 years because that's within RBNZs target band.

RBNZ takes their cue for inflation targeting from the CPI. People need to learn that these are imperfect measues of inflation, even at an aggregate level. Furthermore, NZ banks make their money from mortgages. Their interest rates are adjusted to ensure sales volume meets their revenue / profit targets. Lowering interest rates is simply a nudge strategy to get people to take on debt. The banks appear to be nearing the end of their tether in terms of how low they can go. I worked for a Japanese multinational until 2011. Japanese banks were offering me the same interest rate to borrow for property as NZ banks are offering now (with plenty of perks such as free life insurance).

That depends on how smart you think the banks are. Are they suckering you in right now for their long term gain ? who knows what interest rates will be in 2 or 3 years time. To me the picture is clear until Christmas and maybe a couple of months beyond that. What if you come out of your 2 year fixed starring down the barrel of sky rocketing interest rates ?

If the 30's and 40's, then subsequent decades are anything to go by...who says we couldn't have significant inflation?

https://ritholtz.com/wp-content/uploads/2010/08/1790-Present.gif

{kind=link}

You need a complete wipe out and reset of the currency first, even then I don't think it is likely.

Yea right! And Santa's real.

If I read this article right, the US is going to realise that its fiscal and monetary policies for over 30 years have overwhelmingly favoured the wealthy end of own and will seek to become far more egalitarian. That would involve a huge shift in their taxation system, not to mention the healthcare and social security systems.

I'll believe it when I see it.

Sell less, charge more.

Inflation. For us a typicial suppermarket shop in January was $250 per week, now it is $350 per week and that was also depleting our freezer, pantry store at the same time.

Hard to see what is costing more except for a dollar here and there.

Building is costing more at present due to CV safety and the time it takes to get materials.

Schools are going to be doing more fund raisers and didn't manage to have the annual school gala.

It will be interesting to see how much prices in restaurants / clothing / and other supplies increases due to selling less.

Everyone is in save mode and have realised than dont need as much as they needed before hand.

It will be interesting to see what else will go up. I dont see much going down except for houses.

For us a typicial suppermarket shop in January was $250 per week, now it is $350 per week and that was also depleting our freezer, pantry store at the same time.

Then this kills the restaurants. Restaurants were perhaps a luxury of a credit driven time before the rainy days. If staples are going up, frivolous discretionary spending is going down.

Now the CPI suggests, for the second month in a row, even if monetary policy is effective the business sector may not have time to wait around for some psychological boost. We already know that much from the labor data (as well as clues about that effectiveness). Like 1982 or even 2009, such deflationary months were, thankfully, few and never sustained. As bad as the Great “Recession” had been, after more than a year of it the global economy found a bottom and lower state of equilibrium anyway.

This, however, is something else altogether – obviously we can’t expect anything at all like the middle eighties to save us. Furthermore, those prior bouts of outright deflation showed up at the end of those specific, nasty contractions.

These have appeared right from the beginning. At the very least, it complicates the situation for what everyone hopes will be a “V” shaped recovery since price discounting like this also takes time to ruin more beyond the initial shape (second and third order negative effects).

There was certainly a “V” beginning in 1983, but we are on the total opposite side of the monetary spectrum. And only an “L” from 2009 forward. Neither of those cut nearly as deep as this one appears to have already. It doesn’t mean the worst case, necessarily, but if you’re holding out for the best possible outcome or even something close to it, Jay Powell’s goal and scenario, these are numbers you just don’t want to see. Link

Interesting article.

I'm not sure if I quite agree with them on the extent of inflation from 2022. I think it will be a mild form of inflation.

Something that needs to be factored in are the profound demographic shifts underway which have deflationary tendencies.

More specifically, what I am referring to here is the profound ageing that is occurring in many western countries, which will dampen demand in the economy going forward . Also factor in that for younger people, the cost of living is very high, mainly due to obscene housing costs. This limits discretionary income spending.

Also in NZ much of the higher natural population growth is occurring in poorer parts of society.

I dont think we will see inflation. I think in most western countries fewer and fewer babies are being born, on average people dont want or cant afford to have 5 kids like they use to in the baby boom years.

Which means less demand for everything once they grow up. Demographics is huge. But on the other hand im just a smuck on the internet so im most likely wrong haha

You're an INFP (Myer Briggs) Avocado (that's good)

Inflation is a monetary product. It largely depends on amount of available money. the M3 has been expanding like mad since 1990s. Its growth rate is much much faster than any reduction in future human population. So while real consumption dynamics are probably as you describe, the need for money is even greater. Have you considered the money that needs to be printed to pay health care, welfare and pension of a globally aging population? how governments will do that? they will print money. THey will do it as long as it works until their currency collapses. Now, the trillion dollar question is when? that is what you cannot predict, is it going to be this time? in 40 years time? in 100 years time? who knows.

Except it isn't really printed, it is borrowed into existence. The ability to pay is a part of that calculation. Borrowing has been slowing, hence a lack of liquidity leading to convulsions. I don't think governments can borrow enough to replace that lost in the private sector.

"economic shock driving an even deeper wedge between low- and high-income workers,"

I think the shock in NZ is driving a wedge between 'employed' and 'not employed'.

So fix for a year to 18 months, then fix for 5?

All eyes should be on what happens in China as order books for the next 6 months dry up. In a capitalist country they would see substantial job losses and a probable change of government. In a communist country they would pretend nothing was wrong and go on producing as before at a large loss. Their current capitalist country run by communists model is going to be interesting to observe (from as far away as possible). Hopefully the technocrats in the CCP will be working hard on a good solution and all the best to them.

If China has a big stutter, then the rest of the world catches an external supply shock and does not need a global recovery to induce inflation.

Capitalist country, run centrally, with a heavy dose of nationalism and imperialist ambitions.

All this is so 100 years ago. Passé.

The whole problem is going to be papered over. It banks won't need bailing as the end user will be. It is fake news that the RBNZ QE has to be paid back and just can't be written off. They just don't want people on the street to understand the world's ultimate scam of money printing. A system controlled by elites and where the value is pure illusion. Money is no different to bitcoin.

This is a very positive outlook from MS. The arguments are good. You dont get to work there without being pretty smart. Its clear on what the issue is. Insufficient demand due to weak and insecure incomes. It's clear on the reasons. Trade, otherwise known as global wage arbitrage. Excessive corp power and big Tech. Imop the big one is Trade...Strong reliable income growth will create demand promote investment and with it may come inflation. The good thing is everyone agrees on the problem. We know the causes. We have the tools needed for change. It all comes down to execution. Let's hope we havn't forgotten how to get things done.

Of course MS is referring to the US and the rest of the world. And so am I. NZ has it's own unique situation and it will require a pretty special mix of politics and policy to get us out of the mess we are in.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.