Mortgage borrowing surged in May as would-be buyers emerged from a month of lockdown in April. And the first home buyers were borrowing up large.

According to the Reserve Bank, total monthly new mortgage commitments were $4.318 billion in May, which was an increase of $1.569 billion (57.1%), compared with April 2020, but down 33.3% from May 2019 when $6.47 billion was advanced.

Apart from the emergence from lockdown, the other significant factor in May was it was the first month since late 2013 without any loan to value ratio (LVR) restrictions in place.

The Reserve Bank removed these for at least a year starting from May 1 this year.

And the first home buyers were quick to take advantage.

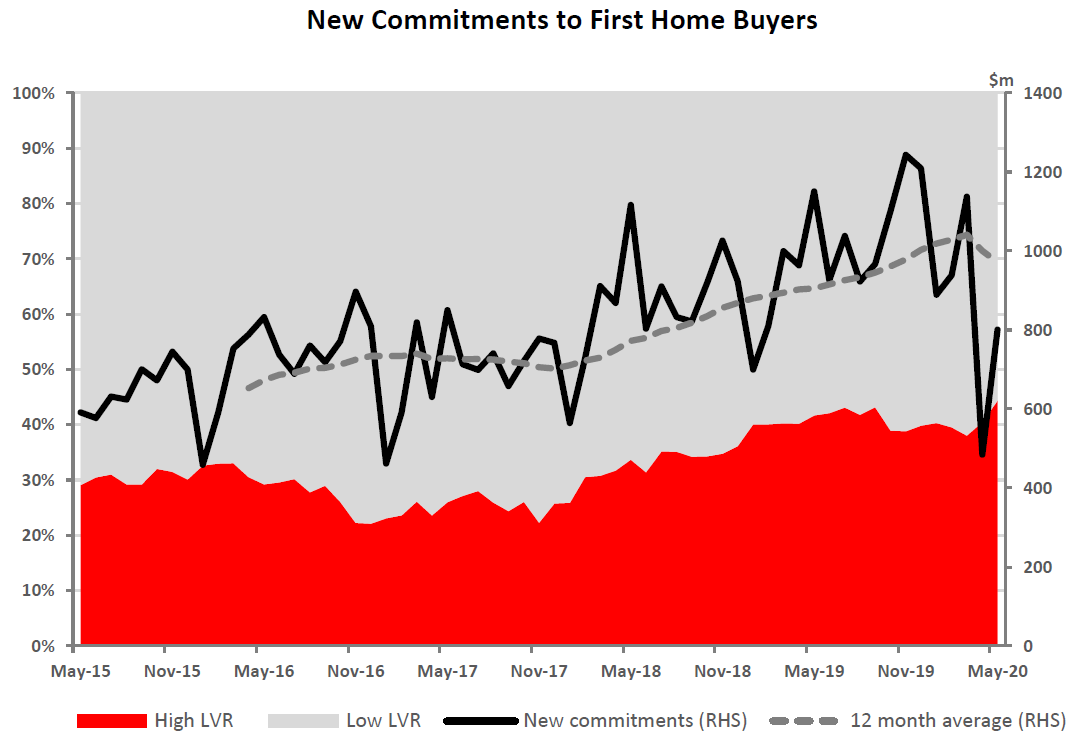

The FHBs were back in some force in the mortgage market, accounting for $801 million of the total advanced in May.

Of this, $445 million - some 55.5% of the total they borrowed - was for loans above 80% of the value of the properties they were buying. 'High' LVR loans in other words.

This is a much higher percentage of high LVR loans than the FHB grouping has been taking up in recent months, with the average percentage normally being around 40% on high LVRs.

In terms of the total amount of mortgage money - the $4.3 billion - advanced in May, the FHBs made up 18.5% of it. That was up from 17.6% in April.

That sort of ratio is more in line the share of the mortgage market the FHBs were claiming in the latter months of 2019 and into this year.

New Zealand was in Level 3 for the first half of May, meaning that real estate agents could show houses by appointment but there were no open homes. From May 14 we moved to the far less restrictive Level 2.

We went to Level 1 from June 9, so the month we are now in will be the first month since February that will have 'near-normal' conditions.

May was the first month without the loan to value ratio (LVR) restrictions, with the RBNZ having removed them from May 1 for at least a year.

The RBNZ has still provided some comparative information.

It says that in the month of May 14.2% of mortgages without investment property commitments involved were (after exemptions) at LVRs of over 80%.

