Labour’s finance spokesperson Grant Robertson says house price growth, and the wealth effect it creates, is not foundational to his “long-term” plan to sustainably grow the economy.

The Reserve Bank’s decision to lower interest rates in a bid to encourage more borrowing, investment and spending is adding fuel to an already heated housing market.

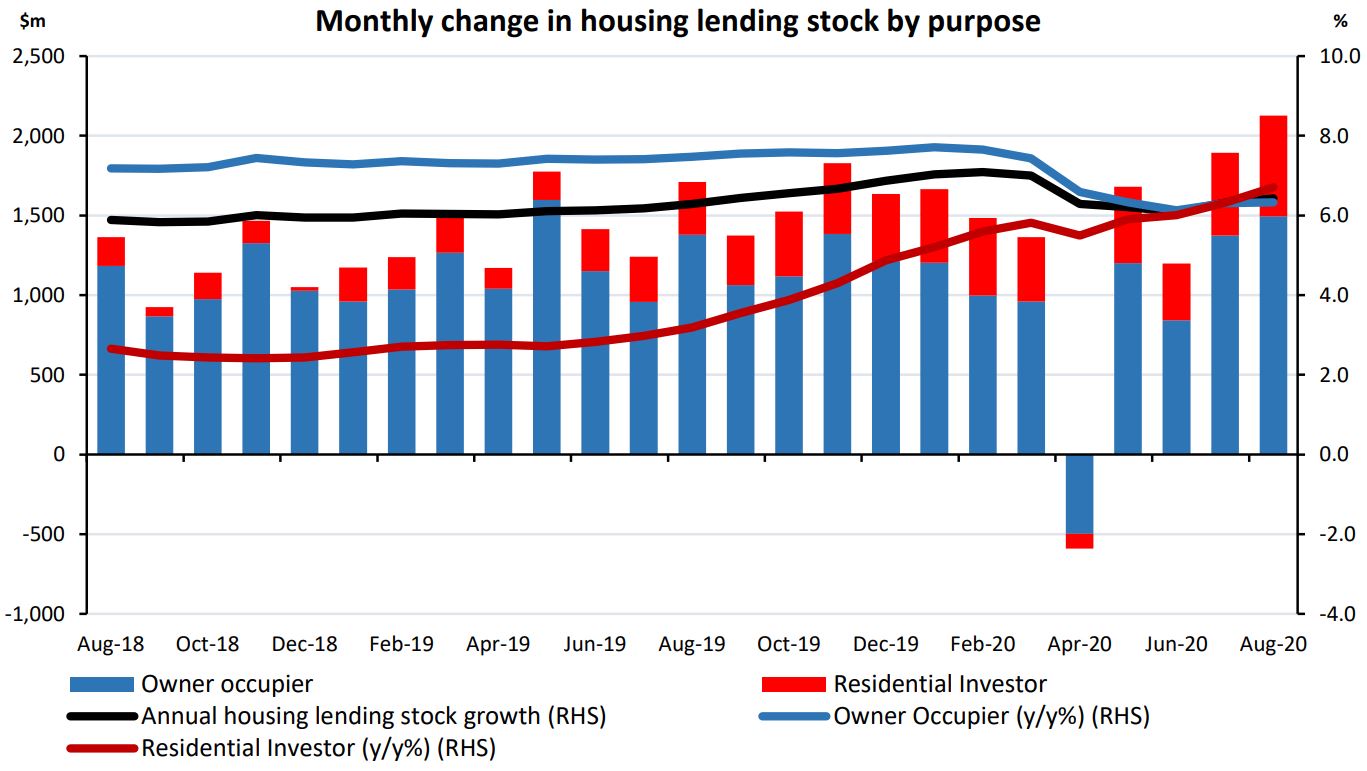

House prices have gone up 7.5% in the past year according to QV’s house price index, with mortgage lending reaching an all-time high.

