First home buyers took a record-high share of the mortgage money advanced last month, according to the latest Reserve Bank mortgage lending by borrower type figures.

In June the FHBs accounted for $1.09 billion of mortgages, which made up 20.3% of the $5.364 billion total advanced during the month. The RBNZ said that was the highest percentage recorded by the FHBs since it had started collating the information in 2013.

Additionally, the FHBs actually out-borrowed the investors in June, which is only the second time that's happened (the first time in May last year) since the RBNZ started publicly releasing the data in August 2014.

Compared with the same month in 2019 the FHB borrowing was up 17.7% from $926 million.

In terms of the outright biggest amount of money borrowed by the FHBs in a single month, that remains the $1.243 billion borrowed in November 2019.

In its description with the data, the RBNZ describes a first home buyer as "a borrower entering the home ownership market in New Zealand for the first time".

"In the case of more than one borrowing parties to a loan, borrowers are classified as first home buyers only if none of the borrowing parties have previously drawn down on housing finance for owner occupation.

"If the borrower, or at least one borrowing party, has previously drawn down on housing finance for owner occupation they are classified as 'other owner occupier'."

Investors were fairly notable by their relative absence in June - and this is despite the fact that the previous requirement for them to find 30% deposits has now gone, lifted by the RBNZ when it removed the limits on high loan to value ratio (LVR) lending for at least 12 months at the end of April.

The $1.04 billion borrowed by the investor group in June represented 19.4% of the total advanced, which was the lowest share of mortgage money taken by the investors since August last year.

And it's all a far cry from the bull rush during mid 2016, when investors were accounting for about 35% of all monies advanced.

It was in mid-2016 that the RBNZ hit investors with a then a very stringent 40% (gradually more recently dropped to the 30% level) deposit requirement. Since then investor involvement has shrunk markedly.

In terms of the total amount of money borrowed in total during June, this represented a continued bounce-back of the housing market after the April lockdown month.

The June total of $5.364 billion, was up 24.2% on the $4.318 billion borrowed in May, while the May total was up some 57.1% on the $2.749 billion borrowed in April.

However, while the June 2020 figure represents a big bounce-back from the days of lockdown, the monthly total was still down on the $5.441 billion advanced in the same month a year ago.

And if we look at the figures combined for the past three months (April, May and June 2020) we can see the total amount borrowed during that period was down by nearly $5 billion (28.4%) compared with the same three months in 2019.

In the first half of this year, total mortgage borrowing has averaged $4.818 billion a month ($28.905 billion for the six months) compared with a monthly average in the first six months of last year at $5.33 billion (total $31.981 billion).