This figure is up quite sharply on the 11.6% figure seen in April, the last month on which the LVRs applied.

In the graph above loans above 80% of the value of the property are tagged as "High LVR" loans will those below 80% are "Low LVR" loans.

75 Comments

TIL Surge == Dead cat bounce

Brave call putting your life savings on the housing market at the moment, doesn't take much for that 10% equity to disappear.

I agree, but real estate is like a drug to kiwis. Apparently we can't get enough of the rush that purchasing property gives us, even if the side effects are bad.

Might have been, but we just got OD'd.

Or they need places to live???

I rent but can understand first-home-buyers wanting to make a move. Especially if they have double incomes, no kids and are open to fixed term mortgages.

If you can find a suitable property and plan living in it long term, give it a go !! .. I guess ?? I believe house prices will decline, but owning [yes the bank really owns it] your own home is a social good.

Also 10% equity will not be every FHB's life savings. Conventional wisdom when buying a house would be to 'stretch yourself' - I disagree:

- Find a house sized and suitable to your needs

- Make sure payments are easily manageable

- Offer less - less is more

- Stand back from the house and ask, "is this house just plain ugly?"

I'll pick it.....200 next month

wow -- what a terribly misleading headline -- are you now like the herald and dependent on RE advertising to stay afloat ?

Desperate stuff !

It's not misleading, just phrased in a particular way to express action and drama. All it's really saying is "post lockdown, as you would expect, people returned to buying houses", but that doesn't sound nearly as exciting.

It's unlikely David chose the headline. That's someone else's job

int.co isnt exactly a big outfit. I bet he wrote the headline. If someone else has that job, then perhaps they need to downsize.

Headline : Monthly mortgage borrowing shot up 57% in May compared with the lockdown month of April - but the figure of $4.3 bln advanced was still down by about a third compared with the same month a year ago.

Is it not obvious that numbers will be uo from April (Lockdown month). Also more FHB than investor - does it not indicate that investors are shying away as not confident and FHB suffering from FOMO.

This is how you end up in the sh##! short term fix, long term misery

Wiseguy

Not a problem, your choice to just keep renting and paying off the landlord’s mortgage. Nobody is giving you stick for that.

Pay landlord's mortgage at <2% yield (gross) or pay 2.5%-3.0% interest to the Bank.

Tom-ay-toe, Tom-ah-toe.

If the landlord wants a braindead 'investment' then who am I to argue.

Cmat

News for you.

Your landlord (if you are renting) is not providing social housing for you. Although currently not great, your landlord will will have done the sums before buying and will be currently looking at a gross yield of at around 5% and a net yield after expenses but before mortgage (tax deductible interest) of around 4%. Don’t ever think that a landlord hasn’t invested not to profit from it (which is about profiting from you the tenant).

No wonder Foreign Buyer hates landlords and calls them “leeches” - sadly not understanding that rentals are called investment properties for a reason.

I have recently noticed a change of tone printer8. Complete frustration I guess?

Printer8. Some news for you.

Not all landlords are that great at the sums, especially when a positive outcome depends on some highly spurious projections.Most landlords in NZ in recent times have included expected capital growth in their sums, and when a black swan such as the one that sailed in earlier this year appears, the sums start to look a lot more like a bad bet than a hard calculation.

Sadly, when investment properties cease being investments (i.e. delivering returns) and instead become liabilities (costing more money to own than they yield), that tiny hole in the dam pretty soon becomes a torrent, smart landlords start to dump, and the market crumbles.

Shame for the FHBs who bought the hype, and the homes, highly leveraged and horribly stretched...and for the investors who don't get out in time. But yup, that's the game.

Shame more-so for those prospective fhb who were hoping to use their kiwisaver

Big Data

You are making a sweeping assumption here.

Firstly, the majority of landlords look at cash flow positive properties. When I was in the investors association it was always “if it isn’t cash flow positive don’t touch it - capital gain is simply an incalculable bonus (tax free) when one sells”.

It is not rocket science that majority of current landlords have owned their properties for some time and would have seen on paper (but naturally unrealised) capital gains.

As for those who have recently purchased properties they are not concerned about short term due to bright line test - this means it is at least a medium to longer term investment and today’s (or short term outlook) values are irrelevant as there is no intention of realising the capital gain or loss.

