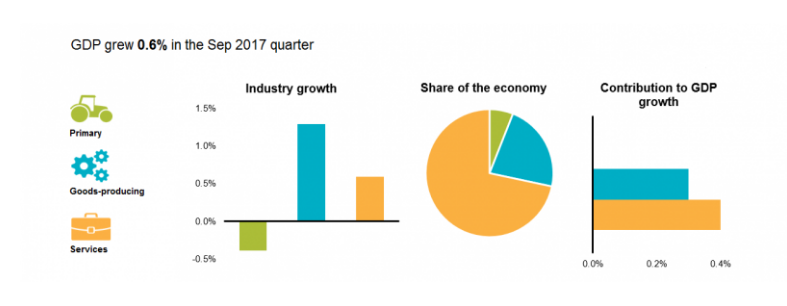

New Zealand Gross Domestic Product (GDP) grew 0.6% in the September quarter, which was in line with the median of economists' expectations.

The September year GDP percentage increase was 2.7%, and the annual average change was 3.0%.

The Reserve Bank had expected 0.7% quarterly growth, and 2.6% annual growth. This comes after the June quarter growth rate was revised up to 1.0% from 0.8%, Statistics NZ says.

Statistics NZ's national accounts senior manager Gary Dunnet says the increase was helped by a recovery in construction activity during the September quarter, unwinding the previous two quarterly falls.

“This reflected higher construction-related investment, with investment in infrastructure and residential buildings also reporting strong increases,” says Dunnet.

Service industries, including health and residential care, business services, and arts and recreation also contributed to the growth.

"Household spending was up 0.9%, driven by spending on durable goods, and services. Spending on durable goods increased 2.3%, due to increased spending on audio-visual equipment such as televisions and consumer electronics, clothing, furniture and furnishings, and used cars," Dunnet says.

Household spending on services increased 0.8% in the September quarter, with increases in spending on recreational and sports services.

Meanwhile, GDP per capita was up 0.2% in the September quarter, down on a 0.5% June quarter increase. For the September year, GDP per capita was up 0.8%.

