There are increasing signs of rising house price expectations on the back of the recent falls in mortgage rates.

The Reserve Bank's latest household inflation expectation survey has shown a sharp rise in the expectation of house price gains.

And economists are increasingly tweaking their house price expectations higher too.

Respondents to the RBNZ household inflation expectations survey are now picking 4% house price inflation over the next year - which is not so high. But just three months ago respondents in the same survey were picking only 2.8% house price inflation in a year.

In addition between surveys the number of respondents expecting house prices rises has jumped from under 50% to 64.7%, which is actually the highest proportion expecting house price rises since the June 2016 survey.

The latest survey results have particular relevance as they come just a week before the RBNZ releases its latest Financial Stability Report (on Wednesday, 27th). A key thing that will be watched for is whether the RBNZ will announce further loosening of its housing loan to value ratio restrictions.

Westpac economists have been saying for some time that house price inflation is set to move to about 7% over the next year and said this week they believe their forecast of 7% house price inflation "is well in train to come good, potentially earlier than we thought".

And economists at the largest bank, ANZ, have just upgraded their house price inflation expectation over the next year to 5.5%.

In the latest Property Focus publication the ANZ chief economist Sharon Zollner and senior economist Miles Workman say evidence that the housing market is tightening up on the back of lower mortgage rates has continued to accumulate.

"House price inflation has accelerated, up 3.3% y/y at the national level in October. And while regional divergence remains a key theme, most regions are displaying evidence of some tightening.

"House sales (up 8.2% m/m) are now picking up after a prolonged period of softness, and nationwide days to sell have dropped further below their historical average (to 37).

"We expect the recent decline in mortgage rates will continue to provide impetus to the housing market, with annual house price inflation peaking at 5.5% in 2020 – a small upgrade since the October Property Focus."

Zollner and Workman say they think "resurgence" in the housing market weakens the case for the RBNZ to loosen the LVRs next week.

"That said, policy, credit, and affordability headwinds are still expected to prevent the housing market from shooting to the moon once again, but that possibility can’t be completely ruled out."

159 Comments

Not awakening but has awakened.

Current market is like old time. Visit any open home and see the number of people visiting - may have to push your way through and auction room are active with houses going near around CV or much higher unlike last year where it was 10% to 15% below CV if not 20% and more below.

Not so much in Auckland, at least yet.

REINZ Auckland HPI prices down on the previous year in both October 2019 and 2018. Low sales volumes persisting. Values vs. RV quite the mixture as they have been over the last year.

Where are you talking about?

63 Melanesia Road sold yesterday, unconditional. RV $2,150,000. I’ll see if I can find out the price. It’s a period plaster house Your estimate? Edit: Price won’t be disclosed until it settles in the New Year. I’m picking $1,750,000 for the plaster.

Depends if it has a cavity but it's 1995 so that wasn't required at the time. If it has no cavity, then id agree with your price. With a cavity, id suppose more like $1,950,000.

It's already showing on homes.co.nz as sold for $1.95m - so you win.

Pretty good price considering 60A Melanesia got smoked - sold for $1.25m on a CV of $1.9m

63 is well presented, even if it is plaster and the REA tried his best to conceal it with crazy HDR photos.

Apparently treated framing but no cavity. The Plaster would still worry me. I'm also not a fan on backing onto public areas unless I use them myself. It sold so quickly I expect there was someone after that location and configuration.

Yeah I wouldn't touch plaster... especially for the best part of $2m!

Pity because the configuration did look nice with the pool etc.

It would be nice backing onto Madills Farm like that but I'd also think it would get loud being right next to the thoroughfare.

Are you sure it was 60A that sold for $1.25m? That's weatherboard.

Edit it was 2/62 Melanesia that sold for $1.25m with a RV $2.0m.

Thanks for the insight Stuart, have you seen any good bargains lately

I’ve been picking a resurgence come 2021/22. Second-guessing myself now as it is starting to look like the pick up may arrive a bit sooner.

Is your name Ashley?

No, but a guy called Ashley has been poaching my predictions for quite some time now.

Or, alternatively, you / Ashley may suffer from dissociative identity disorder?

We both pay attention to market cycles and learn from the past. That is all.

Just out of interest, what lesson(s) did you learn from the 2009 - 2011 Auckland property price cycle?

Did you learn these lessons firsthand from your own experience or from some other method (such as Ashley Church or from a study of historical growth rates of property prices over the past 40-50 years)?