I speak from experience; as previously posted, bought an investment property just before the GFC and saw a 10+% fall on RV. No issue, short term fall but same yield and when I sold in the longer term - 2016 - I realised a good tax free capital gain.

Your comments are inconsistent with property investment - it is about the long term and short term gains or losses in value are irrelevant. Same; if you have a growth KiwiSaver fund it is not about looking and celebrating or fretting about short term fluctuations - a pretty basic premise about investment.

Sorry Printer8 but that's horsesh*t. I'm so glad you made smart investing decisions, and no doubt others have too. But the last several years in NZ have seen many investors 'upside down' on their monthly investment. Take the home I rent, for example:

Investor paid $750k for it in 2015.

Deposit, let's assume 20% = $150k

Rents it at $600 a week - went up April 2019 to $625.

Mortgage payments assuming at a rate of around 5% = $741 a week

Now I'm not a rocket scientist (but I am an investor), but that would put him upside down from the get-go.

Then on top of that, he has other costs, so let's factor in $5k for maintenance, $1000 for insurance, and $2629 in rates, per year.

On a weekly basis that's another $166 on his costs.

He doesn't have a property manager but if he did that would be around another 10% off the top.

Not looking like a great 'investment' on the basis of yield, is it? So I think we can assume that particular investor is banking on capital gains.

But let's be more conservative, let's say he put down 40% ($300k) and got a bank rate of 4%.

That's $494 in mortgage payments per week, plus $166 for maintenance, rates and insurance.

Total outgoings for loan and costs = $660 per week.

Again, with rent at $625, he is still in the hole, not to mention his $300k deposit isn't earning money in the bank.

If an investor in Auckland is not banking on capital gains he's a total idiot, because unless you are a slumlord, with (I assume) sh*te properties that you aren't maintaining, ripping people off on the rent, the numbers do not stack up. Not the same in the regions where yield is higher and capital gains are lower, but certainly in NZ's most highly populated city, it's not going to work out without a monthly drain on your account. Personally I like investments to pay me; otherwise I consider them liabilities.

So, given that we are facing a flat market (at best, more likely declining), with 'investors' making a loss each week, can you now see why many of them may choose to dump their properties, in certain parts of the country? Long term is indeed the plan, but it is not always sustainable for everyone, and the 'investor' who doesn't have cash reserves, and who finds themselves out of a job, may not be able to ride this one out.

FYI my investment homes are cash-flow positive and I've held them for over ten years.

You're numbers don't look right.

The interest rate isn't 5%, it's more like 3% if they fix. I worked out that at $625 p/w, 20% deposit and 3% fixed you would have been so generous so as to have paid $28.5k of your good landlords mortgage off within 24 months. Deduct expenses (rates etc etc), let's call that $6.5k per year, that leaves $15k. Over time the principle keeps falling and the rent keeps rising, your landlord will own that house within 25y when it will be worth around $2.5m

When the LL bought the rate was around 5%, assuming he fixed. Yes he could do a refi but there's added cost on doing that so you're not going to do it every year. Also if he bought later the house price would have been much higher — any LL who bought after 2016 would have had higher payments despite lower rates, and they haven't really started dropping much until fairly recently.

And most of that rental payment to the LL over the 24 months you mention would have been the interest. He's topping up monthly costs anyway, so effectively the bit he contributes in shortfall is like a savings plan, if you think that's worth it.

Your point about future capital value is exactly the point I am making, however. P8 said most landlords will have done the sums and be cashflow positive—my point is that they most likely will not be, in certain areas, and they will, of course, be looking at future capital gains. If the LL is *not* too over-leveraged and can ride through the tough times, despite his need to top up (which should decrease as rents rise, but could take many years), then the deal is good. That's why I own investment homes. Have someone else pay down your mortgage and end up owning outright - awesome (even better if you buy when prices are low and not at peak!).

But if s/he can't continue to hold because to do so is costing him or her on a monthly basis, that may be a trigger to dump the property.

I used 3% because that's where rates are today for a 20% deposit, maybe the houses is worth more or less, it's kind of irrelevant. Your sums omitted to include the fact you are paying off the landlords mortgage. I have to say the example you provided looked like it stacked up fine and probably was cash-flow positive if you use interest only rather than p&i mortgage. I/O at 3% = $346 p/w, so $275 p/w left to cover costs - that looks cashflow positive.

It's not irrelevant, because if he bought a house today for $750k, he's not getting a rent of $625 on it. More like $450 - $500 based on my area.

