The Opportunities Party (TOP) is calling for the Government to enable the Reserve Bank (RBNZ) to give people cash to either repay their debt or use as they please if they’re debt-free.

The idea is for this cash payment/debt jubilee duo to be used temporarily to stimulate the economy and keep inflation buoyed in line with the RBNZ’s mandate.

Speaking to interest.co.nz, TOP Leader Geoff Simmons suggested the RBNZ could pay everyone $250 a week for six months - tweaking the value and duration of the policy as need-be.

Why? Simmons noted even RBNZ Governor Adrian Orr recognised the model of monetary policy being used by the central bank is benefiting asset owners the most.

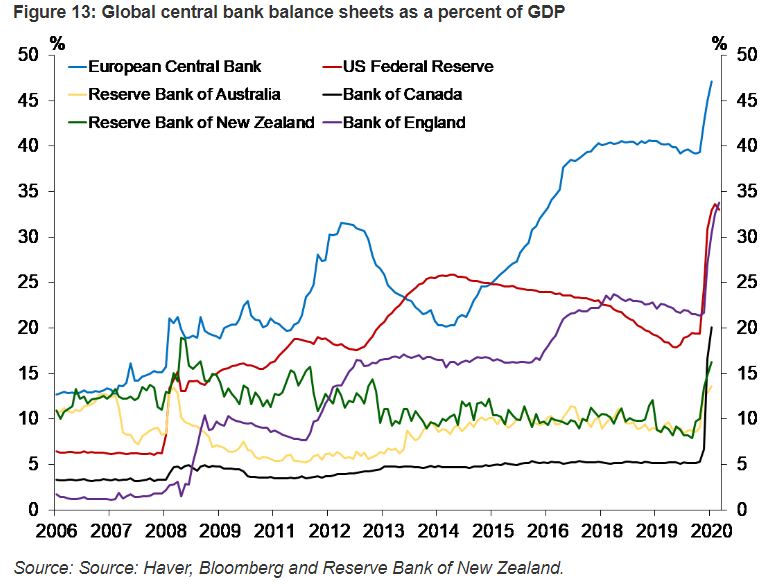

The RBNZ has committed to buying up to $100 billion of mostly New Zealand Government Bonds from the secondary market via its quantitative easing (QE) programme. It’s also preparing to cut the Official Cash Rate into negative territory and lend more to banks at cheap rates through a new facility.

The RBNZ’s aim is to push interest rates even lower to encourage businesses and households to borrow more and invest, as well as support those under pressure servicing their debt.

‘QE for the people’

However, Simmons said this legally mandated model relied on a “trickle down” effect, “which has all sorts of distributional impacts”.

Instead of the RBNZ attempting to reach its inflation and employment targets via the banking system, Simmons suggested it could “do QE for the people”.

A weekly cash payment of $250, given to New Zealand’s working age population for six months for example, would cost around $20 billion.

Simmons recognised this was a lot (the wage subsidy is expected to cost $14 billion by way of context), but again noted the $100 billion QE programme is benefiting asset owners the most.

He said this should be “raising a red flag” given New Zealand already has a housing bubble and inequality problem.

The fact property gets favourable tax treatment and banks like lending against it, adds to the argument much of this $100 billion will flow into the housing market.

Household debt an economic handbrake

Simmons said the advantage of requiring recipients of the universal payment to use it to repay debt, excluding student debt, was that it allows a “reset” within the banking system.

Because debt is an engine for growth in our economy, it has accumulated over time. However Simmons maintained we’re at the point where the burden of repaying this debt is so great, it acts as a brake on the economy.

In this sense, he believed directing much of that $20 billion towards repaying the $223 billion of consumer and housing loans households have, would free up resources in the economy.

With inflation being stubbornly low for some years now, Simmons didn’t see hyper-inflation as a risk.

Asked whether following this “reset”, New Zealanders would get right back to taking out debt to buy houses at higher prices, Simmons said he expected household debt levels to bounce back to current levels over time, but not immediately during this period of uncertainty.

“That’s why ancient civilisations in the past had regular debt jubilees. They had these sorts of things to constantly allow a reset within the system, because there is always going to be that pressure to build up debt,” he said.

Some govt debt should be written off

Simmons’ cash payment/debt jubilee policy inherently relies on Treasury and the RBNZ working more closely together.

The RBNZ argues that by buying New Zealand Government Bonds from banks and other bondholders, rather than directly from the Treasury, it’s ensuring operational independence.

In other words, Treasury is issuing more bonds to pay for government policies like the wage subsidy. And the RBNZ is buying up to 60% of these bonds from the secondary market to reduce interest rates to meet its inflation and employment targets, and also to ensure the market functions smoothly. Finance Minister Grant Robertson isn’t telling the RBNZ it must buy X amount of debt to fund a certain policy.

Nonetheless, Simmons maintained the contested split between monetary and fiscal policy had passed its use by date.

“We have reached the limits of the usefulness of current monetary policy,” he said.

“I can’t see any reason why we are using banks as an intermediary at the moment for government debt. Why can’t the RBNZ just purchase it [bonds] straight off the Treasury and just write it off?”

Simmons recognised this could see New Zealand punished by foreign financial markets. It would also essentially give “people like Winston Peters a blank cheque book”.

Therefore, he maintained institutions and frameworks would have to be developed to ensure any writing off of government debt was done in a considered way.

Simmons couldn’t say exactly how this could be done safely and with appropriate accountability, but said the time was right to do some “empiric experimentation”.

QE ‘blindly imported’

“Has QE actually been evaluated from when it’s been trialled around the world, or are we just blindly importing this idea from overseas?” Simmons said, pointing out that overseas experience suggests it won’t be temporary.

Indeed, RBNZ Assistant Governor Christian Hawkesby in a speech delivered on Thursday said, following the 2008 Global Financial Crisis, central bank balance sheets have remained relatively large for a prolonged period.

“It is not necessarily the case that central bank balance sheets should revert to their former size. It will be a case of what is optimal in the future to enable central banks to fulfil their remits,” Hawkesby said.

Simmons’ ideas unsupported by incumbents

Finance Minister Grant Robertson has indicated an unwillingness (pre-election at least) to making the sorts of fairly significant changes advocated for by Simmons.

He earlier this month told interest.co.nz he wasn’t worried about QE causing major asset price inflation.

Robertson said now was a good time to talk about whether monetary policy was fit for purpose, but was “satisfied we’ve got the environment we need”.

In May he said he wouldn’t look to the RBNZ to print money for specific government policies.

Orr a couple of weeks ago said the current set-up whereby the RBNZ buys bonds from the secondary market, not directly from Treasury, was working well. Hawkesby also stressed the importance of operational independence.

However Orr back in May expressed some openness towards the RBNZ buying bonds directly from Treasury for monetary policy purposes, saying it could be “achievable” if done transparently, for the right purpose and with the right structures in place.

The Bank of England and Bank of Indonesia have gone down this path, with even a former Credit Suisse Asia-Pacific managing director, Sean Keane, being among those to say the peak period of central bank independence is ending.

