The Reserve Bank expects reintroduction of high loan to value ratio (LVR) lending limits from March next year will trim about 1-2 percentage points off house price inflation.

And the central bank, in consultation documents for the reintroduction of LVRs, says it's expecting a 'temporary, small negative effect' on economic activity.

"We consider a reasonable estimate of the impact on house prices of reinstating LVR restrictions on 1 March 2021 would be a reduction in house prices of 1-2 percentage points, relative to a counterfactual in which the LVR restrictions remained off," the bank says.

"However, given housing markets can suffer from ‘irrational exuberance’, LVR restrictions should help to lean against a possible further acceleration."

It goes on to say that if the current rate of house price inflation continues, "we consider this is likely to increase the risk of a future sharp correction in house prices".

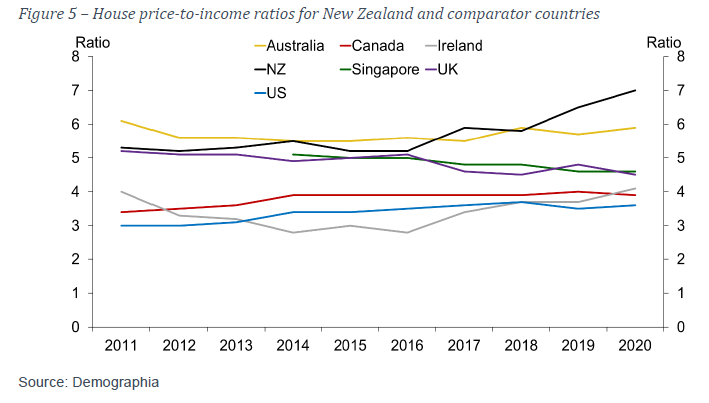

"This is of particular concern given the ongoing uncertainty over the economic outlook resulting from Covid-19, and the fact housing valuations in New Zealand are already elevated."

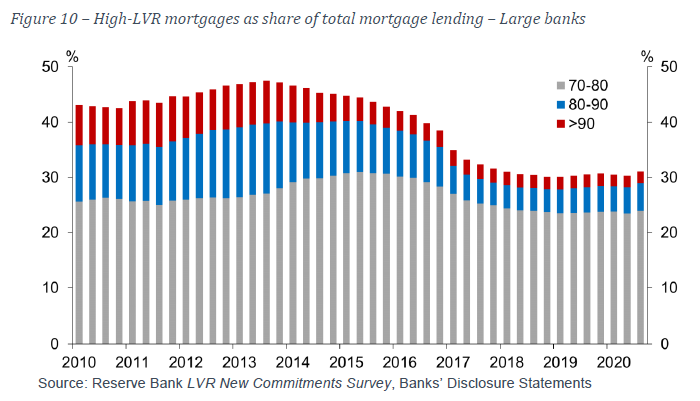

The RBNZ noted that since it removed the LVR restrictions, it had seen "some divergence between banks" with respect to high-LVR lending.

"Some banks have remained broadly within the previous LVR speed limits, while others have increased their high-LVR lending shares," the RBNZ said.

"Given the dynamics of competition for market share in the mortgage market, it is possible that the banks which have taken a conservative approach to date would face increasing commercial pressure to follow other banks’ policies, in the absence of LVR restrictions."

"...We are concerned at the emerging trend of rapid house price inflation combined with growth in high-LVR lending in an uncertain economic environment. While stocks of high-LVR lending are low by historic standards, we consider that if current trends remain unchecked, they could lead to the emergence of financial stability risks in the event of a correction to the housing market."

As stated above, the RBNZ's looking to bring the LVRs back in from March 1. It launched the public consultation process on Tuesday (December 8) and this will run till January 22, 2021, with a final decision to be made by the first half of February.

In effect this consultation by the RBNZ is merely rubber-stamping a decision already taken in principle. And most banks are already implementing the LVR restrictions as of now.

For the benefit of any doubt, the RBNZ's planning to bring the LVRs back as they were when it lifted them on May 1 this year.

