This week’s Top 5 comes from Infometrics senior economist Brad Olsen.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Why’s everyone talking about a lower OCR when it’s become impotent?

Next week’s “live” Monetary Policy Statement and official cash rate (OCR) review has everyone competing to talk down the OCR to lower and lower levels. But the fact remains that a lower OCR might not be the panacea that everyone hopes. Growth in investment and spending looks like it will continue to weaken, and not because borrowing costs are a restraint. In the face of monetary policy becoming less effective at stimulating the economy, two questions must be asked: is it still worth it to cut the OCR if not a lot will change, and what’s our Plan B?

Westpac has hopped on the 1% train, calling for two further OCR cuts in 2019. Chief Economist Dominick Stephens noted that the rationale for the call change was both domestic (a weak labour market outlook) and international drivers (the potential for other central banks to cut and the effect on exchange rates).

Westpac is right that the Monetary Policy Committee (MPC) is ready and willing to cut further, but the lack of effect that further OCR cuts will have on the economy is worth repeating: monetary policy has been accommodative for a long time, but the economy has still slowed. OCR cuts shouldn’t be made just because the economy is slowing, or inflation expectations appear lower; the cut should be made if this action will alter the economic and inflation outlook. If a cut won’t change the economic outlook, then is the cut really justified?

“The Reserve Bank will be well aware of these recent developments. Importantly, recent experience is that the new Reserve Bank Monetary Policy Committee has been activist and responsive to signs of slowing growth. We think they will respond to these latest signs of weakness by cutting the OCR in August, and stating that they might cut the OCR further, depending on the data. We expect that the RBNZ’s published forecasts will show the OCR dropping to 1.1%, implying a good chance (but not a certainty) of another cut. Such commentary would be more dovish than the May MPS, which shied away from providing forward guidance on the OCR.”

2. OCR cuts won’t stimulate the economy enough.

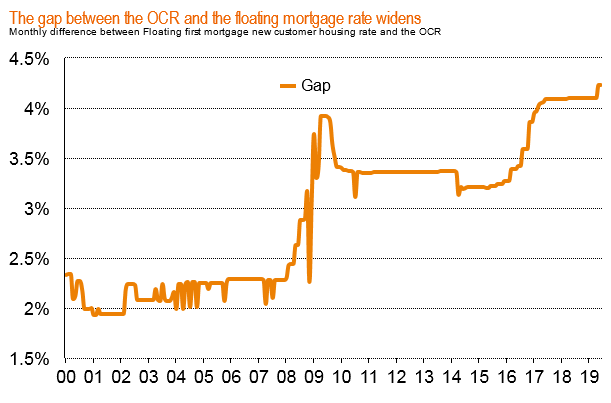

In our latest forecasts, Infometrics has noted the impotence of further OCR cuts. There’s a lack of pass-through of the OCR to retail rates, with May’s 25 basis point (bp) cut only taking the floating mortgage rate down 12bp. The gap between the floating rate and the OCR continues to increase, highlighting the reduced effectiveness of lowering the OCR. Even though retail interest rates will continue to fall if the OCR is cut lower, a) it’s not all going to be passed on and b) it’s not going to make much difference to decision-making anyway, with uncertainty holding back business investment, rather than borrowing costs.

“The Reserve Bank arguably offers even less hope for stimulating the economy. The cut to the official cash rate in May had a limited effect on retail interest rates, and another cut next month is likely to be similarly impotent. “Interest rates are already very low and are not a factor holding back business or consumer borrowing,” says [Infometrics chief forecaster Gareth] Kiernan. “Instead, businesses are reluctant to invest because their profitability has been squeezed by rising costs, while soaring property values have simply priced many potential buyers out of the housing market.”

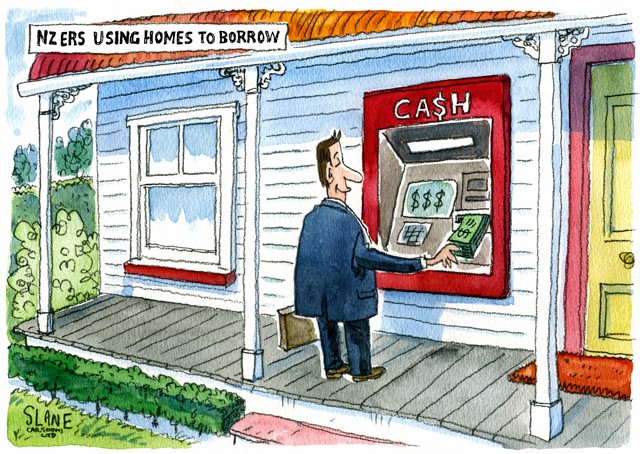

3. Stimulating the economy, or just gilding the housing market?

If anything, the limited effect of a lower OCR on retail rates is only likely to boost the housing market, rather than provide for more productive allocation of capital. Boosting the housing marking through cheaper credit would increase private debt relative to incomes and GDP, with any accompanying rebound in consumption growth unsustainable.