265 Comments

I always wondered how deflation could ever be a serious problem. Surely this is the solution to deflation; print money and give it to people. Either it will cause inflation or it will make us all rich (it will of course do the former). Low interest rates etc just isn’t working and are causing all sorts of other problems.

Helicopter money to create inflation is different to helicopter money to stimulate the economy isn’t it? In my mind if inflation is running at 0% or less then the problem must be that the money supply isn’t keeping up with the growth of the economy. It sounds easy to fix.

This sort of thing will undermine trust in government fiat currency in the long run.

An an aside, Geoff thinks that New Zealand’s fresh water is owned by Maori because it wasn’t handed over to the Crown in the Treaty.

Surely a wasted vote given that they are polling at 0.5% -1.5% with no electorate seat.

Fair question with regard to DD's point.

In regard to Simmons' point, his argument seems to be based on the fact we are currently giving away our water to foreign companies solely to avoid having to address the "who owns the water" question. If we can't answer that question should we not just agree that somebody in NZ gets money for the water than us just giving it away? I get the unfairness that I, as a Pakeha, would not benefit while another group I live alongside would, but also see the irony of DD's post on a thread about how QE benefits one group, property owners, at the expense of others.

Race is very much relevant when it comes to the race-based resource allocation that Geoff supports. Race should be irrelevant, but it isn’t for him. Geoff is fixated with it. Another example - His proposed land tax wouldn’t apply to Maori land, but the rest of would be subjected to it. So many layers of irrational.

I think it is immoral to charge anyone rent for their own land, Maori or not. But I suppose this, and one’s appetite for race-based policy, depends on one’s ethics, or lack there of. I don’t, for example, think it is unethical for the Government, supposedly comprised of foreign invaders, to impose income tax on Maori along with everyone else.

And I don’t consider the non-Maori New Zealanders of today, nor the Crown or democratically elected Government, to be invading thieves. No more so than I consider today’s Maori to be invading thieves on account of the tribal conquest and pillaging that their ancestors practiced.

No, I'm not referring Moriori. Pre-colonisation, inter-tribal warfare and land seizure was commonplace among Maori. There was no concept of a unified Maori nation at that point. I'm not going to try hold their descendants accountable for that or call them thieves.

Even though nobody alive today had their land confiscated, I am happy for the Treaty Settlement process to address legitimate grievances. Logically though we should also be figuring out which tribes stole land from other tribes and compensating their ancestors accordingly. There is actually quite a good oral record of this, but I don't think going down this route is a good idea. A very small portion of land was confiscated by the Crown without compensation. It is actually amazing how much of NZ is Maori Freehold Land, in part to address this. https://www.maorilandonline.govt.nz/gis/map/search.htm

Today we are one country. I firmly believe in equality under the law, regardless of when your ancestors arrived. That means no race-based water allocation, and no tax exemption based on race. Do you think either of these things are justified?

The thieves always want to move on and forget the past. The land acquired under the Maori Land Court was in reality confiscation. 10 Maori would claim to be the owners, normally the local drunks, they could then enter into a sale for a pittance of the land's value. Internal disputes between the tribes was within the same race, nothing to do with Crown theft of land from those who inhabited when taken by the Crown. Especially given the rights afforded under the treaty of Waitangi. This Maori need to move and we are all one people is BS. For that to happen all non-Maori should have their land confiscated as well and have to buy it again. Then we will all be the same.

You’re not making any sense. Emotions seem to be clouding your judgement.

When you say “thieves” are you referring to the small proportion of long-dead colonisers that didn’t buy their land fair and square, or the long-dead Maori that took land through tribal conquest? Either way, none of these thieves are alive today. Almost 30% of New Zealanders weren’t even born here - their ancestors certainly didn’t steal any land here.

Some of my ancestors were Irish serfs - I’m not going to cry about that fact - I’m not the one that had anything taken from me.

My reference is to the Crown who confiscated, stole and through puppet courts instituted fake purchasers from Maori who were not the owners. Hence the need to develop the Torrens system of land registration so as to avoid investigations to the validity of land purchases. Usual common law is that a person cannot give better title than that which they possess. Of course that would impugn land sales in NZ which are all predicated on Crown theft and Crown ownership of the fee simple. The torrens system was formulated for the theft of Australia by the Crown and then adopted in NZ. This differs from the deeds system used in the UK as the torrens system allows a sale by a thief to a bone fide purchaser for value to withstand a challenge from the victim or their estate.

Why would you cry for Irish serfs? They have Ireland which was stolen by the British and subsequently returned to them.

Oh, so not the long-dead tribal conquerors? Cool.

Nobody breathing in this country stole any land. Nobody breathing in this country had any land stolen from them. We’re all either immigrants or descendants of immigrants. The sooner you realise that the sooner you’ll be able to stop feeling like a victim.

If you have something that you know was stolen and the victim's descendants are still alive would you give it to those descendant's?

It's a bit like those people who buy a sofa from a deceased estate and find $10,000 hidden in the cushion. They could justify keeping the money (e.g. I bought the sofa so the money's really mine, or the owner is dead so its not really stealing) but those with morals return it to the deceased's children. I suppose you would keep it.

I didn’t steal it. They didn’t have it stolen from them. You are talking about people that don’t exist - they are dead. You are not your ancestors. I assume you own land and am sure you didn’t steal it - no different to me. I don’t expect descendants of Māori conquerors to give land back to the descendants of those Māori who had their land conquered.

You seem to vastly over-estimate how much land was “stolen”. The vast majority was purchased on fair terms (95%). And the “stolen” land being addressed through the Treaty settlements was actually taken legally (although immorally) through the New Zealand Settlements Act.

Legal and moral are different. The confiscations were legal but immoral. The sofa analogy is absurd. Finding money in a couch is analogous to historic land theft? What!? But if I purchased a sofa I wouldn’t want my descendants to feel obligated to give it to the descendants of the person I purchased it from. How do you like that analogy? 95% of land was purchased on fair terms - the Treaty settlements address the rest.

The thieves made laws to say it is not theft, 150 years later realize they still look like thieves so set up their own kangaroo court to resolve the thefts and pay what they think is fair compensation to claimants who represent nobody.

All sorted now so stop bringing up the pesky past.

That is the "whoosh" passing over your heads.

Give you a heads up HeavyG, there are no fullblood maori left alive in NZ today, The land was sold in many cases (after it was stolen from another indigenous owner). Maybe there should be part payments of rates and part ownership of water based on genealogy?.. Good luck with that can of worms.

Get some knowledge in you. The so called "sales" were conducted with anyone presenting as the owner even if the were not. The Maori Land Court was the biggest theft ever. As for your Moriori reference, that has been shown to be BS to make Pakeha feel like their actions were justice rather than theft. No descendant is full blood of a single ancestor, you're not even full blood of your parent, however you still inherit the rights and property (including legal claims) of your ancestors/parents.

Exactly my point above. Calling something by race is a deflection. It's all a matter of law and the crown has been proven to be on the wrong side of it over and over. Maori entities have been damn patient and persistent in waiting for justice and will no doubt continue. I work for a relatively small trust that took almost exactly 100 years to make first progress to any sort of redress, but it was always going to come because the law was always on their side. Really short version is their land was surveyed against their wishes, 20% taken as survey costs.