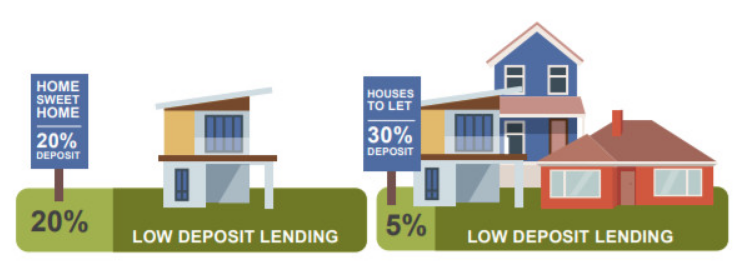

That is, banks will be limited (the 'speed limit') to just 20% of their new lending on mortgages where the LVR is over 80%, while for investors the 'speed limit' is just 5% on LVRs over 70%.

The RBNZ says reinstating LVR restrictions at these levels will mean that stocks of high-LVR lending to investors will "continue on their previous downward trajectory", while stocks of high-LVR lending to owner-occupiers will remain stable.

"...However, we will continue to monitor high-LVR lending and other indicators of risks to financial stability...

"...We may adjust the calibration of the LVR restrictions in future (as we have done in the past), as and when necessary to manage these risks."

In terms of the effect on the economy, the RBNZ says its research has found that, on average, the "marginal propensity" to consume out-of-housing wealth amounts to 3 cents of additional consumption spending for each dollar’s increase in housing wealth.

"In the short term, to the extent LVR limits are effective in moderating house price inflation, they can be expected to reduce consumption and residential investment by comparison with a counterfactual in which the limits remain off.

"However, over the longer term, if LVR restrictions are effective in reducing the magnitude of a potential house price correction, this would support consumption in a downturn and thereby economic growth and employment.

"In either case, while the economic impacts of reinstating the LVR restrictions on 1 March 2021 are likely to be relatively minor, we consider the overall economic impact will be positive over the long run. We expect a temporary, small negative effect on economic activity, however the benefits to financial stability and long-term economic outcomes outweigh this temporary effect."

At the time the RBNZ removed the LVRs earlier this year, it said this would be for 12 months at least.

"We acknowledge our current proposal to reinstate the restrictions on 1 March 2021 is not aligned with this earlier commitment, and hence could be seen as undermining regulatory certainty for the industry and wider stakeholders," the bank says.

"This is not a decision we take lightly. However, recent developments with respect to house price inflation and higher-risk lending are opposite to what was forecast (by both the Reserve Bank and others) at the time the LVR restrictions were removed. Under these unusual conditions, we consider it justifiable to revise our position. Although bringing the date forward by two months is a relatively short period of time."

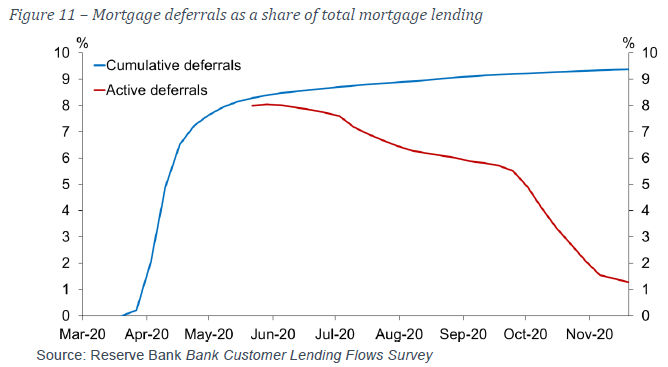

The RBNZ also noted that one reason it removed the LVR restrictionsl was to ensure they did not create an obstacle to the mortgage deferral scheme, introduced in March, originally for six months but extended to 12 months later.

"Our discussions with banks indicate most borrowers who were on mortgage deferrals have resumed payments (on either the original or a restructured schedule), with only a small proportion requiring more support. Therefore, we do not anticipate any adverse impacts on the mortgage deferral scheme from reinstating LVR restrictions earlier than we announced previously."

The RBNZ notes that other macro-prudential tools are available to manage financial stability risks associated with the housing market and again makes reference to the possibility at some point of adding a debt-to-income measure into its macro-prudential toolkit. It tried to have this added before the 2017 election but was knocked back by the National-led government.

"...We have previously consulted on introducing debt serviceability restrictions, such as debt-to-income (DTI) limits, on new mortgage lending.