That recessions don’t last as long as you think or feel they do, don’t sell when things are bad, that the property market is unlikely to fall as much as you’d imagine during a recession, that the cycle exists.

Vendors who WANT to sell vs those who HAVE to sell.

Properties with unrecognized potential are undervalued

The right one has a habit of turning up in different ways and places

Never stop looking

Never stop learning

Any resurgence would be artificial, pumped by an RBNZ terrified of house prices falling, like in Australia now too. It’ll only add to the big affordability problem we have. Current prices are not sustainable, let alone more increases.

If house prices collapse I’ll just claim that the collapse is “artificial” and it’ll be like I was right all along.

“Current prices are not sustainable”? Have a read of this - https://www.interest.co.nz/sites/default/files/hla/2019/september/Auckl…

Nobody wants a collapse. Bubbles can be prevented from bursting for a while with unsustainable measures, but nobody can stop a bubble bursting when it finally does. That’s why the FOMO stage is so dangerous. I see FOMO being spruiked here every time I drop by.

"There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved."

-- Ludwig von Mises

cmat,

Most of the general public are unaware of what a debt bubble is, how to recognise a potential debt bubble or the potential impact on their lives. They just don't know what they don't know.

Yep, here come the excuses for being wrong, DD. Then there's always the other one; "yep but prices will crash at some stage in the future"

Net immigration level is still high!

NZ's desirability to live is still high!

House price to income ratio is not high enough (from 2 to 6 to 10 to 20)!

Politicians are still very useless.

Available land in NZ remain unchanged.

So, price will keep going up around NZ if not in AKL.

"House price to income ratio is not high enough (from 2 to 6 to 10 to 20)!"

Are you a parody?

Woosh

"House price to income ratio is not high enough (from 2 to 6 to 10 to 20)!"

The lack of recognition of mathematical limits by the general public leads to a belief that trees can grow up into space.

Just to illustrate some mathematics here, what does a median house price to income ratio of 20.0x imply? Some people may not know what a house price to income ratio implies, and the mathematical absurdity involved.

Using a current median household income in Auckland of $94,564, this would mean a median house price in Auckland of $1,891,280 today.

1) using a LVR of 80% for an owner occupier buyer, this means that banks would need to be willing to lend 80% of the house price - this would be a mortgage of $1,513,024 (and equivalent of debt to income of 16.0x - go out and see if you can get a mortgage from a bank at that debt to income ratio level).

The principal and interest repayments on the mortgage over 30 years at a 3.0% interest rate (lower than current mortgage rates of 3.5%) would be $77,193 per annum. Note that the annual payment amount represents 82% of gross household income and 107% of after tax household income. Where is the money required to buy groceries, pay for electricity, and transportation costs as well as the costs of house ownership such as rates and insurance?

2) assuming banks are unwilling to lend a debt to income of 16.0x, let's assume the banks are willing to lend a maximum debt to income ratio of 7.0x to an owner occupier buyer. This is a mortgage of $661,948, and represents a LVR of 35%.

Using a 30 year P&I mortgage at 3.0%, this means annual payments of $33,772 - which represents 36% of gross household income and 47% of after tax income.

Now the issue is how many buyers on median household incomes can come up with the initial deposit of 65% of the purchase price to buy? - this is equivalent to $1,229,332. How many average households have this amount available today to purchase a house at a house price to income of 20.0x.

So if people believe that the median house price to income in Auckland can get to 20.0x, can they show me how they believe that will be financed in a free market, by the average owner occupier buyer earning a median household income? Sure, there might be a very few households in Auckland (a beneficiary of a wealthy relative, or winning lotto, etc), but not the average household in Auckland.

It just means that not everyone can buy a house, as is the case in many countries around the world.

NZ is often quoted as having "highest prices" or "near highest prices" in the world, but those articles only consider the developed world. Take a look at price to income ratios in developing countries and you will see that they are often much higher than here in NZ. I'm not saying that's something we should aspire to - just pointing out that it's entirely possible.

"Take a look at price to income ratios in developing countries and you will see that they are often much higher than here in NZ."

Can you please give some examples.

Unsurprisingly, reliable data is hard to come by for less developed countries. My comment is purely anecdotal.

For an informal summary, try:

https://www.numbeo.com/property-investment/rankings_by_country.jsp

Dig in to any of those countries with high price/income ratios and you will see that - in the cities at least - housing prices that are way out of whack with incomes.

" just pointing out that it's entirely possible."

1) What are the conditions that have led to those house price to income price levels in those developing countries?

