You can lock them up but you can't tie the New Zealand house buying public down for long.

The latest Reserve Bank residential mortgage lending by borrower type figures show that nearly $6.6 billion was advanced in mortgages last month - which is the highest figure for a July since the RBNZ started bringing this information together in 2013.

And the first home buyers are continuing to march.

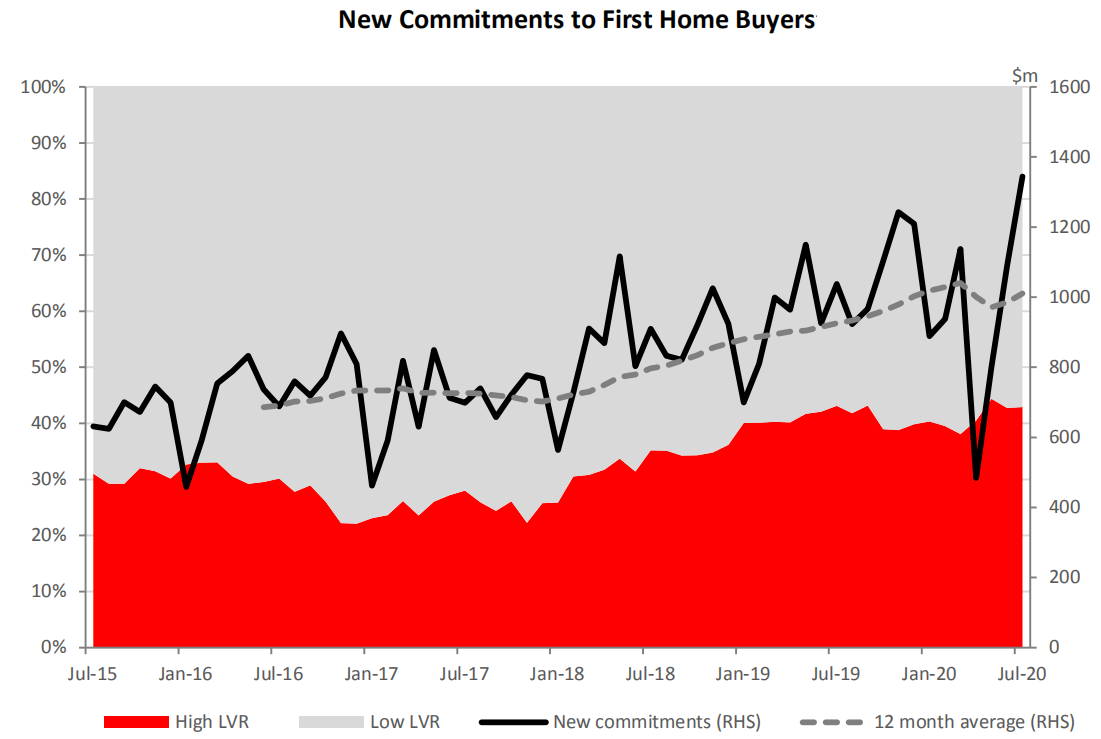

The FHB group borrowed $1.344 billion in July - the highest monthly total by this grouping since the start of this data series, beating the previous record of $1.243 billion borrowed in November 2019.

Additionally, the 20.4% share of the month's mortgage money for the FHBs was that group's highest proportion - just edging past the 20.3% share the FHBs recorded in June 2020.