Bernard Hickey’s recent brilliant piece about the “amour plated housing bubble” highlights not only that this boost in the housing market was ably assisted by previous OCR cuts, but that this assistance looks set to repeat. A lack of productivity, global uncertainty, and a shallow capital market in NZ makes housing our most attractive asset option, but also limits the influence of an OCR cut on the economy, aside from pumping up housing more and more.

“… the Reserve Bank cut the Official Cash Rate by nearly 600 basis points in less than a year, starting in July 2008. New fixed mortgage rates fell from nearly 10 percent to 5.9 percent by early 2009. They have since fallen to under 4.0 percent as the globalisation of services markets through the mobile phone drives prices lower in the same way the globalisation of manufacturing did through the 1990s and 2000s.

… the Reserve Bank is expected to cut the Official Cash Rate to 1.0 percent by mid-November, which could see fixed mortgage rates drop towards 3.5 percent. That's because inflation remains under the middle of the RBNZ's 1-3 percent target range and both the global and local economies are slowing, which is sucking further air out of inflation, aside from housing costs. The Government's spending plans detailed in Budget 2019 are forecast to actually reduce stimulus in the economy, which would force the Reserve Bank to push even harder on the interest rate lever. That may change next year, but for now the Reserve Bank is doing all the heavy lifting.”

4. Below zero is an option, and it might be closer than we think.

Last year’s RBNZ Bulletin article, Aspects of implementing unconventional monetary policy in New Zealand, highlighted the possibility of a negative OCR. It’s an option that is actively being explored as the zero-boundary gets closer. Heading into negative territory would see savers having to pay to store cash which, in theory, could stimulate greater spending activity in the near term.

But a negative OCR has risks. Too low, and cash hoarding becomes a viable option. Hoarding could limit any increase in spending and could also create liquidity issues for banks.

Both Japan and Europe currently have negative central bank rates, and both have also struggled to generate a recovery in economic growth. It’s worth considering how much of an effect a negative OCR could have, either because a) hoarding occurs sooner than expected, limiting the policy’s effectiveness, or b) the OCR turns negative but borrowing costs remain higher due to a lack of pass-through, effectively leaving us without an OCR channel to influence monetary conditions.

“Based on the overseas experience discussed, it would appear that a modestly negative OCR could be implemented in New Zealand. The key consideration is how negative the OCR could go before different segments of the financial market begin to hold cash rather than negative yielding securities. At that point the transmission of further OCR reductions to the wider economy would be hampered.

Private banks, business and retail depositors would face negative interest rates at differing levels of the OCR. The Reserve Bank uses a range of liquidity instruments in its domestic market operations, priced at various spreads to the OCR. Interest rates in overnight wholesale cash markets tend to trade close to OCR. As a result, banks would likely face negative short-term wholesale rates as the OCR itself turned negative. It is worth noting that a few Reserve Bank facilities are transacted at margins below the OCR. For example, if the OCR fell below 1.5 percent, bond lending facility transactions would be at negative rates.

The corporate sector would experience negative rates after the banks, and would face the choice of investing in negative yielding fixed income securities or holding physical cash. Raising finance through corporate fixed income securities would also be affected; based on current spreads yields would become negative at an OCR of between -0.20 percent and -0.35 percent.

Retail depositors are offered a range of deposit rates by banks depending on the term. Call deposits are currently priced about 1.35 percentage points below the OCR, while the weighted average of term deposits is about 0.90 percentage points above the OCR. Based on oversees experience, it is likely that banks will maintain call rates as the OCR falls, but reduce term deposit rates in line with the OCR. Banks would be faced with the choice of accepting falling interest margins, or increasing the spread on lending rates. Were this to occur, it would represent a weakening in the transmission of monetary policy.”

5. Fiscal policy will need to take the driver’s seat, and fast.

Monetary policy, for the reasons highlighted above, has at best lost most of its potency and, at worst, has reached the limit of its reasonable usefulness. If monetary policy is out of action, fiscal policy becomes the key to any economic recovery for New Zealand.