2) What is the likelihood that those same conditions could manifest in Auckland? high, medium, low, zero

3) in the event that there is no or a very low likelihood of those essential conditions existing in Auckland, then are those comparisons with other countries even relevant in Auckland? i.e is the comparison with house price to income of these other countries akin to comparing apples with oranges?

CN, Auckland will go the way of London in the long term.

The average Auckland house transplanted into London will cost you over 20x median UK income. In the future this type of house in Auckland will likely be over 20x NZ income and terraced units will be the norm instead. You can get something like this for £1M in London - https://www.onthemarket.com/details/4477394/ . Not that different from your average Auckland house - 3 bedrooms with a yard, nice but not fancy. This is much more than 20 times average household income in the UK. This may be the average house in Auckland, but it is not the average house in the UK. The average house in the UK is a terraced unit.

Should we compare Gore incomes to Auckland house prices? Notice that CN was using Auckland incomes and Auckland House prices, an apples for apples comparison.

London incomes are much higher than the rest of the UK

http://assets.londonist.com/uploads/2016/02/average_monhtly_income.png

{kind=link}

What is the median or average household income in the greater London area? £30K-£40K. Still over 20X London household income for a typical Auckland house located there.

https://www.towerhamlets.gov.uk/Documents/Borough_statistics/Income_pov…

In London, a house that is considered "average" in Auckland (3 bed stand alone with a yard) is over 20x UK average household income (edit: and median London household income). In the future, I think the same will be the case in NZ. i.e. today's "average" house in Auckland (3 bed stand alone with a yard) will be over 20x NZ household income (edit: and Auckland household income), and by that point the typical house will be something much more like a unit/terrace.

"I think the same will be the case in NZ. i.e. today's "average" house in Auckland (3 bed stand alone with a yard) will be over 20x NZ household income, and by that point the typical house will be something much more like a unit/terrace."

Just to confirm my understanding of your point. So in future say 20 years

1) a 3BDRM house with a yard will only be affordable by the very wealthy

2) the household earning the median income in Auckland will only be able to buy terraced housing, units or apartments.

Yes, but much longer than 20 years away.

London is one of the top 5 most important cities in the world and has been for hundreds of years. Just like Auckland. That's how we can be sure Auckland is going that way and not, like, Cincinnati or something.

I'm talking about Auckland in many decades time, not today. London would've once had the price to income ratio for a stand alone 3 bed house that Auckland has today.

And at that point London will be x 40? x 80? Is there an upper limit on this?

Who knows. But back in the 1960s if anyone dared to predict that Auckland would have a price to income ratio of 9 they likely would've been met with responses as incredulous as your comments today.

Why don't you know? Doesn't the trend continue forever?

Don’t worry about it, we’ll be long dead before that possibility.

I probably got another good 50-60 years left. Or is that still not long enough?

I'm 32 and I intend on living to 130. Likely still not long enough, and I'm not going to speculate.

Why do we need to speculate? We can see the long term trend since records began, and we know they will continue to hold forever. It is simple arithmetic from those fundamental truths.

20 years ago, the median multiple in Auckland was about 4, and now it's about 9. Let's round it down to 8 and say that the median multiple doubles every 20 years.

Thus, in 20 years, we should be at x16. 20 years from then we will be at x32. 20 years again and we're at x64. This is when I will die at the age of 86 cos who wants to live forever. Plus my house should have doubled 6 times so I'll have $64,000,000, which is enough money to die with. If Auckland is at x64 then we can be sure that London will be at x128.

You then have another 40 years to go, so the median multiple should double twice more. Auckland will go to x128 and then again to x256. London should be at x512.

Don't be silly - how can they continue to "hold forever" when we know the sun will engulf the earth eventually? Alternatively, the communists might have taken over before the sun arrives and land could be worthless.

Should be about 5 billion years until the Sun engulfs the Earth. At the current rate of the rise of Communism, they'll take over probably 6 billion years after that.

In 5 billion years the house to income ratio should double 250 million times, so we should be at a ratio of 1.5x10^76.

Forever is much longer than 5 billion years.

Have you seen what's going on at NZ university campuses? It's scary how much traction Marxist ideas have been getting over the last 10 years.

"It's scary how much traction Marxist ideas have been getting over the last 10 years"

Likely to be driven by generational wealth inequality. Rising property valuations mean that many are unable to buy their first home.

When you get the top 1% holding a significant proportion of wealth, and at least 50% of the population are unable to have opportunity to have a decent quality of life in a capitalist system, then socialism certainly seems like a better alternative ...

