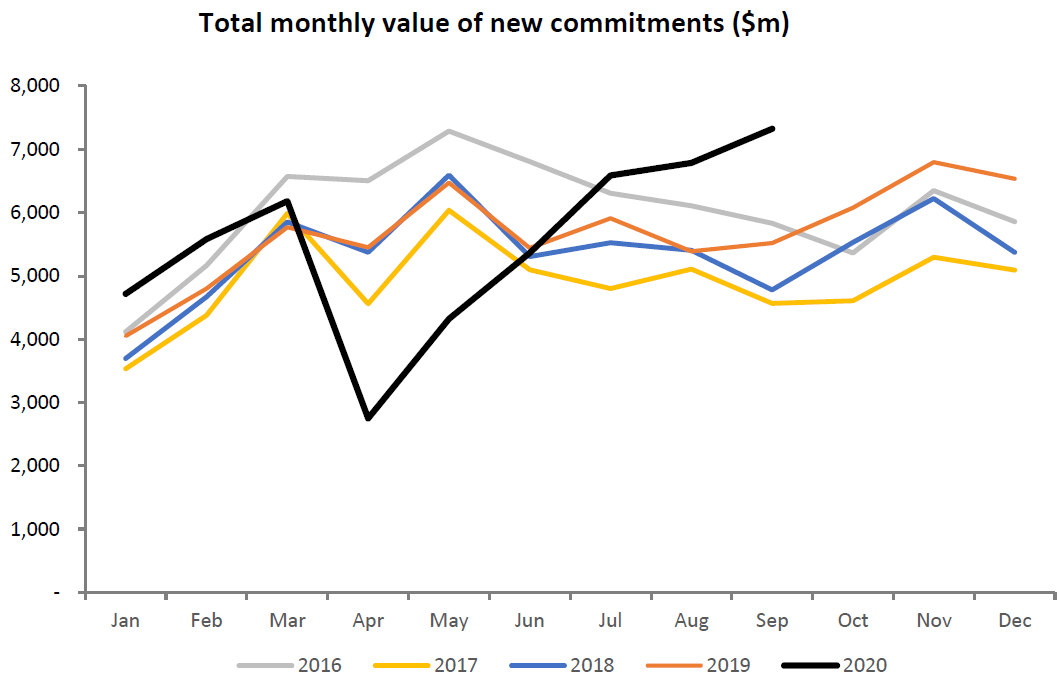

Mortgage lending hit a record high of over $7.3 billion in September.

According to the latest Reserve Bank residential mortgage lending by borrower type figures the September lending was the most since the RBNZ started compiling this monthly data in 2013.

