Just take a look at the swap rate charts at the bottom of this article. The recent surge is 'impressive' - positively if you earn interest, but frighteningly negative if you are a borrower.

The cause behind these shifts up are fundamental. War and premiums related to rising risks are the obvious recent triggers. But even more fundamental is the realisation by investors that the Trump mismanagement will be much more toxic for them that they originally envisaged.

And who are these investors? Actually, they are fund managers who essentially control pension and superannuation finds. These are huge globally, likely controlling about US$75 trillion in financial assets. When these trustees and managers lose faith in US government fiscal oversight, even a small shift can have an enormous influence on financial markets. And the shift doesn't have to start in the US - the non-US portion of these funds is US$25 tln, enough for global influence.

The point is, we can't avoid the implications. Swap markets require two parties and rates rise either because risk premiums to benchmark rise, or if people on the supply side of the transaction, such as fund managers, lose motivation to participate.

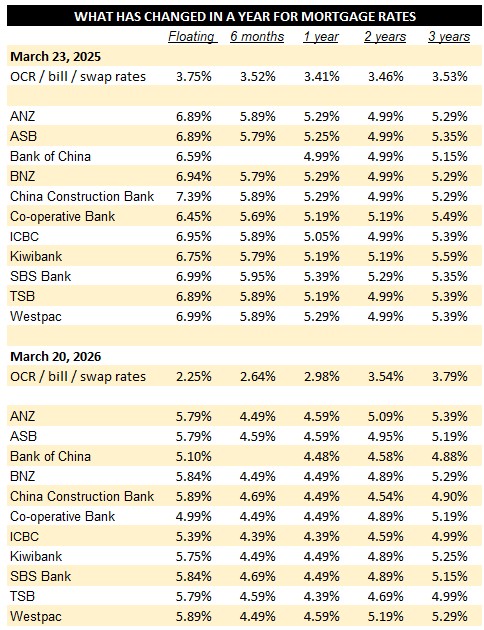

From a year ago, the Official Cash Rate might be 150 basis points (bps) lower, but the one year swap starts this week only 40 bps lower, while the two and three year swap rates are similar to year ago level now.

But the one year fixed mortgage rate is still averaging 80 bps lower, although the two year and three year fixed home loan rates are similar to year-ago levels.

Two things are revealed here. First is that the current one year fixed rates are likely to get an extra push up soon. And secondly, the two and three year rates are likely to move with swap rate movements from here.

And looking at the differences to year-ago benchmarks gives a similar view, although indicating that two and three year rates might find added pressures to be higher.

A lot depends on counterparty participation. It could become a supply issue. Then all bets are off regards fixed rates and borrowers will be left with having to shift shorter, and perhaps take floating rates. It's has happened before. But whatever happens, it opens an era of higher rates for borrowers. Unless of course regulators reprise the pandemic response of flooding the financial markets with cheap money via a put by the taxpayers. You are on your own judging this possibility's likelihood.

(Note, a swap rate is the fixed interest rate exchanged for a floating rate in an interest rate swap agreement, used by financial institutions to manage risk. It represents the "fixed" side of a swap contract, used to turn variable-rate loans into fixed-rate ones, reflecting market expectations for future interest rates).

This week has started with rate card rises for the Co-operative Bank and TSB. The Co-op Bank raised term deposit (TD) rates at the same time but TSB didn't.

We actually haven't had a period of sustained fixed rate rises since the first half of 2014 (pandemic recovery excepted).

We should note that 4%+ term deposit rates challenge residential housing investment net yields, and in many cases residential housing investment gross yields too. These investors are knocked at both ends - lower rents and higher borrowing costs, along with better no-work yield alternatives.

To compare mortgage rate offers in a way that includes the application and account fees costs, or break fee costs if you need to do that), and applying the impact of a cashback/legal fee reimbursement, or other incentive, you can use our home loan comparison calculator. You can find it here. Or, for convenience, we have added it to the bottom of this article.