Look at the civil unrest around the world...

It's driven by a combination of greed, stupidity and a desire to control the lives of others.

Marxist ideas were gaining traction in Universities since at least when my grandfather went. Which wasn't in New Zealand, but I doubt it'd be different. People usually grow out of it.

Bigger question is, do we want it to.

The entire reason my ancestors left the UK 8 generations ago was to get as far away as possible from this rubbish.

Seems the latest breed of UK migrant would rather transport Blighty here, with all its issues, at the expense of the Kiwi lifestyle/childhood.

What have our kids got to look forward to? Visiting the allotment in Kumeu?

Is that really what we want for Auckland?

I don't think that is what we want for Auckland. But what will be and what should be are two very different things, and it is prudent to make investment decisions based on the former.

And what's with trying to draw parallels with an average Auckland house transplanted to London anyway, it's a daft comparison. Of course if Auckland population grows the housing will become denser, so the average house will be smaller. Average house for that market is the valid comparison.

by CN | 20th Nov 19, 7:53pm

"House price to income ratio is not high enough (from 2 to 6 to 10 to 20)!"The lack of recognition of mathematical limits by the general public leads to a belief that trees can grow up into space.

My point is simply that a price to income ratio of 20 for today’s average Auckland house is possible and probable. It happened in London. At one point in the past the London house I linked above had a price to income ration of 9, and simple minded folk would’ve scoffed at anyone that suggested Auckland would one day be the same. But here we are at 9. I’m saying a stand alone house in Auckland will one day have a ratio of 20, which seems to have annoyed you lot no end.

Well, if you are going to compare what will at that point be a far above average house with average income of course you can hit 20x, there are probably some already. Like I said before, a bloody daft comparison.

I have very little respect for you.

How’s ya house hunt going btw?

Eh, I'm so worried about your opinion I can barely sleep..

(That was sarcasm, just spelling it out because you are so full of yourself you'd probably think I was serious)

House market maybe awakening a litttle bit. But it doesn't change the fact that New Zealand is still the second most vulnerable economies to a correction in house prices and has second highest house price-income ration in the world. I only speak with evidence:

https://www.bloomberg.com/news/articles/2019-07-12/canada-new-zealand-s…

Buble will burst eventually if you dont deal with it early. And those people who bought it at highest price will be suffering most from the impact. The Question is who would be those people? The people trust in property agent or bias media or people are willing to look into truth by themselves?

assumptions at the top of the article.. and REALITY right at the bottom..

"That said, policy, credit, and affordability headwinds are still expected to prevent the housing market from shooting to the moon once again, but that possibility can’t be completely ruled out."

LOL, that quote sounds like TTP. "X is unlikely to happen, but the possibility of X happening can't be ruled out!"

Fail to understand the sudden surge in buyers specially million dollar plus brackets who are not FHB in Auckland (how many kiwis FHB on NZ wages afford million dollar house).

Definitely not FHB as unable on kiwi wage to buy million dollar house.

Interest rates are low but stil.....Demand /Supply but still......

May be foreigners through corporate route.

Could understand price being stabilize at this stage but taking a U turn and moving up when ecenomy conditions have not changed except interest rate.

Rumour is that million dollar plus homes are selling in Sydney again due to capital flight from Hong Kong.

Is no such surge. Cite figs and price brackets

Zollner and Workman say they think "resurgence" in the housing market weakens the case for the RBNZ to loosen the LVRs next week.

Simple, lower the lvr' for FHB's to be in line with Kiwibuild, increase LVR's for investors and increase the interest rates for investors... (this was one of the options the rbnz had considered in the past)

Or just leave them alone?

If they truly believe that the global slow down is a risk then why pointlessly expose kids to higher leverage?

Agree, but KB is at 5%, so doesn't really make a difference apart from it being universal...

My assumption is that 90% of FHBs will be buying off KB, as there are not many brand new built in the affordable range..

Am I right in assuming that the lower LVR only apply to new builds?

"My assumption is that 90% of FHBs will be buying off KB,"

I would say that is hugely wrong.. simply looking at the number of kiwibuild sales (<1000 total?) vs the number of FHB purchases in the last couple of years and its quite obvious the FHBs are far more likely to buy an existing home than a new KB.

Edit: oh lol, I was way off.

According to the HUD figures, a total of 252 kiwibuild homes have been sold up to sept 2019. And there are 203 available for sale. almost as many unsold as sold.

for reference, 2257 first homes were purchased in august 2019.. so total kiwibuild sales to date are ~10% of a single month of FHB purchases.