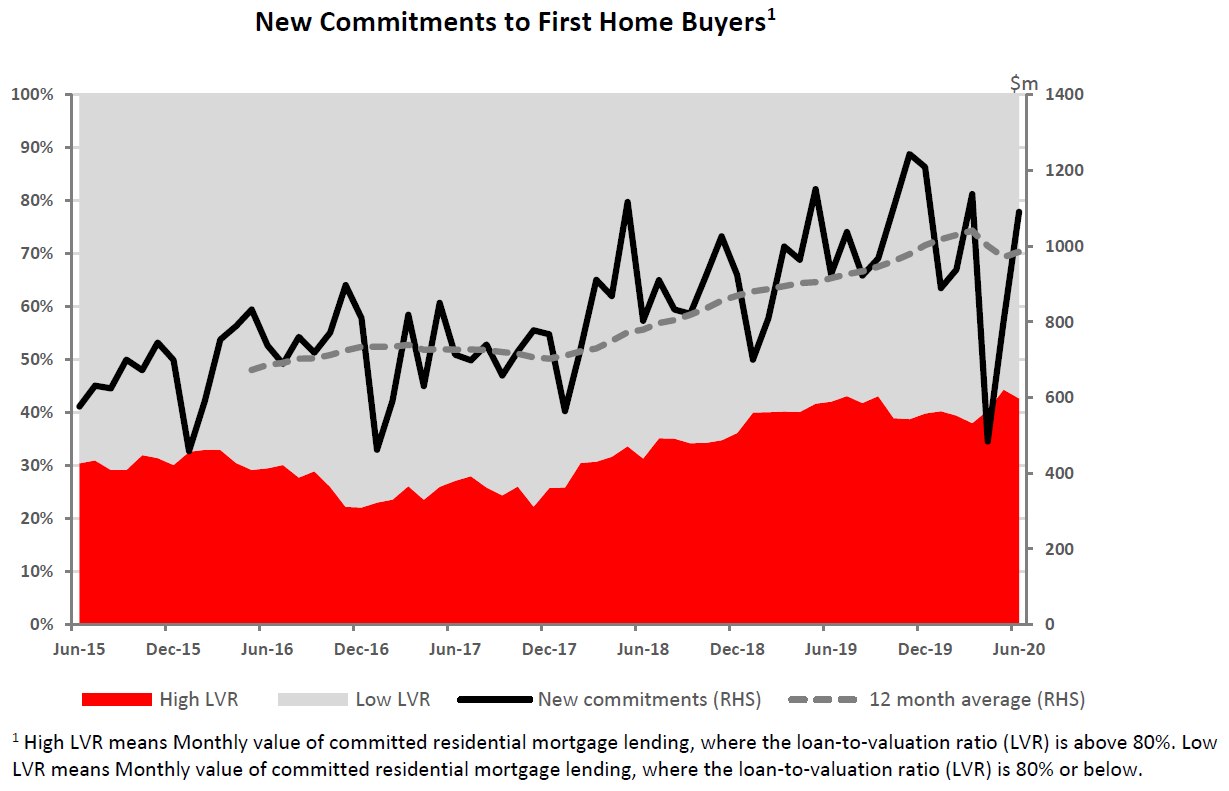

Just looking at some further detail in the first home buyer figures for June, we can see that of the $1.09 billion borrowed by the FHBs, some $466 million of it (42.8%) was for high LVR (above 80% of the value of the property) loans.

In recent times the amount of high LVR money borrowed by the FHBs has tended to make up just short of 40% of the total advanced to that grouping, although the percentage did blow out in May 2020 to 44.3%.

In June the $466 million of FHB mortgage money borrowed on high LVR loans was shared among 930 mortgages - giving an average mortgage size of just over $500,000. Figures for Auckland are not broken out separately in this category.

107 Comments

Why wouldn't you? If you have the deposit, paying 2.5% interest on $600,000 is only $288 as week. Add in your rates and insurance and say $100 maintenance thats $463 to own your own home compared to probably $550+ for the same house to rent. No brainer.

And where do those figures come from? Might be very different in different regions.

Just did the same calculation for the house we rent. $800k purchase price (as of 2019), $600 per week rent. At 20% deposit, 2.55% interest rate (25 years) the repayments are $666 per week. Add rates, insurance and other costs of ownership and you're down $100 per week. That's not bad *IF* you ignore opportunity cost and the expected capital losses in the next year or two.

So again, it's all about where you think the market is going, and how confident you are about your employment. If you think prices will be lower 12 months from now, don't buy now. If you think they'll go up, (and you will 100% have a job), sure, go ahead and buy something today.

he did it on interest only. Which is only an option if you already own a home.

Rducky

Interest only payments considered as principal payments are retained - see it as additional savings for retirement and financial security.

One kisses all rent goodbye.

Yes and no. One still has to make the principal repayments, even if they are ultimately retained.

But principal still has to come out of your weekly paycheck, its far from irrelevant.

And the winner is..................... THE BANK !!

Personally I have decided to buy a boat, better life stories.

Rents will rise. Once you pay off the loan, hey look at that, no rent. People who convince themselves that renting is cheaper than homeownership are playing a fool's game and what's worse for them, they will live to see the colossal error and have no one to blame but themselves. As for all of this 'time the market', its bunk, for some reason everyone who 'times the market' doesn't own squat.

I have always timed the market and am now a older millennial who owns a house outright (no mortgage) thanks to successively buying in a dip, renovating and then selling into a rising market (and renting in between). You don't have to time the absolute bottom or absolute top but it's not very difficult to get within cooey. It has served me very, very well.

Net worth or GTFO :-)

you also need interest rates to remain low. affordability is focused too much on the now, the great unknown is how long those rates will stay down for. obviously house prices tend to move in line with interest rate moves. so if you take out a mega loan now (at low rates) but cannot service it when rates go up (when you go to refix) then you are possibly going to be underwater due to the capital loss, unless house prices go up.

but who knows in this world, rates may remain anemic for the next 20 years and capital inflation goes crazy...

I think a lot of FHBs have been holding off for reasons like that and a potential market crash. You can't hold off forever.

Can any rational person see any possibility of rates increasing in the future though?