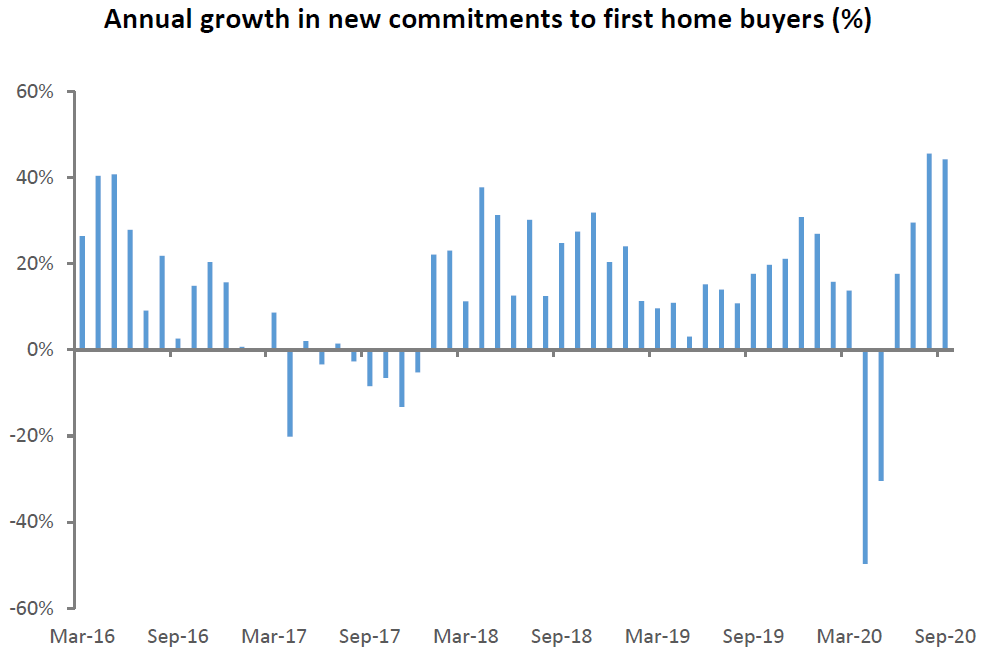

First home buyers again borrowed a new record high amount of just under $1.4 billion, however their share of the overall amount borrowed is starting to decline and at 19% it was down from 19.8% in August.

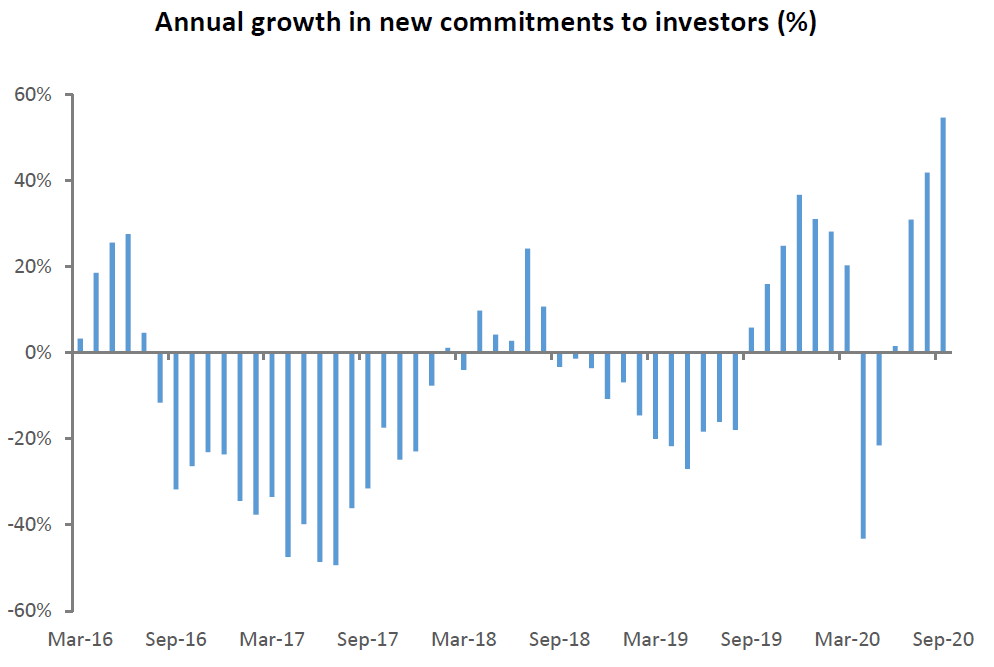

The buyers on the march now are the investors. They borrowed nearly $1.7 billion in September, for a 22.7% share of the mortgage market, up from 21.4% the previous month.

And they are borrowing bigger amounts.

The amount of high loan to value ratio (LVR) borrowing, which for investors is above 70% of the value of the property, was $611 million in September, up from $491 million in August.

The amount of high LVR money borrowed by investors has effectively tripled since June, when it was $204 million.

The RBNZ lifted LVR restrictions, which had been in place in some form since 2013, in May, with the intent that they be removed for at least 12 months. However last week RBNZ Governor Adrian Orr said that the central bank was "looking at" the possibility of reinstating them.

On the question of the recent upsurge in activity in the housing market, Orr said last week: "When will it worry us? When we are seeing it being driven by very high leverage loans and when we are seeing it being driven by investors rather than households and that is where our tools are marketed.

"What are we seeing at the moment? - Early signs of exactly both of those.

"We are starting to see the new lending going back into the 70%-80% loan to value ratios and the investor side."

