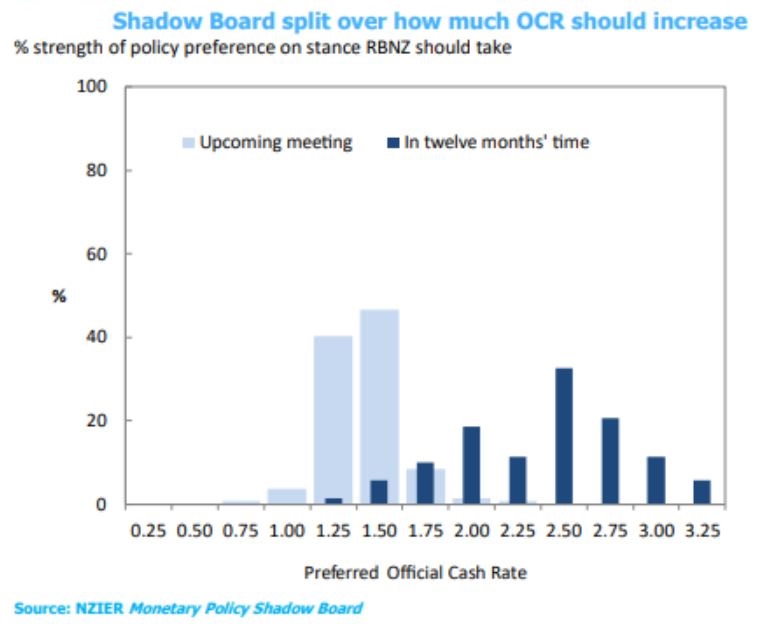

Members of the New Zealand Institute of Economic Research's Shadow Board agree the Reserve Bank should increase the Official Cash Rate (OCR) at Wednesday's review, but are divided over how big the increase should be.

The Shadow Board is sharply divided, the New Zealand Institute of Economic Research (NZIER) notes, with views split over whether the OCR should be increased by 25 or 50 basis points.

"The surge in inflation pressures has led to growing calls for the Reserve Bank to undertake monetary policy tightening at a more aggressive pace to rein in these inflation pressures. While supply-side constraints are driving much of the increase in inflation in the New Zealand economy, the recent rise in longer-term inflation expectations raises the risk of a wage-price spiral developing," NZIER says.

"However, some Shadow Board members called for caution in the pace of interest rate increases over the coming year. The recent weakening in business and consumer confidence due to uncertainty stemming from the spread of the more transmissible Omicron variant of Covid-19 and the war in Ukraine were provided as reasons for a more measured pace of monetary tightening."

"Beyond the April meeting, there is a wide range of views amongst the Shadow Board on where the OCR should end up in twelve months’ time. Shadow Board members highlighted the balance between the need to rein in inflation pressures against the extent to which the New Zealand economy will slow in response to interest rates increases and the heightened uncertainty over the global growth outlook," NZIER says.

The OCR is currently at 1% having been increased by 25 basis points at three consecutive OCR reviews since October. See our full OCR review preview here.

In terms of differing views from the Shadow Board, here are two of them.

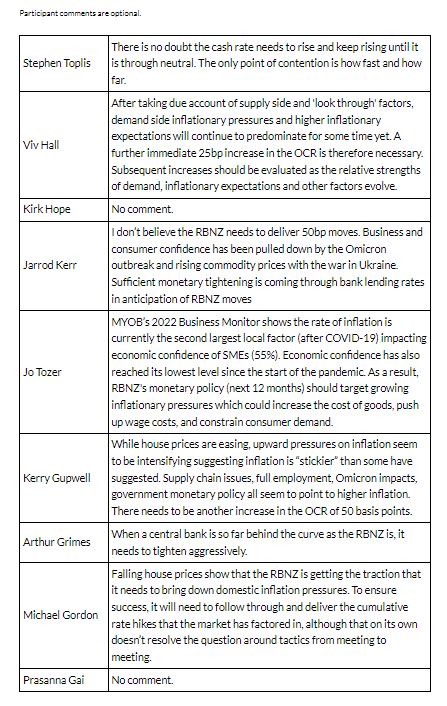

Firstly, Kiwibank Chief Economist Jarrod Kerr.