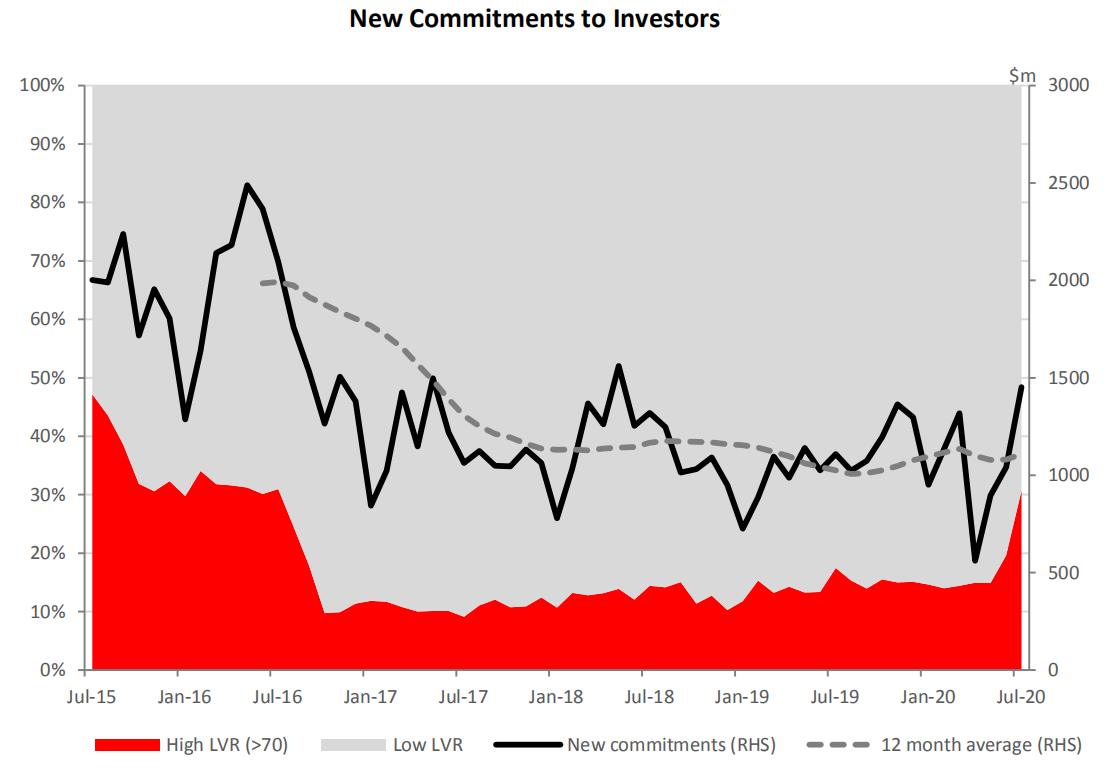

Of interest also is the fact that the share of lending taken by the investor grouping rose to 22% from 19.4% in June.

That's historically low when you compare it with the circa 35% that the investors were taking in the very bull days of mid-2016, but it does show something of a rekindling of interest. And perhaps interest is the point - given that returns on conventional investments such as bank term deposits are now so low.

In fact, the $1.451 billion borrowed by investors in July was the biggest monthly total borrowed by this grouping since May 2018.

The other key point to remember in all this is that the RBNZ from May 1 this year removed - at least for 12 months - its limits on high loan to value ratio (LVR) lending. That means it is now totally at the discretion of banks how much high LVR lending they do.

High LVR lending to investors (bearing in mind that this means above 70% LVR specific-to-investors) more than doubled in July compared with June, to $446 million.

LVR limits were in place from 2013, initially having a disproportionate impact on FHBs and their ability to compete with cashed up investors. That started to change hugely in 2016 when the RBNZ clamped tough special limits on investors, requiring them to have 40% deposits, which was eventually eased to 30% prior to the removal of the LVRs altogether this year.

The below graphs highlight the sharp rises in lending to FHBs and investors. Note the RBNZ definitions on LVRs at the bottom of this article.

Here's some of the highlights of the month's mortgage figures as detailed by the RBNZ:

- Total monthly new mortgage commitments were $6.6b in July – the highest July figure since the survey began in 2013. This is an increase of $1.2b (22.8%) from June 2020 and up 11.4% from July 2019.

- New mortgage commitments to first home buyers increased from $1.1b in June to $1.3b in July and other occupiers increased from $3.2b in June to $3.7b in July.

- First home buyers accounted for 20.4% of new mortgage commitments, up from 20.3% in June. Investors accounted for 22.0% of new mortgage commitments, up from 19.4% in June.

- The year-on-year increase of 11.4% in new mortgage commitments was driven by the increase in annual growth outside of Auckland. In Auckland, new mortgage commitments were up 3.9%, while new commitments outside of Auckland rose 17.6%.

- The nationwide year-on-year growth in value of new mortgage commitments to first home buyers was 29.6%, while new commitments to investors was up 31.0%.

- Monthly new mortgage commitments with high loan-to-valuation ratio have increased since the restrictions were removed in May 2020. High LVR new mortgage commitments to investors more than doubled in July compared with June 2020.

The RBNZ gives these LVR definitions:

High LVR [for FHBs and other owner-occupiers] means monthly value of committed residential mortgage lending, where the loan-to-valuation ratio (LVR) is above 80%. Low LVR means monthly value of committed residential mortgage lending, where the loan-to-valuation ratio (LVR) is 80% or below.