If you want to use IO at today's rate, still based on the house I live in:

House price now - say $950k (conservative)

IO rent at 20% down = $438

Plus $166 in costs = $604

Just scrapes in to the definition of 'cash-flow positive' - assuming no large maintenance bills, no vacancies, and no major hikes in insurance.

However if my LL is on an IO loan I'm not paying off his mortgage so your argument makes no sense - can't have it both ways.

I agree that you have to use current data across all aspects of the equation in order to have credible results. We need an example of a sale and rental at current market to draw a conclusion.

Sure, if you're trying to answer the question of whether buying an investment property now is a good idea.

I was discussing Printer8's statement that, "your landlord will will have done the sums before buying and will be currently looking at a gross yield of at around 5% and a net yield after expenses but before mortgage (tax deductible interest) of around 4%" and posited that "the sums" could only work if they factored in capital appreciation. I don't think there are many Auckland landlords who bought in the last 5 years on returns like that, no matter how many property books they read and seminars they attended.

But for fun let's see if buying now as an investor works. I'll look at Hibiscus Coast since I'm familiar with property values and rental values here:

Let's look at this one in Stanmore Bay, looks pretty decent for a rental.

https://www.trademe.co.nz/a/property/residential/sale/listing/243339098…

3/1, for $679k, let's say I get it for $660k

20% down, P&I loan, weekly payments of $511

Plus maintenance $4k, rates $1,973, insurance $700 = total $128 per week

Making my total weekly costs (without factoring in a property manager) $639

Being generous, I can probably rent this place for $575, maybe $600 tops. It would definitely not rent for more than $639, which it would need to to be cashflow positive. As an investment, with $132k of my capital tied up and not earning in the bank (plus, let's face it, some sunk costs for minor reno to get it tenant-ready, as well as inspection and legal costs), it looks even less attractive.

So no, it doesn't stack, unless your objective is capital appreciation, which doesn't seem likely for the immediate future.

Until homes like that are in the $500k range and market looks set to reliably increase in the near future, I wouldn't consider buying an investment home now, and holding one that is costing me money wouldn't seem very smart, either. My view is that's the level the bubble will reset back to, i.e. a decline of around 25% from where it is now. But who knows, nobody has a crystal ball.

"your landlord will own that house within 25y when it will be worth around $2.5m"

i) Value of house in 25 yrs (the year 2045): $2,500,000

ii) Value of house in 2015: $750,000

so house value expected to increase 3.33x (2.5mn / 0.75mn) in 30 years (between 2015 and 2045)

That is an implied capital price growth rate of 4.1% per annum for the next 25 years.

Assuming an inflation rate of 2.0% p .a - then that is 2.1 percentage points per annum of real growth (ie. inflation adjusted)

For the median house price in Auckland, does that seem reasonable?

No it's not reasonable, it's too conservative.

"it's too conservative."

Just out of interest

i) what would be a more reasonable rate of capital growth for the median house price in Auckland?

ii) what is that rate of capital growth based on?

From memory it is around 5% to 7% compounding in central Auckland over the last 30+ years. Please don't respond with a lot of "whataboutery", if you want to say this time is different I'm not going to buy it. The last 30ys includes a number of economic downturns. You are entitled to whatever assumptions you want to make, I will stick with reality.

Thank you for your response.

FYI:

i) 5% per annum growth rate for 30 years is 4.32x - so that $750,000 house in 2015 becomes $3,241,457 by the year 2045 (25 years from today) - that is inflation adjusted (i.e real) returns of 3% per annum (assuming 2% inflation)

ii) 6% per annum growth rate for 30 years is 5.74x - so that $750,000 house in 2015 becomes $4,307,618 by the year 2045 (25 years from today) - that is inflation adjusted (i.e real) returns of 4% per annum (assuming 2% inflation)

ii) 7% per annum growth rate for 30 years is 7.61x - so that $750,000 house in 2015 becomes $5,709,191 by the year 2045 (25 years from today) - that is inflation adjusted (i.e real) returns of 5% per annum (assuming 2% inflation)

These are averages and the IRR changes depending on a number of factors. You know there is a formula for compounded growth? I just can't type it here (easily). Here you go https://www.interest.co.nz/charts/real-estate/median-price-reinz

$135k/$925k over 26y = CAGR of 7.68% for Auckland. If you assume inflation was 2% then that is 5.68% real return over 26y compounding - just on the capital increase. Tee mortgage would have been paid off so throw in another $110k - that makes it 8.15% gross or 6.15% real. Then adjust it for return on equity (20% deposit - so $26k deposit), then that becomes 40.6% gross return CAGR. Starting to make sense now?