But did they buy new builds?

What that got to do with anything? Kiwibuilds are new builds, but I doubt many other FHB purchases are new builds.

That was my initial point, might pay to read and comprehend before replying

"Zollner and Workman say they think "resurgence" in the housing market weakens the case for the RBNZ to loosen the LVRs next week.

Simple, lower the lvr' for FHB's to be in line with Kiwibuild, increase LVR's for investors and increase the interest rates for investors... (this was one of the options the rbnz had considered in the past)"

Not a mention of new builds in there....

"Am I right in assuming that the lower LVR only apply to new builds?"

Well, it wasn't your initial comment, and no, you assumed wrong..

So share your intelligence, what's right?

Start here, do your own homework... https://www.rbnz.govt.nz/education/at-a-glance-series/lvr-restrictions-…

Yet you did it for me, poor soul

No, I pointed you to the right section of the library.. you still need to read and comprehend the information, and search further. I doubt you actually know the answer.

I don't have to waste my time, when my pa, you, can do it for me

With this bullish outlook it would be a slack performance if the RBNZ loosened the LVR constraints.

The economists have no idea.

The DGM’s biggest enemy - the expert.

Most economists are bad at macro predictions, and not good investors. I don’t think those in charge of central banks even have much of a clue where near negative and negative interest rates are leading the world.

What about property market experts?

CoreLogic? Watch this: https://www.youtube.com/watch?v=SkAbqHzBhZI

I don’t live in Australia, do you? I live in an entirely seperate country called New Zealand.

Is this guy podcasting from his mum’s house?

Not index of banks. Check ownership

"Most economists are bad at macro predictions, and not good investors. "

That is the reason they stay at jobs that employ them and pay them for making macro predictions, rather than pursue becoming professional full time investors.

I know of a widely known and high media profile economist who thought he was so good, that he went out and started a hedge fund. Within 24 months he was back to being employed by a bank as an economist, and market commentator ...

Their models are overly simplistic.

I know many economists working in banks and investment funds (some are PhD's in a niche area of economics). Most look at macro economic statistics such as GDP, current account deficits, unemployment, productivity but miss the linkage with asset prices in free markets.

Was just reading an economist's report on US housing in 2006, and they came to the conclusion that houses prices were at justifiable levels.

They could be much better at drawing wider system linkages.

They also overplay gross data and trends at the expense of aggregate ones.

There are some exceptions. I was reading the other day how John Maynard Keynes proved to be an exceptional investor, beating to stock market by a wide margin consistently in a VERY difficult period in economic history. He kept it fairly quiet but his substantial fortune from investing was revealed after his death. (It was in a book called 100 Baggers - good book, worth a read).

Agree, and very few economists have called financial crises in the past, despite quite obvious signs.

Taleb is always worth referencing on these matters.

Heavily biased experts. Who are their paymasters? The banks, who, of course, are heavily invested in talking up the market.

Maybe Interest could ask the opinion of non-bank economists.

Annoying when they don’t tell you what you want to hear, ay? Must be biased.

No.

All I have said is they are biased. And have vested interest.

I listen to experts who are independent and have no vested interest.

So as I said maybe this website could get one of several good independent economists to provide their view.

These experts that you listen to, do they all tell you what you want to hear? Can you give me an example? Are any of them YouTubers with 10k subs streaming from their mum’s basement?

I have a double major in economics and I have my own view. It differs from the bank economists.

There are a few independent economists who are good in NZ. I don't know their views, they may be similar to the bank economists. But it would be good to hear from them as all we ever hear from are the bank loudmouths

Good on you. Watch out for confirmation bias though. If you are relying on yourself as the expert it’d be difficult to avoid telling yourself what you want to hear.

Yes agree.

That's why it would be nice to hear from some independent economists. Barrie, Eaquab, Reddell or Greenaway are good options.

Lol! Earlier Fristz said "the economists have no idea" so he is saying he has no idea hahaha

"Watch out for confirmation bias though."

That is why we all benefit from a high quality discussion of differing viewpoints. High quality and logical refutations and rebuttals lead to better outcomes.

Some people who are less capable of clarifying their own logic to support their viewpoint or in providing logical rebuttals to the opposite perspective unfortunately choose to resort to name calling, ad hominem comments, and misdirection of the conversation in order to feel heard.

"Watch out for confirmation bias though."

(Chuckle!) What do you think this article is providing....