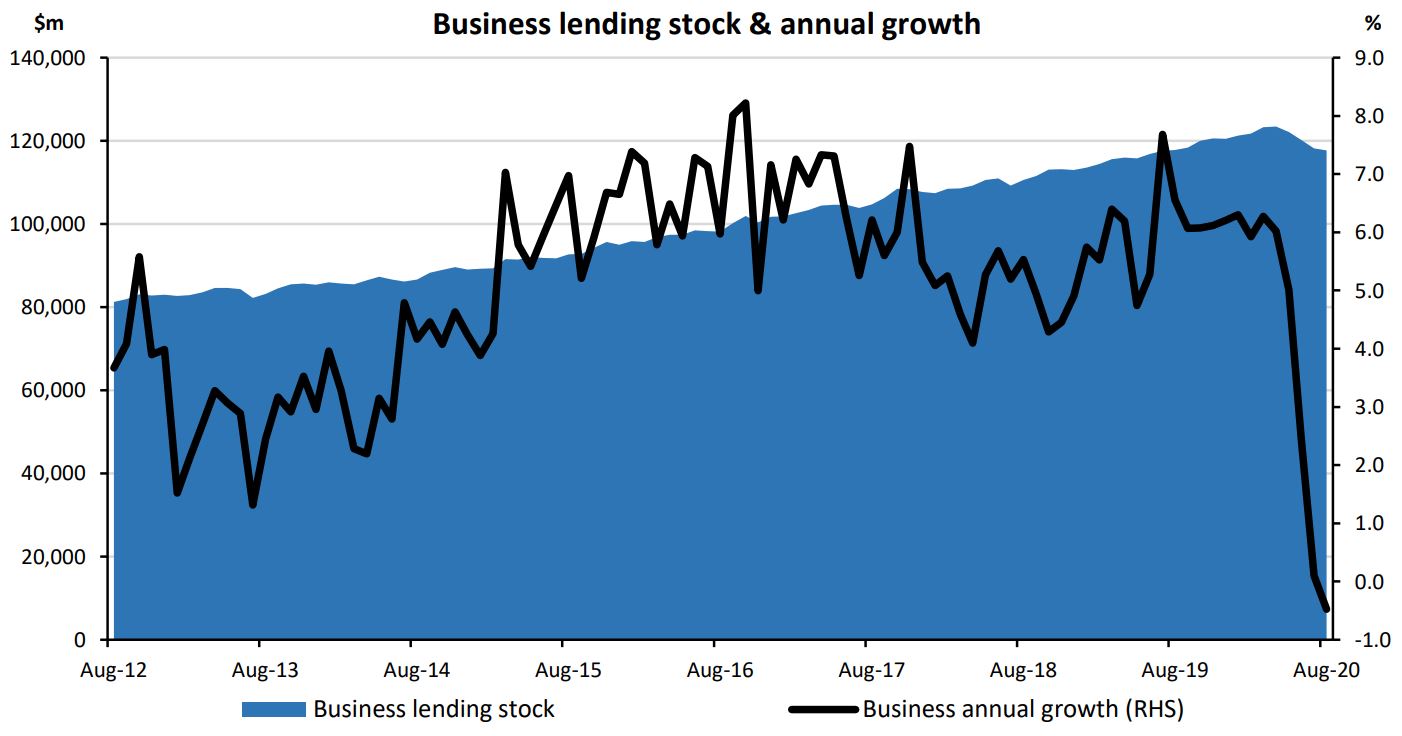

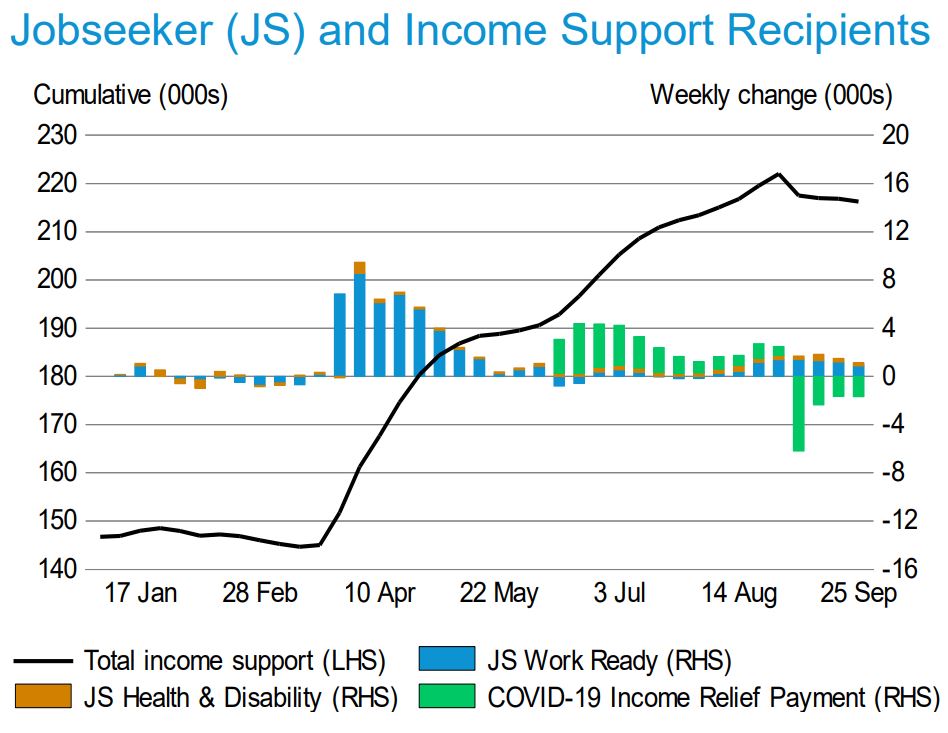

Meanwhile business lending has fallen, and the number of people to go on income support has increased by around 80,000 since March.

Speaking to interest.co.nz, Robertson acknowledged low interest rates prompt people to “look at” assets like housing.

Yet, he wanted to see low interest rates also encourage more consumer spending and business investment.

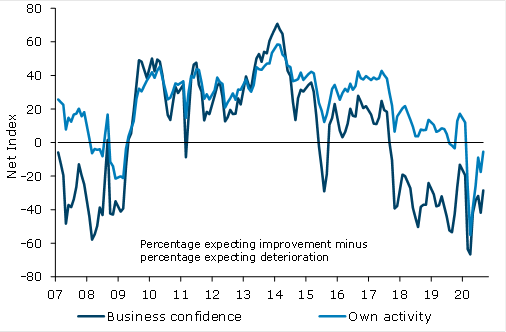

“Business investment… is about confidence, and we’re starting to see some confidence return,” he said, referencing improved ANZ Business Outlook Survey results.

A time for ‘balance’ rather than ‘transformation’

On the issue of whether fiscal stimulus by the government is keeping up with monetary stimulus by the Reserve Bank, interest.co.nz put it to Robertson that someone with a $500,000 mortgage, who switched from paying the average two-year mortgage rate at the beginning of the year to the average two-year rate now, would save $217 per month on interest payments.