So there are still muppets that buy into the double in 7 thing? You understand where that equation leads right? Median of $3m+ in Auckland? Do you GENUINELY believe that? What would incomes need to be for that to be true? Also, given Akld has gone zilch in the last couple, that means still needs most of the growth in the next 5-8.

The median house price in Auckland as at May 2020 was $910,000 - https://www.interest.co.nz/charts/real-estate/median-price-reinz

FYI, median house price in 25 years (i.e the year 2045) at the same growth rates above:

i) 5% per annum growth rate for 25 years is 3.39x - so that $910,000 house in 2020 becomes $3,081,583 by the year 2045 (25 years from today) - that is inflation adjusted (i.e real) returns of 3% per annum (assuming 2% inflation)

ii) 6% per annum growth rate for 25 years is 4.29x - so that $910,000 house in 2020 becomes $3,905,602 by the year 2045 (25 years from today) - that is inflation adjusted (i.e real) returns of 4% per annum (assuming 2% inflation)

ii) 7% per annum growth rate for 25 years is 5.43x - so that $910,000 house in 2015 becomes $4,938,964 by the year 2045 (25 years from today) - that is inflation adjusted (i.e real) returns of 5% per annum (assuming 2% inflation)

Yes, $910k is correct. Why are you turning 7% annual growth to 5.43%, to adjust for 2% inflation? Adjusting for inflation makes it difficult to analyse, just leave them gross. What is indisputable is the returns have been nothing short of spectacular when compared to the equity put in.

The amounts are all nominal.

(1.07)^25 = 5.43x

Yes, so 443% gross return. We're in violent agreement, so would you take that return?

Te kooti, forget the equations, what misterB said is what you need to understand. House prices and income are tied at the hip. Now you can increase the leverage on the income to drive house prices up (essentially pulling demand from the future into the present) but this is close to being maxed out already . House prices may go up in the short term.. due to reduced rates, and no LVR restrictions, but they have only done this because it is a ponzi scheme that they need to keep a float to protect the poor souls that they have screwed over by allowing this thing to get out of control.

"Your landlord (if you are renting) is not providing social housing for you."

Never said they were.

Your comment has no relevance to my comment.

I was simply noting that "paying someone's mortgage" can be the same, if not less than, the dead money going to the Bank.

Current gross yields are not 5% in Auckland. They are 3.25% on average. (Unless your "sums" include some speculative cap gain element, which I mean would not be surprising)

https://www.barfoot.co.nz/market-reports/2020/may/suburb-report

Using your assumption of 1.0% for maintenance and costs (are we assuming a 100+ year asset? - that's nice and not conservative at all) that's a net yield of 2.25% (and it's not really a net yield, but anyway).

'Investors' are hardly as super savvy as you're making them out to be.

Property Apprentice accidentally sent me all their training materials after I signed up to listen to their initial spiel (and noted all the violations of the FMA) - it was hours of the most rudimentary mathematics and common sense.

Them "doing their sums" is like a remedial class using a calculator for the first time.

cmat

"Your landlord (if you are renting) is not providing social housing for you."

Bottom line is that investment property is that - an investment. Landlords are not providing you social accommodation at a loss - they are profiting from you.

Don't kid yourself otherwise.

cmat is kidding him/herself that landlords are providing social housing? I can't see where cmat stated this, or was it implied and I'm just not joining to dots? Please explain - thanks

"(Unless your "sums" include some speculative cap gain element, which I mean would not be surprising)"

Cmat

FYI, a property investor selling a property in Christchurch. Here are the calculations:

https://www.propertyclub.co.nz/2020/06/16/180c-colombo-st-beckenham/

Observations:

i) 100% financing assumption (cash deposit of $0) - using equity release, deposit recycling techniques presumably

ii) it is negative cashflow (3.1% net yield on property vs 4.3% average interest rate over 10 years). Even based on current 3.00% interest rate "specials", it is negative cashflow (assuming that the borrower even qualifies for a "special" rate) - https://www.interest.co.nz/borrowing

iii) capital appreciation assumption of 4.5% per annum

I wish the FHB well and that they enjoy the security and intrinsic value of homeownership.