For investors, high LVR means monthly value of committed residential mortgage lending, where the loan-to-valuation ratio (LVR) is above 70%. Low LVR means monthly value of committed residential mortgage lending, where the loan-to-valuation ratio (LVR) is 70% or below.

87 Comments

Ouch, better hope the New Zealand housing market is now to big to fail.

It is too big to not to fail.

I don’t know who’s more irresponsible- the first home buyers themselves or the banks lending to them.

Just when I thought the housing market in Auckland couldn’t get more ludicrous yet here we are! My view is that this is the parabolic move, and we know sharp declines usually follow.

Takes 2 to tango

The assumption that all FHBs are mid-20s, early-career workers and are likely to put the housing market at risk of delinquency is incorrect.

There is a large cohort of recent first home buyers that are mid-career expat professionals in their 30-40s with higher than average incomes, having recently gained permanent residency in NZ.

"The assumption that all FHBs are mid-20s, early-career workers" - I don't think anyone sane assumed that in the past 5 years or so. We all know that buying a first home in one's 20s has become very difficult without parental help.

Exactly.

We're a 35 year-old couple and have recently bought our first home. Most of our friends have purchased their first homes within the last 5 years. All of them have secure mid to high-level careers and good equity in their homes. Our way of getting ahead was that we invested in growing my business, while my wife expanded her career. We're now lucky enough to have 40% equity in our house, a solid business/career and a manageable mortgage.

These days it takes until your 30's/mid 30's to pay down student loans, get a deposit and have a job paying enough to be able to service the mortgage.

Yeah I agree with you. It takes that long now to get established and have the ability to pay a mortgage, let alone to have the deposit. Having said that things were probably not that much different in the past if there was no help financialy from family.

"There is a large cohort of recent first home buyers that are mid-career expat professionals in their 30-40s with higher than average incomes, having recently gained permanent residency in NZ."

Have you got any solid evidence of this apart from the 1 anecdotal evident above ?

FHB do not have to be experts in finances to get a mortgage, on the other hand it is banks who must do due diligence and advice to whether the loan can be signed so take your guess :)

The banks are only doing what the RBNZ Gov wants them to do - prop up the market.

Have any banks changed there forecast to a 10-20% increase yet? Because that's what's happening at the moment, some absolutely massive prices being achieved

This is going to be an election issue for sure.

Just when the twentysomething renters thought a decline in prices were finally coming, boom, prices look to march even higher.

By March they will be even higher

Some big calls being made here!

I say it' still too hard to call.

Big support provided by bargain basement mortgage rates, which will go even lower.

Balanced by the economic carnage still to come....

Some banks are going to be 40% out! Economists eh ...

Bank economists don't forecast, they provide spin to sell their agenda. That means "house prices only go up" until there's free money on offer, then they predict a "possible decline of up to 10%". Better get some free money just in case.

"The causes of all panics, crashes and depressions can be summed up in only four words: the misuse of credit." ~ Ludwig von Mises

Sure. Whenever I raise the point that most if not all bubbles are primarily credit-driven, the response is typically mute.

The assumption that all FHBs are in their mid-20s and at early stages of their careers and will put the housing market at risk of delinquency is incorrect.

Many people at work are mid-career expat professionals in their 30s with higher than average incomes, having recently gained permanent residency in NZ are either looking to buy or have bought their "first home" in the last few months.

Many people who have lived here the whole time are in their 30s, DINKY professionals who have taken time to accumulate a deposit for obvious reasons. The difference is servicing or even getting ahead of a massive loan on lower wages, which people who live here may be more used to.

I stand to be corrected but from recall the average age of a FHB in New Zealand is between 33-36 years of age. The issue regarding 'mid career expat professionals" " having recently gained permanent residency",buying homes, whether this is just a recent anomaly or occurrence, is clearly in issue at present and for the period going forward given the dearth of new arrivals, or any arrivals.

They will all be in a negitive equity position shortly. Its a shame that a few more fathers couldn't have looked after their kids futures a bit better with some useful financial advice.

They will all be in a positive equity position surplus shortly. It's great that a few fathers have looked after their kids futures with some useful financial advice.

You mean financial advice and a $100,000 gift.

Would you like my bank account? I accept all donations

Completely spot on, actually many of those parents likely supported their children thinking they were doing them a favor. There's a concerning lack of financial culture and banks are not really doing their part.

Thanks b21

Sorry - whinging about the need for bank of Mum and Dad is not necessarily the case.

My wife and I have four children between us - all four had purchased homes by their early thirties.