Haha.. stop banging the "old moriori myth" drum.. I never mentioned it. I was actually referring to inter iwi battles that took land from each other via conquest. Many cases exist of one iwi displacing another before colonialism occurred. There are many cases of that happening around the Central Plateau and the Eastern Bay area, Ngati Pikiau, Ngati Kuhungunu, Whakatohea, Tuwharetoa/Te Arawa/Ngati Awa etc.

Contrary to what some would have us believe precolonial life in NZ was not some utopian existence of peace and coexistence - it was tribalism and competition for resources, slavery was actively practiced and there was constant tension between neighboring iwi

Yeah.. perfect. Take all the technology and medical systems too. The remaining inhabitants have their life-spans halved and everyone who leaves doesn't have to listen to the grievance industry anymore.

BTW how do you propose to designate who is Maori and who is non-Maori?

The treaty industry is set up to ignore reality. How were the applicants tot he tribunal authorised to make a claim? Were they elected democratically by the members of tribes they claim to represent?. You know nothing of the reality and process and are merely repeating the Crown's talking points, even the "you can stop complaining now".

If the applicants can't get their application together after all this time - RE: Ngati porou and co then it's the applicants problem .. not the Crowns. Even now in the 21st century we have tribalism alive and well detracting from from an overall advantageous outcome. Stop blaming the process and start looking at the internal dysfunction amongst your hapu. While you're at it stop blaming the crown for the appalling incarceration, domestic violence and child mortality rates. Maoridom has some deepseated and ingrained problems and the sooner they are admitted the better for all

It's got nothing to do with grievances or compensation and everything to do with the truth. What you believe to be the "truth" is a lie. Yet you prefer to live in ignorance as that fits your world view that there was no widespread theft of land from Maori, no murder of Maori and no destruction of their communities that ravaged Maori resulting in the negative outcomes they experience today. The "stop complaining" chant is your mantra to avoid having to actually do some research into what really happened.

The complaining will stop when you acknowledge what actually happened. I prefer the hard core racists because they at least acknowledge the truth (i.e. we screwed you Maori hard) and then go on to say "get over it". You fairy land dreamers are the problem as you seek to deny the past and say "there's nothing to get over so stop complaining".

Own water? Which water? Water molecules are continually moving through the hydrological cycle. The water in the river today was evaporated from the Tasman sea, maybe the Indian ocean. Which molecules can anyone "own"? Perhaps they can find them somewhere in the pacific ocean and retrieve them?

Sell outs with no authority to settle on behalf of Ngai Tahu let alone all Maori. back in the day you bought land of the local Maori drunk and claimed it was a real purchase. Now you give some money to the person with the biggest greenstone around their neck and think it's all good.

BWAAAHAHAHA... man you sure are one unhappy camper. There's that tribalism kicking in. Tell me, how come there are only two iwi called "Ngai"? Were they the smart ones? I've heard Ngai Tahu were the navigators and tohunga, Ngai Tuhoe were the healers. Were the "Ngati's" the squaddies?

Telling porkies again Hook:

https://www.govt.nz/treaty-settlement-documents/ngati-awa/ngati-awa-dee….

Living up to your "long porkies" label.

I may be wrong but have a vague recollection that if the people saying they supported TOP policies before the last election voted for them they would have got over 5% but because people thought it might be a wasted vote they didn't vote for their preference, and lo and behold they missed the cut. Democracy's a funny thing.

...and the real world consequences of getting people well and truly hooked on their extra $250 a week and then taking it away? Sounds like a drug pusher to me.

Would the government then supply support services to help people get off this addiction, just cut them off cold, or go soft and keep on handing it out?

I've got a long shopping list of wants that would love an unexpected $6k.

And no, I think very few of the rich people really earned it. Just a case of supply and demand (skills) and not so much to do with hard work, however you manage that.

I just don't see how you can give something like this then not expect some real damage when you turn the tap off again i.e. if you're going to start something like this, then there's no going back.

Give a man a fish/teach a man to fish. Long term what is more fulfilling to the individual and to society and our communities?

What is that definition? The money supply has to grow as the economy grows, otherwise the total value of the economy cannot increase. Can you think of a better way to achieve that than inflation controlled fiat currency? I guess you could argue that fiat should be controlled at 0% inflation rather than 2%.

Is the purpose of money to allow an easy exchange of goods and services or to hold value over a long period of time? It’s not easy to achieve both of those IMO, fiat is doing a pretty good job in most countries.

“ Money is any object that is generally accepted as payment for goods and services and repayment of debts in a given country or socio-economic context. The main functions of money are distinguished as: a medium of exchange; a unit of account; a store of value; and, occasionally, a standard of deferred payment.”

Money needs to be a store of value which fiat will never be. The value of the economy is not determined by how much money we have created, otherwise we could just print our way to riches. It’s that kind of assumption that is causing the issues we are seeing manifest now.

I heard an apt joke about it - fiat money is like masturbation, it’s fun at the start but in the end you realise you’ve just screwed yourself.

I’d sounds like your advocating for money with a fixed supply. The problem is the deflationary aspect - why would you ever spend it if it’s purchasing power increases as the economy grows (even population fuelled growth). This is why I think it’s very difficult to achieve both a median of exchange and a long term store of value.

I’d sounds like your advocating for money with a fixed supply. The problem is the deflationary aspect - why would you ever spend it if it’s purchasing power increases as the economy grows (even population fuelled growth). This is why I think it’s very difficult to achieve both a median of exchange and a long term store of value.

Which is an argument for Bitcoin as a store of value first and medium of exchange second.

C'mon JC, Bitcoin is similar gold in that it's only worth what the next buyer wants to pay for it. BC is not related to any currency, is only backed by speculation and thus is the ultimate fiat currency.. an illusion backed by illusionists. It most certainly isn't a store of value.. ask any of the poor saps that bought it at 20K US. At least gold is a tangible asset, admittedly hard to buy your groceries with but if you own the actual metal it is "real"

I can't see how people get so caught up on this weird hypothetical. Human beings are subject to time. It doesn't matter if the bread will be half as expensive vs my savings in six months time. I'm hungry now. It doesn't matter if the movie tickets will cost half as much vs my savings in six weeks time, I'm bored now. This weird idea that if money gradually went up in value then people would stop spending it makes no sense.

"why would you ever spend it if it's purchasing power increases" Because stuff now is better than "cheaper" stuff never.

Because the money created by the RBNZ is funneled into the trading banks who then lend it out to importers. If you can't create money, especially in a CA deficit like ours then the system grinds to a halt because we import more than we export. Imports would be severely reduced. Yes we might manufacture more products in NZ but they'd be so expensive no one could afford them. Do you remember the days when you had to get Govt permission to purchase a car from overseas?

You have just described perfectly how things have got out of whack and how we are living well beyond our means.

I hope you realise we can’t live beyond our means forever? We import more than we export because we create money out of thin air. This will eventually catch up with any country. Magic beans are just that.