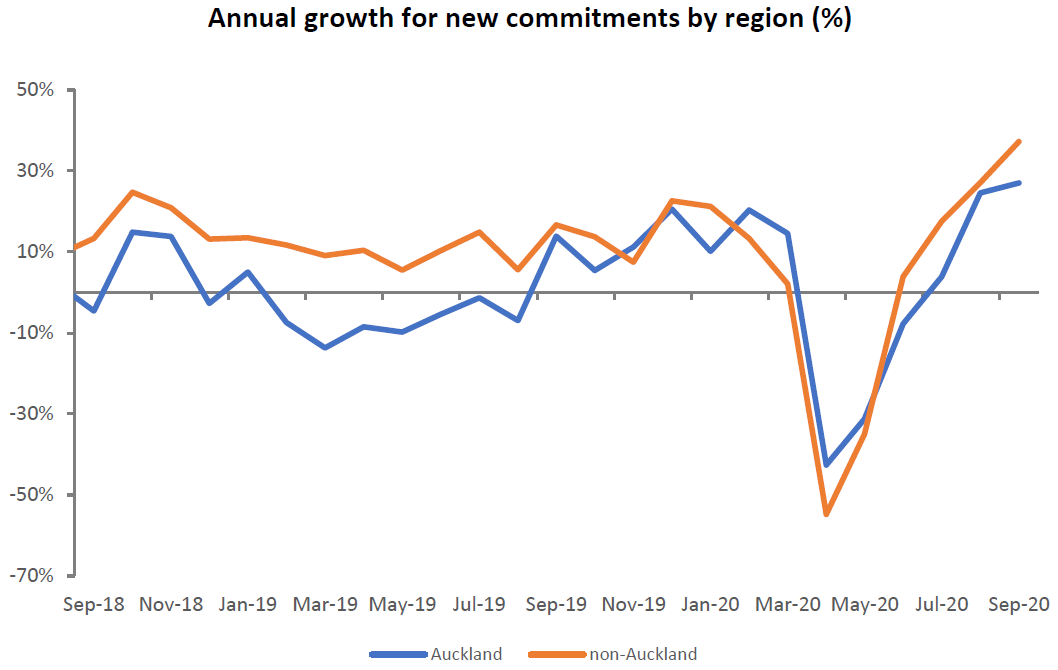

Much of the latest heat in the market is being generated in the regions, rather than Auckland, with annual rates of lending in the rest of NZ increasing at a faster rate than those in Auckland.

The Reserve Bank supplied the following key facts:

- Total monthly new mortgage commitments were $7.3 billion in September – the highest month on record since the survey began in 2013. This is an increase of $0.5 billion (7.9%) from August 2020 and 32.8% from September 2019.

- New mortgage commitments to first home buyers were $1.4 billion in September, up from $1.3 billion in August while other owner occupiers increased from $3.9 billion in August to $4.2 billion in September.

- First home buyers accounted for 19.1% of new mortgage commitments in September, down from 19.8% in August while share of new commitments to investors rose from 21.4% to 22.7%.

- The nationwide year-on-year growth in value of new mortgage commitments to first home buyers was 44.3%, while new commitments to investors was up 54.7%.

- The year-on-year increase of 32.8% in new mortgage commitments was largely driven by regions outside of Auckland. The annual growth rate for new mortgage commitments in ‘non- Auckland’ increased from 27.1% in August to 37.2% in September, while rising from 24.5% to 27.0% in Auckland.

- Monthly new mortgage commitments with high loan-to-valuation ratio have increased since the restrictions were removed in May 2020. High LVR new mortgage commitments to investors saw an increase of 24.3% in September, up from 10.3% in August.

55 Comments

Annnnd the transfer of wealth to the older generations continues...

Looks like the return of Inheritance Tax and Gift tax then.

Annoying things to have to spend the time circumventing, but needs must....

On the other hand, I believe CGT brought back wouldn't be a 'new' tax as its still on the books but currently rated at 0% at the moment.

But somethings going to have to give.

Where is CGT at a rate of 0% in the Income Tax Act?

Please advise

skip

Re: “Transfer of wealth”??? Another example of baseless moaning.

Try reading the data.

For the month 3023 mortgages (5,000+ people) went to FHB - the highest number since RBNZ data produced in 2014 and twice the number of FHB as then.

Interest.co article today highlights improved affordability.

Whether one thinks it is a good to buy or not, FHB are the most active they have been for the past six years.

