By Bernard Hickey

The Reserve Bank has reported back from stress tests of bank dairy lending that the banks faced posting losses of up to an average of 8% of their dairy loans - or about $3 billion - in the most extreme scenario.

But it said the banks were able to handle the losses through lower profits, rather than having to eat into their capital.

Banks had lent over NZ$38 billion to dairy farmers as at the end of June last year, although this is expected to have increased substantially since then as the banks supported loss-making farmers with working capital lending. The Reserve Bank's stress tests suggested the banks -- including ANZ, ASB, Westpac, BNZ and Rabobank -- could collectively book losses on their loans of more than NZ$3 billion over the five years in the scenarios included in the stress tests.

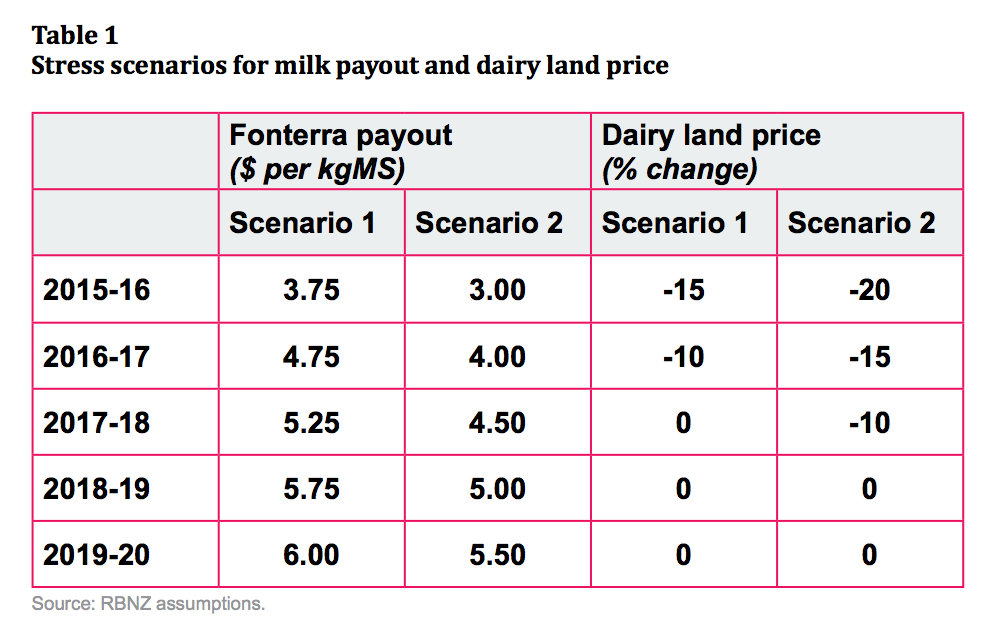

The tests included two scenarios: one where the payout recovers to NZ$5.25/kg by 2017/18 and land prices fall 20%, and a second scenario where the payout was NZ$3/kg this year and remained below NZ$5/kg until 2019/20. The second scenario generated land price falls of 40%.

"On average, banks reported losses under the two scenarios ranging between 3 to 8 percent of their total dairy sector exposures,” said Reserve Bank Head of Macro-Prudential Bernard Hodgetts.

“Bank lending to the dairy sector stands at around NZ$38 billion, which is approximately 10 percent of the banking system’s total lending. We would expect losses of the order seen in the stress scenarios to be absorbed largely through lower bank earnings rather than through an erosion of bank capital," Hodgetts said.

The Reserve Bank reported the results of the stress conducted by the banks on their dairy loan portfolios in October and November in this bulletin article.

"Consistent with earlier work, the scenarios generate significant increases in loss rates that are manageable for the banking system as a whole," article author Ashley Dunstan wrote in the article.

"There is a risk that the time taken to resolve stressed dairy exposures could be longer than reported in the tests, creating an ongoing source of uncertainty for banks," he said.

The stress test scenarios are detailed in this table:

The test results found that 40% of the debt was held by farmers with a break-even payout of NZ$5/kg or higher, and a current loan to value ratio of over 50%.