"I don’t believe the Reserve Bank needs to deliver 50 basis points moves. Business and consumer confidence has been pulled down by the Omicron outbreak and rising commodity prices with the war in Ukraine. Sufficient monetary tightening is coming through bank lending rates in anticipation of Reserve Bank moves," Kerr says.

And here's Arthur Grimes, Senior Fellow at Motu Research, Professor in the Chair of Wellbeing and Public Policy at Victoria University of Wellington’s School of Government, and a former Reserve Bank Chairman.

"When a central bank is so far behind the curve as the RBNZ is, it needs to tighten aggressively," says Grimes.

Below is a compilation of comments from members of the Shadow Board.

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank. Views expressed by the individuals who make up the Board are their own, and not necessarily those of the organisations they work for or with. Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision.

NZIER says the Shadow Board was established with the aim of encouraging informed debate on each interest rate decision, helping inform how a board structure might operate, and exploring how board members may use probabilities to express uncertainty.

100 Comments

25 is the safe call. 50 is the bold move. Grimes is right, we've fallen so far behind that in terms of monetary policy, we have to be bold and catch up. If that triggers a political flow-on effect, then the politicians who are elected to manage the country will need to do their jobs. That isn't RBNZs' problem. The Omicron peak is passing and a short sharp increase now may also buy us some NZD movement to help curb imported inflation in the short term.

50 is the safe call.

25 or 0 is the bold move.

Tip toe thru the tulips

Many are anticipating overseas trips, once the door opens money will flow out and we might see a big slow down domestically.

Probably by nothing, inflation is supply driven.

Treating it like demand driven inflation will just put more pressure on households that are already highly leveraged or unlikely to get access to a home. We need to fight inflation where it matters, in the supply chain, not punishing consumers who are already being hit by huge inflation.

If this logic is sensible, then why did we reward consumers with lower interest rates when inflation was falling? (i.e. goods are getting cheaper, so here have some more cheap money to throw around).

You can't have it one way, then not in the other.

Globalisation > cheap imports > deflationary > lower CPI > decrease OCR to zero > create debt/asset bubbles.

Now we have decided that the above sequence of events is only true when it means that debt servicing gets easier - but if we have supply chain issues, that you don't raise rates....why the hell would you drop rates than to prevent the deflation caused by good supply chains? Either than or the last 20-30 years of dropping the OCR to zero was some what fraudulent as we used the benefits of external supply chains to enrich asset owners over our younger people and the future prosperity of our people.

If central banks don't raise rates, and the inflation doesn't go away, they are going to look like much bigger fools than they already are for creating this mess in the first place.

I agree 100%. Not raising interest rates, and aggressively, willy structurally and deeply damage the NZ economy in the longer term. Interest rates must be normalized with the maximum urgency. The OCR should have been at least 3% by now. The longer we wait to normalize rates, the higher they will have to go later on. There is no free lunch and it is time to pay the piper.

Rates were dropped to make up for the fall in wages that came with those cheaper imports. Over the last few decades, we fell behind much of the OECD on R&D investments, shipped away our productive industries to cheaper locations, lost innovative enterprises to foreign ownership, and replaced that void with hospitality and tourism.

I have had one Post deleted today. I trust this platform will stay independent and not delete this Special Report from Sky news.

It wasn't sensible before either, you were wrongly assuming that.

However, current rates are in line with most of countries we like comparing ourselves with if not higher so increasing them even further will be shooting ourselves on the foot since will do nothing to control inflation and will have negative effects for consumption.

It's a valid point that our OCR is much higher than most other western nations that we compare ourselves to or have similar attributes.

Back in my original home country, there is a thing called usury rate, which officially set the legal maximum lending rate for a bank, for different kind of loans and maturities.

it is currently set at 2.51% for rates below 10 years.

I guess you’d have to pardon my French in a modern country as NZ to use an old word like “usury”. I wonder sometimes if the way to say it here is landlord…

Am I reading the graph right that there is some support for no increase and tiny support for a small cut?

Yip, outweighed by 75 and 100 bps respectively. Looks like about a 60:40 split in favour of =>50 bps.

I noticed that too... which one thinks there will be a cut??