With RBNZ trying to keep the NZ Dollar as low as possible on behalf of our exporters, there is no room to increase our interest rates until Europe, the USA or Asia increase theirs or we will face a wave of foreign investment wanting to buy NZ currency to make the most of better interest returns here. I don’t know about you but I can’t see any chance of the USA or Europe increasing their rates any time soon.

CourtJester

So when do you plan to buy?

It sounds to me by just using a very simplistic and solely economic argument to appease yourself why you continue to rent rather than become a FHB.

For a starter, homeownership is far more than initially simply for economic advantage. There is considerable social and financial security as well as intrinsic value in homeownership. Economic advantage of increasing value, use of increased equity and being less than rent are longer term considerations.

So from an economic perspective, homeownership is long term and current - or even short term - comparisons are irrelevant.

In the past three years RBNZ figures show 80,000 FHB mortgages; that is probably about 140,000 people who are FHB.

So CourtJester, you just keep paying off the landlord’s mortgage; don’t mind him profiting from you; don’t mind the intrusion of regular property inspections; don’t mind the landlord deciding that he or family are moving in and you moving out and the kids having to relocate their schooling; either you don’t mind the landlord evicting you at an inopportune time to you because he/she has sold the property or the new landlord being a grump and doing those regular property inspections you just laughed at; deciding to paint all the interior walls in that bland horrible colour cheap bulk lot of paint . .

And in ten years don’t moan that you have been financially left behind. Boomers are often criticised because they are financially secure in their homes . . . What you tend not to hear about is the boomers who have rented all their lives and are now living in dingy little council social housing.

LOL nice try, but FOMO doesn't work on me.

If you really care that much, I plan on buying around the end of 2021.

By the way, please clarify what you mean by "There is considerable social and financial security [...] in home ownership." Do you mean financial security in home ownership *without* a mortgage? That would make sense. Not sure how owing $600000 to the bank and having no cash (or TD's) would make me more secure financially.

You tend to get "conditioned" once you've tried to time the market once or twice and realised at the end of it all if you'd just jumped in at the earliest opportunity you'd be far better off. Back in 2005, at 25, I paid off my student loan with a cheque (it was incurring 7+% interest at the time) rather than buying a house because the house prices had surely done their dash back then and were due a massive fall.

Then the 2005 election happened, Helen Clark made student loans interest free and the market had another 2+ years of really decent growth in them before they hit a plateau in 2008-2009 (didn't really fall much). Finally bought my first house in early 2013 at 33 having endured another eight years of flatting in squalor.

I've since done very well and the pain of missed opportunity buying something back in 2005 has lessened somewhat since I've been lucky since and probably narrowed the opportunity cost with some unintentionally shrewd moves. Still would have been best if I just jumped in in '05 though, and would have had 8 years of my life improving my own living standards rather than living like a poor student to build a deposit again.

First-home buyers who got in two or three years ago (or longer) are creaming it now.

Yet there were people here telling them to hold off buying a home..... Their shortsightedness was pathetic.

TTP (Tom)

Again, using the word pathetic while talking about fellow commenters' opinions. Why are you so upset that some people hold different views than yours?

By the way, nobody's talking about FHB's who got in 2-3+ years ago. I'm talking about getting in now. Actually, I don't think you understood my comment at all. My conclusion was, you should either get in now or not, based on what you think is going to happen to prices in the next year or so.

TTP

Agreed.

I find it a hard to believe that many of those who were calling imminent bubble burst over the past four years or so are still bleating the same.

Mind you, some like RetiredPoppy, seem to have rightly disappeared no doubt rightly somewhat in shame. :)

I have watched several houses around me which sold in 16/17 and then again in 19 take ~$300k losses. So even leaving aside the "future will be like the past" aspect of it, I don't even agree with your assessment of the past.

With all due respect, realterms, I think you and your DGM mates would be hard pressed to find first-home buyers who have lost $300,000 in the last 2-3 years.......

Most first-home buyers have done damned well - as you surely know - and to top things off they're paying minuscule interest.

Suggest you face reality. There's no point in being jealous and angry - like FraughtJester......

TTP (Tom)

I do not claim that these were FHBs. As 2m purchases they would not have been anyone's idea of a fhb. Be that as it may, their owners certainly did take 15% (300k) losses for having bought at the top and being forced to sell.

FHBs haven't done as badly I agree. But equally those who bought in 16 - including several sets of friends - are probably back to where they started. Certainly wouldn't say they've done fantastically well.