OK, so when we forego our flatscreen TVs, our coffee machines, our EVs, most of our clothing, all our ICE vehicles, trains, ships, defence equipment requirements, all our whiteware, half our food (all of the out of season stuff), all our machinery and heavy industry durable inputs, aircraft, medicines, computers and consumer electronics, fuel, glass, most of our steel, all our heavy Ag processing equipment, all our telecom equipment,.. are you getting the picture?? Better plant those beans son.. we're gonna need them

Those without debt won't 'splash the cash'. They'll save it.

Most people will have some sort of home-made Excell spreadsheet that tells them ( and even if they'd don't, they instinctively know it) that the money they'd saved for retirement was going to get them through to 95 (or whatever) with interest rates at 7.0%. At 3.5% it'll get them to 75, and at 1.75%...well, not far at all. So they won't spend. That's what happens when the Demographic change occurs to society, and it has (2011 onwards).

The lower rates go, the more people will save - no matter where it comes from.

Exactly, so we have to target the debt write off to get the outcome we want then. That outcome being more allocation/expenditure into the real economy (i.e., not the FIRE economy). And so, the first logical port of call for any government write off, is student debt. Overnight every individual with a student debt will have 12% more after tax in their wallet. That 12% is proportional to their current earnings - so such debt relief is equitable (whereas a fixed sum $250 per week isn't). And the young are exactly the right age demographic to target - they are our future spenders and business builders, not the already cashed up/elderly.

Next cab off the rank should be a write off of WINZ debt - as this captures a younger population who are less likely to benefit from the student debt write off.

I really don't understand why intelligent, trained economists fail to think practically and sensibly - especially if they have specific concern for intergenerational equity.

As at 2018, the total balance of all this student debt is NZ$15.8 billion. This puts the average student loan balance at NZ$22,065. The median student loan balance is NZ$15,939.

.

Thanks, but it is so obvious, it's embarrassing to our political class that I'm sitting here in my lounge suggesting it.

And the thing about an overnight student debt write off is that I doubt we'd be 'punished' by global financial markets for it. In fact I would bet that the action would be repeated all over the world where the student debt is 'owned' by the government..

Kate, when the stock market was at its low point due to COVID-19 a few months ago I said “There will be a recovery at the end of this. A prudent fund manager will be converting more liquid assets and buying on the way down so that when the recovery arrives the fund gains more than it lost.”

You disagreed and said “And 'converting more liquid assets and buying on the way down' - LOL - and (even better) ... following this greatest crash in living memory, hey, you're going to become richer than you were before!!!! Companies go bust - shares become worthless. I'd go for fixed interest funds (capital preservation) until the dust starts to settle.”

The stock price recovery is now complete and my aggressive growth KiwiSaver is now well up on where it was before the downturn just a few months ago. Your approach would’ve locked in the losses and totally missed the recovery.

Would you like to amend your outlook?

https://www.interest.co.nz/news/104176/nz-super-fund-ceo-has-dropped-89…

Two points.. the ones that go bust won't be listed or if they are they're "penny dreadfuls" no right minded fund manager is buying, The other thing, DD is correct, plenty of money made in the latest correction and there will be with the next one. People that followed your advice just missed a golden opportunity that doesn't happen often, to their long term financial detriment

Of course some will go bust and become worthless. This applies in good times and bad. But selling in the dip has proven to be a mistake once again. Do you deny that anyone who converted their KiwiSaver into cash or conservative funds a few months ago essentially locked in the losses and missed the overall price recovery?

What I am saying is I don't understand your argument. Your premise assumes all exits (fund movements) occurred at the same time (i.e., once all losses to be had had been had) and none of the exits re-entered a higher risk fund when the markets on the way up were less than or equal to their exit price.

No, none of those things are assumed. What I (and virtually all fund managers) am saying is that if you are in a growth fund and the market falls, you are best to stay put in that growth fund instead of irrationally converting into safer funds (like fixed interest) in an effort to stem losses, as you suggested in your earlier post. As has been demonstrated over the past few months, markets recover, and if you remain in the growth fund you receive the benefit of that recovery. If you have a competent fund manager, they would’ve been buying on the way down as well so that you end up better off than you were before the downturn, as was the case for me this time. Conversely, if you convert into a conservative fund after the downturn, you miss the recovery. Anyone that took your advice and converted into a fixed interest fund in the depths of the downturn a few months ago would be kicking themselves today.

As has been demonstrated over the past few months, markets recover, and if you remain in the growth fund you receive the benefit of that recovery.

Nope. You're making the assumption that the market has gone up so it has 'recovered' (and you've only benefitted if you've realized any gains). The same phenomenon happened in the great depression before things really went tits up.

Actually the market HAS recovered and what DD is saying is that people (Kiwisavers and retail investors) who exited on the down going curve will be worse off than if they'd just stayed the course. You are ignoring the facts.. DJI at a record high, NZX fully recovered to Feb levels. He's not talking about realized gains, he's talking about actual realized losses experienced by people who panicked and shifted into conservative/cash funds who missed the recovery. Had they stayed in their growth oriented funds they'd be no worse off now and may (depending on fund and fund manager) be better off. Shifting to a conservative fund, there's a high likelihood they'll be worse off now.. probably significantly so

You don't have to miss the recovery! You just have to move money between funds. Get out when the signs look ominous and get back in when the rally looks like it might last for a while. I don't think I get an admin charge for moving between funds, do I? Might have to go check!

Oh, sounds easy, just be smarter than all the other traders out there and sell when the market is high and buy when the market is low. So simple! Please tell the Chief Executive of the NZ Super Fund to use this strategy, because he has stubbornly been sticking with the approach that I advocated above.

Please explain why you weren’t able to spot the bottom of the market a few months ago when it was the perfect time to buy growth stocks, yet you advocated people switch to fixed interest???? You suggested this on 20 March 2020, when the NZ market was at what we now know was its low and it was the right time to sell fixed interest and buy growth stocks. Strange, it’s almost like you had no clue the bottom had been reached along with pretty much everyone else...

The only thing we have evidence of is you saying to get into fixed interest (as if the market was going to fall further) right at the moment people should’ve been getting into growth funds as the market was actually about to shoot up by about 40%.

Did you buy growth assets on 20 March 2020? You would’ve gained about 40% by today if you had. Any sane person that knew the upswing was coming, as you claim it is so simple to do, would’ve taken advantage of this...

My growth fund is well up on 12 Feb 2020 and 2 March. Hindsight shows your relative was better off to stay put in growth in March - you realise they had the benefit of a significant upswing?

Glad you are happy with how it has all panned out for you. You will likely find this completely boring and all wrong-headed thinking, but here goes.

I moved not due to what the market was doing (rarely watch the stock market specifically), but rather what NZ/the world was doing - i.e., imposing flight/travel restrictions. In other words, as soon as there was no doubt the pandemic had gone global, to my mind it wasn't the time to be in a high risk fund. The relative wasn't in a fund but rather was investing via a brokerage. He explained he had lost $75K in the last week. But on further discussion it turned out he had only 'lost' unrealised capital gains and hadn't yet lost any of his earned income. My recommendation was to cash in on those unrealised gains and bank them, or withdraw his initial earned income and bank it - leaving the unrealised gains to continue betting on. It doesn't mean one has to cash out completely - just take the unrealised gains when/while you can. But lots of people don't operate that way, I know.