Negotiate. How flexible banks may be will depend on the strength of your financials.

One other useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is here.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now.

Here is the snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at March 23, 2026 | % | % | % | % | % | % | % |

| ANZ | 4.49 | 4.59 +0.10 |

4.89 +0.20 |

5.09 +0.20 |

5.39 +0.20 |

6.09 +0.20 |

6.19 +0.20 |

| 4.59 | 4.59 | 4.75 | 4.95 | 5.19 | 5.55 | 5.69 | |

| 4.49 | 4.49 | 4.69 | 4.89 | 5.29 | 5.49 | 5.69 | |

| 4.49 | 4.49 | 4.89 | 5.25 | 5.69 | 5.79 | ||

| 4.49 | 4.59 | 4.85 | 5.19 | 5.29 | 5.39 | 5.59 | |

| Bank of China | 4.38 | 4.48 | 4.48 | 4.58 | 4.88 | 5.28 | 5.28 |

| China Construction Bank | 4.69 | 4.49 | 4.49 | 4.54 | 4.90 | 5.10 | 5.20 |

| Co-operative Bank | 4.59 +0.10 |

4.59 +0.10 |

4.89 +0.20 |

4.89 +0.26 |

5.39 +0.20 |

5.75 +0.20 |

5.89 +0.20 |

| ICBC | 4.39 | 4.39 | 4.49 | 4.59 | 4.99 | 5.09 | 5.19 |

| |

4.69 | 4.49 | 4.69 | 4.89 | 5.15 | 5.55 | 5.69 |

| |

4.59 | 4.39 | 4.99 +0.24 |

4.89 +0.20 |

5.29 +0.30 |

5.55 +0.36 |

5.69 +0.40 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

11 Comments

Up up and away.

7% mortgages by years end.

Kryptonite to the debt junkie monkeys.

I took a different view. I have a small mortgage of about $500 k left, I have sold a business with settlement at the beginning of April, which would repay all of the mortgage. I have decided NOT to repay said mortgage but to fix it for 1 year at 4.49%. My reasoning is that I believe that real price inflation is going to be at or higher than my mortgage rate, thus making my mortgage cost free, whilst I back myself to invest my money for a greater return than 4.49% pa.

Hard to know where to invest isn't it? Is there anything that isn't overvalued and wont disintegrate if we have stagflation?

You could argue gold, but even that seems very elevated.

I guess oil was a good investment a few months ago, and maybe now if it keeps increasing.

I'm doing the opposite to you, paying off debt ASAP, so the bank has no stake in my main asset. Although in my case it will still take a few years...

Gold may not perform that well now that interest rates are back on the rise.

Swap rates are on the rise IO, interest rates will surprise you because they will rise modestly only. Why? Governments are simply too indebted to be able to survive with high interest rates.

Also, what matters for Gold is not the interest rates per se, it's the REAL interest rates, meaning interest rates minus inflation. This is quickly approaching "0" (zero).

Well the evidence is currently showing the opposite. Gold is dropping in price in inverse correlation to swap rate (rises).

Investors selling gold to buy higher yielding bonds (which they can then sell again for a profit if interest rates do drop, then re-buy gold at a cheaper price).

You're making a fair point IO. But the reason why yields are dropping is because fewer people are buying bonds, (they are paying less for bonds), despite the wars, investors are not retreating to safe heaven assets like government bonds or Gold, instead the USD is rising, which I will admitis an enigma to me. Why is the USD rising when it seems that the world is slowly shifting away from it ?

There's no greater gamble than Gold IMO. Tread carefully.

Who needs the RBNZ to do anything. Swaps rates lead the way as interbanking trust heads downhill.

🍿

It will be a complete joke if Breman comes out this week and tries to talk wholesale rates down but then they keep going up regardless.

Interbank trust heading downhill? Jeez thats a bit cooked, thats the sorta language you use when banks stop lending to each other, not when swap rates move 30–40bps.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.