If they are feeling confident regarding the security of their job and income and can service their mortgage there is little to fear. Clearly their bank concurs with them - banks have a vested interest in being prudent lenders. I would also be prudent, and as at any time, by paying down the mortgage as quickly as I was able.

For those who are knocking the FHB, you just keep renting. Nobody is criticising you for that and your landlord will be loving you paying down his/her mortgage.

I wish them well too. I don't think my LL is loving things all that much right now. The lovely home we rent from him has developed serious structural issues that will probably cost at least $30k to remediate. Probably wouldn't be such a big deal were in not for the fact that the price has already dropped a fair bit over the last couple years, and appears likely to be back at what he paid for it in 2015 within the next 3 years...just going by what "some people" are saying (to borrow a phrase from TTP). He also has to replace the carpet, and electric is looking a bit dodgy, and with that new healthy homes bill, there are going to be some other costs coming up soon. Must be eating into that profit margin big time.

I'm happy to pay him rent in the time being...while I watch for the right place to come on when the market finishes its reset. C'est la vie.

Big Data

If you only see doom and don’t like risk; stay in bed every day.

For every horror story there are a multitude of positives.

I find your comments in conflict with the abundant comments of other anti-property posters who are claiming property owning boomers are ripping off the system with tax free capital gains.

What is the party line? Are property investors “losers” or “leeches”? :)

Why not both? Rental yields really suck compared to S&P500 over the long term, especially considering the costs.

The leeches are the ones who buy multiple rentals to live off of their children's paychecks, stealing good deals from FHB's because they can afford it. And then tell everyone how smart they are to have invested in property... while people who made good money on the stock market (where money tends to go into productive ventures) over the past decade or two usually stay quiet.

CJ

Now you really have me confused - investors are “losers” and “leeches” . . . bit of a flip flop response not unexpected.

A couple of points:

Most boomers have experience of 1987 so are gun-shy of heavy investment in shares. Not a great experience.

Also, don’t get besotted with % gains (and I don’t necessarily accept that shares have out performed property) of shared vs property but remember that property investment is leveraged against the mortgage (ask if you need me to explain). . . . and please spare me the implications of short term falls as it is about long term, and

Hindsight is a wonderful thing, equities are volatile, and most (not all) property investors are older and more risk aversion.

You know that leverage up does mean amplified losses on the way down, right?

Perhaps most property investors are older because an entire generation has (largely) been priced out of housing

Why do people in this country always think that the stock market is buying shares in dodgy companies? Gambling your capital away. Sure, you can do that and a lot of people get burned that way.

But it's pretty easy and safe to buy an index fund of the top-performing listed companies in a market. The S&P 500 index is the 500 top US companies combined. Over the last 10 years has returned on average 15.3%. If those folks in 87 bought index funds they'd be multi-millionaires by now.

Does it fluctuate up and down more than property, yes. Will it crash and rebound, yes. But the growth of those 500 businesses (including Amazon, Microsoft etc), the economy and inflation means its always going to be trending upward over the long term.

We need to communicate the diversity of investments in this country. Not all property, not all index funds. But the same principle, buy and hold for extended periods. It's as safe and profitable as houses.

Leverage works both ways (ask if you need me to explain). Most New Zealanders haven't experienced property price falls, hence the illusion that it's a risk-free investment.

Yes, investors can be both losers and leeches. Do I really have to explain it to you again?

Also, why are boomers so scared of the stock market? Do they need a comfy blanket like 3-4 year olds?

Printer8, you may not be able to believe it, but *gasp* there is no 'party line'! So you can't lump what I say into 'doom and gloomers' just because I'm not a spruiker. Here's some things that will blow your noodle:

- I am a landlord, currently own two rental homes and have at one time had four. I'm not selling either of them any time soon, but I also don't think now is a good time to buy.

- I used to be an agent, but I believe spruiking the market is unethical. I wouldn't tell anyone now is a good time to buy.

- I work full-time for one of NZ's largest corporates and run another business on the side - I am pretty comfortable with risk, I don't stay in bed all day, and I have money in the bank. Still don't think now is a good time to buy though.

- I currently rent the home I live in, but I don't think my LL is a leech or a loser. I feel rather bad that he has all these maintenance costs coming up and hope paying our rent on time is at least one less worry. Still don't believe now is the time to buy.

- Not all landlords are boomers, although I think my partner could be older than my LL.