Treasury yields follow nominal GDP growth. The latter is going to be phenomenal due to the high inflation created by the central banks in 2020. So it was obvious that yields would eventually shoot up / bond prices crash.

See Interest rates and growth:

https://www.sciencedirect.com/science/article/pii/S0921800916307510

NZ's OCR change will not have an impact on the part of inflation created by the US. Much of inflation in NZ has been created by inflation-promoting policies by Labour.

Demand is already dropping because of low confidence, higher prices for imported non-substitutables like oil, and higher mortgage costs. Hiking rates will increase the cost of living, reduce demand further, increase unemployment, and do next to nothing about prices. My personal view is that anyone shouting for higher rates has an austerity fetish.

My view that anyone shouting for lower rates the last 10 years has a vested interest in creating wealth inequality and enriching themselves at the expense of others via central bank and government backed debt bubbles. We dropped interest rates to zero using cheap imported goods....now the imports aren't so cheap we can't maintain that broken philosophy and people might start panicking.

The best thing (from a long term utilitarian view (in my perspective)) that could happen is for the current system to implode and reset.

Its like keeping the sick relative in their 90's who wants to die, alive, via life support. Its just painful for everyone.

The current system imploding is fine and all but without new options for government we will end up in the same position again.

I agree, i dont think we have the competence for a proper reset.

We have stolen so much energy from the future via debt that is unrepayable when it all implodes the only play in the book is (you guessed it) bail outs, massive QE that will dwarf anything before it, the poor will lose everything and bank executives will make 7 figure bonuses...

It's a massive welfare state for older asset speculators, essentially. Living off the wealth of other generations.

As things stand, we have a large cohort sitting on billions of dollars of unearned housing gains.

They are competing for resources with those who have to actually work for their money.

High rates would destroy nominal housing wealth, reducing the ability of rentiers to out-compete workers and lowering prices (lowering inflation!)

Unemployment is the unfortunate by-product, yes; but there's at least the hope that with less capital directed into speculative activity, real growth will return.

My personal view is that anyone shouting to keep rates low desires a feudalistic state where real wealth is only ever inherited.

Whether rates are high or low, the fruits of renters' labour flows to rentiers. That is a design feature of our economic system - value is extracted from our natural and human resources for the benefit of those with power and money.

High rates may lead to some housing price corrections (and good!) but they also protect the huge financial wealth of the top few per cent of NZ society. High rates benefit those with wealth, low rates benefit those with debt.

"low rates benefit those with debt".....so why do we keep pandering to them?

Our crazy high debt levels are the problem....not the solution to our problem...

Yet we have central bankers saying to avoid deflation and a possible depression we need banks to LEND, LEND, LEND.....then 6 months later say, oh we are worried that FHB's might find themselves in negative equity if the market turns.

We are living in a period of economic/financial insanity, but we won't be able to grasp the severity of it until the dust settles on the other side....

Are we talking about the same country?

The financial wealth of the top 10% in this country is housing.

Low rates benefit those with debt = yes, and who has debt? Property owners. The poor have small debts, payday and car loans. They don't get mortgages. The bulk of it is owed by the same people who have extracted the wealth. Low rates have allowed them to turn debt into nominal wealth! (Which they eventually want to exchange for real goods and services, hence inflation...)

I feel like you're applying a mental model that fits other countries, where wealth is ownership of companies and the like. Here, wealth is the ownership of real estate which you have acquired by leveraging collateral in existing real estate, enabled by cheap debt.

Thankfully, we have statistics that prevent us needing to reach for the reckons.

The top 20% of households by wealth in NZ have average financial assets of around $2m and housing assets of about $1m. So, around two-thirds of their wealth is financial. The wealthiest 20% have an average debt of just $176,000. So, tell me, are higher rates good or bad for the most wealthy?

The lowest 20% of households have on average $75,000 of assets and $81,000 of debt. So, again, tell me who high rates benefit?

A good riposte. I'd like to see more detail on those figures though.

eg: that lowest 20%; are they mostly <30s with few assets and large student loans (not sensitive to rate hikes)?

That $2m of financial assets owned by the average 20%er: what percentage of those are financialised real estate assets?