Great to see those 5,000 FHB with initiative and commitment now in homes and as long as they are prudent in paying the mortgage down they have little to fear from short term fluctuations in the market.

Those potential FHB who have either lacked initiative and commitment or balls or waiting for the bubble burst - and especially those who have done so the last three to well over the past ten years - are just seeing prices just get that much more expensive.

And despite the moaning and denials; homeownership has always involved making a commitment and sacrifice.

The reality is that those six months ago who were calling 50% and more drop have been proved wrong. And for those who are still calling bubble burst . . . there are those who claim (facetiously) that RBNZ wont let that happen and for financial stability they could be right given RBNZ comments and actions.

By 'initiative and commitment' read: 'money, probably mostly their parents' money'.

I think you are missing the point. Where is that money that FHBs are paying for their new house, going? It is often going to older people who are selling up and possibly moving into rest homes. So the older people are making all the money in that case.

The word 'affordability' is a red herring IMO. They are only 'affordable' at the current inflated prices due to the historic low interest rates, due to both a health and financial crisis, and the moves to try and help with this. The byproduct is inflating asset prices even more. The problem is the actual 'price' people are paying, especially when compared to the average wage. We need to bring in loan to earnings ratios. Most peoples houses at the moment are earning via capital gains as much as someone who is working full time. That isn't sustainable and is a big problem.

The problem is the actual 'price' people are paying, especially when compared to the average wage.

Income and 'cost of credit' is an interesting relationship. If incomes are flat or falling, a lower cost of credit is welcome. When the cost of credit can't go much lower, that's when all the shenanigans start happening.

Yeap. Negative interest rates are something I never thought I would see in NZ. And then we get all the new terms that most people have never heard of, like FLP , Funding for Lending. It is madness.

IMO, the banks should be forced to bring in Loan to income restrictions. But it won't happen, because they then probably would be able to lend very little.

Your example of 5000 FHBers exactly proves the point.

It may be you are confusing "transfer of wealth" (which the sellers are getting as they almost certainly paid less for it) with "transfer of debt" (which the FHBers are getting as they are almost certainly committing to a higher ratio of their income than any other generation)

I reckon my kids could be looking at paying 10-15 million dollars for a one bedroom townhouse with an average salary of $100-$150k at this rate.

I look forward to lecturing them that despite their moaning and denials, homeownership has always involved commitment and sacrifice.

Patience there champ, the movie hasn't ended yet and these central bankers will drive the entire system off a cliff before then. Even geriatric geezers should live long enough to see it.

Good on them. They worked hard.

If the young are greater fools to pay up I would take their money too.

The housing ponzi only keeps going as a greater fool is shouting a higher number each time.

Rather callous to simply call them fools. Young people are seeing their hope of home ownership slipping further and further out of reach, with the powers that be doing everything they can to support this and avoid addressing it. They must feel potentially damned if they do and yet almost certainly damned if they don't. I hardly think they are being foolish in the true sense.

The best and brightest will leave and third worlders will be imported to replace them. New Zealand is a basket case and it's not going to get better.

Our people and our economy are being systematically hollowed out. The only game in town is predatory property speculation.

Where our country is going to end up over the next decade or two is horrifying to contemplate.

Could not agree more. I wish more than just a few people were willing to exercise their right to protest here. We're just going to watch this happen instead.

Quiet Desperation: Perhaps educate yourself here and stop being so sensitive: https://www.investopedia.com/terms/g/greaterfooltheory.asp

The greater fool theory states that it is possible to make money by buying securities, whether or not they are overvalued, by selling them for a profit at a later date. This is because there will always be someone (i.e. a bigger or greater fool) who is willing to pay a higher price.

until there isn't - pop!

Of course. You clearly only meant to refer to a theory, nothing denigrating in your comment at all..

You are obviously part of woke movement.

Go and have a hug. Be kind.

They are fools if they buying up with less than 20% equity and bidding up houses due to FOMO.

If they cant pay in the future the principal on there over priced run downs houses dont expect to be bailed out.

Take their medicine and let the friendly bank sell there houses.