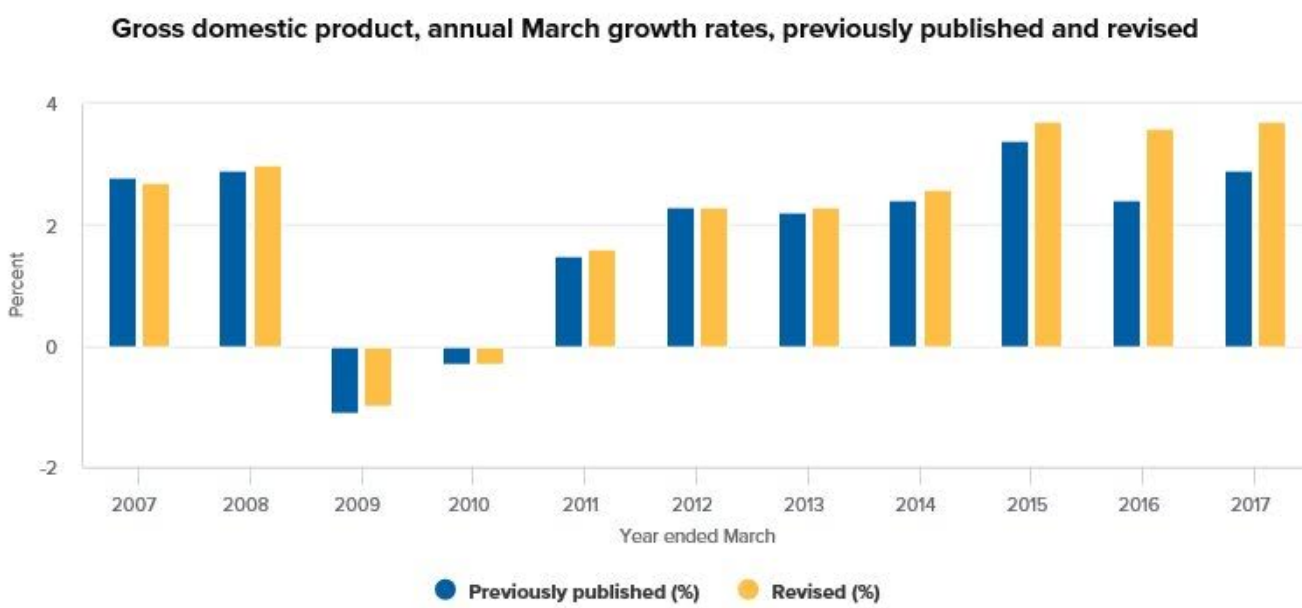

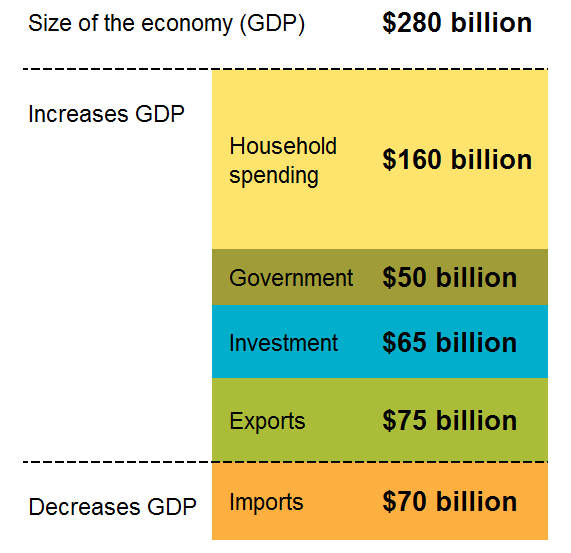

"Annual GDP growth for the year ended September 2017 was 3.0%. The size of the economy in current prices was $278 billion," says Dunnet.

Earlier than expected OCR hikes?

ASB economists Nick Tuffley and Jane Turner say revisions over the past two years lifted GDP growth by a cumulative 1%, revealing a much stronger economy than previously believed.

"The Reserve Bank is likely to focus on the implications of the revisions for future inflation pressures. With the economy performing better than previously thought, the Reserve Bank may bring forward its expectation for Official Cash Rate [OCR] increases closer to our view for hikes to begin in early 2019," Tuffley and Turner suggest.

The Reserve Bank's November Monetary Policy Statement didn't expect the OCR to increase until around late 2019.

Westpac senior economist Michael Gordon notes the NZ dollar rose 1/3 of a cent against the greenback on the data, and 1/2 a cent against the Aussie dollar.

"The upward revisions to GDP will have implications for monetary policy. To some degree they suggest a higher rate of potential growth than previously thought - we know that inflation was subdued over much of the revision period. But they also suggest that the New Zealand economy may be closer to full capacity than thought," says Gordon.

'Broad-based inflation pressures still MIA'

ANZ senior economist Phil Borkin takes a different view to the ASB economists.

"At face value, the stronger historical growth performance suggests the economy has absorbed more spare capacity, running with a larger positive output gap than previously thought. All else equal, that is obviously relevant for monetary policy," says Borkin.

"However, with broad-based inflation pressures still MIA, it is actually not clear-cut. There remain plenty of questions regarding the outlook for inflation from here, so we suspect the Reserve Bank will be somewhat cautious in interpreting these figures hawkishly. Rather, we suspect a good chunk of the upward revisions will feed straight into its estimates of the economy’s potential growth rate, rather than its estimate of the output gap."

Borkin notes a new annual benchmarking methodology used by Statistics NZ and some other methodological changes have seen historical GDP revised up significantly.

"For example, in the years to March 2016 and 2017, the economy is now reported to have grown at 3.6% and 3.7%, from 2.4% and 2.9% respectively. This paints a vastly different picture with regards to the economy’s recent performance," Borkin says.

Size of revisions a surprise

Meanwhile, Tuffley and Turner say the size of Statistics NZ's upward revisions surprised them.

"Over the past two years of data, Stats NZ has revised up GDP growth by a cumulative 1%. Just under half of this growth, 0.4 percentage points, was added to the first half of 2017. The rest of the upward revisions appeared to take place in the 12 months to September 2016. The economy’s performance on a per-capita basis now also looks much healthier - although we do note that over the past year momentum did slow with annual per capita growth of 0.8%, compared to 1.8% annual growth in September 2016 and 2.1% in September 2015," the ASB economists say.

"In summary, momentum is healthier than expected but growth did still slow over the past year. According to Stats NZ, the key source of revisions over the past two years was a higher value-add in the business sector, with income growth outperforming inputs, and incorporating unconsented repair work from the Canterbury earthquake rebuild. Meanwhile, dairy production’s value-add contribution to the economy has been revised considerably lower, possibly reflecting the increased use of supplementary inputs by the industry, i.e. feed. But there was some offset from dairy manufacturing activity having a higher value add than previously estimated."