However, roadblocks remain to getting fiscal stimulus going. The government is struggling to get some of its funding out the door and is lacking a group of ready-to-build capital projects that could provide relatively immediate stimulus to the economy. Without substantial progress towards securing an inventory of construction-ready projects, and more policy work to design and implement supportive tax and transfer settings, New Zealand might well be caught napping when economic growth falls below 2%pa.

“There is considerable uncertainty around the impact of fiscal stimulus on general economic activity. In any stimulus, there is a high risk the additional spending is saved, or spent outside New Zealand, reducing its stimulatory impact.

Most spending projects will face constraints beyond lack of funding. These include capacity constraints in the construction sector, limited ability of agencies to manage additional large projects, and long planning times required for implementation. While we can identify some areas of capital spending that can be quickly increased, focused on repairs and maintenance of the public estate, these alone are unlikely to provide a fiscal stimulus comparable in size to those implemented by most developed economies in the GFC.

Tax changes or cash transfers to households are the policy options more likely to meet the criteria outlined above. These also have the advantage of being potentially highly targeted to specific groups, aiding equity objectives. The tax options could include temporary variations to some rates. Cash transfer programmes can be an effective stimulus, but, if poorly designed may lead to perverse outcomes if the stimulus is saved or spent abroad.”

52 Comments

... wouldn't it be easier and healthier to just accept a recession - embrace the flushing out of financial excesses that it brings - rather than force the OCR down through the floor boards and into the basement ?

Politicians would rather keep smoking the financial crack pipe than shake out the fraudulent sectors of the economy.

That would be a tacit acknowledgement that inflation targeting and Monetary policy don’t work. We must keep the illusion going for longer, most likely switching to fiscal policy to keep things propped up for a while.

We need to try to push that out so it only affects other people, not ourselves. 'Tis the way today.

No. The only people crying are the pensioners whose TD rates are taking a battering. Time to eat your principal old folks.

Yeah calitalism requires the occasional bloodletting to weed out the fools, criminals and the like. The GFC however was all about keeping the players not just out of gaol but continuing the status quo.

The payout now will be even worse than it should have been in 2008.

... yes , it is the nature of our capitalist system that we need to have recessions occasionally... the tide must go out to expose those who're swimming naked ...

Kick the can down the road , as we have been , and the eventual clean out will be an epic flushing ... GFC repeated...

Except that no political party wants a recession on their watch or they are gone next election. We have totally the wrong lot in control with the current COL, they have zero business experience and its going to hit hard this time if GFC2 comes before next election.

Can’t see cuts stimulating housing. Best investment at present is gold stocks. Everything else is a bubble.

Bitcoin ! ... if ever there was a red light flashing its warning to the financial world it is the bubble on steroids , AKA : Bitcoin ..

Bitcoin is a con.

Bitcoin is the ultimate Ponzi. Make something out of nothing, sell it for actual money, watch it rise to a fictitious value when everyone tries to get on the bandwagon. If there is anything out there that can suddenly go to ZERO value overnight, this is it. The only good thing to come out of this was the Blockchain technology.

GDX was up almost 6% today. Only problem with gold mining stocks is that they've been rising rapidly. The word's already out.

Not yet it isn’t. How many investors hold gold? Most don’t. Wait until they add.

..."The impotence of OCR cuts"

An interesting, but nonetheless misleading headline.

Cutting the OCR in half from April 2015 and more has significantly raised the net present value cost of funding outstanding financial liabilities: - Read more (PDF)

I can't understand how BH links smartphones with low interest rates. What services avail via smartphone could have such an effect...uber eats?

As for fiscal policy, how can any government enact it anymore, they've sold off all non core govt assets like ministry of works. They have to go back to the direct method. The old MOW might not have been everyones favourite son but it sure kept regional economies going via some pretty big, well paid jobs on public works schemes. Put that kind of money toward any of the privately owned infra companies and it will just go to shareholders while the workers eeek out $18 p/hr....

Fiscal spending sits uncomfortably with public sector ideology in NZ and Australia. Singapore and Japan are the masters of implementing and executing. In NZ, we don't really have the same level of coordination and capacity so it's spending just for the sake of spending. Perhaps better to top up everyone's bank accounts and let them go on a shopping spree.

I've always argued for the establishment of a Conservation Corps. Anyone between the ages of 18-23 can join it for a maximum of 3 years. Set the salary around the average wage. Best stimulus available getting money into the hands of youth. Instead, we presently lumber them with student debt or send them into the arms of criminal gangs.