The household net worth statistics are, I am pretty sure, based on the Household Economic Survey... in which case "the equity in property held by trusts is allocated to the settlors and quasi-settlors (settlors who are also beneficiaries) and reflected in the individual/household asset and liabilities (i.e. in the real estate line not the financial asset line)". My take is that the big money is in pension funds, shares, bonds, etc.

The data is here: https://www.stats.govt.nz/information-releases/household-net-worth-stat…

Max Rushbrooke literally wrote the book on analysis of NZ wealth - well worth a read. He was able to get data that you can't get online.

My personal view is that anyone shouting for higher rates has an austerity fetish. Indeed:

It’s the greed of the financial sector, basically, and the takeover of the government by the financial sector here as happened under Margaret Thatcher in England and then Tony Blair. You’ve had both countries essentially enter permanent austerity programs, and the only way to cure his is for housing prices to go down. But if the housing prices go down, then the banks will go broke. Link

How else, other than austerity programs, can the government begin to address this consequential national debt debacle?

I don't know, maybe an actual economic / industrial strategy? In the current global climate, and the very different climate that is coming, we need an even balance of trade coupled with energy & food security.

I don't know

Same here - but this poignant and currently relevant article makes the point.

But you are right to point out the need to increase the tax base with productive capacity to overcome infrastructure deprecation caused by austerity.

Low consumer confidence doesn't necessarily mean demand is dropping. Low consumer confidence can be caused by inflation as price and business cost are going up.

Economic reality is exactly the opposite of what you are saying. Hiking rates will not increase the cost of living, but it is actually keeping rates too low for too long that has been one of the major contributor to the rising of inflation. Rates must be hiked aggressively right now, before it is too late, if we want to have any hope to keep the cost of future living increases to a manageable level.

The claim that inflation is due purely, or mostly, to imported non-substitutables like oil is deeply and factually incorrect: actual data clearly shows that NZ has had for quite some time a big problem of non-tradeable, locally-generated inflation caused by a ultra-loose monetary policy that has structurally damaged the NZ economy, productivity. financial stability and competitiveness.

Hiking rates increases mortgage costs, increases the cost of doing business (putting pressure on prices), puts pressure on rents (or allows landlords to justify increases), pushes up futures prices, and increases unemployment. This is literally what hiking rates are INTENDED to do - they allegedly work by reducing demand. The problem comes when price increases are not caused primarily by excess demand - i.e. too much money chasing too few goods. In this scenario, hiking rates protects financial wealth at the expense of those on the edge of the labour market.

I am not claiming that inflation is all offshore - but have another look at tradeable vs non-tradeable inflation and wage growth. What you will see is that our domestic inflation has been tracking just below wage growth, rent levels etc and most of us in NZ have been increasing our standard of living a bit by relying on imported goods that have been falling in value in real terms. Those goods are now getting more expensive. It's a reckoning.

A failed economy caused that, not hiking rates. When you have a strong and healthy economy, hiking rates are actually good.

Inflation was rising before the local Omicron outbreak and before Ukraine was invaded. But down the memory hole that little detail goes, because we want to believe it's all contingent rather than baked in to the insane economic situation we've allowed to develop.

It was transitory then. This is just a second, separate transitory bit. There may be more transitory bits, but they're all independent and couldn't possibly represent a broader long-term trend that we'd have to admit to. Absolutely out of the question, apparently.

Does anyone know how many people are on their 'Shadow Board'?

I just went to the NZIER website and couldn't find info.

they all seem to have top jobs and well qualified backgrounds.would they exempt themselves if they had property investments?you would think anybody taking home mega salaries in NZ would have had property investment and corresponding large mortgages to mitigate the tax they pay.

Nine. They are listed in the article, with comments from each.

Oh ok, I thought they were only key ones invited to comment.

I don’t understand the graph,then, as it shows 1 or 2% of the shadow board wanting a decline to 0.75?

You obviously can’t have 1 or 2 % of 9 people.

or is something else happening in the survey? Like ranges of options

100 points !

.... do you want to eat a rat sandwich slowly , nibble at it .... or , chow that sucker down quickly ...