'Quality bump'

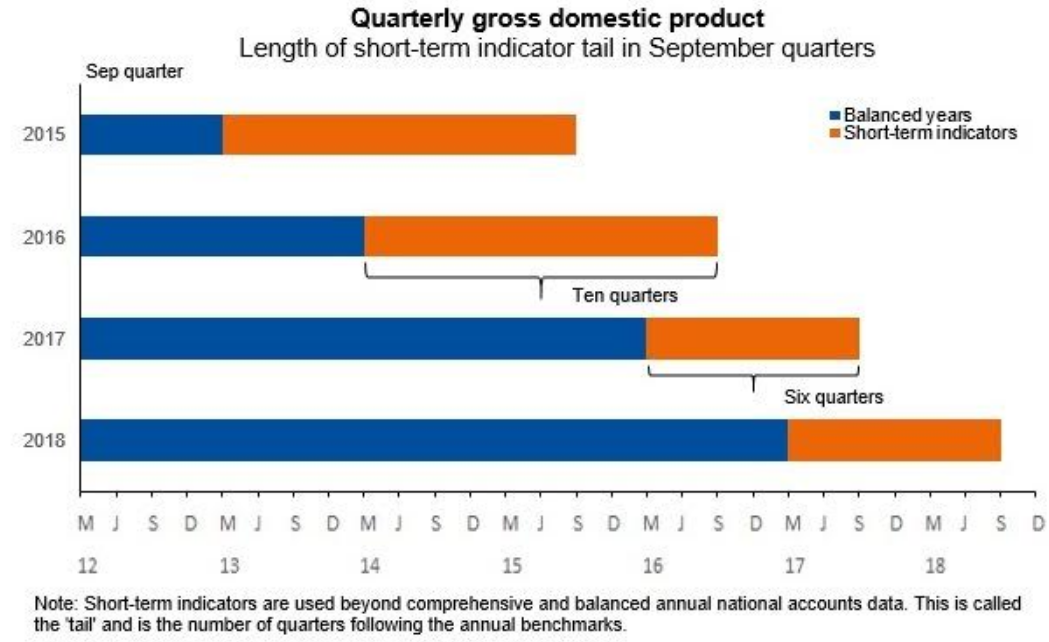

Meanwhile, Statistics NZ says GDP quality has received a "bump" from new annual benchmarks, noting in the September quarter annually it makes changes to improve quarterly GDP data.

"These changes allow us to incorporate more accurate, but less timely data, and improve the quality of our quarterly series. In 2017, we analysed and reconciled an extra year of national accounts data. We now have a comprehensive view of the economy and the goods and services flows up to the March 2016 year. This sees our national accounts statistics reflect a more up-to-date structure of the economy," Statistics NZ says.

"It also allows us to introduce an additional two years of annual benchmarks to our quarterly GDP estimates series this year. Quarterly GDP is a comprehensive suite of short-term indicators that allow us to translate the more historical view of the economy into a quarterly basis and provide contemporary insight into economic growth."

"With two new annual benchmarks, rather than the usual one, we will now have four fewer quarters of economic growth being based solely on short-term indicators. This means that, when we publish the September quarter, instead of the latest 10 quarters being based on short-term indicators, only the latest six quarters will be. This is shown in figure 1 [below]. This takes the maximum number of quarters that will be based on short term indicators from 13 to nine," Statistics NZ adds.

18 Comments

In the latter stages of the September 2017 quarter, we discovered a historical error in the ‘secondary income outflow’ component of the balance of payments data – in the ‘miscellaneous current transfers of general government’ data series. This error affects the secondary income data back to the December 2015 quarter. We have chosen to delay further historical corrections at this time until we complete a full investigation of the flow-on effects across the balance of payments and the wider suite of GDP measures. In early 2018 we will determine the best time to implement full correction and revise affected time series.

http://datainfoplus.stats.govt.nz/item/nz.govt.stats/21aff6d5-18b6-4a65…

The solution to every social and economic ill is to "grow our way out of it."

The solution to unemployment = jump-start growth by expanding consumption, spending and borrowing.

The solution to stagnant wage = jump-start growth.

The solution to declining profit = jump-start growth.

The solution to government deficit spending = jump-start growth.