Whereas someone on a benefit is $100 better off per month thanks to benefit rate increases made by the Government in response to Covid-19.

Asked whether it was fair that the support the Reserve Bank was providing to property owners was, in this modest example, worth more than the increased support the government was providing the more vulnerable, Robertson said the example didn’t compare apples with apples.

But he acknowledged the concept, and said changes made under his government were putting more cash in people's pockets - particularly sole parents.

He also noted Labour was campaigning on welfare changes, including changing abatement rates so that beneficiaries can earn more through paid work before their welfare payments are docked.

Asked why he was changing tack this election and campaigning on being “balanced” rather than “transformational”, Robertson said, “We’re in the middle of a one-in-100-year economic shock.

"Monetary policy has carried a portion of the load. The balance that we’re talking about is making sure that on the fiscal side we do invest heavily, which I believe we are. But that we also make sure we’ve got enough money available for public services and a careful management of the economy.”

Minimum wage hikes stimulatory

Robertson also pointed to the stimulus he maintained would come from increasing the minimum wage in 2021 from $18.90 to $20 an hour. The minimum wage was $15.75 when Labour came into power in 2017.

“Those on the lowest incomes are those who spend whatever increase they get, so that does flow through the economy,” he said.

“For the whole time I’ve been in politics, people have told us that when the minimum wage goes up, somehow or other this would have this massive impact on jobs. I’ve never seen that happen.”

Asked whether now was the time to increase costs for businesses (noting Labour also wants to permanently increase sick leave from five to 10 days), Robertson said it was a matter of balancing support for businesses with support for low-income earners.

Labour is campaigning on making a three-year extension to the Small Business Cashflow Loan Scheme, which enables businesses to get interest-free, unsecured loans from the Government. It’s also pledging to reduce the fees businesses pay their banks for accepting debit and credit card payments. And it wants to offer digital training vouchers.

One week at Level 3 could be enough for a new wage subsidy extension

In terms of other forms of fiscal stimulus, Robertson said he would continue to take a targeted approach.

He didn’t think the economy was in a dire enough state for helicopter payments to be warranted - in the “foreseeable future” at least.

Should there be a move back to Level 3 lockdown, Robertson said he’d rather look at a wage subsidy extension or something similar.

Asked whether a week at Level 3 would be long enough for the wage subsidy to be reinstated, Robertson said: “I think we’re moving to that…

“We can look at, potentially, week-by-week subsidies if we need to. It’s really more a systems thing than anything else. And I think they [the Ministry of Social Development] are probably in a position to be able to do that now.”

In terms of the Government directly helping “economically strategic businesses” like Air New Zealand, Robertson said he would continue to be ready to talk to businesses, if re-elected.

He said the type of support that had been discussed to date has been debt, not equity.

Social insurance could come as a surprise

Robertson remained elusive over when he would introduce a social insurance scheme and who would pay for it.

Social insurance would see someone who loses their job receive a higher payment than Jobseeker Support for a limited period of time. This would presumably be funded by the government and ACC-like levies charged to businesses.

Asked why Labour was committing to designing such a scheme, but wasn’t explicitly campaigning on it, Robertson said there were other more “immediate” issues for it to focus on at this election.

Asked whether he would put the scheme to voters before implementing it, his response possibly indicated the taxpayer, rather than businesses, could cover the cost of the scheme - to begin with at least.

Robertson said: “We’ve been very clear about our commitment around taxes and levies and so we would be seeking a mandate for that. But there’s an awful lot of work we can do... There would be other ways of funding that too that wouldn’t necessarily have that kind of implication.”

Dairy: ‘Volumes can go up if we can be sustainable in doing so’

Finally, Robertson acknowledged the Coalition Government’s decision to ban new offshore oil and gas exploration without consultation “clearly” evoked a “negative reaction from people”.

“But I think it’s now largely accepted as part of our plan for more sustainability,” Robertson said when asked whether he would rule out pulling the rug out from beneath an industry in that way again.

“We must bring people with us.”

As for the future of dairy, Roberson was focussed on adding value to products and making the sector more sustainable.

“Volumes can go up if we can be sustainable in doing so,” he said.

91 Comments

Grant Robertson on why now is the time for 'balance' not 'transformation'

Wrong, wrong, wrong Grant!

NOW is exactly the time for Transformation.

I know it; You know it, and so does Blind Freddy. That's why you're hedging your words and being so careful not to stir up the silt that's settled at the bottom of the pond.

What you do after the election ( if you get back in, that is!) will be either see the remaking of this country or its continued pitiful demise.

I helped vote John Key into Government becasue he was making all the same noises that you are today, and he failed us badly. He was even gifted two economic shocks to our economy, that he could have used to justify any transformation - the GFC and the Earthquakes - and he squibbed it.

You have the same sort of economic environment to work in - don't do a John Key, Grant! Do a Churchill....

“Never let a good crisis go to waste”.

Agree with you, so why not go and vote to 3rd party like Stuart mentioned.

Citizen too can and should experiment for political party to not take votes for granted.

Grant Robinson is got half wrong as this is the time to reset the economy for future and not maintain status quo. Does he realize that economist and experts are in favour of reset / change to use this crisis as an opportunity.

NZ has typical politicans but No leader.

One leader can transform the country like Lee Kuan Yew of Singapore - need to be bold and have vision unlike our politicans - ballot form should also have the option of none of the above while voting for this politicans to see themselves in the mirror.