“The recent weakening in business and consumer confidence due to uncertainty stemming from the spread of the more transmissible Omicron variant of Covid-19 and the war in Ukraine were provided as reasons for a more measured pace of monetary tightening.”

Hmm, has any of them thought about Inflation could be one of the major factors that cause business and consumer confidence so low? I don't think you can have a strong consumer confidence when you have high inflation in the society, can you?

If you bring more transmissible Omicron variant and the war in Ukraine as excuses two month ago, it would be more persuasive, but if these can be an excuse, I guess we can include China's Omicron outbreak potentially causing recession as another excuses, there will be more excuses like these in future. In that case, why would we bother data and facts anymore? We just keep rates forever low so everyone can be happy, can we?

We used the CPI the last 30 years to show that we are very close to deflation so that we can drop rates each year, so that we can create more debt, so that asset owners become richer by applying lower and lower discount rates to the sum of future cash flows.

Now that the CPI is going in the other direction, we need to call that inflation 'transitory' because it would destroy that philosophy and the wealth of those who have received this paper wealth, not earned via incomes.

Central banks can't afford for this inflation to exist as it is their kryptonite....it exposes all of their weaknesses and the insanity of their monetary policy 2008- now. And they can't do anything if it doesn't go away....other than destroy the economy. They will look like fools if they don't act strongly enough, yet they will also look like fools if they don't do enough and it gets away on them.

Completely agreed, before covid hit us, I started doubting about whether Monetary Stimulus is actually effective to boost economy when it's close to a recession. We've had ultra loose monetary policy yet business for many years and consumer confidence stayed low most of time. The damage its causing to the economy had much larger impact.

If they hike OCR, housing market is at the risk of crashing to cause recession. If they don't, out of controlled inflation will crash the economy. We can recover from a housing market crash, it might take a bit time. But I am not so sure about whether we can recover from a hyperinflation.

1% at least... it will defend the currency somewhat, and with a current account deficit the last thing we need is a weakening currency. And then will someone please boot Orr into touch. His performance over the last couple of years can be compared to Gordon Brown selling the UK gold reserves to China at the bottom of the market

The OCR should be already at 3% right now, at the very least. The RBNZ is so behind the curve that it is not even funny.

.50 or 1 watch NZD tumble if they don’t comply to FED,s wishes this would also increase inflation as NZD loses value.

They should cut rates. It's the "path of least regrets."

Should the OCR be moved up to 2% or 3% on Wednesday ? That should be the Question.

Orr and his mates behind closed doors - If we sell the question of "Should it be 25bps or 50bps ? " then when we make it 50bps we will actually look proactive, responsible and diligent, we will gain trust and respect once again . Yeah great idea Adrian, Orr you are just too much, they will never suspect our negligence, in fact they will praise us on Wednesday.

25. Most of our inflation is from outside NZ. The only reason to make it 50 it to keep our dollar up.

But we'll end up doing whatever the IMF & World bank says we should do. It's out of our control.

25 or 50. Will it be a short term improvement, flat-lining or, a slight hiccup or something meaningful?

Will this ward off the external inflation factors? How?

Its going to be 25, anything more will scare the horses. Going forward its going to be 25 every 6 weeks so it will get there eventually.

Scare the houses...

Everything is nearly open, it's BAU written all over the wall.

Then why the emergency rate of 1 or 1.25?

If the deduction can be 0.75 then the raise should be at least 0.75 or 0.50.

If the raise will be again 0.25 this time it clearly means the decision-makers are either low on IQ or corrupt.

50

0.25

50 bp = RBNZ accepts that inflation is way out of range and is 'cautiously' trying to address it without bursting the housing bubble.

25 bp = RBNZ accepts that inflation is way out of range but is more concerned about another part of our 'economy', namely housing.

That is probably closer to the truth than most.

Why not.... 0.35%

too difficult the don't understand percentages

Can anyone explain to me in relative laymen terms how increasing the OCR is going to fix inflation in this country.

The way I see it inflation in this nation is mainly a supply issue driven to by overseas factors and government policy rather than too much demand.

Couple of examples which affect families the most.

1. Housing - supply issue. Increase the size of our population by 20% over the last 20 years and not build enough housing and infrastructure to support them - equals higher house prices due to lack of supply

- not train enough trades to build extra houses mean increase labour costs to build houses

- not enough competition in the building supplies industry means excessively high building material costs compared to over seas.