- I believe property markets reset when they get out of whack; you just have to make the best decisions you can with the data to hand, and not get too freaked out when you make a small loss or gain. The big ones are the ones to watch out for. It is impossible to time the market perfectly, but if it looks like a duck, walks like a duck, and quacks like a duck, it's probably a duck. Unless it's a swan.

Good luck with your investments, I trust you are snapping up all that the NZ property market has to offer right now.

"I wish the FHB well and that they enjoy the security and intrinsic value of homeownership"

What is the price of security and the non financial aspects of ownership such as peace of mind, free from fear that the landlord will sell the property and the tenant has to move?

That is up to each individual's personal preferences, and how much they are willing to pay for those qualitative factors.

Some owner-occupier buyers on a 80% LVR, may be willing to incur an unrealised loss in equity of 100% for that peace of mind, while others may be unwilling to incur such a large unrealised loss in equity for that same peace of mind.

For some recent owner occupier buyers, some believed that they were willing to accept a 50% unrealised loss in equity for that peace of mind at the time of their house purchase. Amidst the backdrop of a 10% forecast of drop in house prices by some economist (resulting in a 50% unrealised loss in equity for the 80% LVR buyer), now some of those recent owner occupier buyers are experiencing regret with their recent property purchase.

The information below shows the impact of property price changes on their equity value is provided to enable them to make their own informed choice.

Which will the owner occupier regret most:

1) missing out on future potential gains in equity?

2) potential loss of their savings invested as the initial deposit for purchase of the house or even potential negative equity?

For owner occupiers, a reminder of the impact of leverage (it amplifies property price changes both on the up and down):

Scenarios of financial impact of leverage on equity, assuming an 80% LVR for owner occupier, for a recent $1,000,000 property purchase, $200,000 initial deposit, mortgage $800,000. (simple round numbers used for illustration purposes)

A) Scenario - property price rise:

1) property price rises 5% to $1,050,000, mortgage $800,000, equity $250,000, so 25% gain in equity value from $200,000.

2) property price rises 10% to $1,100,000, mortgage $800,000, equity $300,000, so 50% gain in equity value from $200,000.

3) property price rises 15% to $1,150,000, mortgage $800,000, equity $350,000, so 75% gain in equity value from $200,000.

4) property price rises 20% to $1,200,000, mortgage $800,000, equity $400,000, so 100% gain in equity value from $200,000.

5) property price rises 25% to $1,250,000, mortgage $800,000, equity $450,000, so 125% gain in equity value from $200,000.

6) property price rises 30% to $1,300,000, mortgage $800,000, equity $500,000, so 150% gain in equity value from $200,000.

7) property price rises 35% to $1,350,000, mortgage $800,000, equity $550,000, so 175% gain in equity value from $200,000.

8) property price rises 40% to $1,400,000, mortgage $800,000, equity $600,000, so 200% gain in equity value from $200,000.

9) property price rises 50% to $1,500,000, mortgage $800,000, equity $700,000, so 250% gain in equity value from $200,000.

10) property price rises 100% to $2,000,000, mortgage $800,000, equity $1,200,000, so 500% gain in equity value from $200,000. (i.e if they believe that the property price doubles every 10 years)

Remember, the owner occupier must be able to hold on under ALL economic environments (including any potential significant reduction in household income).

B) Scenario - property price falls:

1) property price falls 5% to $950,000, mortgage $800,000, equity $150,000, so 25% loss in equity value from $200,000.

2) property price falls 10% to $900,000, mortgage $800,000, equity $100,000, so 50% loss in equity value from $200,000.

3) property price falls 15% to $850,000, mortgage $800,000, equity $50,000, so 75% loss in equity value from $200,000.

4) property price falls 20% to $800,000, mortgage $800,000, equity is ZERO, so 100% loss in equity value from $200,000.

5) property price falls 25% to $750,000, mortgage $800,000, equity is NEGATIVE $50,000, so 125% loss in equity value from $200,000.

6) property price falls 30% to $700,000, mortgage $800,000, equity is NEGATIVE $100,000, so 150% loss in equity value from $200,000.

7) property price falls 35% to $650,000, mortgage $800,000, equity is NEGATIVE $150,000, so 175% loss in equity value from $200,000.

8) property price falls 40% to $600,000, mortgage $800,000, equity is NEGATIVE $200,000, so 200% loss in equity value from $200,000.

9) property price falls 45% to $550,000, mortgage $800,000, equity is NEGATIVE $250,000, so 225% loss in equity value from $200,000.