The economic advice from this father was "you are on your own, if you want it, then do something about it". They appreciate it and have a great sense of achievement and pride in home ownership.

Clearly there are at least some of this site who feel entitled and whine that they need to bludge off their parents - clearly been given poor economic advice.

Nobody is whining printer8 except for you with this deplorable comment, I do not think you read my comment carefully since we mostly agree in the basic idea.

No b21; you may not have been whining but I keep hearing about the assumption for the need for bank of mum and dad to become a FHB.

I suspect “deplorable” to many because I didn’t helped them out.

I have a great relationship with my boys - get invited to a cricket/rugby test match weekend with them at least once a year. They see it as being a reminder of the matches and time I spent with them as kids.

I do not make personal comments towards you or any of the members on these forums, please avoid personal references yourself. I encourage you to find a reference where I mentioned what you claim, might be others but not me.

Yeah right, you most definitely make personal "comments" towards me

Blunt, but not deplorable.

Realagent, why would you assume it is fathers that give the financial advise? My husbands knows zip about finance, whereas I'm the one who manages all our finances and investments, teaches our kids about finance and economics etc (as their mother). I also know significantly more about finance than either my own father or my father-in-law.

Good on you Ginger - you also make more insightful comments on this site compared to many posters. :)

Absolutely she does

Thanks GN

Gingerminja - I was figuratively speaking, by father, I mean anyone who watches over or cares for their wellbeing. Surely that was obvious.

No it was actually sexist but carry on Boomer ;-)

Also known as parents.

First thing that came to my mind too. Casual sexism alive and well. Thanks for the call out GN.

Theoretically, as interest rates tend towards zero, house prices could tend towards the stratosphere as people can afford to service larger and larger mortgages.

God help them if the process reverses and intrest rates rise. An increase of one percentage point, from 1% to 2%, is a 100% increase or a doubling of the interest rate.

Well no, theoretically (if retail rates never go negative) the limit is the affordability on a 30 year payback. If they start upping the time limit or have negative retail rates though it could absolutely be stratospheric.

Multi-generational 100-year mortgages, anyone?

Bit of a problem when many of the Auckland houses are good for 30 years max and then need a wrecking ball put through them before they fall down in a rotten pile of sticks.

50 year mortgages are an option in the UK and Europe. They are feasible only when interest rates are low, which is what we have now.

Sure as eggs some bank "intellectuals" here will roll out ever longer terms to make houses more affordable while holding price growth up. The day of reckoning can thus be put off until it is somebody else's watch.

How much of this increase is just pent up demand from the huge drop in lending during lockdown? We have seen this recently with the sugar rush to people's credit card balances; it would be naive to think it wouldn't occur with other (housing) credit expansion.

https://tradingeconomics.com/new-zealand/credit-card-spending

"High LVR new mortgage commitments to investors more than doubled in July compared with June 2020."

Ohhh dear....

The Govt, RBNZ and retail banks are now not even hiding the fact they want the housing market to continue up into the stratosphere. I for one am worried about what happens in the future. Anyone have a crystal ball?

As previously posted I find the numbers of different mortgages more telling - in terms of amount loaned is less reliable as prices are not consistent, and percent of different borrowers is less telling as activity of different groups changes (e.g. affordability for FHB, market outlook for investors).

Looking at numbers of borrowers there are two very significant features in the data.

Firstly, the number of FHB at 2,960 is the highest on record since data was first collected in August 2014. Clearly FHB are finding that falling interest rates have improved affordability - the number of mortgages at 2.960 suggest that the number of individuals becoming FHB was likely over 8,000 in July.

Secondly, investors are more active with 4,324 mortgages taken out by investors. That is up from 2,285 in May and 3,169 in June. Investors who are in the market for investment reasons are generally both experienced regarding the market and astute as to the likely direction of it - clearly there are more investors feeling that there is upside to the market. I have posted numerous times that investor activity is probably one of the best indicators as to the future direction of the market.

So for those who not only have an opinion as to the market's future, but also prepared to back this up with their money are seemingly believing there is an upside to the market.

To those on this site who continue to preach doom and gloom regarding the market and especially regarding FHB - well your anonymous unsubstantiated comments are not being borne out.

That's a very myopic view you have there P8; what does the long term (12 month) trend suggest investors have been doing? It's going to take a lot more than one month's data to generate any conclusions regarding what investors are doing but then that wouldn't suit your narrative would it?

Albert

Just keep watching that data.

Monthly investor numbers equal to May 2018 but last significantly higher in 2016. Numbers are up three months in a row. Check Column W - "Total Borrowers E4 Investors".