2. Food - supply issue. Most of our food actually comes from overseas now. 30 years of globalisation means we are no longer a country that feeds itself. But in the quest for better returns companies have offshored and overseas brands have bought local brand and then offshored them. So that means we are totally dependant on global markets for most of our food. Because of supply problems with COVID and War and we are seeing food prices go through the roof.

- on a local level climate change policy is also massively increase product costs for growers and farmers in New Zealand which means higher prices at the supermarket.

- again lack of competition is another issue, why Progressive Enterprises (Countdown) were allowed to buy up every super market chain not owned by Foodstuff is beyond me.

3. Fuel - supply issue . Government policy - no local oil drilling and closing down our only oil refinery has increased the prices we pay at the pump, especially diesel as most of our diesel come from Marsden Point. Also the governments intent to shutdown natural gas in this nation has also dramatically increase prices for it over the last 6 months of companies scramble to recover there investments

War - Russia supplied a substantial amount of the worlds energy, shutting (not debating the rights or wrongs of it) them off means decreasing supply which pushes up prices.

Housing, food and fuel are the 3 biggest expenses for families by fair. Increasing the OCR is not going to do anything to make any of this stuff go down in prices or even have any effect on the inflation of it.

You might argue increasing interest rates will cause housing prices to fall and therefore make them more affordable. I say no to that. First lets look at rent - rent is just going to go up as land lords look to cover the costs of higher interest rates, insurance and council rates. Because we have a supply problem, people can either pay or live in a tent, that is the choice they have. There is no alternative to find a landlord who charges less rent.

Buying a house - say you bought a house 700k and had a 600k mortgage, you fixed 6 months ago for 2.55% (for 1 year), you would be paying $2,387 a month for the mortgage. Now lets say house prices fall 15% and now the house is bought for 595k and they have a mortgage for 495k, but now there 1 year fixes term is 5.5%, now there mortgage is $2811. So again so we see interest rates increase has cause an increase in the cost of living.

So again I ask, how is increasing interest rates in this environment meant to lower inflation instead of feeding and throwing a large percentage of our population into poverty?

"Can anyone explain to me in relative laymen terms how increasing the OCR is going to fix inflation in this country"

In precisely the same manner that we decreased the OCR to zero in 2020 to avoid deflation.

Oh and a large percentage of our population are already living in poverty - talk to the people running the food banks......and the quantity of NZ'ers that required assistance on a weekly basis from the government in order to pay the rent and put food on the table.

The system is already broken - raising rates will simply be medicine for the disease (excess debt) as opposed to pretending the disease doesn't exist and wondering why we don't feel very well (current economic situation).

The root of a lot of inflation is rent and or mortgage payments forcing all costs higher . The bubble needs popping, speculators declared bankrupt, and the system reset without the crippling burden of debt/bank profit for no productive gain. Yes it will be ugly, a few banks will take a hammering, but Iceland did it at the end of the GFC and was back in good graces of global lending after a couple of years.

Our underlying export economy will allow us to do the same. We can feed ourselves, cloth ourselves, heat ourselves.

Don't think banks are seeing massive profits just because interest rates are rising. Remember, inflation erodes debt over time, this is good for person in debt and bad for the creditor (the bank that lent the money). Rising interest rates puts a stop to this, by charging the debtor the equivalent amount of money per month that they're losing through inflation.

If interest rates were left low what you'd see is wealth transfer from the banks to people in debt, thanks to inflation. And likely hyperinflation, since people would catch wind of this little loophole and go for gold.

Again a supply issue. Why have house prices gone mental the past 20 years.

If we want to get speculators out of the market the answer is simple, in addition to LVR rules its called a capital gains tax. But because the government doesn't work for New Zealand as a whole but only special interest groups they won't do it.

But again if we didn't have a housing supply issue for the last 20 years speculation wouldn't be such a big issue.

The government had the right idea with Kiwi Build, but were either to stupid or lazy (or both) to do it probably. It's a problem that will take 10 years to fix right.