I am offering no predictions about the future here, though I don't suppose that will stop you labelling it as 'DGM'.

For goodness sake, realterms, the whole context of this article/thread is first-home buyers.

Read the first three words in the headline!

TTP (Tom)

Funny that. And here I thought you were talking about bubbles (or not).

Even in strictly FHB terms I very much dispute that those who bought 3 years ago are "creaming it".

Might help your argument if you separated reg to FHB in Auckland and elsewhere. FHB in Auckland have seen barely any cap gain in 3.5 years whereas in other parts of no they have

How about rent, mikekirk, or did you conveniently forget about that?!

Did it occur to you that first-home buyers save a bundle of $$$ by not having to pay any further rent?!

Had you not noticed that Auckland rents can be quite high?!

Get real, old chap!

TTP (Tom)

Actually, rent in Auckland is frequently cheaper than servicing a loan to buy the same house.

Exibit A : https://www.hud.govt.nz/news-and-resources/statistics-and-research/hous…

TTP did you conveniently forget about rates, insurance, maintenance (especially on the over-priced trash stock at the lower quartile used in many 'affordability' measures?)? Did it occur to you that FHBers may have assumed job security and then they (i) had a baby (ii) suffered reduced income due to covid or (iii) lost their job?

Being a property spruiker, i thought you'd be well aware that the rent charged relative to the house value price in Auckland is actually pretty poor, for $600/week you can rent a million dollar property..

Calm down old chap. You are bordering on hysterical.

Hi Tom,

certainly rents are an incentive to buy at these level of interest rates. Quite so.

Problem at present in Auckland esp, is the level of risk to those under 30, re employment. First to go if there are job cuts and 2 incomes are needed to service a mortgage

Hence, FHB purchasing in Auckland since end of March 41% down in Auckland in $600-850k bracket.

Housing is certainly an excellent investment outside of Auckland due to land being $200-350k cheaper on average, even 40km away from CBD

Plus, there is the pesky deposit to raise still.

Have owned outside of Auckland for 3 years, my mortgage amount would cover just the deposit on a $600-850k bracket home. Increasing our mortgage payments to the equivalent of median rent (Wairarapa) would have us paid off in 9 years or 5 - 6 years if we paid the equivalent of median rent in Auckland.

"First-home buyers who got in two or three years ago (or longer) are creaming it now."

Absolute b*ll*cks.

FHBs who purchased around 2017 in the Hib Coast area have seen price falls, with more on the horizon. Worse, there is way more choice of properties now than 2 - 3 years ago, not a great feeling when you look around and realise you could have got what you really wanted if you'd just waited a bit. Not exactly what I'd call 'creaming it'. Unless you have a different definition than I do.

Are we approaching the "no one left to buy" phase of the demand cycle?

No Jonny

Just that number of FHB is at high levels (2417) which is high over the six years that RBNZ have been collecting data.

Improving affordability might have something to do with it.

Great for FHB.

Less competition from investors who see less upside going forward?

Yeah I think that is it, investors are taking a bath in Oz too (see recent vid on FMA (Edit: DFA: https://youtu.be/Wx8pOQBZDYA) site).

The smart money starting to withdraw from the market, leaving other types of money...

Yup that's it. Everyone else has taken a seat, only the young and naive are still dancing. Music stops soon.

I thought the music was a 10 year long track on repeat?

Grandma is drunk and dancing close to the turntable..

Yeah I feel that’s probably right. Although John Key just bought his son a house, that’s probably a good index to watch as well.

Yeah, NZ's equivalent of "Don't fight the FED".

Auckland commitments have dropped back from around a remarkable 55 percent of new lending in June 2016 to 42 percent currently.

Interesting that investor percentage is quite a bit lower than previously.. Some retrenchment still to come?

Hook

Investors are solely looking at buying as an economic Investment. Widely held view is that there could be some fall in house prices so it makes sense to hold off.

FHB are purchasing for other reasons. They are simply deciding not to put their lives on hold, get that home and start having a family which for a number of reasons is far preferable in one’s own home rather than a rented flat.

We have been hearing of bubble burst on this site for five years - keep renting, keep putting your life on hold.

We have been hearing of bubble burst on this site for five years - keep renting, keep putting your life on hold.

Property bubbles are driven by credit bubbles. Both eventually burst. Always do. Now is probably a good time for that to happen.