Bernard Hickey’s recent brilliant piece about the “amour plated housing bubble” highlights not only that this boost in the housing market was ably assisted by previous OCR cuts, but that this assistance looks set to repeat. A lack of productivity, global uncertainty, and a shallow capital market in NZ makes housing our most attractive asset option, but also limits the influence of an OCR cut on the economy, aside from pumping up housing more and more.

I don't buy into this. With all the turmoil caused by too much cheap credit, it doesn't make sense to start speculating on the target (housing) of all that cheap credit. Of course, if there are historical examples to compare with, the idea might carry some weight. The Japan experience when rates were cut drastically doesn't support this view. The Japanese didn't all start piling into property when debt became cheaper.

Suggesting that piling into the NZ property market for safety and security appears to be a daft idea to me.

It is hard to know what the risk is for another economic crisis like the GFC. But if the risk exists and I would assume from articles like this, that it does exist, then New Zealand should learn some lessons from the 2008 GFC.

Chiefly not to let the construction industry collapse like it did between 2008 and 2015. That interest rate cuts by themselves may not stimulate the construction industry.

To mitigate against this potential economic crisis the coalition government should immediately start a construction future proofing fund to create a mechanism to provide modest fiscal subsidies to the construction industry. Such as a subsidy for seismic strengthening and energy efficiency in developments that provide an equitable mix of housing typologies, ownership and tenure models and that include a range of affordable rent/price points.

If the government had such a mechanism then if a GFC type downturn occurs it could ramp up fiscal support to the construction industry, to keep the industry building affordable houses, which improves disposable income for middle to low income earners. This would help stimulate the economy at multiple different levels thus counteracting the economic downturn.

I wrote about this at the end of this article. https://www.interest.co.nz/opinion/99927/brendon-harre-has-proposal-inc…

"not to let the construction industry collapse like it did between 2008 and 2015"

Say what?

Builders have been on an endless gravy train of house price bubblification, "value add renos"and an immigrantion ponzi since 08 ... all those nice utes dont grow on trees

and why subsidize any one industry? where is your end game here ?

Because this isnt a downturn coming - its a depression

If growth aint coming back and the only way forward is endless handouts via Govt deficits, having a few earthquake proof houses will be the least of our worries

Inflation is here alright - just not in the official figures

The construction of houses per capita halved post GFC! The GFC was rack and ruin for tradies. Housing bubblification was good for bankers, landlords, real estate agents... not so good for workers and businesses which have skills at building things....

Have to disagreeably agree with you Brendon, now construction is in the "too big to fail" category. The government will have to step in once the margins for developers and builders has eroded, and should be drawing up plans to keep everybody employed and everybody housed.

Tradies and sub-contractors are not too big to fail -they are the first to be laid off. Maybe Fletchers is. But it shouldn't be. The government needs to do more than one thing at a time for the housing and construction sector. Namely if they provide a construction subsidy then then they also need some reforms to break up the building supplies duopoly and they need to tackle landbanking....

So, everything is predicated on keeping the housing sector going strong ?. That includes the construction, banks, speculators, etc. The only game in the country ?

Interest rate cuts don't work so well when house prices are declining, according to the BIS. Funny that wasn't mentioned.

Raising tax thresholds and cutting tax rates, especially on the private sector, would solve the problem, of course. Labour just hate the very idea, of course. NZ seems set for yet more Patronage networks on the Roman model, and less reward for those what can. The Decline of the West is easily reversed, but we gotta want it first.

And we insist on primarily taxing hardest those who engage in productive work, while giving a free ride to windfall gains and landbanking. Then wonder why we're not gaining in productivity.

The policy of running a current account deficit forces us to import excess capital, which pushes up the price of existing assets. This is policy. It is a distraction to blame the individuals who benefit from the skewed incentives, whether by accident or design. The problem is the policy, not each other.

It is very difficult to design a tax-cut that doesn't benefit high-income earners more than low-income earners. Not only are tax-cuts likely to be inequitable they are also inefficient as high-income earners tend to save more and have more overseas trips. So tax-cuts to high-income earners are less stimulatory than they could be.

NZ already subsidises housing -it is called the Accommodation Supplement. It is benefit that goes more to landlords than tenants.

NZ would be better off in my opinion subsidising the building of houses not the renting of them.

Building affordable homes that are warmer, dryer and more likely to survive earthquakes should be considered an infrastructure asset that provides long-term benefits to the nation.