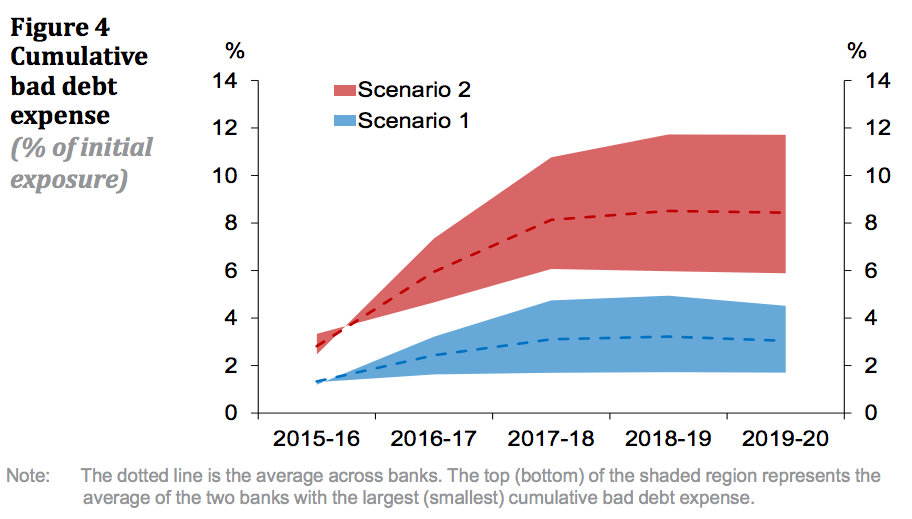

The Reserve Bank said the tests showed that most of the impact on bank profitability would occur in the first three years of the scenarios and it published a chart showing the cumulative bad debt estimates under the two scenarios.

"Throughout the entire scenario, the average bank reports a cumulative bad debt expense equivalent to about 8 percent of initial dairy exposures in scenario 2, and 3 percent of exposures in scenario 1," the Reserve Bank said.

The Reserve Bank reported that banks found up to 25% of dairy loans would be written off in the most severe scenario, although this does not account for recoveries on loans, which generated the lower net bad loss average in the worst scenario of 8%.

Risk of long lag of 'managed turn-arounds'

The Reserve Bank warned the scale of loans written off would likely result in "very challenging conditions in the market for dairy farms, particularly in the last two years of the scenario," given the number of farms the could be sold would be larger than the number of buyers with sufficient capital.

"This analysis suggests that banks should plan for the possibility that the time taken to write off stressed dairy exposures could be significantly longer than assumed in the tests," the bank said.

"Under these circumstances, banks could be left needing to manage a large portfolio of foreclosed assets for an extended period of time. This would mean that uncertainty about the scale of eventual write downs would persist for longer, potentially requiring the banks to hold additional capital to boost confidence," it said.

"Losses on written-off loans could also increase if ongoing management costs and forgone interest income are larger than initially provisioned for (possibly offset by any growth in dairy land values that occurs in the interim)."

Reaction

New Zealand Bankers Association acting CEO Antony Buick-Constable said the results showed the banking system was resilient and the long-term outlook for dairy remained positive.

"It’s very much in the banks’ interests to support farmers through both the tough times and the good," Buick-Constable said, adding that banks worked with customers with a range of measures to maintain the viability of of their businesses.

"Depending on individual circumstances, banks might be able to look at reducing or suspending principal payments on loans and temporarily moving to interest-only payments. Banks might also consider allowing term deposits to be broken without associated costs," he said.

"Banks can also help by providing affected farmers with financial management and budgeting assistance, and access to workshops on enhancing farm productivity and performance."

Labour Leader Andrew Little said the stress test results showed the banks had room to stand by farmers.

"National has done nothing but make excuses for banks, instead of ensuring they stick by farmers. This report shows that banks have the room to be flexible and stand by good, efficient farmers," Little said.

"Those who have profited during dairy’s good times must now come to the table to work through a long-term solution. That should start with passing on interest rate cuts and doing everything possible to keep Kiwi farmers on their land," he said.

(Updated with more detail, reaction and charts)

21 Comments

I am lost here, so would the banks raise a provision for doubtful debts on non-performing loans , and offset these against income until the loan went bad or was rehabilitated or became a mortgagee sale ?

It appears they are stating that they completely absorb the loss without tapping into capital. So yes the losses would be offset against income. There may be some accounting in there as I do not know how they write off loans against a secured asset.

That's not to say that a much worse scenario could happen otherwise banks wouldn't have capital requirements.

It is important to be very clear here, "income" includes deposits. In other words, what you and I have in our bank accounts. It is not our money, but a resource for banks to shore up shonky business practices. all banks are the same. The less money held in a bank, and the less debt you have, the safer you are.

Say it enough times and you will believe it.

The question is the multiplier effect of dairy. I don't think rural NZ can handle that.

Tell me when banks actually lose.

When they get caught Frank.........light on the loose change.....wearing kilts instead of pants...that kinda thing.

Even when they get caught and it is obvious to the most casual viewer, they still escape.

https://www.sfo.gov.uk/2016/03/15/sfo-closes-forex-investigation/

Correct. Can doesn't equal will (happy to).

One can imagine some of our good friends in Sydney and Melbourne going absolutely ape shitte about the prospect of a cash or accounting loss (let alone insto investors).

Interesting to see if APRA require extra equity raises to account for the loans smoked. Hard to see how the collective share prices would kick up on the news (or has it already been factored in).