You are right .. just as I am right when I confidently predict that the world will end one day.

Neither of the 2 true statements is any help in making a financial decision.

Neither of the 2 true statements is any help in making a financial decision.

Well, if there's any risk the property and credit bubbles burst, making a 'financial decision' like buying an overpriced house is something you don't want to take lightly.

Agreed, if buying your own home there isn't really a "good" time or a "bad" time.. only the "right" time depending on personal circumstances.

Start that family they cant afford due to crippling debt?

Hi Printer,

as a matter of interest, take a look on RBNZ stats page and see the newly added info re income brackets for FHB and which income brackets' borrowing is increasing.

Only those with income over $115,000 have increased borrowing in last 3 months.

And it does not state whether there are 2 incomes in that.

Problem crux for FHB is generally need 2 incomes and in current climate, one of those would likely be at risk, generating, if so, a big headache re affordability

One would expect investors to drop out. They are getting older, cap gone has gone, neg gearing has gone, tenancy rights are increasing. A few fhb's have been suckered in, but the smart money is staying parked. The fhb's will soon drop off, job uncertainly and a growing swing in sentiment will take care of that.

Just look across the ditch.

Rastus

Same old, same old as for last five years. Bubble burst, bubble burst . . .

Remember the tale concerning a shepherd boy who repeatedly tricks nearby villagers into thinking a wolf is attacking his town's flock. When a wolf actually does appear and the boy again calls for help, the villagers believe that it is another false alarm and the sheep are eaten by the wolf.

Surely you don't think there's no difference between the last 5 years and this year though. These are fairly unprecedented times.

Novel coronavirus sparks a once-in-a-hundred-years global recession, causing millions to be unemployed (and therefore cannot service mortgages / pay for rent) and literally stops tourists from coming in to a tourism-dependent country like New Zealand.........

"Nope! Not different at all to 5 years ago."

ha ha....loving it. Now...back to my gold stocks......

Rastus's credibility has also burst.

TTP (Tom)

Not Tim anymore?

Hi gingerninja,

Call me Tom/Ted/Tim/Trev/Todd/Tony/Theo/Toby/Trent/Terry/Troy/Tau/Travis/Thane - or whatever you like.

It's the quality of the discourse that counts for me.......

TTP (Tostig)

Tum? ('Tim' with a strong provincial kiwi accent)

Greetings Tim the Enchanter.

Hey Tim, given your intimate knowledge of the housing market, have you noticed a lot more FHB activity and a corresponding reduction in investor activity? What news from the Property Brokers coalface?

Sorry, Gingerninja, I don't know any property brokers.

I rely upon people like you as a source of knowledge and wisdom.

TTP (Thane)

Rastus - Where on earth do you get this - A few fhb's have been suckered in, but the smart money is staying parked ? I would say from my connections in the market that is 100% wrong. Smart investors and smart FHB's are very active in the market and for good reason. To date there looks likely to be little or no drop in prices excluding Queenstown area. For most parts of the country it is cheaper to buy than rent if you have a good deposit. Be happy for these people it's a rear opportunity for them to get on with their lives in a home of there own.

...take off the blinkers, push away the rear view mirror and look at the road ahead (or are you a landlord or banker perhaps..desperate fr the fhb's to bail you out)?

Rastus - I think you are RP undercover, seem very similar, same story, anyone buying now is a mug, disaster around the corner....

I'm a very successful retired ( self funded retirement ) Landlord, this is a great time to buy property, as long as you have a good deposit and the bank will make sure you can afford it, still using 7% interest rate in their approvals. Actually I am looking at the road ahead in my new supercar I took delivery of on Friday, testing it in the Coromandel over the week. Happy Investing !

Hi Shoreman,

Congratulations on your supercar purchase! (But beware - some here will get all nasty and jealous.)

Will look out for you on the picturesque roads of Coromandel.

I'll be driving my trusty 1969 Hillman Hunter 1725cc (with whitewall tyres and towbar).

Best,

TTP (Travis)

Let them eat cake.

TTP (Tosser)

A few fhb's have been suckered in, but the smart money is staying parked ?

'Smart money' has not been flowing into NZ houses. That much is guaranteed. It's been flowing into assets like gold and gold miners. That should be quite obvious by now.