Except for the referendums my ballot paper will be blank

BW, maybe the problem is not the politician's but us! A lot of the wealth holders and electorate are tied to status quo - people hate change and significant fast transformation rarely happens outside revolution.

The political term in democratically elected office is short (most nations restrict these to 2-3 terms) - you signal to the populace 'pain's going to come but for the long-term greater good'; you can kiss your re-election to office goodbye!

Either our politicians are not competent or they don't work for us.

Doesn't matter how competent a politician you are when the currency is controlled by unelected and unaccountable powers. No government can adress housing and inequality when RBNZ is gifting money to the rich

Yes, BW I'm on the same boat screaming until realised from humble healthcare professionals point of view.. that eventually soon we'll get another lv4 lock down again, by then the OCR negative interest by RBNZ/Orr's team will start to nudge the 4 OZ banks bottom line. GR will continue JA saying to be kind, more quick swift grants & subsidies, albeit in the absent of audit properly controlled distro - Now, imagine all those in govt+RBNZ+5mill teams being asked to push up the snow ball up to the highest peak, getting heavy, unbearable.. plenty of stronger participants quit this idea of being kind scheme towards 'specific group of investor' - I let your imagination run its course.. with closed border.

Politicians will have all excuse but if have the intent could have controlled hyper bubble with LVR but did opposite to add fuel to fire as they knew very well what ultra low interest will do to housing market along with QE.

Finance Minister comming out to justify in itself indicate how big the crisis (or good crisis as per national and now even labour) and rising house price is helping them (As no one is raising the issue in this election) as have taken the attention away from panademic and lockdown as politicians of all breed only act if they feel that may lose vote and election. For now they know that they will govern in next term if not alone than with partner.

So all FHB should also vote for Green though may not like them but now Labour = national

House price have not gone up by 7.5% but anywhere between 10% to 30% in just last few months.

Greens lost their credibility when they support stimulus (11 million dollars) for a private school.

I think TOP is your party if you really want a party that truly works for NZ.

Yuck. Green. Remembering the greens have been in government the last three years and so are accomplices to the problem. Greens have sat back and DONE NOTHING TO HELP THE HOUSING CRISIS. The Greens do not equal change, they are as self serving as the rest of them. FHB's need to vote TOP, at least they have a clean slate.

Now is the time for stimulus and stability. Labour’s proposed tax hike will be counterproductive.

This depends on how tax is applied, stimulus needs to come from somewhere, but given their track it will likely be a burden on the shoulders of those that cannot escape from paying it.

Robertson acknowledged low interest rates prompt people to “look at” assets like housing.

Yet, he wanted to see low interest rates also encourage more consumer spending and business investment.

“Business investment… is about confidence, and we’re starting to see some confidence return,”

[ Shouting removed. Not needed here. Ed ]

The image of Grant Robertson is apt as he is laughing at FHB and they deserve for voting him.

Still time to vote and may be if not green than national as aleast national does by saying that housing crisis is a good crisis unlike Labour who say one thing and do another.

Whereas someone on a benefit is $200 better off per month thanks to benefit rate increases made by the Government in response to Covid-19.

I thought benefits were increased by $25 a week, so $100 a month?

You're right. Apologies. Corrected.

Hi Jenee, Wonder why rising house price is not an issue in this election. If last time were in bubble than now in hyper bubble.

Understand are in panademic and only two topic are been talked about in NZ - panademic and house price still Housing is not an issue in this election - may be because National has no face to raise it and why would labour digs its own grave but how come even journalist and so called experts are silent on the issue that affect FHB. Falling interest rate does not help FHB as rising house price has offset it.

Just like homelessness is not an issue this election - because Labour is in power this time round and it doesn't suit the media class narrative.

Good question Stuart. A few thoughts:

- There are only a few political journalists who are also interested in monetary policy. Monetary policy is usually covered by business journalists, who don’t report on political issues.

- Labour is shying away from talking about housing because prices are shooting up, KiwiBuild has under-delivered and the wait list for public housing is nearing 20,000. Much of what Phil Twyford has done in this term of government has been to set up a new housing agency and give it the powers to do large-scale developments fast. The building blocks have been put in place. We haven't yet had time to see how effective they will be.

- National sees repealing and replacing the RMA as the silver bullet to increasing housing supply. It also wants to change the Residential Tenancies Act to tidy up body corp issues, which seems like a good idea. But beyond that, it doesn't have major housing policy. Judith Collins has given the housing portfolio to the low-profile Jacqui Dean.

- ACT has some new policy on urban development, consenting and insurance, as does TOP. I had an interesting chat with David Seymour about this back in August. But because the two major parties aren't talking housing, it isn't getting as much coverage as it should.

- Going through the ins and outs of the RMA, planning rules, urban development policy statements, etc is complicated and dry, and not as sexy for mainstream media as a story about a politician doing something funny on the campaign trail, or a story about tax cuts. But readership numbers on our housing-related stories suggest it is absolutely front of mind for NZers. I'm interviewing Megan Woods on Labour's housing policy next week.

Thank you for the excellent work Jenee. Nice to see that Journalism is not totally dead in NZ

Great stuff as usual Jenée. You understand the pantomime well and also can grasp the bigger and real issues.

Thanks Jenee for the response, so you may get an opportunity to ask some good questions with minister.

Low interest rate understandable but when know that house price have taken another leap from what seem to be a peak why not have LVR in place again, specially for investor. Know quite a few people who used their equity to buy another house in last few months as now no restriction of 20% - it is good for them but is this not adding fuel to fire specially in low interest environment and if government is serious in controlling the bubble.

