Outgoing Reserve Bank Governor Graeme Wheeler is rejecting clamouring from real estate agents and politicians for restrictions on banks' high loan-to-value ratio (LVR) residential mortgage lending to be eased.

In a speech entitled Reflections on the stewardship of the Reserve Bank made at the Northern Club in Auckland, Wheeler said LVR restrictions aren't expected to be permanent, but their removal would require a degree of confidence that financial stability risks won’t deteriorate again.

"However, debt-to-income ratios have risen in recent years, and with the underlying drivers of housing demand - population growth [and] low interest rates - remaining strong and demand outstripping supply, there’s a risk of a housing market resurgence, and a sharp lift in high LVR lending, if LVRs were removed at this time," Wheeler said.

“LVR restrictions have reduced financial stability risks as house prices became increasingly stretched. Requiring new borrowers to have a greater equity contribution in their house purchases reduced the overall riskiness of banks’ mortgage portfolios," Wheeler said.

“Nationwide annual house price inflation has declined to 1% due to LVR restrictions, the tightening in bank lending, the rise in mortgage rates and increasing concerns about housing affordability."

Wheeler's comments on LVR restrictions come after both National Party leader Bill English and Labour Party leader Jacinda Ardern, speaking as the September 23 election approaches, expressed dissatisfaction over how LVRs were perceived to be impacting first home buyers. English and Ardern's comments followed the Real Estate Institute of New Zealand calling on the Reserve Bank to remove LVR restrictions for first home buyers.

Economic prospects promising

Meanwhile, Wheeler said in the absence of major unanticipated shocks, prospects look promising for continued robust economic growth in New Zealand over the next two years.

“The greatest risk we face at this stage relates to the inflated global asset prices and the continuing build up in global debt," Wheeler said.

“If growth in the global economy slows, we have some scope to buffer our economy. We’ve greater room for monetary policy manoeuvre than central banks in many advanced economies. Our official cash rate is 1.75% – above the zero and negative interest rates of several advanced country central banks – and the [Reserve] Bank has not grossed up its balance sheet by buying domestic assets. With a budget surplus and low net debt relative to GDP, there’s also flexibility on the fiscal policy side.”

Wheeler's due to leave the central bank when his five year term as Governor ends on September 27. He'll be succeeded by Deputy Governor Grant Spencer for six months until an as yet unknown permanent replacement takes the reins in March.

Big drop in highly leveraged loans as 1st home buyers still get their share

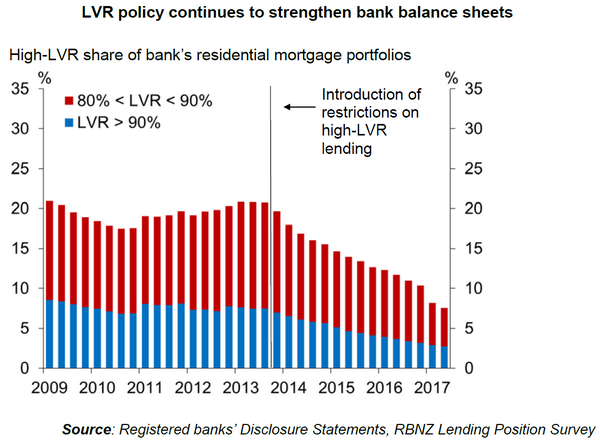

Wheeler noted that when LVRs restrictions were introduced in October 2013, 21% of the stock of mortgage lending across the New Zealand banking system was at LVRs of 80% or higher. With a third of new mortgage lending at that time happening at LVRs of 80% or higher, the overall stock of high LVR mortgages was "likely to approach" 25%.

"As a result of the LVR restrictions, the stock of highly leveraged loans across the banks’ mortgage portfolios is now around 8%," said Wheeler.

"While some first home buyers wanting high LVR loans have been affected by the restrictions, banks have given priority to first home buyers within their 10% speed limit," he added. "Over the past 2½ years the share of first home buyers in real estate transactions has been around 21%, its level in early 2013. Over this period, first home buyers have taken out nearly $21 billion of mortgage loans from the banking system, with 28% of that lending at LVRs greater than 80%."

He went on to say that the LVR restrictions have targeted reducing financial stability risks as house prices became increasingly stretched. The restrictions aren't expected to be a permanent fixture. The conditions for their removal, Wheeler said, would be signs that financial stability risks have eased, and a degree of confidence that these risks won’t worsen again when LVRs are removed.

