This content is sourced from the World Gold Council.

The volatility of numerous assets has shifted along with the performance of gold, which has recently rebounded to nearly flat on the year.

Given this shift, we consider it important to assess the current gold market conditions from a volatility and derivatives perspective, along with what technical charts are suggesting about where gold could move in the near- and long-term.

We believe that regardless of an investor’s gold sentiment, the following conditions are present and create an opportunity:

-

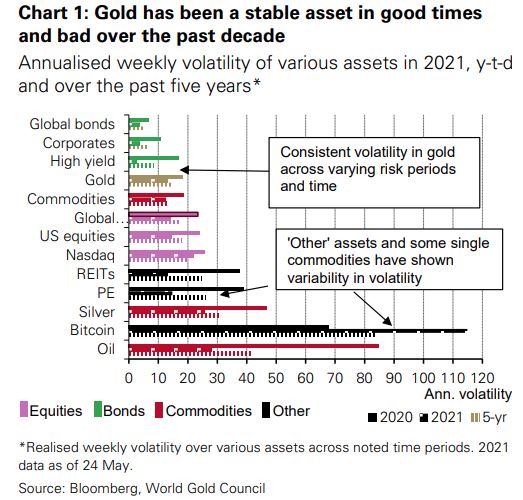

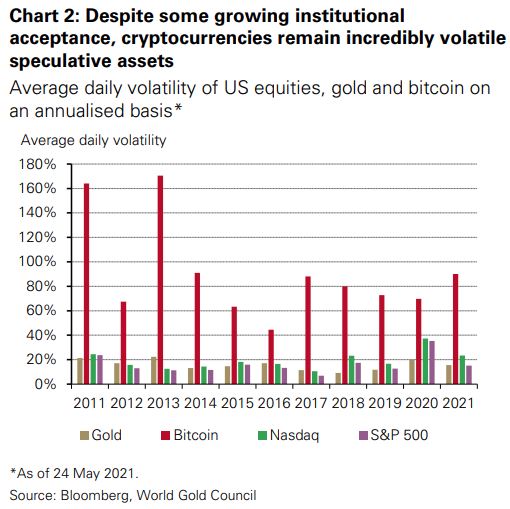

Gold has been one of the most stable assets from a volatility perspective – both, during the pandemic, and during the subsequent rebound, giving additional credence to its role as a portfolio diversifier.

-

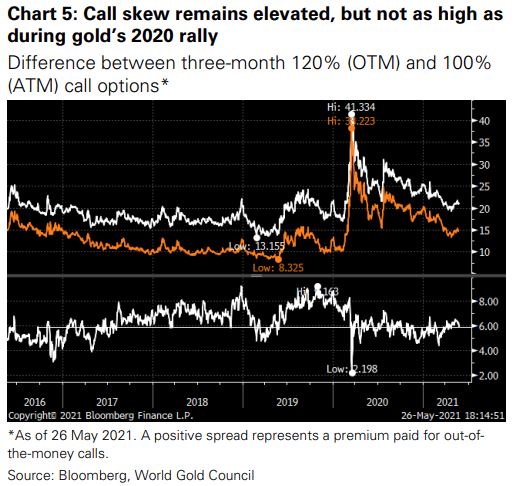

The at-the-money implied volatility of gold1 has fallen considerably with its recent muted realised volatility2, yet the ‘smile’ of the options strikes remains significant, with both out-of-the-money (OTM)3 calls and puts trading at higher premiums, versus at-the-money (ATM) options, suggesting investors anticipate extremes -- either very little or very significant gold price movement5.

-

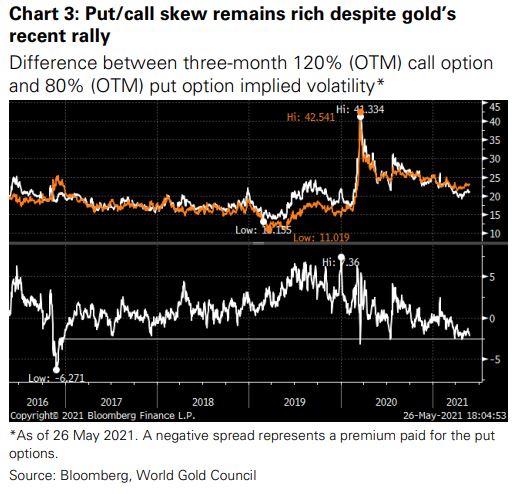

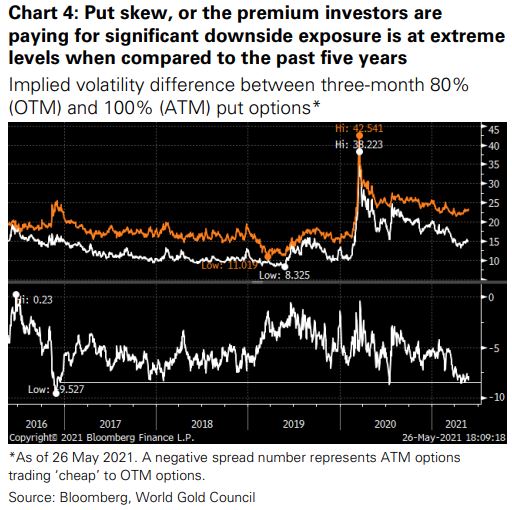

Put volatility, particularly OTM volatility, remains elevated, suggesting investors are still positioned for downside exposure in gold, despite the recent rally.