(NB: You'll probably be well aware of my views - that mortgage rates are going to plunge; the OCR is going to 0% and LVR's are going to be enhanced - 95%?. All 'things' that are perceived to be 'good' for the market - but they aren't, and they won't be! All they signify is desperation on the part of those who 'control' our economy in an attempt to avoid a calamity. But as I just suggested - they won't)

Lol, so when it suits you, they are the experts, when it doesn't, you know better...wow

" ... economists have no idea."

The group of sages who know anything is becoming smaller and smaller and smaller

Let the Gooood Tiiiimes Rooooll, oll

Respondents to the RBNZ household inflation expectations survey are now picking 4% house price inflation over the next year - which is not so high. But just three months ago respondents in the same survey were picking only 2.8% house price inflation in a year.

In addition between surveys the number of respondents expecting house prices rises has jumped from under 50% to 64.7%, which is actually the highest proportion expecting house price rises since the June 2016 survey.

Wealth effect or wealth illusion?

The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

I don't really understand that at all. Just get a house and get as many financial assets as possible.

The quote confuses savings with assets (a 101 mistake), replace the word "saving" with "assets" and it will become clearer. Also it is unclear to me why lower rates for longer increase the liabilities. Yes lower for longer increases the value of an asset but why would it increase the liability (mortgage) on that asset?

Why can't the gov impose a rule to say

House price can't go up wit the current interest rate (probably applicable to kiwi build houses only). this prevent crazy market inflation.

If price still goes up, buyers will end up borrowing more money and in the long term, this could be worst for repayment.

It's not just NZ that's at an economic turning point:

For 30 years, the fortunate citizens of Australia, the lucky country, have enjoyed an unending wave of economic growth, powered and juiced along by resources, credit and the once-in-a-century property market. On the other hand, this has created a bipartisan political paralysis where governments are loathe to go anywhere near the sacred cow of house prices.....Australia is willing to subjugate all other interests to the inflation of its property market. It will do this even if it means forcing homebuyers to bid at auction against international criminals, drug dealers buying with powder-coated cash or terrorism financiers.

https://www.michaelwest.com.au/fatf-caves-as-australia-keeps-propping-u…

Interesting article thanks. Although the takeaway from it seemed to be that it's more of the same in Australia!

NZ got a callout for moving ahead of Australia with its AML efforts.

Jump on in the waters great. Prices will keep going up. This time is different.

Yep, that's what we were told the last time arround.

There are no new tricks, there is less wriggle room with rates, the people are not smarter.

There maybe another push higher bit logic says it is a stack of cards which is about to fall.

"Prices will keep going up. This time is different."

So which is it?

Prices will keep going up, as per usual

Or this time is different

Can't be both

Time scale missing as usual with you.

Since march 2017, prices (median) have fallen form $900k to $850k A FALL.

If you mean prices rise in long run, well yes, brilliant, what an insight.

Find me an instance of anyone this site ever unsarcastically claiming that prices never fall. Just one single example from any date is all I ask.

Obviously he is referring to long term trends, and the claim that this long term trend is all of a sudden about to change is a claim that “this time is different”.

Always amazes me how the doomie gloomies on this site accuse others of thinking that “this time is different”, when they are in fact the ones that think the housing market characteristics that have been evident since records began are all of a sudden about to change.

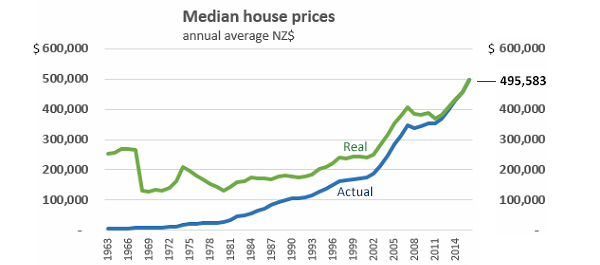

Since records began... if we forget about the records that existed before 1983 and records from anywhere else in the world.

No need to ignore records prior to 1983. https://www.interest.co.nz/sites/default/files/embedded_images/median-h…

{kind=link}

And New Zealand is not Ireland or Australia or China or Timbuktu.

But Auckland is London?

amirite?

[And looks like you ignored the line that is labelled "Real" in that graph... i.e. the line that actually matters]

By 'market' you mean 'speculative ponzi scheme of colluding interests' and by 'awakening' you mean 'renewing inflation based on the availability of more cheap credit'.

Call it as it is Goebbels

Seems a bit harsh. We shouldn't lose sight of the fact that this is a business web site that concerns itself with such things as the housing market.

Also if you can buy a property and cover the costs by renting it out it surely is not a "ponzi scheme".