If a tenant, gets to live a house that they could not otherwise afford, they surely benefit as well? are you saying that if it wan not for accommodation supplements, rents were going to be cheap as chips? i totally accept that the no subsidization would have brought the rent floor down. But not by much. And the people who get the subsidy would have still been unable to afford the rent so they would have needed government housing.

Even if land was free, the cost of construction, infrastructure, rates, insurance etc, would have required a bottom level of rent that would have still been unaffordable. If you are going to build cheap houses (e.g. poor insulation) then you would need to subsidies power prices (what happened in NZ before privatization). The underlying problem of low wage economy, low skill work force, unfavorable geographical location (for business purposes at least) is the underlying driver for the need for "subsidy" for things that people cannot afford. The seller of those otherwise unaffordable things will off course profit, but it is a fallacy to say that the consumers who are getting a free subsidy are not benefiting from it as well.

Pretty easy actually, reduce tax rates below 50k of income and increase at them at the top end so low earners get a cut and high earners pay the same or more.

Difficult to sell to the rich, but it's certainly not difficult to design.

If the economic stimulus package included taxes increases for the high income earners would National call it the tax increase package? Or maybe they would moan about it punishing success....

You might be missing my point. If the objective is to stimulate the economy, my contention is that tax cuts are likely to be the most effective way of doing that. The objective is not to balance the budget, but for the government to inject money into the veins of the economy. Tax cuts allow each of us to choose how best to use the money. By all means skew it to the lower paid, they will tend to spend it, if increased spending is desirable. Skew it to the higher paid, if increased savings is desired. Don't get sidetracked.

The point is related to how industrialisation works. If money flows to the masses, eg, from jobs in textile manufacture and mining, then the whole of society benefits and living standards rise for all. If money flows to the government or finance, as in the oil kingdoms, then the top echelons of society benefit greatly, and everyone else depends on their patronage (trickle down). Eventually, the starving people at the bottom revolt.

I see the problem as the value of the underlying assets that have been borrowed against. Nearly anyone can get a credit card buy a new car, great holidays, big house, it's the ability to service that debt thats going to cause us to come unstuck.

We don't have the earning potential to justify the housing bubble, it was never about productivity and wages.

Thats why interest rates have to crumble as we enter a recession, I don't see that policy as a success so far. We need that 280 billion on deposit to earn income or those depositors stop spending and go to ground. We will end up with in a deflationary spiral as people put off spending, they know things will be cheaper next month, year, decade.

I don't see us returning to growth for a very long time.

NZ could copy what the UK did in the 1930s (and arguably what NZ did too). Namely using fiscal and monetary policy to build itself out of trouble.

There is a great article here by Professor Craft about this. https://voxeu.org/article/escaping-liquidity-traps-lessons-uk-s-1930s-e…

For this policy to be effective;

1. New build housing supply needs to be able to ramp up in response stimulus i.e elastic supply is needed.

2. House prices (or rents) per m2 needs to equal the real competitive marginal cost of construction so that housing is affordable to FHB and renters.

3. These homes need to be locations where affordable transport options can be provided for residents to access productive employment in a timely manner.

So various housing and infrastructure reforms, such as, creating a Housing and Urban Development Authority, by modifying the RMA, by addressing infrastructure deficits and infrastructure financing, by bring competition into the building supplies market etc.

Brendon, I've got an awful feeling our problems are bigger than that. One thing we have had is monetary stimulus over the last few years, you can see it in the asset prices. We have borrowed off the future and it just doesn't look bright enough, we ate tomorrows lunch, look at Japanese property prices.

The bond market is saying no growth for the next ten years. Kiwifruit orchards are selling for 1 mill a hectare, apple orchards are going in at 350k a hectare to develop, yet they tell us they cannot afford a $2 an hour pay increase for seasonal labour.

Maybe you are right about global growth prospects Andrew and PDK. The global economy since the GFC has not been the same. Certainly the high price of horticultural land is ridiculous given the industry can't support paying workers a liveable wage.

The subsidising of housing construction would not just have a productivity rationale it would also address inequality. There is huge demand for good quality affordable housing in New Zealand. Our public housing waitlist has cracked 12,000, even as Government vastly exceeds its building target and even though the government is building more houses than any government in the last 20 years. https://www.stuff.co.nz/national/politics/114700141/public-housing-wait…

There would also be an environmental rationale for higher quality housing too. This was addressed in Parliament yesterday with a question from James Shaw to the Minister of Urban Development that discussed how a better urban form could reduces greenhouse gas emissions and respond effectively to climate change.

https://vimeo.com/351315434

On point AJ

What is causing this problem, how can you pay 1 million a hectare for a Kiwifruit orchard and not afford a $2 an hour wage increase for pickers who are there for a month? this is for unskilled workers, those who smoke a packet of fags a day and live in rented house with a car on finance

.