"On the former measure, the financial risk picture is improving. Banks are carrying a lower share of high LVR mortgages as a result of the LVR limits having been in place, and the slowdown in house price inflation is positive - although prices remain very elevated relative to incomes and rents," Wheeler said.

"However, the underlying drivers of housing demand [being] population growth [and] low interest rates, remain strong with housing demand still outstripping supply. There is a risk of a housing market resurgence and a sharp lift in high LVR lending if LVRs were removed at this time. The [Reserve] Bank will continue to review developments, bearing in mind that removal could be made in stages as a safeguard to a resurgent market."

The case for debt-to-income ratio restrictions

Wheeler said it’s encouraging that NZ-wide annual house price inflation has dropped from a peak of 21% in August 2015 to 1% now. He attributed the decline to several factors including the tightening of investor LVRs in October 2016 by the Reserve Bank, more restrictive lending conditions by banks, the rise in mortgage rates early this year, and increasing concerns about housing affordability.

However, he remains cautious.

"A strong resurgence in house price inflation would increase the risk of a subsequent future correction. With a debt to income ratio of 167%, up from the 2009 peak of 159%, households are already heavily exposed to the risk of rising interest rates or falling house prices," Wheeler said.

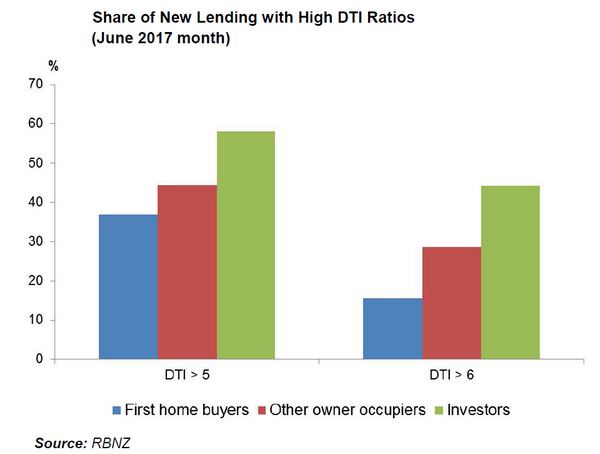

"In addition, the share of high debt-to-income (DTI) lending to first home buyers, other owner-occupiers and investors is high, making borrowers more vulnerable to rises in interest rates and/or reductions in income, e.g. associated with unemployment. This increases the risk of forced sales in a downturn leading to falls in house prices and flow-on effects on bank balance sheets and the broader economy. This is why we have been consulting on whether a DTI instrument should be included in the macro-prudential toolkit. We wouldn’t seek to use it while the housing market continues to moderate."

26 Comments

Good on him

Couldn't have said it better.

Accepting now that temporary measures have become a permanent feature should we not now reform these measures to support first time buyers into the market? This is likely to have profound and ongoing implications for New Zealand society and I would venture that the idea housing, however basic, could be out of reach for a generation is fairly unpalatable to many of us.

Once the price of housing corrects downwards, it becomes in reach. That's how you help FHBers into the market - the price of entry, and the cost of construction, whilst variable, is the least impediment to a lower price structure.

Fix the price and the LVR problem goes away for FHBs. I see protecting them from a future of massive indebtedness as a positive.

I don't think you have thought that through.

Would you mind expanding on how that is meant to work?

Does the government just walk around slapping price tags on houses and if so why would anyone sell? We are already see listing dropping quickly in Auckland they will hit all time lows if you put fixed prices.

You are sort of right. No more debt. But only because there won't be many houses to buy.

There are many levels the government can pull on both the supply and demand side that would reduce house prices. Even if nobody sold an existing home, if new houses were supplied below the current market price then house prices would fall.

For a start the government should get rid of the first home subsidy and Kiwisaver withdrawal which just enables more debt, and therefore more money to Nationals rich buddies with the FBH taking on all the risk. 20% deposit is quite reasonable. If 20% is not achievable then the house price is too high. Tax land on unimproved value and open up building standards to more methods and materials and you'll see the market totally change.

Why not get rid of all checks on lending, then everyone can borrow to own a house no matter how overpriced it is, what could possibly go wrong?

Meanwhile, Wheeler said in the absence of major unanticipated shocks, prospects look promising for continued robust economic growth in New Zealand over the next two years.

“The greatest risk we face at this stage relates to the inflated global asset prices and the continuing build up in global debt," Wheeler said.

These comments are problematic. First he talks of "major unanticipated shocks" without actually being able to point out what they might be. Wheeler then goes on to identify the root cause of risk (and no doubt the previously referred to "shocks") as excessive debt and asset price "bubbles" in the NZ and global economies.