Also just like OIO declaration that buyers have to sign while buying a house, why not have a declaration for vendor/sellers to declare if they own any other property either individually, jointly or under trust just to emphasis the seriousness of Tax - BLT, which many are able to evade by using loopholes.

No one is also asking government what they are doing to protect savers/deposit holders just like they have been so prompt and proactive to protect borrowers/ mortage.

"The building blocks have been put in place." Next term Phil is going to graduate to Lego blocks?

We have significantly raised incomes... But forgets that also significantly raised costs...

He doesn't really know what he is doing. Has no idea how to stimulate an economy. Printing $100b and giving it to the banks and asset owners is not stimulatory. Pretending it is, is duplicitous and pretty much criminal.

Time to vote for real transformation people, its EXACTLY what is needed now.

He can get away with any nonsense knowing that will get vote to be in next term hence the smuk on the face.

I too now think that vote for anyone but labour so that next time will think twice before taking vote for granted.

Hope you dont mean 'top'......

Labour suffers from a lack of depth in people who can deliver. Imagin how dismal 'top' would be with considerably less depth......

GM would get the call up and the ensuing 'I know it all' would be insane...

TOP aren't so interested in having ministerial posts, they have said repeatedly that they will simply support any party that implements as much of their policy as possible. Which they would have in a position to do if holding the balance of power.

Or you could just vote for National or Act or Labour or NZ First. But if you do, don't come on here winging how useless they are when you get more of the same,which is exactly what will happen. Surely people can see that a vote for the same thing expecting different results is a wasted vote.

If you want to invest in businesses, you need capital. To have capital u need a decent rate of return.

Grant would rather shovel out the loans. Grant loves malinvestment and raising asset prices.

Don't be fooled.

As far as I can see asset price inflation is the only game in town.

Productivity has peaked, there seems little political will to support the wider economy (e.g. building infrastructure, reskilling workers etc.) and there is no desire to remove the impediments to progress (e.g. the RMA, tax reform.) We remain in the holding pattern we've been in since the Financial Crisis of '08.

I'd go as far as to say that if I where a young person in New Zealand I'd probably think about leaving once the current pandemic finishes.

Ozzie home owners behind on their mortgages just started getting "Time to sell" letters. Many of those young kiwis you mentioned will want to "look at" life over the ditch when plague conditions abate.

Such a disappointingly conservative character.

Not conservative.

More unresponsive - begrudgingly reactive to events, unable to work out whats important (compare things) and then prioritize.

Add this to or because of the self impossed restrictions - being left of centre & and having a self identifying lefties tree hugger PM expectations of him are ever lower.

Back to core principles first principles.

The history of socialim & capitalism

https://youtu.be/0iRvEPcQV3I

Best GR revise his assumptions of the human condition.

Doubtful he will change, he is having too much fun.

Real estate is the lazy peoples investment option. Who wants the hassle of developing IP and staff when you can do nothing but drink gin and watch sunsets. And then there is the tax free gain. Really underlines why the tax base should be changed to a lazy land tax and away from punishing productivity thru paye, gst and company taxes.

Change the tax burden. Promote productivity. Pretty sure one party has that as a lead policy.

Stupid asset price debt is sucking the financial wellbeing out of NZ. To foreign owned banks.

I agree 100%. Parasitic and passive investment (like housing speculation) should be very heavily and immediately taxed, with no exceptions.

On the other hand, entrepreneurial risk taking and investment in productive capacity and innovation (in particular, venture capital, R&D investments etc.) should be encouraged with a particularly favourable tax treatment, and possibly even with private-public partnership and shared risk-taking. It is time to be courageous and innovative: the current caveman settings and policies (around roads and landlords, favouring parasitic behaviours), should be completely reversed.

Not lazy, smart. I'd rather watch the sunset and take my last breathe knowing my tamariki are provided for than try and fight the system and vent on forums.

Yep waste of time venting on here nothing is going to change. GR thinks lowering interest rates gives people more money to spend to stimulate the economy wrong if it was me I would just be using it to pay the mortgage off even faster.

Speaking to interest.co.nz, Robertson acknowledged low interest rates prompt people to “look at” assets like housing.

Yet, he wanted to see low interest rates also encourage more consumer spending and business investment.

Hmmmm...what about the fact lower interest rates raise the discounted present value of liabilities which disadvantages asset deficient households more than the minority that are asset rich. Why is a labour government in the business of blatantly picking winners?

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link-pdf

Because they're not smart enough to understand that Audaxes

I woul agree with that. Lack of original thinking resulting in solutions that solve problems is either lack of intellect or lack of intent. The later is normally because of focus elsewhere. Like the nose bag.

Extremely good point, Audaxes.

I don't know if they are too disingenuous, self-interested (or attentive to self-serving interests of a minority), negligent, lazy or stupid to comprehend it (or a combination of the above). And the RBNZ are equally if not more responsible for this.

PS: I voted Labour the last elections, so I am not starting from a political partisan perspective, and National have been equally negligent in this.

But the RBNZ makes it's OCR decisions independently of the government. Supposedly.

One mans liability is anothers asset. Key is assessment of risk premium within the market. Everyones looking for a home for their money... the hunt is increasingly harder to find right investment for your given risk/return.

I've heard sharemarkets abroad is so disconnected with free cash flow that those trading are doing so without regard to intrinsic value.