I do the same with my TAB account - the big wins get banked, lest I get too cocky :-). All my bets are modest and purely for the fun of it. I've only ever topped it up a couple of times in years - for example when the TAB was offering 'freebets' (two ways to win on a single bet) associated with the RWC competition.

As to my KS account - I'm still in a conservative fund. I'm only interested in capital retention/preservation. To me, the reason to be in a KS account is to get my employer and the governments contributions. I'll stay in conservative until the global pandemic and all the central bank actions associated with it is over.

Hahaha cmon Kate, do you really think you can actually pick when a "rally" looks sustainable? By then all the easy gains are off the table. If you do give me your address and I'll happily have you manage my portfolio. As for admin funds I don't know.. KS isn't a big part of what I invest through, maybe <2%

Most of the data to date seems to suggest people exited as the market declined very rapidly. Given the processing lags they would have booked most of the worst losses. Again due to processing lags any that switched back (haven't seen any figures) would probably still have entered at a higher level on the curve than they left. Overall it was an ill conceived move to shift funds. Much as any decision regarding market timing moves generally are. Play the timing game with money you don't mind losing.. not your retirement fund.

Yep, I'm picking the younger generation as winners. Us olds didn't pay for our education anyway, so really, the inequity is less than you'd like to portray. And, as I mentioned, WINZ debt should be next cab off the rank.

So, yes, for those of us in retirement, sitting in our debt-free household with a good paying job into our retirement to boot - get nothing because we need for nothing. Sounds eminently equitable to me.

You speak as if everyone’s wealth is determined by their age. This is what I don’t like about identity politics, you get lumped together whether your situation is the same or not. There are plenty of oldies who are doing it tough just as plenty of young folk who are doing well.

How about we either treat everyone equally or look at peoples individual needs instead?

Be honest - that's exactly what a student debt and WINZ debt write off would do - i.e., look at those most in need and provide appropriate relief.

Those plenty of oldies who are doing it tough aren't doing it as tough as the unemployed - as the level of Super has always exceeded the level of the Job Seeker benefit. Single person Super = $850/fortnight after tax. Single person Job Seeker = $500/fortnight after tax.

And if a superannuitant hadn't been able to make ends meet (i.e., struggled with cost-of-living) and had had to go to WINZ to borrow, say for a fridge replacement or a housing bond payment - then they too get a debt write off under my suggestion.

You may not need it gone, fair enough - but if it is gone you will have another 12% of your gross wage in your pocket, and we need you to use that for something far more productive and beneficial to the wider society than paying back your student loan debt.

It's not just about need, it's about the 12% of your gross wage doing something worthwhile, i.e., for the collective good.

It’s kind of the other way round Kate. Look at the pay equity deal that was passed. The gist was to pay people who do different work and made different choices the same. Equality is the same opportunity, equity is the same outcome. Hence why him saying your idea isn’t equitable (not equality for that matter).

The gist [of the pay equity legislation] was to pay people who do different work and made different choices the same.

I think the intent of pay equity legislation (and it was appropriately called pay equity, not pay equality) was to improve gender-based equity between employment sectors (i.e., typically male vs female dominated labour sectors/markets).

Yeah, I've heard the "equality of opportunity" mantra - it's another neoliberal era chant - and it's a ruse (i.e., it doesn't exist). Policy set to improve social equity (i.e., equitable outcomes for the whole of society) raises the prospect of better outcomes for those disadvantaged by the inequality of opportunity.

Perhaps not directly Fritz but as parents they certainly had to pay a significant chunk of their child's tertiary costs. A degree definitely makes a difference in the labour market.. as long as it's a worthwhile degree. I certainly don't hear any engineers, vets, Dr's, lawyers or other business professionals regretting their choice.

We didn't pay for any of our children's tertiary costs and neither did they qualify for allowances, as our parental income was too high. We did buy each of them a car to get to-from where they studied (both chose to study out-of-area). Our thought was, if they had chosen to study locally they would have had free food and lodging - and if they wanted independence, they needed to 'earn' it (or in their case 'borrow' it).

The ever-frugal first son finished his qualification and sold the car to pay off his loan. The never-frugal second son, wrote off the car going too fast on a back country road (no one but the car and the fence hurt, thank goodness) and learned the hard way about debt.

Now they're both ever-frugal :-)!

Well I guess the lesson there is "all's well that ends well". I'm glad son#2 wasn't hurt, actually I hope he went back to the farmer and learnt some fencing skills.. haha. Fact is Kate, the best lessons are those learnt when there are ramifications. Your sons learnt there are ramifications regarding choices so I think forgiving student debt removes some of those ramifications, even if the lessons learnt will only be imparted at a future time. At worst your sons learnt there are no free rides, very valuable in today's world

What about those who have been repaying or indeed have repaid their student debt. What if that repayment had a material effect on their ability to get on the property ladder?Just bad timing? Suck it up? That's the problem with all debt 'jubilees'the prudent and unlucky are punished.

Both our sons have fully repaid theirs. First son was 'annoyed' when second son's remaining loan went interest free. First son bought his first house at 21 and only needed a 5% deposit in those days. Second son purchased his at 27 and had to have a 10% deposit. There is only 18 months between them and still 'timing' was everything. It's just life.

Kate - I suggest the answer to your question is right next door to you

Here is the Economics Faculty promotional page from Massey University

The emphasis is (exclusively?) on Macro-Economics and policy studies

https://www.massey.ac.nz/massey/explore/departments/school-economics-fi…

I live in the world of Micro-Economics. Search on Micro-Economics in NZ and you find nothing

Search as you may the following site keeps appearing

http://economicsnz.blogspot.com - try reading that and despair

You are right in your proposals to forgive debt to Student Loans and WINZ debtors

That causes a destruction of the drive and effort and intellect on the part of those dragged down by debt for many years. Many will never rise out of the swamp they find themselves mired in. I could tell you that. But nobody ever asks. The economic world in NZ is overwhelmed by macro-economists who revel in producing and analising pretty big-pictures.

For comparison

I have been researching and documenting an article on the birth, rise and fall of IBM (International Business Machines) the founder of the digital age as we now know it. IBM became so large and powerful it exceeded the economies of many small to mid-sized countries. In 1970 the Department of Justice commenced Anti-Trust action against it. In 1980 CDC Control Data Corporation developed disk drives compatible with IBM mainframes. IBM responded by exercising its monopoly power and refusing to service any of its clients who installed CDC disk drives. The Anti-Trust action ran for 20 years and occupied so much drive of the executives of the company it failed to adapt to the evolution of Mini-Computers and PC1 and Microsoft. Today IBM has a market capitalisation of USD $115 billion while Microsoft has a market capitalisation of USD $1.65 trillion. That's what happens when the intellectual capacity of anything is dragged away from its core.

I could give you a number of such examples

Thanks, really interesting to get an opinion from someone trained in economics. The lens I view everything from is equity/fairness. I get really frustrated when talking with orthodox economists. They have so much dogma in their language - dogma in the sense of wee phrases (which I assume come from some theoretical background) that they spout out as if they were immutable laws. It is a complete paradox to me that the discipline of economics has been so bereft of disciplinary/body of knowledge development.