So what he's essentially implying is that the debt and asset prices are driving the health of the economy. There is no independence, Debt and asset prices are not the by-product of a successful economy. They are the economy in itself.

The only real takeaway from that is that nothing has changed since the GFC. In fact, in terms of magnitude, it is quite possibly far worse.

Talk about a "cup half empty" interpretation. I understood Wheeler to be saying, barring something bad happening (e.g. a flood, earthquake or zombie apocalypse) NZ will continue to have economic growth.

He then cautions that there are risks in respect of asset bubbles and increasing debt.

The two statements are not linked.

No, it's an interpretation based on what Wheeler actually said. Wheeler says that the major risks to the health of the economy are high asset prices and excessive debt (if you take umbrage at the existence of those factors, direct your protests at Wheeler. His words and perception, not mine). That suggests that Wheeler thinks those factors are "key drivers" and removing them will negatively affect the health of the economy. Whether or not these "drivers" are related to "shocks" is unknown, but very odd if Wheeler structures his communications by mentioning "possible shocks" then highlights the issues of debt and asset prices.

Applying your "feelings" (half empty / half full) has nothing to do with probability and outcomes.

Wheeler is undoubtedly correct: LVR's are best left in place for a while yet.

RBNZ has learned (like everyone else): property prices in NZ are like an untamed lion....... give them a bit much leash and they will take off and be damned hard to reign back in.

What he actually said was "LVR restrictions have targeted reducing financial stability risks as house prices became increasingly stretched" and that the conditions for their removal would be "signs that financial stability risks have eased, and a degree of confidence that these risks won’t worsen again when LVRs are removed."

So based on Wheeler's perception and using the power of inference, the level of financial stability is not strong enough to remove LVRs.

If wheeler believed economic growth was been funded by asset prices and debt why would he introduce the LVR restrictions?

Your logic goes:

1) Wheeler thinks asset prices and debt are funding economic growth;

2) Wheeler does not want a shock to stop this growth;

3) Wheeler introduced LVR restrictions to prevent asset price growth and excessive debt (which is inconsistent with (2) ergo the logic is false).

Nope. The logic of what Wheeler says is as follows:

The greatest risk we face at this stage relates to the inflated global asset prices and the continuing build up in global debt"

If asset prices and debt are the greatest "risk", they're effectively a "driver". That means their absence will have the greatest negative impact on the economy.

Also, it cannot be disputed that debt-driven bubbles are also positive for an economy, particularly on consumer spending. That's why bubbles are promoted and tolerated by institutions.

Wheeler said in the absence of major unanticipated shocks, prospects look promising for continued robust economic growth in New Zealand over the next two years.

It's up to you to determine what these "unanticipated shocks" could possibly be, but Wheeler's mandate is related to financial stability, which he believes he can mitigate using LVR restrictions.

If you think that there is no relationship between financial stability, debt, and asset bubbles, that is entirely up to you.

Are houses for New Zealanders anymore?

Or are NZ houses now an investment vehicle for offshore buyers, who may also be buying via NZ residents of some sort?

So the LVR is another measure against NZers.

"As a result of the LVR restrictions, the stock of highly leveraged loans across the banks’ mortgage portfolios is now around 8%," said Wheeler.

Only partly correct. A decent portion of the drop is down to increased housing stock value - i.e. the V, not the L.

Nope, that's wrong.

Banks are required to report LVR stock results using V as-at loan origination.

“With a debt to income ratio of 167%, up from the 2009 peak of 159%”

I cant reconcile those numbers with any of the BIS data. Closest I can get is P:A:M:770:A (lent to private sector by all sectors) However according to the BIS, private sector debt in NZ has been steadily increasing since mid 2014. That’s strange isn’t it. House prices have been skyrocketing (okay that makes sense) but high LVR loans have been on the decline? That indicates to me that FHB’s have not participated in recent price rises.

Wheelers argument is that introducing LVR's in 2014 successfully decreased investor activity and increased FHB's. It is in the detail on the RBNZ website.

That doesn’t make sense empirically or intuitively. Banks lend on equity.

Good point

well said Sir

QE also is being talked about on how best to start unwinding. But its been a long wait for the authorities before they could start thinking on this...wrong foot and u could create more mess than what u have cleaned by introducing QE

Same applies to LVR..m sure very diligent and well thought strategy will already be in place on how and when to start unwinding LVR..its bit early in my view..still some water to flow under the bridge..also i dont agree that timing and nature of that strategy shld be made public..RBNZ knows how best to play this and we shld leave it to them..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.