A high level of liquidity preferences, the low level even lack of economic growth to provide opportunity causes investors to seek refuge in what they consider to be safe liquid assets. The consequential rise in sovereign bond prices reduces term interest rates, which in turn increases the discounted present value of cash flows associated with all assets. This encourages investors to capitalise such an outcome in other asset classes. Speculation follows on quite quickly when bank offers of leveraged, collateralised borrowing allows a larger cohort of capital deficient participants entrance into the casino.

I don’t think it’s about picking winners. They reach for the quickest, easiest tool in the box to show the populace they care about their ‘economic lives’. Even if they have a long term view and strategy for the nation, they know to stay in power, the people must have bread.

Says it all about a "Labour" party when instead of having an economy ministry they have a finance ministry instead. Shame on not doing their job reverting neoliberal policies which have turned the economy into a wild west and pushing private debts to unsustainable levels.

Think and Vote.

Even Hardcore Labour supporters should think as now their is no difference between Labour party and National party.

May be as suggested, should give more to Green Party for if they reach even 7% or 8% would give them more bargaining power though even they are.....but......

What is it about Greens you like?

1. Is it the people (which ones) you like.

2. Is it their philosophical thought base.

3. Is it a particular policy.

Have to vote and now Labour = National so why not Green.

Politicans of all breed are same so why not Green.

If you feel none deserve your vote then don't vote.

Sorry, I don't think the previous poster is silly enough to play into your hands like that. Rolling over and playing dead is not a good option, it just leaves the underbelly exposed for the predators to attack.

Stuart's issues include his making justification of the assertion Labour = National.

Stuart is free to vote for one of the other parties, gone are the days of the two party system under FPP.

In my opinion this is not about a specific party, it is about Labour/National vs all other alternatives, we have seen what these two had to offer, which is more inequality and half-baked policies from the 80's which did not work to improve our lives except for just a few. Other parties, perhaps not having the pressure of power are coming up with 21st century ideas which some are proven to work such as a UBI to replace a broken old welfare system, maybe it is time to alleviate that pressure from them to apply some sensible polices once and for all.

Buy houses and shares then I guess! Sad how lending to businesses seems to be decreasing. Banks really only seem to want to lend on houses as far as I can see.

Buy into all asset classes (with the exception of residential housing, which is the most inflated and illiquid and which I would not personally increase) if you have a decent investment horizon like 10 years min. Diversify as much as possible, across asset classes, countries, currencies.

Keeping any significant money in NZ banks, especially as term deposits, is only about subsiding other people's risk-taking and their assets inflation, and for no rewards. Keep some cash available for potential opportunities (such as if things go pear-shaped after the US elections).

Grant

Adrian Orr runs nz not you! His plan is increasing house prices so that's what will happen.

In regards to people not seeing house price inflation as an election it's simple. People love who is delivering the message. Jacinda was in Newmarket yesterday in Auckland and people were dancing and singing around her. Beeping car horns and waving. I was there and caught a bit on my mobile.

This is South American style cult of personality electioneering. All that's missing is jacinda with a presidential sash and in a convertible with horns and dancing girls.

Example.. I know I guy with an 80k student loan. In 2017 he was fuming saying its destroying him and immoral. In 2020 he still has a near 80k loan. But nows he's totally cool with it and its no big deal.

Shows how much people/populace are shallow and only vote for the figure not the policy. Retards

If labour doesn't pass Jacinda will have a nice job at the UN and might even (likely) try to become secretary general

Adrian Orr or the best of us, doesn't matter - It is the central bank that is in control/problem

Cue witchy cackling....

I love it. I just love it. The naive open eyed rubbish that comes out of the mouths of people like this.

He has no clue what low interest rates will do to the fabric of NZ. He has no choice but to go along with it. He presides as does the RBNZ over the acceleration of the destruction of the middle class of NZ into the benficiaries at the bottom, and the working poor, and beneficiaries that the top.

Make no mistake good people of NZ, look at business investment. Those are the people that make jobs that give people the freedom to live their lives by their own will. If this does not turn around, only government spending and the pet projects that that money props up will be the only game in town. The underclass will be enormous, the rich will become beyond rich, the average man will be born into a system in which it will be very difficult to have social mobility. We are in a banker ghetto. Do not look to the government to save you. They want you dependent either on credit lines, or on their taxpayer funded programs. It is antithetical to freedom. That is the future this man and those like him think you need.

It's been inevitable for years. Let's get it over with. I wonder if there is a People's Democratic Republic of Soviet Socialist Aotearoa party I can vote for?

Good point, the question of pet projects, crony capitalism and green cronyism, the Taranaki Green School Scheme.

A question as to why the shakie funding can continue, & how good administration of crown partners infrastructure spending can demonstrated (remember NCITR were reporting direct to PM dept.).

Makes an ICAC type office seem to have plenty to do.

And another thing. Increasing minimum wage. I'll bet GR he stuffed more youth employment and undereducated with that one than created stimulus in those people on minimum wage. Just like bringing in new tenancy rules got more landlords out of the business and drove up rental prices. They don't know in the ivory tower what happens in the real world in reaction to their policies. They're blaming record high youth unemployment on Covid. So if Covid hit the young and cheap labour harder why bring in special Covid dole rates of 400 bucks a week?? Suddenly normal dole isn't good enough? Covid killed some good paying jobs. Minimum wage hikes killed the low paying jobs. They don't understand what they do. And the poor will vote for them.

Just like bringing in new tenancy rules got more landlords out of the business

Not sure if theres a shortage of property investors at the moment. All the bluster in the media hasn’t amounted to much.