Thank goodness for people like you who are championing new methods and perspectives. Why are the rest of them holding so tight to their orthodox theories, when the evidence in front of them (let alone the suffering of the growing masses) is so blatantly observable.

Thanks... and I should be marking!

Yes, Geoff and Gareth are perfect examples - so I'm happy to name names :-). When they went for offsets and market pricing (i.e., polluter pays - the great neoliberal ideology) as the principle means to solve our environmental problems last election - they lost me.

kate... If you view everything from equity/fairness perspective, then your idea of forgiveness of student loans and WINZ loans does not make sense.

At least Tops idea of a UBI/debt jubilee is fair and equitable. ( Originally Steve Keens idea, I think )

If you want to forgive those loans as an act of charity, then fine, but I'd argue that you might be favouring some over others , which some might view as inequitable and unfair.

In the same way, RBNZ transferring wealth from savers to borrowers is also inequitable and unfair.

I dont have any issues with Charity..... if its worthy.

In regards to student loans... I have heard enuf anecdotal stories to think that quite a few students game the system. ie. there is an incentive to take the full entitlement of the interest free loan, even if they are not really that poor. ( maybe some of them even holiday oseas? )

I dont know anything about WINZ loans.... those people might be a more worthy cause for charity..

Nobody seems to care to much about hardworking people on the minimum wage who work long hours , live within their means, dont borrow and still manage to support their families.... i think there are plenty of them out there.

At least Tops idea of a UBI/debt jubilee is fair and equitable.

No, a UBI is equal, not necessarily equitable. But more to the point, in this article, Geoff Simmons is not suggesting a UBI; a $6,000 one-off injection is not an income, it's his idea of an economic stimulus.

I'm sure those students who have paid off their student debt will be charmed if others have their debt forgiven. To make it equitable perhaps we should repay those those who have paid off their debt. How far do you go back? Forgiving student debt is not the answer.

Sadly, $6,000 over a six month period is hardly rich - which is why 'flat rate' helicopter money doesn't work. Didn't work in the US, won't work here. Debt write off is great, but you have to target it at the right type of debt - e.g., such as educational debt and cost-of-living debt.

Ya and the hard worker is going to feel great about that. Why do people still go to work and pay tax? Hey Grant there is more on that tree, no not that one you just came from that one. Yes that one. Shake it off and bit more. Well done. Great idea that was. Maybe a plan would suite better.

Actually Kate, tradespeople don't incur "student debt". As apprentices they are paid slightly less than a fully qualified tradesperson but they don't pay to be trained. Some less than forward looking employers don't reimburse course fees but they then lose the qualified tradesperson on completion of their training. I'm afraid your reality is flawed

For starters I see having an HT licence as a qualification;

https://www.seek.co.nz/truck-driver-jobs

As for the can't afford a house in this market - who that doesn't already own one can? I'm pinning some hope on new types of ownership arrangements emerging as a means to address the affordability question;

https://thespinoff.co.nz/politics/24-07-2020/what-you-need-to-know-abou…

Doing a polytech course certainly doesn't make them tradesmen, those courses are designed to be precursors to apprenticeships. A tradesman is qualified when they recieve "Trade Certificate" or lvl 4 NZQA certification and complete a fixed term (normally 4/5 years) of training. If your sons didn't do both then they are "journeymen" NOT tradesmen.

Sorry, I'm using a wider sense of having a trade, as opposed to a profession. One got a diploma in film and television and went on to work up from camera operator through to director in that industry. The other wanted to work at sea and got a certificate in fishing, followed by a diploma in marine science which included PADI qual to Dive Master.

Geoff Simmons must have just read Michael Hudson's book: "And Forgive Them Their Debts". That's a decent historical treatment of the private debt problem and its last-known, tidy solution in Bronze Age palace economies. Modern finance has a lot more complexity and legalistic resistance to reform (a la Katharina Pistor) so I think Simmons' proposal needs more work. As pointed out above, TOP is unlikely to become the government this time around, so he will get some time for revision. Still, the debate is worthwhile and I look forward to debt jubilee V2.0.

Michael Hudson, yes a very wise man, it's just a shame that he is not more widely known in this country. He has his own website here for anyone interested.

https://michael-hudson.com/

Geoff is exactly right here. The entire economy is structured to flow money into the pockets of existing asset holders. So unsurprisingly we are starting to see and will see even more asset price inflation with the money being pumped in by the government.

Robertson has come out saying they will use the crisis to reset inequality. He is utterly failing at this and will actually make inequality worse because he fails (intentionally ignorant) to understand the tax/economic advantages driving inequality. At least Geoff recognises this.

The answer is massive changes to the tax system to change the game away from asset price appreciation being tax free and encouraging productive enterprise. Combined with giving those at the bottom who are currently lining up at all the food banks a way out of their situation.

Trickle down economics, which favour the rich, practised by ideologues working at central banks causes inequality. Regularly cutting interest rates in half dramatically increases the discounted present values of cash flows associated with assets and liabilities. Those without excess assets have been impoverished over the last four decades.

I dont think the answer is massive changes in the tax system. I think alot of gains in asset values is simply a function of Monetary inflation.

Simply taxing those assets on their inflationary values ( TOPS idea), will simply move another class of people towards hardship and struggles, in my view.

My own view is that we need a complete restructuring of the Monetary system.

Maybe its time to rethink the idea that the Private Banking sector can create credit, that can be used as Money..?

The UBI/ debt forgiveness idea might be a part of that, as would restructuring the tax system.

Trying to fix the current system simply with Taxes, in the name of equality, will bring unintended consequences.... and is just more of the same .

eg.. trying to force house prices down with taxes and yet allowing Monetary inflation to continue as it is.

The tax system is geared to ensure unproductive assets (that are more and more financialised, therefore tradeable) have very low taxes applied to them. This has driven up the price of those assets. At the same time, the tax system receives almost all of it's funds, from taxing productive enterprises. Our productivity rates have been dead for at least a decade. More and more productivity makes us richer. It's new businesses, higher and higher efficiencies, delivering more for less.

The prices of assets have risen dramatically. The price of productive work has not. This is because the above facts ensure funds (from borrowing) flows into unproductive industries. This is because it is tax efficient, it makes investors gain a higher rate of return. This should tell you that taxation forms the basis for many investment decisions.

I think we can all agree with the above - we only need to look at the a few graphs from the past decade or two to prove it. Your argument that it will somehow impoverish people (who own many assets??) doesn't really gel with me. If you hold enough assets to be taxed, surely you are doing well. That is the whole point.

I am not advocating for a change in the tax system to ensure equality - that is Robertsons problem and claim that he can do it by pushing money into the same economy that ensures the fruits go to the already wealthy. Which obviously won't work. I AM advocating for equality in taxes. I AM advocating for tax system which encourages productive investment. We don't have that at the moment, which is beyond stupid. It is a system that ensures the asset wealthy do not have to pay as much tax as those on wages or struggling businesses.

"I AM advocating for tax system which encourages productive investment"

And i repeat ... The key problem is resource limits... not tax

You cant have MORE so called productive enterprises without further Resource base drawdown....