"Although we consider restrictions on high-DTI lending could complement the current LVR policy, this tool has not yet been tested in the New Zealand context and is not currently part of the Reserve Bank’s Memorandum of Understanding (MoU) with the Minister of Finance. We are not proposing to implement DTI restrictions at this time, but intend to undertake further work on this option following our decision on reinstating the LVR restrictions."

50 Comments

Speculators overleveraging for existing property is bad for the economy. Literally stack a building full of economists and they just pump out high-school theory. Just a tiny bit of critical thought or common sense and we're sorted. Unlikely we will get it though.

Bad move. This should be reintroduced with immediate effect. Otherwise it will generate a call effect in the months until then which is going to make things even worse in the meantime. I refuse to think they are idiots but the other option would be that they are doing this willingly, knowing that will harm households even more.

Has there been any justification as to why 1/3/21?

All of the main banks are already implementing the new rules for investors, the only place to get an over 70% loan on an investment property is via second tier lenders and even they are being cautious. I am a mortgage broker

Banks are not applying any homogeneous restrictions to FHB though, the call effect I am talking about will apply nonetheless and banks are free to change their minds at any time anyway since they can just do it until the official restrictions take place.

This can't be true, Jacinda said we should all expect a small increase each year. I'll back the PM on this one...hard to stop a runaway train.

LVRs aren't the problem, its the lack of supply.

We need higher density living, not the urban sprawl that keeps on occurring.

I don't agree - property ownership rates are continually declining across NZ. Everyone else is renting.. Granted people want to rent for a range of reasons however can guarantee most people would rather be paying their own mortgage. Continual encouragement of rental investment via Government policy and inaction is a large driver.

https://www.nzherald.co.nz/business/property-prices-home-ownership-in-n…

LVRs aren't the problem, its interest only loans.

Too much demand =lack of supply. Why do 95%+ comments go with lack of supply with no mention of demand? Demand side is faster and easier to address.

Yip imagine an immediate ban on investors buying existing dwellings. How much of the housing stock are they buying at present? That would be a massive amount of demand, gone! Boomfa. Houses will still be built, supply would still increase....seems to me that its the obvious answer but just imagine the bitching (from darklords)

Landlords are an important part of the housing solution. Not everyone wants to own. They get a hard time for supplying a product that people want.

New Zealand must have been a hellhole back in the 90s with 74% of houses being selfishly owned by the occupier, depriving people of the opportunity to rent.

Quote of the month! Brilliant...

Yeah nah I'm over that narrative because I think its bull shit. Investors are using equity in other properties to outbid FHBs, pushing prices up, then taking rent of other people and claiming accommodation supplements paid by the tax payer. Its a rort and what you say is a false narrative.

It's a stupid argument, unless landlords are picking up properties that FHBs could afford, but are choosing not to bid for, at rock-bottom prices.

Which is not, you may have noticed, what is happening.

They are when they are supplying a service to those who want to rent. But the current situation is landlords are pushing potential homeowners out of the market. So right now, collectively, landlords are not providing an essential service, they are helping to deprive a generation the opportunity to own their own homes.

The “ban landlords from buying existing properties” comment shows how complicated the real situation is.

It may sound good, but if you did this slowly the rental properties would be pushed out to the suburbs and the central older properties would no longer be available to young renters whose needs much better suit these. Housing unfortunately is very complicated

It is lack of supply, but that is partly because there are so many houses that are left empty, ad we keep pumping people ito NZ, when we don't even house enough available houses for people already in NZ. So why are they allowing more people in with out building the houses and infrastructure first?

Also because of uncertainty, people aren't selling at the moment. Listing are down by more than a half in my area. Agents are bringing potential vendors chocolates to try and get people to list and sweeten the deal.

Problem is, you can never have enough supply of a government subsidised and protected investment. Supply of accommodation is another issue.

So, acc to Mr Orr, the wealth effect on spending of $1 increase in house values, is 3% on propensity to consume

Propensity to consume NOT used when speaking of inequality he is aggravating of course.

What about a researched figure for impact on propensity to consume fo the bottom 50% whose rents are rising at ridiculous rates over and above wages then? We are not given that.

Apart from banning evictions, what did Labour coalition gov do for renters during the temporary recession of 2020? Any deferment of their rent? NO.

Another piece of cherry picking or nit-picking for all my fans:

Sales and prices are cyclical (you remember the cycle don't you? it is the up and down thing that things do)

Well total sales in Auckland over 4 year cycle 2008-12 were 128,626

In last 4 years? 130,655

2012-16: 169,130

Source: REINZ

Spectacular increase.