These stats contradict your anecdotes

Savvy Investors knows when to buy and when to wait just like in stock market as of now institutional investors / Banks are not going all out to buy stock but waiting on sideline with cash unlike retail investors (Equivalent to FHB) who are investing and many by borrowing as interest rate is low and till now have been lucky, which again gives them a false sense of being stock savvy and investing beyond by borrowing.

Dangerous environment where risk is very high compare to return - unless one has already made a fortune and have deep pocket to play around.

Only time will tell so is wait and watch specially now.

I could tell a great joke about asset price inflation - but only a small number of New Zealanders would benefit.

hahaha I'd pay to hear your joke but the price has doubled the last time I checked

Haha, a joke about centrally-driven wealth redistribution! Suck on that, younger generations! And get out there and work so you can pay for older Kiwis' pensions.

It sounds like the classification for a FHB is just you are taking out a first mortgage in NZ... so ostensibly..

- returning Kiwi having sold overseas property?

- new migrant who could be any age and have owned numerous properties in their lifetime?

- previously bought a home in NZ without needing a mortgage and then at some stage mortgage a property you own?

.... and all still be counted as a FHB?

How many of those counted as FHB are actually buying a home for the first time in their life?

The RBNZ may have lifted the limits but what I have heard is that the banks are still bring cautious. Perhaps that explains the relative lack of investor activity.

Fritz

Agreed, dispite many claims that banks are reckless, it appears. that they are protecting themselves and being very cautious - in fact tighter in their criteria than over the past few years. Looking very closely at both job and income security, and seeing wage subsidy as a red flag.

However the equity issue (despite RBNZ removal of LVRs) seems to be disadvantaging FHB more so than investors.

Agreed, dispite many claims that banks are reckless

Depends how you look at it. They have many customers with elevated house prices but living payckeck to paycheck. This is a result of their 'lending into existence' to punt on house prices. Arguably this could be considered "reckless". It appears it's coming back to bite them in the arse right now.

Printer8, why do you think the equity issue is disadvantaging FHB more? The stats in this story seem to suggest otherwise - noting we can't be sure what is behind them.

Fritz

Low equity is more commonly an issue for FHB and less so for investors who more commonly leverage of equity in other properties which is commonly higher. Banks are applying low equity premiums, are looking very closely at those who have low equity and especially their income and jobs - this is less of an issue for investors with multiple (employment and rental) incomes.

I posted a month ago that talking to a broker - family so not spinning me - that FHB were very active (which has come about) but many were finding it tough and were frustrated due to low equity but this was not so for investors. Many investors were just watching and waiting given likelihood of some price correction.

If banks are scrutinising the amount and security of income then without the international student and tourism numbers (returning Kiwis are a drop in the ocean and are no way near filling the void) and with unemployment likely rising later this year, there is likely to be downward pressure on rents and therefore investor income. If the investor has several properties and high leverage, then any capital losses would be amplified by that, especially if they have been recycling maximum equity. So these group of investors might be struggling to access lending more than FHB who do not have all their eggs in the one property backet.

It would be good to have the data on how many applications are being rejected as mentioned above.

Ginger

Anything is possible; there is no script based on current experience.

However the downturn in international students and tourists on working visas are going to be very much niches (e.g. less so 3bedroom family homes) and somewhat confined to some localities (e.g. Auckland and Queenstown).

I have also post previously that this RBNZ data and increasing investor activity is particularly value as a possible indicator that investors - those with experience of property - consider the market bottoming.

As to demand for rental accommodation, here in Hawke’s Bay I have previously posted that there is considerable shortage with up to 20% of motels housing homeless and MSD offering to manage properties, including finding tenants and guaranteeing rents all at no cost due to the shortage.

As for rents - irrespective of it not being desirable- the accommodation supplement is holding rents up to the detriment of those who don’t receive this allowance.

As for FHB, their focus is about buying a home - not an investment property. Two very different things. FHB are in for the long term so short term fluctuations and timing the bottom of the market are less critical. For FHB, the extent and timing of the fall of the market is so uncertain - the most important consideration is being able to service the mortgage and being prudent and paying it down as quickly as practical. Given that bank economists have revised their estimates of fall down (from 10 to 7%) so the significance of the possible fall is of equal significance to buying well and buying poorly. (Yeah, yeah, the team of Westpac economists and knowledge of what is happening is all cr*p and the lonely interest.co key board warrior sitting in their dingy little flat knows far better!)

Personally, I am pleased to see 2400 FHB (3700 people) - which is historically high - achieving their goal of homeownership.