Sick of the I want it now generation and the woke telling you what to say like yourself. They need to work harder and save more. Less credit spending on the latest Iphone, car, handbag and 8k TV. So my message to you and others is harden up we are in for a rough ride! I genuinely hope we get a good unemployment scare and the 20% decrease in houses resulting from it.

And you call me sensitive? Get over yourself. For many of these 'fools', if they sit this out and don't take their chances now, they run the very real risk of never being able to afford their own home and instead, find themselves stuck paying ever increasing rent. That 20% they keep saving for just grows further and further out of reach. There are plenty of potential FHB out there not spending money on any of those things and have zero family support. I'm sick of the older generations that think younger people just need to harden up. You don't like being told what to say? Yet you sure love to judge and criticize everything outside your own experience - without the intelligence or wisdom to understand and empathize with the situation that other people are in.

Funny thing is buddy I am young not from an older generation as you have wrongly assumed. So the message is coming from their own age group. But I have I worked very hard. So much so I stopped working 3 years ago in Dec. Nothing from the bank of Mum and Dad. Nothing inherited. Nothing from tax free capital gains in property. Tax paid on all my wealth.

They all need to learn personal responsibility. Get a second job on Saturdays and Sundays and at night if a house is so important. That is what hardening up is about.

If I ran through the expenditure of all the moaners you will find plenty of non conservative expenditure. They all need to learn to cut their lunch, cook their dinners and have a tight budget and they can get there. Spend on nothing else other than food and power and rent. In 10 years time you will surprised at what savings can grow to if they educate themselves on investing and compound growth. Problem is the young want it now....

Thinking I have to buy now or I will miss out is what is driving the market. Its classic greater fools theory.

Get a second job on Saturdays and Sundays and at night if a house is so important.

And this is the country we have become and accepted. Maybe in a decade we will sub in "drinking water" for "house".

"older generations"

The boomers ..... yeah nah, gen x (I am one) are aged 40 to 55 and millennials 25 to 40 or so. Many of them are homeowners too don't forget. So no need to be ageist Skippy and sorry to hear that you're not a homeowner (yet)

Many Gen X won the birth lottery...twice. Once with their own capital gain on property and again when they inherit(ed) their parents capital gain. Even a chimp born into a middle class family between 1960 and 1970 should now be extremely wealthy. Absolutely nothing to be proud of.

Chimps are wimps but you should be so pleased.

Hats off to the RBNZ...

Some heads need to roll off the back of this.

Our Government and its arms whether the RBNZ or ComCom and Government Departments never has a post mortem of decisions.

Skeletons are buried with an announcement of a reset. Reset means policy failed and wont be talked about after today and targets proposed will be said in the same press conference as an aspiration.

It's like the Chinese buffet or smorgasbord when the plump people start rocking up in greater numbers. More food being consumed (4th and even 5th helpings) is going out meaning that profits are lower. Drop the cost for the punters and it gets even more difficult.

Meaningless without digging behind the headline: download the C31 workbook, add a column dividing total borrowed (B) by total borrowers (T), adjust for the 10^6 scaling, and discover this:

- 2014 August borrowing averaged $172,275

- 2020 September borrowing averaged $286,918

Factor in Interest rates for those periods, and the conclusion hasta be: Doom Averted?

Try it for 2017 - how much of the increase occurred between 2014-2017 and 2017-2020

....or simply, delayed.

With having interests of how business lending performs for these two years, I've found some Sector lending statics on RBNZ website:

https://www.rbnz.govt.nz/statistics/c5

Business lending and personal consumer lending started to decline from Apr 2020. Business lending annual growth rate is -0.5 and personal consumer annual growth rate is -11.5. This clearly indicated that lowering OCR is not working to improve our economy performance.

Total monthly new mortgage commitments were $7.3 billion in September

The government raised net new deposits of $7.8bn in the same period - probably to finance consumption via transfer payments.

Can anyone confirm there was a combined equal injection of investment credit for the creation of new goods and services or productivity gains that generate income?

I guess not.

Well done Adrian for using all your ammo to continue to push our country towards further inequality, increase risk in the financial system and encourage further investment in this non-productive asset class. All I can think of in Auckland is investors saying ‘mine mine mine’

The problem will be if the bubble bursts and house prices drop. Investments don't always go up. Some people may have paid too much.