If we can figure this out then I think we will be getting closer to the heart of the issue, ie why are these asset prices so high, why don't we tax assets to discourage speculation in housing? Why don't we encourage investment in productive assets and keep houses and non performing assets as affordable as possible? Why have we allowed the finance sector to financialise the homes we live in? Why has the non tradable sector(councils etc) been allowed cost increases and regulation that have suppressed development in the economy?

I've come to the conclusion there's four answers to all your questions and they have their roots in our near neighbor. It's not so much their direct fault as simply the culture that they work by. The RBNZ seems to agree to the extent that they are heading down a track that would see them reined in a bit.

The DGMs on here here perhaps aren't so much about Doom and gloom but simply can not see the emporers clothes.

And the income is all based on growth in China.

@Andrewj..'Financialise the home'...Love that phrase. May lead to economic bankruptcy down the line ?

It is akin to sexualising kids. Society has become morally bankrupt.

"Both Japan and Europe currently have negative central bank rates, and both have also struggled to generate a recovery in economic growth"

The

Could it be that more and more countries are arriving at the ceiling? They didn't teach you this in economics, Brad - nor did the 'brilliant' Mr Hickey choose to join the dots - but we are up against the physical limits now. Nothing you ecomnomics types do, will produce 'growth'- t'ís over. Spend an hour watching this:

https://www.youtube.com/watch?v=HMmChiLZZHg

The human race is up against it now - despite the avoidance aptly demonstrated by some commentators. We need to focus on new goals - and 'making money from endless growth' isn't one of them.

... an hour ! ... we can't do that ... dontcha know we're living under a climate change emergency .. no time to spare for your frivolities . .

Must make a list : baked beans , tin foil hats , high powered rifle plus bullets ... it's been declared folks. .... Climate Change Emergency across NZ ... tea bags , pate fois grois ... pinot noir... gummi boots . ..

Perfect targeted timely and temporary fiscal stimulus is a state job guarantee at the minimum wage. Mop up all the underutilized and underemployed and give them decent secure jobs that sustain demand and put a floor under wages and conditions in the private sector. Don't stimulate inflating sectors. Spend at the bottom not the top by giving those who want to work but can't get decent employment a job. These are the people who will spend.Your job guarantee wage becomes your basic price anchor. When things improve people move away from jg and back into private sector. Stop using underemployment to discipline inflation. The stagnant economy is a story about poor demand and labour underutilisation. Uber eats is not the lifestlye that sustains family formation etc. Stimulus doesn't have to be hard hat projects. It needs to get money where the mpc is high. We conserve surplus commodities but we nonchalantly abandon surplus labour.

Excellent piece, one of the best for a while.

And yes, fiscal stimulus desperately needed. A mass state-led house build program would provide that....

It would kill two birds (a sagging economy, lack of affordable housing) with one stone

Indeed and if they adopted a passive hause standard for these homes the resultant education in the building and construction industry would have a significant benefit for the future of all new houses in NZ in years to come.

nice idea, real legacy building stuff

Why don't they do it???????

We have a serious problem and no one is pointing out that the Emperor has not clothes .

We have a problem with DELFATION .............. and there is no easy way around the problem

The cost of money is not the investment issue for businesses. A whole lot of of other constraints are causing businesses to be reluctant to borrow. Is our Reserve Bank Governor incapable of seeing how other economies have progressed, with low to zero to negative interest rates, or is he under the influence of the usual suspects who benefit from such policies?

Businesses invest when demand exceeds current capacity. Interest rates are less important. With no sales increases no one invests. Our economy has a demand problem linked to high household debt and stagnant incomes. This is not helped by governments running stupid surpluses instead of sensibly spending to fill the demand gap.

I see the Australian government recently tried to sneak through a bill to ban transactions over 10K. Is that a step towards a cashless society where nobody can escape negative interest rates. Meanwhile in NZ all of a sudden we have a deposit guarantee scheme being talked about. It all seems bleak. A friend was asking me what she should do with her money that's come off a term deposit, and I suggested that she bring it to Germany. Whatever paltry interest you get in NZ might get eaten up by currency depreciation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.