-

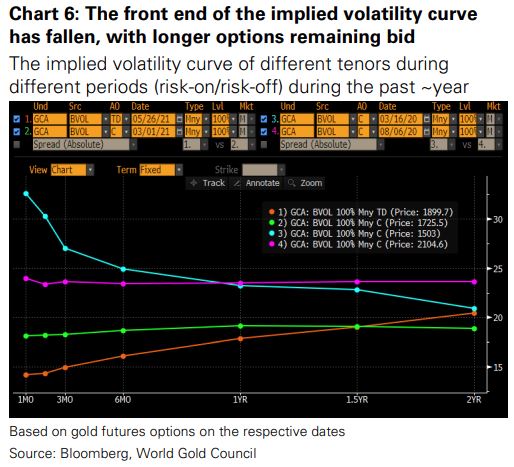

The term structure of gold options have steepened as shorter dated implied volatility has fallen.

-

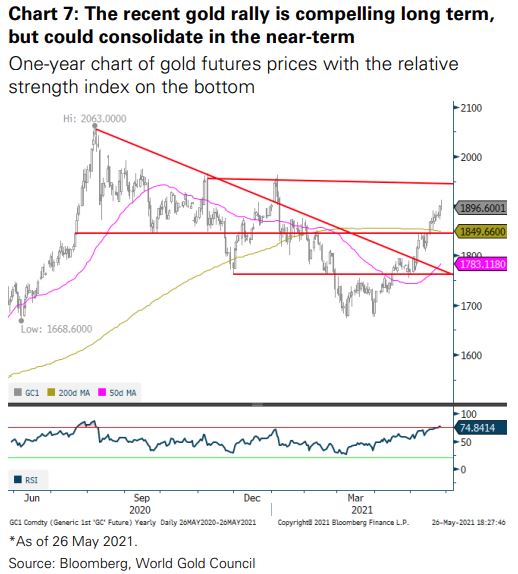

Gold had an important technical breakout recently, and looks poised to test all-time highs, but could be overbought in the short-run.

What positioning trends could we expect to see in the gold derivatives markets?

Where investors are bearish on gold, we could expect to see activity including:

-

Buying at-the-money puts: Implied volatility remains low for at-the-money (ATM)6 puts, and for an investor who believes gold could move meaningfully lower, we may see an outright put purchase that would provide maximum downside exposure.

-

Buying put spreads7: Put skew is rich8 from a historical perspective right now with out-of-the-money puts implying a higher volatility than at-the-money puts. We may see bearish investors buy put spreads with the aim of achieving capped downside exposure with less premium at risk.

Where investors are bullish on gold, we could expect to see activity including:

-

Selling puts outright or selling puts to finance buying calls: The rich put/call skew in gold options creates an opportunity for investors to use the premium from selling the relatively expensive puts which would bode well should gold stay range-bound, or to use it to buy upside calls at a lower cost.

-

Buying call spreads9: The rich call skew could lead to investors buying call spreads; this could provide ample capped exposure to the upside with less premium at risk.

-

Buying at the money calls: Implied volatility remains low ATM; those who believe gold could move meaningfully higher in the near-term could consider buying the calls outright.

1Implied volatility refers to how much the market believes the price of gold will move over a given period.

2Realised volatility is the measure of how much gold moves over a given period

3Out-of-the-money (OTM) options are those that are struck at a distance away from the current price of the underlying security. For instance, a 95% or 105% strike option is an option that is 5% below or above the current strike price.

4Three-month expiries are used as a general barometer to factor in the most widely traded options on average, along with options markets standards.

5The term structure of gold futures is the difference in implied volatility across different tenors (or expirations) of the options.

6At-the-money (ATM) options are those that are struck near the current price of the underlying security.

7Buying put spreads lowers the costs of gaining directional exposure to the price of a certain downside level.

8The terms “rich” or “cheap” are used to describe a set of options, volatility or assets that, when compared to a like set, are either more expensive or less expensive on a relative basis. These terms can also be used to highlight comparisons versus historical averages or periods.

9Buying call spreads gives the investor the ability to have long exposure to gold. The difference is that the upside exposure is capped.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

6 Comments

I'm going to throw a post in about GDX and see if I get any responses - but given our obsession with property its unlikely anyone will reply....

Anybody selling GDX at the moment or people expecting more upside in gold so holding? I jumped in back in 2018/2019 when getting a bit nervous about where markets were so have done well but not sure if to recognise some profit now or no. Any thoughts out there?

Where are you trading GDX? I used to trade options and shares with Halifax Investments (NZ) from 2016, but they went bust in 2018 (along with my account). I am interested in holding bullion as an insurance (Exter's Inverted Pyramid) but can't see how to trade with decent brokerage fees in NZ with the gold miner ETF's. Given up on option trading now from here.

Wow - I got a reply on a non-housing related post!

I use Jarden for an ASX holding and Hobson Wealth for a USD holding from NYSE.

I think Jarden might be opening up access to US and UK markets in the near future...but for now I use Hobson. Just have to make a reasonable investment though noting fee's for those international transactions. Fee's for Jardon on the ASX I think are $30 - so in theory if you wanted exposure to gold miners you can do so relatively cheaply from the ASX....but will cost you more if you want to hold via NYSE.

You say you're interested in holding bullion as insurance, but then ask about ETFs. A paper gold contract isn't insurance, it's an IOU. In a serious crisis, the value of that contract would be the same as your Halifax account.

What is a "halifax account" ?

Holding.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.