The problem will be if the bubble bursts and house prices drop. Investments don't always go up. Some people may have paid too much

Yes, but the implicit story being sent to the sheeple is that the ruling elite is omnipotent so there is nothing to fear.

On a long enough timeline this happening is an absolute certainty. Without the mortgage holidays and ignoring the rules it would have already happened.

I guess it just goes to show that debt holders are the protected class in this country.

No the lockout affected workers AND business people. But the wage subsidy did not indemnify business owners who are also debt holders, for their losses. Debt holders of all kinds have lost money based on a govt decision to lockdown

Bring back LVRs urgently. They should be adapting to the current situation, not trying to justify why they are still in place IMO. As houses are seen as the only alternative form of investment in NZ, it is no wonder people are in rushing to buy houses due to FOMO.

It will all likely end in tears.

I would like to see it trialed on investors only first, or restrictions placed on investors similar to foreign buyers, e.g. they can only invest in new builds at high LVRs. Give FHBs a chance to buy their 1920s shack without investors bidding the price through the roof only to rent it back to them.

Agree. 10% LVR on first home, 50% on second, 100% on 3+

Is anyone surprised by the correlation of more borrowing and higher house prices?

It seems only Mr Orr couldn't see that coming

It needs a lot more than that - this has to be stopped dead in its tracks

Except I understand they are wanting house prices to increase, because they think it simulates spending amongst house who own a house, as people feel richer. I guess it also means people can borrow more against the house, if it is worth more.

I dare say the current "mini-boom" hasn't run full course yet.

On the back of Covid-19, NZ has become very much a preferred country to live in.......

We're truly on the world-stage - thanks to Jacinda and out very competent public health scientists.

TTP

On the back of Covid-19, NZ has become very much a preferred country to live in.......

Wow.

With the world over publicity of how we are essentially Covid-19 free and how we are one of the best places to live in the world, can you imagine the immigration stats as soon as we open the boarders ? You ain't seen nothing yet in terms of house price increases. Plenty of multi-millionaires looking for a safe house. House prices doubling in the next 10 years is back on, local wages are irrelevant if your again competing with international money and it will happen because we "Have to keep moving".

The PR lady makes some good PR.

Anybody who wants to live in New Zealand hasn't actually lived in New Zealand.

Free social welfare money, free kainga ora houses to live in, free primary and secondary education, free pension money after ten years. when you are on the money wheel no one asks any questions. NZ is a dream come true for immigrants. I could also add beautiful and peaceful, but we all already know that

Hi TTP

Well spoken, oops written... there is now a call to reopen the borders to international tourists with/without quarantine. The govt is worried that when the tourists arrive so will the immigrants. In the year to March there was net migration of 90,000 .. didnt this govt just 3 years ago 'promise' us lower immigration...

Not surprised by any of this

There has been a sense of frenzy erupting around here and in the NZ Herald and its Oneroof and the Barfoot and Thompson auctions and news of queues 50 long attending open homes

The amount of high LVR money borrowed by investors has effectively tripled since June, when it was $204 million.

Need say more..

Prices were firm after lockdown and it was fron June that the craziness started so......

I wonder if part of the problem is FOMO, and the lack of stock over winter. Add in those young people who now can't go overseas, and need to buy something instead. I wonder how it will pan out over Summer as more housing stock comes online. Also from what I have read, there could potentially be between 100,000-200,000 empty houses in NZ. So I am not sure we don't have enough houses already. Just that some people are sitting on them empty, possibly for for tax free capital gains. They can make more money than working, with the cheap money investors can now buy. Empty houses IMO should be taxed an empty house tax.

Lol since when is 30% deposit "high LVR"? If RBNZ increases the investor LVR to 40% of the value at some point then get rid of it, would the definition of "high LVR" to you be any lending with less than 60% deposit on a property? You can then push "the amount of high LVR money borrowed by investors" have quintupled and we must knee-jerk react now before the sky falls :P

Presumably that is also what Orr wanted in stupidly removing the LVR limits

There is no doubt that the Elites who are implementing these (crazy) monetary policies designed to push up asset prices and debts know it better than anyone else that this is NOT sustainable.

Are they betting there will be huge debt forgiveness or UBI at the end of the game? I think they are!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.