APRA may require the banks to raise and hold more capital to support home loan lending to investors (they being different to owner occupiers). As Simon posted seems you can have four houses and loans here and still be classified as an owner occupier of all.

http://m.smh.com.au/business/banking-and-finance/bank-capital-requireme…

APRA noted this week Australia was one of several countries where housing investor loans received the same capital treatment as owner-occupier loans, and that this would be the subject of future review.

The comments were contained in an obscure document published on the Basel committee website, in which APRA responded to a review of its implementation of the Basel III rules.

APRA's comments relate to the large Australian banks that use an internal ratings-based approach to credit risk – ANZ Bank, Commonwealth Bank of Australia, National Australia Bank, Westpac, and Macquarie.

Q: Anyone know Basel handles farm loans? - thats over and above portfolio losses.

They have lost many times, hence bailouts. The question is which government will lose by allowing bailouts if such an event occurs. Riots anyone?

Riots wouldn't happen here I don't think. Kiwi's are way too apathetic. We care...but yeah nah not really.

We need a few more incidents of 600 tractors in the city like they do in Europe when they aren't happy. In NZ we just bend over.

https://www.rt.com/news/335353-helsinki-tractors-farmers-protest/

He's not exactly going to say "Hey everything is bananas,pull your money out and stuff your mattress"

Ben Bernanke quotes pre GFC:

(March 28, 2007) “At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.”

(January 10, 2008) “The Federal Reserve is not currently forecasting a recession.”

"Banks can also help by providing affected farmers with financial management and budgeting assistance, and access to workshops on enhancing farm productivity and performance."

For many Farmers this should have been at the.... start... of a good plan......not the crisis plan to lock the gates as the horses bolted from view.

No, no no Christov.

Banks are the last place farmers should go for budgeting and financial management advice and most definitely NOT workshops on enhancing farm productivity and performance. There is one bank in Southland promoting such a workshop to young farmers - for the cost of $7000. It is a farmer that is running the workshop. This sort of help and advice can be got for free via farming mentors via the DairyNZ Connect programme. http://www.dairynz.co.nz/what-we-do/services/dairy-connect/ or via word of mouth. Farmers are far better to approach their accountants who will help them negotiate with the bank than go to the bank.

Bankers are salesmen/women - nothing more, nothing less.

Thanks CasO....agreed but somewhere at the beginning the business plan was unable to operate at $4PKG and below......it should have been a scenario at the beginning not an end game for those less skilled.

I do take your point on Banker salesmen/women however, without appropriate skills what were they lending on...? Fonterra's Utopia..?

Say Dairy NZ should run a few training sessions on how to lend money and write up a rural loan proposal and credit paper (several of us could lend them the notes from Lincoln days). It would be extra for learning to pick a fgmp servicing number.

If we charged $1,000,000 plus, per banker student, its still cheaper than the losses they are looking at now.... But we need someone to play the Bruce Ryde role.

http://i.stuff.co.nz/business/farming/advice/63862312/school-is-hard-bu…

Ta Henry .........sounds plausible ........this is yet to play out ,with more collateral damage than there needed to be . ......Stay Well

Headline reads differently on Stuff:

http://www.stuff.co.nz/business/77948349/reserve-bank-stress-tests-show…

OMG. The banks are described as being resilient.....

Indeed - swap price spreads to governments definitely confirm some sort of bank balance sheet disruption/incapacity. Risk is not priced to reflect reality and those responsible find themselves unable to arbitrage the position to reflect the inherent and accepted risks. NZ Government debt zero capital risk weightings have to be officially re-arranged - what's the regulator doing? - hiding in the corner?

A little exercise.

If I had $100k and then e.g. borrowed $900K from any bank who doesn't have the money either but creates it out of thin air...........and then charges me interest on that created money..........whilst taking my deposit......with a very small portion retained for capital ratio requirements as set out by the RBNZ.

So the bank I borrowed from can now charge me interest on the $900K @ e.g. 7% = $63,000 I have to generate this excess income.........to pay for something that is in existence but isn't in existence and then a stress test is undertaken because my ability to pay is threatened by a real market situation..........and my real market situation has threatened the profits of the system that has no real money but charges for my future promise to create the real money to pay down the desk top created transaction.........now my ability to service this created out of thin air money has threatened the system so much that they have to run stress tests.........how about cutting the rate of that interest on the created money portion of a loan and give the real creators of the forward promise to pay a break from the greedy system? The fact is the banks have been able to walk away year after year with enormous profits to distribute to shareholders who have also invested in this well known system of income and profit transfer from those who do the real work. So how about the banks dropping the interest rate to say 1% above the OCR so 3.25% so my new equation would be $900K @ 3.25% = $29,250 pa.........I would have thought it is high time the banks learned to trim their costs and budgets......and banks should also be forced to retain some form of security over depositors funds.!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.