And so on.So what happens when most people have not just the basics of life, but a surplus of stuff? Where is the growth going to come from if people already have everything? Do they:

1. Replace a perfectly good product with a new product and dump the old one

2. Buy duplicates and put the surplus products in the closet or storage facility.

3. Buy gimmicks (Pet Rocks, etc.) that are tossed in the dump shortly after the holiday gift-giving season ends.

This is of course insane. Decisions aren't being made as if scarcity matters; the goals and incentives are set to encourage perverse and destructive overconsumption and overspending: not only are we squandering resources in the sacrifice to the false gods of "growth," we're indebting households to do so, stripping income that could have been saved and invested in productive uses.

In the lunatic asylum of the current economic model, media anchors sport grins of delirious joy when reporting increases in holiday spending, as if a bump higher from $680 billion to $700 billion is a gargantuan win for the flailing economy. Wasting resources, capital and income on stuff nobody really needs is a monumental disaster on multiple fronts. Rather than establish incentives to conserve and invest wisely, our system glorifies waste and the destruction of income and capital, as if burning time, capital, resources and wealth on stuff nobody needs is strengthening the economy.Isn't it obvious that this system is a one-way path to collapse?

Isn't it obvious that if we set out to design the most perverse, toxic and doomed system possible, we'd end up with the Keynesian Cargo Cult's insane permanent growth/Landfill Economy? Common sense suggests that, but common sense is scarce in a world trapped in a bizarre Keynesian madness.

(CH Smith 20/12/17)

Got to look after the banks you know.

In a Trump world the new "beneficiaries" are the super rich, multinational corporates and klepto-autocrats.

The rest of us will be encouraged take on debt to buy stuff we don't need, but education, health, other essential services and infrastructure will be reclassified as unrealistic impediments to progress and unaffordable, unless ordinary citizens embrace more debt. New feudalism just rewards the Peter Theil's of this world.

The growth rate is getting high enough that OCR hikes are envisioned. They are currently getting up to the 3%+ range annually. Curious... The GDP growth rate still needs to increase by almost 40% in order to attain the GDP growth rates that are in the current government financial estimates. See: http://www.labour.org.nz/fiscalplans-forecasts Be fun to see where the OCR ends up if the labour fiscal plans are accurate!

Note that they are forecasting >5% gdp increase from this fiscal year to next fiscal year. They get "conservative" for the year after next, dropping the gdp increase forecast down to 4.7%.

So they start with $78bn in tax to June 18, then they forecast that they will increase that by an average of $4.4bn for each of the following 4 years.

In the financial year ended June 2022 they expect to take $95.76bn in tax, an increase of $17.76bn or 22.7% over this year.

Fiscal responsibility is easy if you tax the productive sector until it’s on its knees. The moniker Taxinda is absolutely on the mark.

Any economic commentator who gets excited over the prospect of earlier OCR hikes is, in effect, sticking

it to the thousands of young hardworking first home buyers who have made that ultimate stretch to secure

their first home. I thought we were over that stage when particularly the big bank's economists were each

trying to outdo each other in predicting the earliest hike.

Anybody that mortgaged themselves to the hilt in times of record low mortgage rates and didnt leave wiggle room for the inevitable increases was just plain foolish.

Using that logic, the young have already stuck it to the old...

So - not just the 'migration driven short term saccharine hit ' which many commentators here dismissed the GDP growth trend as.

GDP up 0.6%, GDP per capita up 0.2% so immigration is still providing twice as much growth as productivity.

Yup sure, but ideologues insisting that productivity and underlying economic growth were stagnant, had it wrong. In our businesses, we were seeing non immigration driven activity running quite strongly all year and were puzzled at some of the data. The piece about renovation spending not captured by building consent data, caught my eye - I suspect that might explain a bit.

You are right it is not stagnant - productivity is actually in decline https://www.interest.co.nz/opinion/91435/2017-interesties-featuring-jac…

Interestingly the contribution from productivity in total since 2013 has been negative - roughly aligned to the period of largest house price gains.

Way to GO Labour! #Letsdothis

You mean the Labour party that lost heavily at the election or some other 'labour' entity?

Hmmm, they lost so hard they have their person in the PMs office. Can I "Lose" Lotto this weekend please?

Sorry you poor losers but we have MMP.

Yep, you got it. The one who learned from TV news she was to be PM. Your lotto analogy is good - you don't have the numbers to win the contest but you still travel to Wellington to get the prize.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.