Regarding Jenée’s question at 3:20, she seems incredulous that central government stimulus is benefiting middle New Zealand and not only beneficiaries. Middle NZ matters too - both in terms of economic recovery and the general wellbeing of the country. The idea that it is immoral to provide stimulus to anyone other that those on the dole or minimum wage in times of financial crisis is ridiculous. The political leanings of this website are clear, and they shouldn’t be.

And later in the interview I asked whether now was the right time to add costs to businesses with another minimum wage hike and social insurance levies. I also asked Robertson whether he would commit to not pulling the rug out from beneath an industry without consultation, like the Govt did with oil and gas...

Yes it was a nice balanced interview, despite what some think...

Speaking of balanced interviews, Katherine Ryan did a brilliant one on GR yesterday

Jenee - Why didn't you raise a deposit guarantee for savers? Orr and Robertson can print $100 billion and arrange mortgage deferrals for 12 months and make interest rates zero but a deposit guarantee requires more work? Both have said they want banks to be bold and lend and take risks and put deposit holders at greater risk for zero return?

Yea, I didn't ask the question, because I didn't think I would get a different answer to what we've reported in recent months. Consultation is underway and the plan is to implement the scheme in 2023.

I also wonder whether it would be a bad idea to try to implement this kind scheme quickly, in the middle of a recession/period of major volatility and uncertainty. It could panic the average person on the street, make them think the banking system isn't sound and cause them to react in such a way that could have perverse consequences.

What's more, I suspect the RBNZ would rather get banks to start implementing new capital rules to make them stronger (the start date of these has been deferred by a year due to Covid) rather than pay levies to fund the ambulance at the bottom of the cliff.

And from a resourcing perspective, staff at the RBNZ, Treasury and retail banks have a lot on their plates at the moment.

"Staff at the RBNZ, Treasury and the Banks have a lot on their plates at the moment"

Doing What ? doing Make Work

Thanks for answering. But do you not agree that the landscape has changed significantly from when the scheme was announced?

Robertson and Orr have pushed the banks to lend removing LVR rules and creating an artificial environment of higher risk and zero return for savers. It makes no sense to get zero return for increased risk?

In addition they have allowed banks to provide no additional capital for what ordinarily would be classified as underperforming loans.

They have to be answerable to deposit holders. But they are silent on what risks they are facing for zero return. I do agree with your comments above that very few journalists cover these sorts of issues.

I am sure Roberson and Orr would not appreciate being pushed on the issue but good journalists like yourself need to hold them to account.

The crown retail deposit guarantee in 2008 was just announced and it didn't create uncertainty to the public. If anything it gave deposit holders confidence in retail banks.

What are your thoughts?

Interesting points re risk and return for depositors. I will have to think about these. Good to keep deposit insurance on the agenda for sure.

Many thanks for your reply. Yes the nature of a bond is that the return increases when the risk increases. When they are re-rated to junk the return goes through the roof. The market prices in the risk. However we have deposit holders and TD investors getting effectively zero return for greatly increased risk. Further your funds cant attach to any asset of the bank and in the event of the trouble via an OBR event you will loose your funds.

The market trend of holding cash in deposit accounts and not TD's indicates that some may be aware of this.

Appreciate your consideration as it is one that not many journalists would even cover outside of your team. Would love to see some hard questions asked to Robertson and Orr on this topic!

Risk free rate is zero because central banks have said they will buy (almost) all and any risk. The norms of financial theory no longer apply around risk free rate, present values of discounted cash flows etc. How can they be true given what we’ve just witnessed this year?

Time to rewrite the tertiary text books for finance/economics. Old rules no longer apply. There is a new game in town and based on what we’ve just witnessed with central banks buying up all bad debts, why do we have private ownership if companies can’t survive a downturn without the state owning their risk?

Also banks issued covered bonds which were secured against their lowest risk mortgages, this left deposit holders with even more risk.

Andrew

Zero return must equate to either lack of alternatives or assumed deflation conditions over term of investment...probably mix of both.

Looks like the fiat system is broken... better off trading in real goods.

That’s cool Jenée. I look forward to the day you ask Geoff Simmons a difficult question.

I’m likely off to 403 land now.

Economy? Jacinda has got this. "Ardern wants us to capitalise internationally on "brand New Zealand".

Gower responded with incredulity, stating: "So trade on our brand is your visionary idea".

https://www.rnz.co.nz/news/on-the-inside/427331/jacinda-ardern-vs-judit…

I have interacted with and presented (didn't charge for my time) on behalf of NZTE / Beachheads. The 'brand NZ' stuff is well executed, but it gets boring after a while. There's a heck of a lot of public sector people riding the coat tails of it.

Interesting observation of this threat is no one has pointed to a positive policy and/or the successful delivery or implementation of anything that can be credited to Labour. Part of this is being well left. But a big part is the PM herself.

Analysis: Ardern's popularity defies her track record

https://www.rnz.co.nz/news/political/427531/analysis-ardern-s-popularit…

Many people react as fans because of the emotional feelings they find themselves feeling. The PM generates feelings in many, fan/celebrities feelings - nothing to do with good governance or sound administration.

(The latest PM oddity is that Australia is having a travel bubble with us, but we not with them - soils her narrative of world leading, again - even if elimination was viable....).