So an upturn - but a notable and significant one. Its like a Saturday night party when at university - look for the early signs of a likely great party. If you wait until you hear that its a great party, then you are too late.

Yes, but April and May figures were significantly lower this year (due to lockdown) compared to previous years hence its no surprise there is "catch-up" in the following months post-lockdown. Once again, you're just massaging the numbers to suit your narrative.

Hasn't anyone told you its creepy when middle/older aged men continue to turn up to Uni parties?

Albert

Thing about dementia is that one retains long term memory. Those uni parties just seem like they were yesterday.

Note this older gentleman (women I know say not "creepy" though) is now home on late nights by 9.30pm so no risk of catching me at a good Uni party.

As house prices are up about 8% compared to a year ago it is not a big surprise that loans are too.

Around parts of the Wellingon region, i'm seeing it's more like 15-20% in a lot of cases, or higher.

Three years ago $750k would have got you a decent centrally located 3-4 bed villa in Welly, now the same houses are $1.25m+

I was looking 3 years ago and couldn't get a decent, centrally located 3-4 bed for $750k! More like $900k+. $750 was back in 2015/16. And now i'm seeing a lot of the nicer villa's in good locations going for more like $1.4mil+. On my street (spitting distance to the Botanical Gardens) a 4 bed/2 bath sold for 2.2mil end of 2019 and a 3 bed compact townhouse a few months ago for $1.34mil. BONKERS!!!!!!!!!

Tens of thousands of bureaucrats and hanger-ons (contractors) earning big dough.

Prices will go even higher when Wellington's Proposed District Plan is notified.

You can't lose in Wellington.

I don't think even a National led government would take to the ridiculously oversized bureaucracy there.

They never have, they just create a good wicket for contractors at twice the price.

Maybe my villa's were a bit more rustic!!! That is punchy though! Still, you can buy a nice place in Welly and a good bach in Coro for less than a place in Auckland, that always seemed better value.

Te Kooti, my villa was "rustic" when I bought it and its still a frickin building site over a year on but I wouldn't want to live in Auckland even if it was was the same price as Welly. I'd choose Napier, Havelock North, New Plymouth, the Tron, Cambridge, Nelson... almost anywhere remotely urban over Auckland. I don't like Auckland city center, it doesn't have soul and isn't very pretty compared to the rest of NZ, after that it's just suburbia stacked to infinity with a bunch of ugly congested roads linking it together.

Auckland's suburbs are much nicer than Wellington's. I say that as a born and bred Wellingtonian. Even my die hard Wellingtonian father says that. Auckland's climate is better too. And has an amazing marine and coastal environment. Also good access to the amazing Coromandel and Bay of Islands.

I also have to disagree a bit on the respective merits of the CBDs. Wellington's feels very 1990s in many places.

Depends what you consider a nice suburb or climate to be eh.

Do you *really* like Wellington's climate???

Summer is almost non existent, windy, several degrees colder than Auckland.

Each to their own...

Wellington is nice to visit for a pretentious hungover hipster weekend, but Auckland is a better lifestyle re climate and outdoor pursuits like you say.

Wellington is just full of people from Palmy, NP, Wairarapa and Napier that didn't leave after uni and got sucked into FIRE or gubmint!

Kapiti coast is nice though.

Must be because of the awesome weather. Nothing quite like an overcast windy wellington day. Yum.

Wellington does have poor weather, but it makes the place more interesting. I give you Brisbane, Florida and Gold Coast as warm yet cultureless hell holes as examples....

Auckland is too hot for me in summer. I would have to spend every day trying very hard not to sunburn! Plus it just takes so long to get from one place to another. I prefer Queenstown in winter to Auckland in summer. There are other places that are more beautiful than Wellington. I'm back to the West Coast again in September and it blows my mind how beautiful it is there. But Wellington has a great balance for me. I get to see the sun rise and set over the harbour and mountains every day but still have music venues, great arts culture, good restaurants, international airport etc. It just depends what floats your boat.

The use of FHB in statistics is becoming as bad as all the other junk statistics out there at the moment, being thrown around by Stats NZ etc.

This category technically also includes people that used to own property since there is no 'Second chance' buyer anymore, they just get assessed on whether they have property or not and then you're magically now a FHB.