V good effort mate

Market has changed in Auckland - Manukau area for sure as now asking / expectation for most houses be it unit,townhouse or independent house is more than CV.

Between starting of this year to September and now, market has gone up by at least 10% (Can low interest be the only reason - doubtful as something is at play for ecenomic conditions have not changed) if not more (earlier houses were going at a discount and any house going at a premium was rare but NOW most houses are going at premium and any house going at a discount is rare).

This is just the begining and if it continues (It should) next boom is on.

This sudden change in market surprises - if prices would stable (not fall) could understand but this jump in price is surprising at this stage.

Stuart this is more worrysome as ecenomy condition has not changed and if house price starts to rise rapidly only based on low interest (in absence of all other factor remaining the same) and if for any reason falls again and soon will be a disaster (earlier was soft landing but not this time, if it happens).

Also million dollar house is not supported by FHB so.........will have to wait for experts to analyze and explain (not demand/supply please)

It's surprising that the auction results that Interest.co.nz post don't seem to support this. So far, results seem pretty much along the lines of what happened this time last year.

Is this an attempt to talk the market up?

Price rises = lower sales. Means fewer home owners.

Plus increasing supply means LOWER prices. Otherwise cannot sensibly state that lack of supply raises prices.

Usually you state lower (fewer) sales leads to lower prices but above you say lower sales = price rises, which is it? (actually it's none fyi)

Then you say lower (fewer sales) means fewer home owners. That's non sensical, for each seller there is a buyer. If there're 2 sales today but only 1 sale tomorrow there's still the same number of home owners. What makes the difference is who the seller and buyer are (home owner or investor) NOT how many have sold

It would be nice if you could cite me accurately. You have in fact reversed the position of the variables in misquoting me, so eager are you to jump in.

I do not say fewer sales = lower prices. Why would I?

Lower sales does mean fewer home owners because 75% of what is being sold that is NEW is being sold to landlords to rent out.

Plus many sources confirm that owner occupation is falling and this has been case since 1992 and it is worse in Auckland due to stuff being too expensive.

Housing market cycle is NOT complete in its down phase. Forced selling to meet loan repayments not set in yet. This is for Autumn 2020. All this guff is mere speculation

Mikekirk29 hope you are correct but my brother who is looking for a house and am helping him, can feel the difference between September and now. This is firsthand experience and not as an expert theory or view.

Good decent free standing (built in 1960s/70s) with CV of High 900s to early million were asking and going for high 800s to early 900s but now similar houses expectation are in million and also being sold. Also when calling RE Agents now, are not shying away with asking/expectation which was not the case earlier - body language/confidence is back in them and also justify as are able to sell at that price. Even we initially thought that this is just marketing or trying to build artificial demand for price rise but when you attend open home (25 to 30 Families attending – earlier will be lucky to find 1 or 2 families) and them selling at premium price compare to earlier in the year than it cannot be a speculation.

Can check Howick, Pakuranga, Bucklandbeach area.

At the same time most of the houses coming to market now are those houses that have been purchased in 2016 or after - indicating that those investors/speculators are trying to use this opportunity to offload and if they are doing to sell with minimum loss or no loss no profit after holding for few years – send a signal that even they are nervous and not sure about the market trend, if this is sustainable or why would they sell now and not hold for more months after holding for few years and get the desired profit.

So is confusing for people like my brother who is a FHB and could see/feel that market is much strong that it was two months before and now with election even the government will promote (Openly or behind the door) for house price to rise to portray rock star economy and sc%$# FHB

You are correct basically now Labour Led government will do everyhthing that national government was doing to prove that NZ is still a Rock Star ecenomy.

So whom will you vote now ?

Any experts, now what will happen to Labour support support (Luckily for FHB that intially they bought FBB - fresh from victory otherwise would not even do it, if not done at that time like CG tax)

134 Union Road, Howick has an asking price of $995k (100k below CV).

49A Union Road, Howick has an asking price of $870k vs cv at $890k (this is the second time i've seen this property listed this year, perhaps the reason it isn't selling is that the buyer paid $830k in 2015 and was expecting more)

World recession will severely impact Auckland housing market in 2020 and no one has said much about this in media.

Prices can be identified by suburb or sub area or by Auckland median.

Everyone seems to have an anecdote at moment but I study the 12m running trend of sales and it is not improving and in last 4m to end of September, was worse than in 2018

Forced selling to meet loan repayments not set in yet.