Increase 2019 to 2020 was 10%

But of course in July-Oct it was 48%

Mr Orr's not stoked demand of course.

What he did was un-block the dam of demand for the period of flat sales for period 2016-19.

If you are determined to judge a market solely by a 5m block of sales, the cycle is what you omit.

Last 12m sales to end of Oct were 34,335.

That is 10% higher than 2019 but 28% LOWER than last peak which was 2014-15 (47,816)

In terms of the effect on the economy, the RBNZ says its research has found that, on average, the "marginal propensity" to consume out-of-housing wealth amounts to 3 cents of additional consumption spending for each dollar’s increase in housing wealth.

Hmmmmmm - What planet are these guys on.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1…

Furthermore: http://www.omo.co.nz/Discounted-cash-flows.JPG

{kind=link}

I would like to see their research Audaxes. I will ask them.

Great! House price inflation to drop to 22% p.a. That'll help!!!

Yeah and about time too! Was a bad move to remove LVR's in the first place.

Jacinda says all home owners (and herself) would like a small increase in house values (meaning prices) pa.

Except for small little matter of her refusing to countenance DOING anything to achieve that, or any other form of economic control that politicians are forbidden to enter into by the straitjacket OECD countries adopted in the 1980s of New Public Management and gutting the State whilst subsidising private sector contracting and endless bureaucratic delays from RMA. In UK in 1950 - 1965 they produced 300,000 houses pa. That equates to roughly 23,000 for NZ size population, pa.

NZ chronic shortage of housing is due to anti-State prejudice from 1984 - 2017 (National and Labour) plus increasing pop by 1.5m in the meantime. Utter absence of? Planning (nasty Socialist thing)

Yes, we're just not having the right discussion here. These house prices increases are not free money for homeowners and investors. We don't create new wealth in this, we are only shifting it from younger Kiwi workers and savers to older Kiwi asset owners.

Is that a fair and moral thing to be doing? It's an important discussion we need to be having, and we need to be openly acknowledging where this wealth we give to asset holders is coming from.

Jacinda has spoken, small house price rises are what we want, so, why not have the reserve bank target house price inflation, say 1-3%, favouring 2%. This would bring it's target inline with the tools it has to use. Expecting the reserve bank to affect the CPI especially in a positive manner is unrealistic, as they don't have a tool kit for this.

That isn't sustainable....

Average house price = $750,000. 2% increase = $15,000 increase p/a

Average household income (after tax) = $80,000. 2% increase = $1,600 p/a

(https://www.stats.govt.nz/information-releases/household-income-and-hou…)

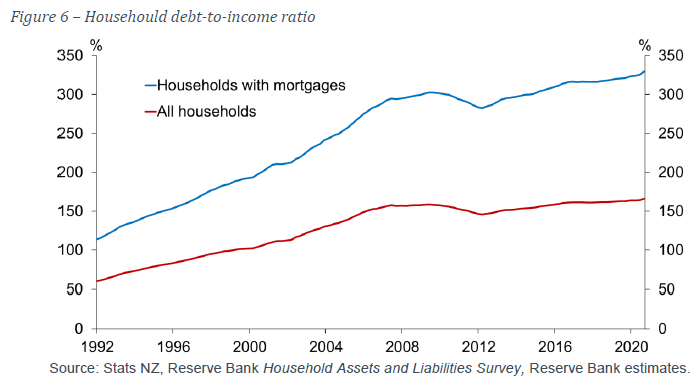

A compounding increase in house prices compared to household income isn't sustainable, even if house prices rise only by CPI measured inflation. At some point the debt can't be serviced to allow houses that are 10x average household income to increase at the same rate. 'At the end of the day' its household income that pays mortgages and its mortgages (debt) that determines prices. Eventually that debt load becomes too big and it can't grow any further because there is insufficient income to service it.

You are correct, none of this is sustainable!

The problem is we seem to be bound to this course, mostly because the majority don't want to miss out on the party.

I fear this just has to play out to the ugly end.

Agree - the latest round of QE is probably just going to make things worse long term, but it means we can avoid 'reality' for just a bit longer.