Others react extremely negatively toward the PM because they see someone attempting emotional connections with folk, on the basis of no tangible governing or administration success - to these people the actions of the PM are exactly the same as a commercial swindler and fraudster or terrible potential life partner - lot of folk have experienced dating the wrong people (hence their reaction).

Polls show Labour moving in the wrong direction and being unable to govern on their own right.

The next two weeks will be fascinating.

Nail and head accurate

So what are labours plans on solving the housing crisis?. It appears to have got significantly worse during the last 3 years. It should have least improved. The RB are now printing billions of dollars, and much of that is going into assets such as housing and shares, and pumping up the asset bubble. It is coming at the coming at the cost to savers, who will lose billions in lost potential interest in the bank, so many who are retired, will have less money in their retirement.

I wanted to buy a kiwibuild house, but hardly anything on their website, nothing in my area. Apparently some are currently being built, but don't know where, and probably not in my areas, and can't see me ever being able to get one.

I don't see why we need a social insurance scheme. People can already get income protection insurance, and I understand banks often require it if buying a house. If the unemployment benefit isn't enough to live on, then it should be raised.

What about bank deposit insurance? People can't insure their money in an NZ bank. With the low interest rates, people who have money in the bank appear to have quite a high risk, compared to the very small returns, and NZ is one of the only countries in the OECD that doesn't have this protection for it's people. In Oz it is 250k per bank. It needs to be at least that in NZ, considering we probably have less banks to spread money across. At the moment, it appears a lot of people are using their cash to either buy houses, or could be in the process of doing so, based on all the people who have moved their money to oncall accounts, from long term deposits, which are hardly paying any interest..

1) Social insurance is ABSURB. Due to an economic system focussed on inflation targeting the unemployed are unemployed through no fault of their own (unless we want slavery & no minimum wage) Why should the employed gain yet further subsidy while the unemployed languish at the bottom. Work with the private sector make income protection insurance readily available irrespective of cause. Those that want it can take it up. It could run from 80% of income down to 0% over, say, 6 months.

2) Ban recourse mortgages. Its a free ride for the banks & no wonder banks wont lend to businesses with the risks so badly skewed.

Housing price growth, controlled etc. - it's not in their long term plan, but watch out their short term measures. Seems rosy looking right now, but I think they on to something between now until 2023 - they seems to put an unknown/twilight zone reality moving forward to the NZ promoter of this biggest ponzi scheme, the 4 OZ banks. What now remains to be seen is their reaction.. they're testing the water with plenty of caution & backup plans.

"The Poverty Effect" would be accurate to describe whats happened from house price rises. So much income going out on rents and mortgages, there is little left for other things. Even for working middle income people.

It's a national disaster.

When people of my age could no longer afford to buy homes back then, society’s solution was to pump prime everything with dubious credit, funny money that eventually blew up in everybody’s faces with terrible consequences. That cannot be the solution to the problem this time around. And be in no doubt that a huge problem is coming. Research released this week shows that it is metastasizing and getting ready to explode all over again. Barely three years after I bought it, the house was worth less than half of what I paid for it.

It never went away, you know. The greatest medium-term threat to.... economic and social stability – which is just jargon for the fortunes of businesses and people – is not the fallout from coronavirus, it is the housing crisis, whose most grotesque features have been distorted even further by the pandemic.....housing has been such an undulating horror show for the best part of two decades. This destructive pattern must be brought to an end before it swamps social cohesion and distorts the whole economy.

https://www.irishtimes.com/business/housing-crisis-will-become-a-monste…

Sorry, but this is Thought Crime. NZ uz duffrunt.

I keep thinking on Steve Keens analysis, briefly there are 3 ways to create money in the economy. 1 govt runs a deficit, 2 commercial banks issue more loans, and 3 country runs a surplus. Seems to me that the third is the most important because its the only one that's sustainable without negative consequences. But we just lost tourism (20% of GDP) and foreign students (5% of GDP) and oil exploration. In the context of the countries surplus, How can the current state of affairs be anything other than an economic disaster for the country? I understand that NZs surplus is unexpectedly in the green but I'm having trouble believing it.

Every single policy, from highest per capita immigration in the OECD, lowering interest rates, lowering LVRs, non govt guarantee on bank deposits, tax advantages on property investment, cumbersome planning restrictions, money printing etc has the intentional effect of keeping NZ house prices among the most expensive in the world.

100% agree. No reporter seems to be able to have robust debate with politicians even in an election year on these topics.

I suspect topics are set before the interview

Hogwash.

The political deficit in this country is jaw dropping. We have leader who came into power on the promise of a Capital gains tax, in partnership with the man who wanted a property register. Never has a country needed these things more. But we get neither. Why does a property investor get the same interest rate as a FHB. The risk profile is definitely different. Why do property investors not have to pay tax on their gains but the FHB has to pay on the money he earns and saves. Why does the reserve bank give saver's hard earned and taxed depositd to property investors for free.

Then to cap it all when covid hits they give 64 billion to bailout property investors(that is what it was... no ways interest rates were coming down without that bailout) it is absolutely criminal that that money was pumped into the system with no corresponding policy to prevent it flowing into asset prices .I would like to see investor rates at 7% and 2.5% only available on a first home. Every mortgage being tracked against a property. Remortgaging the family home to buy a second property would be at the investor rate. All of this policy is simple with a property register... But our politicians do nothing..' It's all too difficult' THEY SAY. No it's not,the problem is the property investors ARE the politicians and they create bailouts using your future taxes to ensure they will be able to buy more property using our savings for free. We need a Trump.. NZ politics is a cesspool.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.