Interest rates are low so percetage of default will be much lower, if it happns. For that to happen in this market scenarion, housing market has to crash.

No, sorry, forced selling by developers is crux. Revenues needed to meet debt inadequate means higher payments and then default. it is coming

Ha ha yes, yes and yes.. ANZ, JK visit to CCP no.1 - yee haa...flog it more, more & more. We can only watch from the side lines, what would the result be in the medium-longer term future of Aotearoa.

All fuelled by ultra-low mortgage rates. $700k at 3.5% a lot different to $700k at 5%. Feel-good factor of rising house prices vital to spending intentions, but it's a Ponzi scheme at heart propped up by cheap debt. Last in, worst hit. First-time buyers beware. As to immigration, isn't it fulled by students and temporary workers? They don't buy houses and there's a net loss of 'citizens' according to this website. Keep grounded everyone, the fundamentals just don't stack up.

The property market is only a Ponzi scheme if sales are to people who will not afford to repay the debt in future (as was the underlying cause of the GFC magnified by many folds due to these crappy debts being securitised and sold to investors in a chain of crap built on crap).

Do you have any information that indicates the NZ debtors are in serious risk of default in near term? that will be factual based argument informative for all, otherwise calling something Ponzi is not informative, Ponzi how?

That is not correct definition of a Ponzi scheme. Such a scheme is where the rise/gain is dependent on continuing stream of greater fools buying, to maintain constantly rising price. When buyers do not enter in ever increasing numbers, the pyramid collapses. Buyer numbers have been falling since 2013 and especially since 2016 and prices are flat as a pancake. Crucial question is whether this will lead to those developing property failing to get enough revenue to maintain payments on their debts. If not, then the Ponzi will implode as forced sales drive down prices and spiral ensues. That is what I expect as last leg of down cycle, in March 2020 and for rest of 2020/21. Decks will not be cleared til end of 2021, when I expect prices median in Auckland to bottom at $670k.

If price is heading up north, we have to thank Jacinda who did a good job promoting NZ to overseas buyers!

https://www.rnz.co.nz/news/national/403700/stephen-colbert-in-new-zeala…

I'll overlook the FBB for a second to address the basis of your comment - that it is foreign buyers to blame for price inflation. This may be part of the case, but from my own personal experience, it is just as likely that Kiwis (that's right, people born and bred here) and their obsession of property - as an asset for retirement, secondary income, or even a holiday house - are as much to blame by riding the wave of globalization and cashing in, disregarding the damage it does to society and the generations that will one day be taking them out for their once-a-day zimmer frame walk.

If I sound like a pissed off millennial, it's because I am. And there's a lot of us feeling the same way.

Hear, hear!

Wonderful to hear....since much of the NZ economy is artificially propped up by unsustainable house prices, while the global economy continues to weaken, it should be good for NZD rally as well. Keep buying those homes, and thanks for the gain. :)

Headline is "housing market awakening"

Then it is said this is due to expectation of price rises.

Price rises cause falls in sales.

it really would be nice if someone could define their terms as to what a good "market" is and how one might recognise it.

If people could afford houses in Auckland for instance, that might indicate a "good" or healthy market.

However, since sales are lower than in 2013 in Auckland, plainly not enough people can afford them, or they would be buying, esp as we have 6.5% more stock now.

It is not a healthy market.

Also, although sales increased in October 2019, compared to 2018, in some areas of Auckland, it was patchy and total sales fell below level of October 2018.

Sales growth in one month can be balanced by lower sales next month, YoY, so best indicator is 12m sales series to end of each month, showing the trend. This fell in Auckland, from May-Sept 2019, while it rose in that period in 2018.

Supply is increasing and people keep talking in next breath saying that prices will go up. This is a contradiction of laws of economics.

"Supply is increasing and people keep talking in next breath saying that prices will go up. This is a contradiction of laws of economics." - Not if demand is also increasing...

Sales in Christchurch, Nelson, Whangarei etc, all falling due to rises in prices.

What are the author's criteria for a "good" market and a "growing " market.

Or is this stuff purely for landlords?

It'd be interesting to know the "mean time since previous sale" for house sales, and compare that stat with a few years ago. Or better still, bucket the sales stats in to a few ranges, e.g. under 1 year, 1-2 years, 2-5 years, over 5 years.

I suspect there's a lot less short term profiteering and quick renovations now, and that that accounts for a big part of the drop in overall sales. If that's the case, then lower sales volumes doesn't really indicate a less healthy market or an imminent fall in prices.

RIP and Bust Van Winkel.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.