The house price debate here in NZ is fascinating! Its the one topic that gets everyone engaged. NZ is overpriced for houses, and this will continue to get worse. Its unlikely that incomes will rise during covid, and its common knowledge that NZ's productivity levels have underperformed compared to peers for over 15 years! OCR rates will go below Zero soon and bank mortgage rates will drop to around 2%. Mortgage debt will boom and houses prices with it. Government's will continue to set policy that does NOT disrupt house values for 10 plus years! NZ's future will be massive house prices and modest (meaning low) incomes!

yeah ,not so long ago i would of disagreed ,i would argue logically this doesnt make sense, yet demand for housing and pricing continues to rise,im baffled.

I worry all it will do is widen the void between those with, and those without.

Election issue 2023. For now the pressure builds.

Panademic has been not deter but possible boosted housing market.

Biggest fear to any government is not fall of businesses but fall of housing market as is too BIG to fall and for the same reason government is going all out to support and promote housing market AND not businesses as only economy in NZ is housing.

Mortage holiday should be for people who have lost job or business but instead is been used by many to opt for for mortage holiday as an opprtunity to borrow more to speculate - courtsey Government.

LVR removed reasoon to protect housing market or to boost speculation.

As government knows that if housing markets fall - NZ is doomed so are reluctantly supporting businesses as are forced (so much pain and thinking in giving 4 days extra wage subsidy) But are proactive to support and promote.

Currently housing market is touching unseen new highs and now even JA must be thinking that housing problem is a good problem. All politicans when in power are......

If you’re on a mortgage holiday surely there is no way a bank would lend you a further loan to invest in another property

Record Mortage so where is the crisis :

https://i.stuff.co.nz/business/money/300091277/no-car-no-job-falling-be…

How is mortgage lending year to date 2020 compare to the same period last year- I can understand a peak in June & July post lockdown but what is the number for the year?

RBNZ C31 :

Jan to July 2020 = $35.5 Billion

Jan to July 2019 = $37.8 Billion

Lord have mercy on their souls

Congratulations to all the first home buyers

I am personally advising my friends that now is still a decent time to buy.

The fact is, once you have become a housing-secured debtor in New Zealand, you become a protected species. Every effort of government and central bank is dedicated to propping up the value of your asset.

Right or wrong, that's a damn good place to be. Consider the alternative - saving cash. Governments are hell bent on making this as unattractive as possible, they are actively destroying the value of your asset. I would MUCH rather be a young person now going into debt, than an oldie trying to squeeze returns out of a fixed capital base. I don't think house prices will do much in real terms over the next 20 years, but at least they will hold their value better than cash or financial assets.

Correct. Any government particularly in NZ will and have to do anything and everything to protect the housing as entire economy of NZ it seems is based/depends on housing.

Any fall or correction in housing market will lead to their downfall and politicans of all breed will do anything for power.

So yes mortage deferral and policies around housing market like LVR are to support and promote speculation. Low interest rate is suppose to help business and it does but like double edge sword it helps more to boost asset class.

Now housing economy is so big and important that government has no choice but to protect and one of the best way is mortage d efferal from 6 months to year to 2 year.....with low interest.

CHECK ALL MEASURES / STIMULUS THAT HAVE BEEN DONE BY GOVERNMENT / RESERVE BANK TO PROTECT BUSINESSES AND PROPERTY MARKET - WILL FIND MORE EMPHASIS IS ON TO PROTECT HOUSING MARKET AND EVEN POLICY TARGETED FOR BUSINESS ARE ACTUALLY MEANT TO BOOST HOUSING IN GUISE OF STIMULUS TO BUSINESS.

No experts have asked :

If have stimulus of mortage holiday till 31st March in panademic to protect housing market WHY not have stimulus to protect Job till March end as that too will help business - if apply the same logic.

Yes, every setback (perceived or real) will be countered by another "kitchen sink" until the fiat currency system reaches breaking point.

Every policy will be on the table in the coming decade.

Correct, this is a key point. Unfortunately the individuals prosperity in NZ is totally linked to house ownership. Presently governments on any side will not touch any policy that is negative to house values. Both governments also know they can set immigration policy to protect house values at any time! or increase house values! think about this, NZ is seeing the almost total destruction of the tourism industry (I think around $10bil plus in revenues) massive destruction of SME's, hospitality right now, and houses keep going up! Printing cash to prop up the sharemarket and houses is creating a growing divide! Based on this NZ's future looks like a place for the wealthy to store money in houses, and live here when retired. Forget business!

Just highlights that those folk invested it should never be putting the boot into other welfare beneficiaries, for the others have received far less in welfare from government.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.