10) property price falls 50% to $500,000, mortgage $800,000, equity is NEGATIVE $300,000, so 250% loss in equity value from $200,000.

For owner occupiers, an example of buying at lower purchase prices - the median house price in NZ was $680,000 in April, and fell 8.8% to $620,000 in May.

A) purchased in April

1) At purchase

Median house price at purchase price $680,000

Mortgage $544,000 (at LVR 80%)

Equity deposit $136,000 (20% of purchase price)

2) value today

Median house price at purchase price $620,000

Mortgage $544,000 (now LVR is 87.7% due to house price fall)

Equity value is now $76,000 - the original initial deposit of $136,000 is now worth $76,000 - a fall of 44% in just 1 month.

B) Alternatively purchased at today's median house price of $620,000

Same equity deposit of $136,000 as above

Mortgage $484,000 (now LVR is 78.1% due to house price fall) - the mortgage is 11% less than above - resulting in:

i) lower debt service payments, lower interest costs over the life of the mortgage (30 YEARS) or

ii) same debt service payments as in scenario A resulting in shorter repayment period of the mortgage loan, lower interest paid over the life of the mortgage.

A lesson in how leverage is a two way street. The debt mediarys dont understand this.

Reminds me of when we bought our first house we never even looked at the state of the local economy let alone what was happening in the USA. Just jumped into the market boots and all. Sure wouldn't be jumping into the current market but hey now older and wiser.

Looking for some advice re: new build.

We are looking at doing what was a kiwibuild (but now just requires we meet certain requirements) in bay of plenty.

500k for a 3 bedroom in a nice area.

With prices dropping is this a good call? We have 12% deposit but new regulations mean if the value of the new build drops too much by the time it is finished our equity might have dropped too much.

In saying that - this is the best new build price/deal we've seen (we have looked around). At this stage we are looking to go forward with it.

But I'd love some advice.

I would never buy with less than 20% deposit. Most economists predict an 8-10% house price fall in NZ this year. At an 8% drop, 66% of your equity will be gone.

Would a new build in a very nice area really drop that much? It's already extra cheap thanks to kiwibuild.

We are looking at other bank options. ANZ apparently does some sort of guaranteed pre-approval so we're looking down that avenue.

Sounds a bit risky, reliant on values holding up to be able to settle. So if you cant settle then you could potentially lose your deposit. Do you have someone who will go guarantor? When is expected completion date and settlement date.

And a more salient point... income and surety of income

Teacher and nurse with permanent contracts. Probably in one of the most secure income groups currently.

Nice. Do the sums. It should be <5x your income and <40% take home pay. You should be able to live on one income. Be prepared to pay more interest, given the low equity. Newbuild is great in that you wont need to put aside the same money for maintenance. I built recently in the regions, best decision (yes met all the same tests)

February next year.

Parents would only do guarantor if they absolutely had to.

The take-home point is the significant decline in credit growth year on year. That in itself will lead to house price declines.

*cough* ponzi scheme

Down one-third yoy... due to the restart most likely. Borrowing is effected on settlement date which takes time to process after a property goes unco. Low or non existent April sales. Lower number of sales overall as well.

Noise. Wait till the subsidy end. It is however lolly scramble year, so when may be is up for debate/election bribe.

FHBs are taking out large mortgages to buy excavators and then buying garden shovels using AfterPay to dig an even bigger hole.. Nice future for NZ

It's a stretch to call it a surge. It is 33%+ down on same month last year. It's obviously not a surprise it is higher than April, when everyone was locked in their houses.

As a side, the RBNZ data set is not about advanced loans - it is about loan commitments, i.e. the contract is signed. The settlement may not yet have happened.

Great time to re-balance your property portfolios. Offload your junk holdings to FHBs and re-capitalise for prime ones later. Great opportunities at this point of the cycle, don't miss the boat or you may end up waiting another 10 years! Drum up the FOMO!

Sad but true CWBW. They say the GFC saw the greatest transfer of wealth the US has ever had.

Be careful out there everyone, there will be blood on the streets before this is over—make sure it's not yours.

Have seen an uptick in FHB on my Instagram since lockdown! Especially in CHCH. A lot of my friends just don't seem to grasp or care about the extent of the economy

FHBs buying or just bored and browsing?

Brilliant, so person putting down 10% deposit can get hit with leverage loss as equity evaporates in next 12 months. Great idea, encourage young folk who know no better, to get into move debt.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.