Question will become, when do younger generations come out and say 'fuck it, I'm done with this system as its completely rigged against me'. I'm moving overseas, or I'm peacefully or non-peacefully going to change the rules of this system.

QE and FLP are just subsidies for the housing market, and a desperate attempt to punt the can down the road.

Young kiwis were never particularly engaged politically, my own young folk are just dispirited, to them the kiwi dream is just a living nightmare.

And as for changing the rules, I don't see that happening before a system failure, after that then maybe there will be apatite for change.

A big problem is, once people have bought into the housing market, monetarily or even just psychologically, they become committed to it's perpetuation.

It's like when people can see retirement age coming up, they become committed to perpetuating the pension system.

Yip it looks, smells and behaves like a ponzi to me. Once inside it, people then become an advocate for it, knowing it needs more entrants to sustain itself, and the more that join after you, the better it becomes for you financially.

unless a sustained bout of inflation is allowed to occur ; which is the unspoken but obvious plan.

What happens to interest rates during levels of high inflation?

Aparantly wages will rise faster than interest rates (is the story I'm told by property investors) so that won't be an issue either. But I just don't see that because in the shoes of company CFO - debt obligations to pay, interest costs rise, increased revenues with increased price level, but nothing to generate excess income to increase staff wages at or higher than CPI.

Don't see how inflation helps with this amount of debt in the system.

Something doesn't add up here, do they count retirement villages as home ownership, or a tenancy?

https://www.msn.com/en-nz/money/homeandproperty/homeownership-rates-low…

Early November- Me frantically calling RE agents and getting very slow responses on listed properties on Trademe

Early December- RE agents calling me and asking me if I’d like to put a conditional offer on XYZ houses as they were passed in at auction. RE agents calling about new listings coming on to the market

I can already see the market slowing in Auckland. With the LVRs investors who cannot stump 30% in an Auckland market will find their 20% goes a lot further in the regions. Predicting Auckland to be flat now and regions especially Chch to continue growth

Will knock 1% or 2%...is he joking.

It is a drop in ocean.

It's perfect really. How can this claim ever be validated once the LVR comes back in?

What he means by economy is housing ponzi.

Being apologistic to all speculators for have been forced to introduced LVR though have given opportunity window to whip as much as possible for next few months

The USD is losing value ever day at some point the interest rates will have to go up in US to protect the USD from oblivion this will create chaos in most places around the world and hit NZ big time

So they think they have so much control that they know exactly how much the LVR will take off the house prices?

Well then, they must also know exactly what they would have to increase the LVR by to get a 0% increase in house prices.

But I call their bluff on that and say they are talking BS, otherwise, let's see them show their skill in halting these runaway prices.

And while they are doing it, here is some music for them to listen to, especially the words.

Hey, no fair, Dale. It was a free-range, organically fed chicken, the entrails of which the haruspices at RBNZ used for their divination/wild-ass guess/out-of-context quote carefully considered prediction....

To be fair to them Waymad, I think they have at least progressed to a dartboard over a few (too many) drinks. Everything looks better with beer goggles.

Logged in just to up-vote the haruspicy reference. Commendations on the devastatingly accurate simile for the dark art of hubristic central bank prognostication.

Where is the identification of the key players in this imbroglio? Media continually focus on the RBNZ and the Government. Yet it is the banks, in particular the Aussie subsidiaries, which have undertaken mass issuance of irresponsible loans. The RBNZ presaging of reintroduction of an LVR in March next year will cause the banks to start to adjust, but they should not have indulged in such an extreme surge in loans to specuvestors in the first place. The four banks in question all have corporate social responsibility policies, but these are shown to be empty promises. The agricultural sector has been starved of investment capital (the ANZ leading the charge to switch to residential some time ago) and the market has been flooded with capital available for the residential sector. Corporate social responsibility - what a joke.

Ouch C'mon, please don't. There's a reason why in 2013 it's being introduced by RBNZ, and it's clearly dented the housing supply, now after the removal even in very dire predictions? the supply suddenly flourishing. NZ should stop pressuring RBNZ to keep tinkering just for PR services, let them do their job. NZ really needs this negative OCR, tripling the current QE and LVR still off, we are away off from good balances, putting back LVR is clearly, just a soft hint warning due to populous bias. Remember even a quick short, small correction? is very dangerous to NZ 'economy'

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.