The fruits of all that MONEY creation has to go to the balance sheet ... resource limits says it has to

(ie if the masses can suddenly spend like billionaries its collapses the resource base)

Much of higher productivity will come from efficiency gains now, not from extractive industries. I don't quite buy the "excessive draw down" argument, yes that is happening now. And I doubt we will get away from the current drawdown without massive consequences (climate change etc). However it is my hope (too optimistic?) that we can switch to draw down resources that are less scarce and damaging (see electric cars) with the aid of technology and deliver more "lightweight" productivity improvements (large increase in software delivery which is less resource intensive, for instance). I aren't advocating for us to restart heavy industries or coal mining when I talk about higher productivity. But you can look around and see a hell of a lot of work that can be done automatically and people redeployed to higher productive industries.

How about letting the system correct and allowing bad debt to be purged from the system the old fashion way? Might be painful for a while, but at least the pain would be felt mostly by the irresponsible lenders / borrowers that got us into this mess. Then we can return to some semblance of capitalism and the efficient allocation of resources, which should lead to more prosperity for all.

This would be the fairest way to deal with the current bubble and reduce the chances of the same thing happening in the future - but, sigh I suspect it won't win many votes!

As NZ runs current account deficits that only leaves the government as a source of money to repay household debt and the government must run continuous budget deficits for this to happen as sectoral balances explains.

https://gimms.org.uk/fact-sheets/sectoral-balances/

I agree completely with you, but you are dreaming, unfortunately. This would be the most correct course of action, but it just ain't going to happen.

It is much more tempting to keep selling houses to each other, and make money cheaper by the day, rather than to address the current economic imbalances. Orr's prescription to the alcoholic is to give him more and more alcohol. Very clever indeed.

It is baffling to see how the country can allow such un-elected public servants to wreck the economy and get away with it.

Listen to the silence

Two week ago Orr acknowedged lower interest rates advantage asset owners

Two weeks of silence

Simmons is the first economist to come out and take up the cudgel

Why are the intelligentsia and the academics and ALL the pet go-to macro-economists remaining silent

Are they bought and paid for?

what does not advantage the asset owners? pretty much any thing favours them as a collective group. We can damage some but their damage will be rewards for another class. the only thing that disadvantages them is innovation (and only if the said innovation survives their buying power early on). That truly distorts that valuation of the existing class of assets. It can render them worthless. Truly valuable skill is another great equalizer. But attaining it is harder than you think and requires a large list of prerequisite the hardest one being a hard working, committed, driven personality.

This helicopter money, will all end up in rich people bank accounts. In the pockets of supermarket owners, importers, fuel companies etc.

Alice in Wonderland is bored sitting on a riverbank with her sister. Noticing a talking, clothed white rabbit with a pocket watch run past, she follows it down a rabbit hole where she falls a long way to a curious hall with many locked doors of all sizes. She finds a little key to a door too small for her to fit through, but she sees a garden. She discovers a bottle on a table labelled "DRINK ME," the contents cause her to shrink too small to reach the key on the table. She eats a cake labelled "EAT ME"

How does land have a tax advantage over other physical assets like gold, machinery, vehicles etc? This is repeated so often by the likes of TOP but a logical explanation is never given.

Like other physical assets, the income from property (rent) is subject to income tax. And if land is sold within 5 years of being purchased, or purchased with the intention of selling for a profit, it is subject to “CGT”. Unlike other physical assets, it is subject to council rates, so is actually at a disadvantage from a tax perspective.

It's really the relative safety and stability of property, the ability to keep up with and sometimes exceed inflation, the willingness of banks to lend money on it, the straightforward earning potential of rental properties, the need for people to have a roof over their heads and the ease with which it can be seized and sold by the mortgagees that give it an advantage. There is no "tax advantage" but there are a few other advantages which is why it is so popular. The returns can be meagre at times though and it is not entirely without risk.

I think if you factor in the significant increase in ownership costs those figures would be closer. The CPI doesn't factor rates for a starter. In general house prices appreciate by about 7-8%/annum over the long term. Comparing CPI and housing increases is a bit disingenuous. Try comparing CPI increases and wage increases.. wages will lag. I'm self employed in a relatively short staffed industry and I can assure you my rates haven't moved by anywhere near the CPI increase, in '92 I charged about $35, now $90 and I'm paid a pile more than the same person in permanent employment so to be honest I think your calcs are a bit suspect

No, they are taxed exactly the same. The same tax provisions apply.

I’ll give you a practical example since you seem reluctant to do so.

(1) I purchase $1M of gold in 2019 with the intention of selling it at a profit. I sell it in 2020 for $1.1M and pay $33k on the profit.

(2) I purchase a $1M investment property in 2019 with the intention of selling it at a profit. I sell it in 2020 for $1.1M and pay $33k on the profit.

In the above example, the property investment is subject to $6k council rates, so is actually at a tax disadvantage in comparison to the gold.

You’re being very vague when explaining why you think land has a tax advantage. Be specific.

Yes you do. If you say that you didn’t purchase the gold with the intention of earning a profit, you don’t pay CGT. This is what happens in almost all cases where retail investors buy physical gold. Property is actually treated more harshly because there is no bright-line test for gold.

This scenario applies to all forms of gold, including bullion and coins, but if you purchase a gold chain and then sell it on trademe a year later for more than you purchased it, you won’t pay CGT. Same for boats, machinery and other physical assets.

The IRD assumes you purchased gold for the dominant purpose of disposal. The onus is on the taxpayer to prove otherwise. "It is important to bear in mind the distinction between motive and purpose; the reason why the taxpayer decided to acquire property with a view to disposal in due course is not relevant." There's a document on the IRD website that lays it all out with some examples of case law.

If both land and gold were purchased for profit, you pay tax. If they weren’t, you don’t.

In the first 5 years land is always deemed to have been purchased for profit, unlike gold, so it is at a tax disadvantage. Also much easier to hide a piece of gold than a piece of land.

“IRD does accept that in some situations a taxpayer’s dominant purpose in acquiring gold bullion may be other than disposal.“

This is a misconception. The same rules apply to both (with the exception that land has the tax disadvantage of being subject to the bright-line test), so if you purchased neither with the intention of earning a profit, you pay $0 tax for both (which is never the case for land within 5 years due to the bright-line test). If you purchased both with the intention of earning a profit, even after 5 years, you pay $167k tax on both.

Factually incorrect. The assumption is exactly the same as land. IRD does accept that in some situations a taxpayer’s dominant purpose in acquiring gold bullion may be other than disposal. Especially if the gold is in the form of jewellery.

In fact, if you are selling within 5 years, land is actually treated more harshly because the bright-line test mandates that the assumption must be that you purchased it for profit.

Not factually incorrect according to the IRD

“ IRD has concluded that the proceeds of selling gold bullion (gold bars, gold coins, certificates or units in gold) is taxable income. Tax legislation treats as income any amount a person earns from selling property the person has acquired with a purpose of disposal. IRD has reached this conclusion because gold bullion does not provide annual returns of income while held. Accordingly, the only way for a taxpayer to realise a return from an investment in gold bullion is for the person to sell it. IRD’s view is this indicates the person must have had a dominant purpose of disposal when the taxpayer acquired the gold.”