It's a pity RBNZ does not request banks to supply a schedule of rejected formal applications for residential homes subdivided into home buyers, investors. and FHBs. That would give a clearer overall picture than just what mortgages they actually write.

So at 2,5% mortgage rate the instalments have halved since it was 5% ( not so long ago )

We now have the ridiculous scenario where its cheaper to own than to rent a home .

This is pure arbitrage , prices will rise very soon and the gap will close

If this were true, investors would be rushing in headlong at the tempting yields. Not much evidence of that, though.

Real terms

Investors are just watching and waiting.

Exactly. They're not drooling at the returns on offer. And why is that?

You're all speculating. The proof of the pudding will be the second derivative of mortgage credit wrt time. You can see what's happening at the end of the month when the next tranche of RBNZ C5 credit aggregates come out.

Don't disagree about speculating. But do you really think you can read a second derivative off a monthly series reliably right now?

.

Monthly with a 12 month lag for the difference. Then it’s automatically seasonally adjusted. After the GFC that metric bottomed out in 2009 which corresponded to the ideal time to buy a house

You're right though realterms. From an error propagation point of view, taking a difference amplifies the error and so doing that twice is even worse. However the larger the time difference the smoother the result. On monthly data a delta of 12 time points gives you a year which smooths it out a lot. I wouldn't use a delta of 1 month. That would be meaningless.

Hahaha realterms ...what yields !! .....kiwis have lost the meaning of the word "yields" ! ...I'm getting a 15% gross yield on a property in the USA ....but all the "sheeple" have been brainwashed as to what a "good" gross yield is .... 6% fantastic ....5% top stuff ......4% excellent .....3% very good ......2% good ......1% don't forget about those "endless capital gains" !! .....and that's the whole point - without any capital gains in NZ you actually lose money.....but who cares, as long as the bankers, RE agents and all the hangers on are happy, that's all that matters !! ......caveat emptor !

It was cheaper to buy than rent 7 years ago at 5.15% interest. What's changed is that everything has just doubled while interest rates have halved.

How much is increasing government regulation and other factors cooling investor demand though?

It may not be a purely financial decision not to buy now.

I suspect many landlords and land owners (farmers) are feeling increasingly picked on by rapidly increasing government and council regulation and see a strong likelihood that will only get worse as it looks inevitable that Labour or Labour/Greens will easily form a government in September without Winston Peters to occasionally put the brakes on their plans.

There are many, many caveats to that.

The obvious one being the possibility of interest rate rises -- which I will agree is not likely in the near term, but a mortgage is usually 30yrs now...

Also, the standards are not necessarily comparable. Sharing a flat, me and my wife pay $320 p/w to live in a place where the mortgage would be $1200 p/w, a huge house in the inner suburbs with garden and swimming pool. Granted, sharing a flat as a married couple is unthinkable to many, but in terms of quality of life, it's half the price of renting or buying a windowless 2bdrm unit. One of the remarkable things about our inflated market is the relatively small price gap between the crappiest of the crappy and properly desirable places. The desperation has really pushed the prices at the bottom end - what most FHBs can actually afford - up far beyond what makes sense from a qualitative point of view. I'd argue that, compared to other markets, big old villas in Mt Eden at $1.5m aren't massively overpriced -- but $900,000 townhouses on tiny sections in Flat Bush are absolute madness.

You know you can buy a house and share that too. Depending on how many people you're currently sharing with your mortgage payments might be a lot closer to $320 p/w on your $1200p/w example if you're sharing with two other couples.

I suspect it the income side of the ledger that will bring things back into balance.

Not true since prices are still disproportionally high and rents are going down.

Auckland FHB numbers are well down on 2019 over last 4m I am afraid. And June was tself 7% lower in bracket most associated ie 600-850

Rest of NZ bracket for FHB is about 200k lower so not surprising that sales excl Auckland are up

Why do agencies in nz never give full figs!

have you considered that many of the houses that were selling at the high end of the 650k-850k bracket are now selling in the next higher bracket.. inflation I think it's called.

I have yes but house price inflation in last 3 years in Auckland has not been much to write home about

Last 3 years? You were referencing 2019. And the 1y Auckland HPI change is 7.7%.

Not for FHB type purchases it isn’t

Also 2016-19 prices barely moved except down a bit

So credit is not growing year on year...anyone want to have a guess what that does to house prices?

Congrats to all the FHBs

FHB, just buy that house. You going to be a slave to the banks anyway.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.