From the same website “IRD does accept that in some situations a taxpayer’s dominant purpose in acquiring gold bullion may be other than disposal.“. It is treated the same as land. If IRD takes you to task, you must show whether or not it was purchased for profit. If both land and gold were purchased for profit, you pay tax. If they weren’t, you don’t. Buy the gold in the form of simple jewellery or commemorative coins to be safe.

“ IRD does accept that in some situations a taxpayer’s dominant purpose in acquiring gold bullion may be other than disposal. However, the presumption is that this is not the case and the onus is on the taxpayer to provide evidence to rebut the presumption. IRD states that a taxpayer’s purpose in acquiring gold either as a long-term investment, a hedge against inflation, for portfolio diversification, or as a store of value outside the monetary system is not sufficient to rebut the presumption of a dominant purpose of disposal.”

Try to prove that you bought gold because you like to look at it and see how that goes.

Long story short and my last post on it is that in reality, you will always be taxed on gold.

Almost nobody pays CGT on physical gold when sold.

Seems like you agree that the same tax code requirements and rates apply to gold and land. But you believe that it is easier to dishonestly avoid CGT on gold in comparison to land because it is more difficult to claim that it wasn’t purchased for profit. I have three counter-points to this - (1) Within 5 years of purchase, land is always deemed to be for profit, unlike gold, for which you are allowed to make a case that it was not purchased for profit. (2) It is very easy to make a case that gold in the form of chains, bracelets etc is not for profit - an easy tax dodge. (3) Is it easier to hide ownership of a piece of land or a piece of gold? The answer to this is why almost nobody pays CGT when they sell physical gold.

The default position for land / housing is that you DIDN'T buy it for the sole purpose of disposal for profit.

The default position for bullion is that you DID buy it for the sole purpose of disposal for profit.

They have opposite default assumptions. In each case if IRD decides to investigate you, you'll need to show your evidence if you want to avoid paying tax. For gold bullion they're more likely to investigate you in the first place (not many people dispose of 1/2 million of gold bullion) than they are for land, and you've got a higher bar to reach in terms of being "not for disposal" than you do for land.

You surely agree that the same tax code requirements and rates apply to gold and land? You just think it is easier to dodge CGT on land in comparison to gold. If so, the answer is to make the bright-line test infinite instead of 5 years, not the imputed income stupidity that TOP tries to advocate.

It is much easier to hide gold than land. Also, within the first 5 years land is always subject to CGT, but gold can be argued with IRD. Also, not all gold is bullion - it is very easy to buy very high value quantity of gold in the form of jewellery an argue very convincingly that it was not purchased for profit (not that you’d ever need to debate this with IRD in the first place because they have no idea that you have the gold in the first place). Also, land is subject to annual council rates, unlike gold, so in addition to the bright-line test is actually at a tax disadvantage.

I think the reality is that you just buy bullion, tell yourself it wasn’t purchased for profit, and then when you sell it don’t pay CGT. IRD is none the wiser because they have no robust way of tracking or enforcing this. Not an honest thing to do, and not something I would do as I don’t hold physical gold, but this is what happens in reality.

If the IRD goes after gains on shares I think that is going to be a seriously resources hungry exercise, Yes they can look at broker accounts for managed portfolios but there will be many who manage their own affairs so it will be hard to police compliance.. it'll be interesting to see how it goes I guess

How about if you purchase gold, not with the idea of making a profit, but with the idea of having something that retains it's purchasing power once all the money printing has stopped?

I guess it depends how you measure "profit". If it's measured in a fiat currency that has been devalued, are you really making profit?

“ IRD has concluded that the proceeds of selling gold bullion (gold bars, gold coins, certificates or units in gold) is taxable income. Tax legislation treats as income any amount a person earns from selling property the person has acquired with a purpose of disposal. IRD has reached this conclusion because gold bullion does not provide annual returns of income while held. Accordingly, the only way for a taxpayer to realise a return from an investment in gold bullion is for the person to sell it. IRD’s view is this indicates the person must have had a dominant purpose of disposal when the taxpayer acquired the gold.”

From the same website “IRD does accept that in some situations a taxpayer’s dominant purpose in acquiring gold bullion may be other than disposal.“. It is treated the same as land. If IRD takes you to task, you must show whether or not it was purchased for profit. If both land and gold were purchased for profit, you pay tax. If they weren’t, you don’t. Buy the gold in the form of simple jewellery or commemorative coins to be safe.

This government is still trying to pump up property market by lowering interest rates and mortgage deferrals, the people who are in trouble are the ones paying most of what they earn on rent this is putting people into hardship and if property prices continues to be pumped up, more will be thrown into poverty. I know Teacher’s who won’t live in Auckland because it Is to expensive to buy or rent. This is not sustainable and will crash at some point. Any money the government has should be put into job creation and let the housing market find a more sustainable level

FHbs with young families who were caught on the wrong side of this occurrence are the ones facing the most hardship, not renters. Many stand to lose their deposits, equity and possibly their futures. Renters are well protected by the current regs.. Homebuyers not nearly so much. I personally feel very concerned about FHBs who just managed to scrape together a deposit and secure a home for themselves and their family only to see it potentially disappear.. it must be frightening.

Crazy! I started watching the interview thinking, bad idea, then in the middle of the interview, I thought he makes some valid points and in the end… I'm not so sure?

I find it amazing that the brightest minds in Economics worldwide really don't know the best way forward in something as important as the world economy, just crazy!

Yes, I find it kind of amazing too. I think the problem is that govts have set themselves a Mission Impossible: "Manage The Economy". I'd rather they just stop trying; Maintain some environmental protection regulations, and a basic safety net, but let prices and interest rates run wild.

Given how quickly capital and ideas, and even to an extent labour can slosh around the world these days the self corrections would be a lot quicker and individually less dramatic than decades of Mission Impossible manipulation followed by Rioting, Revolution and Resets.

Key quote about QE... "Banks get to clip the ticket".

The more this farce continues, the more it looks like the RBNZ is just protecting bankings foreign owners. Is it in the national interest to keep eveyone endlessly enslaved in debt...no. Should bank profit become more important than eveything...no also

I sure dont recall ever voting for either.

The helicopters that this big drop needs to come from will not be doing that anytime soon. They are the helicopters of all the giant corporations operating in this country without paying anywhere near their share of taxes. They are the helicopters of all the industry that has outsourced production of to the cheapest bidder to sell for maximum profit back here. They are the helicopters of investors owning vast numbers of houses, farming people till the time comes they can realise their untaxed gains. They are the helicopters of technology, automation and robotics stealing jobs.

It is now official: money does grow on trees. The solution to all economic imbalances is just to grow more money on more trees. Maybe Mugabe was right after all in his witchcraft magical thinking approach to the economy.

Every new day gives me the increasing confidence that I am right in running away from deposits with NZ banks as fast as I possibly can, and that this is the most cautious course of action.

It's nuts, but the current situation by reducing the OCR as low as they are, and going negative is also nuts. Savers are the ones who end up suffering, even though we teach children young to save. Instead we incentivize getting into debt and borrowing, to increase assets bubbles, over saving.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.