They need to train people in the trades. Instead of offering a year free uni to learn about social sciences or arts or something that money to have been prioritised to industries that need more people, the trades to fix the housing crisis and medical fields to fix the never ending waiting lists (or just plain lack or expertise).

At the same time they need to fix the building industry supply issues and work to increase competition to lower prices on building supplies. A perfect example of this was we closed most of the wood mills. So all the wood was going overseas but nothing was coming back. That should never have been allowed to happen.

And lastly they need to pass the required laws to lower compliance costs that councils love to add to fund pet projects that don't need to exist and also force councils to open up land for housing development.

If we end up with more houses than people that is far better than what we currently have which is a homeless probably that never use to exist.

Bring back apprenticeships. Best way to produce skilled workers.

They did bring in free trades training. Whereas uni students only got one year.

If interest rates are not in line with FED the NZD will lose value making inflation higher, the government put rates at emergency levels and people went out bought houses at over valued prices people must of been aware rates would go back after emergency was over. All this has done is raised house prices too 12 X average wage earners salary in Auckland creating a huge amount of people with mountains of debt which people and speculators will be paying for a number of years. The other side of coin is to have hyper inflation where house prices stay same but food and living cost skyrocket and things like people fighting over bread petrol creating a complete breakdown of society. If people are stupid enough to buy a three bedroom house in Auckland for a million or more they have to pay for own decisions.

Again the house price thing is primary a supply issue. Yes lower interest rates has contributed to higher prices, but they are not the cause.

I bought my house in Sep 2020 in the Mananwatu. We had to move and weren't able to find to a rental, turns out land lords only want to rent 4 bedroom houses to people who don't have kids (again because demand is higher than supply so they can choice who they want) so we were forced to buy, either that or live in a tent. We needed a four bedroom home because of our family size but found there were literally only 3 houses in our price band in the entire Manawatu (500k to 700k). When all was said and done there was only 1 house that worked for us so only one house we bid on. We ended up having to offer 13% above asking as what we later found but presumed at the time that we were in competition with 10 other offers, (all this happened within a week of the house being listed too). If there was more supply we would have had more choice, had less competition for housing and therefore probably wouldn't have had to bid 13% above asking. Lower interest rates just meant we could afford to buy a house full stop.

If there is proper supply interest rates should have very little impact on prices. Example, car loan rates were alot higher 15 years ago, but cars dropped in price as car loan interest rates also decreased. Car prices are only now increasing due to supply constraints and government mandated safety tech pushing up prices.

If there is enough supply to balance out supply prices should be stable, if there is too much supply prices should decrease, if there is to much demand and too little supply prices increase. Using interest rates as to control house prices is a blunt tool that in the case is going to make things worse.

In terms of the fed rate they don't also match up. I know the theroy is that high interest rates should increase increase the NZ dollar and therefore make imports cheaper, but that can hurt local industry and therefore have a negative impact on employment.

Also it doesn't always work that way, in the early 2000s the NZ dollar was worth very little. In 2001 on average it was worth .42cent USD despite NZ having higher OCR than the US fed.

In terms of hyper inflation, one don't print money, and two secure are supply lines to vital things like, fuel, food, and building supplies (both things the NZ government is doing the opposite of).

If house price’s were 3 or 4 X average wage earners salary this would allow far more people to own house and stop people having to pay crazy rent prices.more supply is coming onto market every day and will stay there till prices come down.

If house prices go back to 3x - 4x wages you'd have so many recent buyers underwater that spending would grind to a halt. It's not to say it shouldn't be what we aim for, but there has to be a plan and targeted relief.

Better targeted relief for renters and FHB than welfare for speculators as has been the approach to date.

If you choose to buy a house at a million plus in Auckland on tiny lot or a old run down damp box that is your choice when the market starts to crumble people need to remember this was the gamble people made. Prices go up and down just this time house prices were so far over valued a couple on average wages would need 12 x income to buy a 3 bedroom house in Auckland most people should have seen red flags over last 6 years.with government lowering OCR to emergency levels which created FOMO people were conned now a reversal of market is happening and people holding to these million plus houses will get burnt. Don’t be surprised to see house prices back too 2016 levels in next couple of years.

The Reserve Bank and successive governments created this problem and the FOMO that drove it with their mismanagement of housing, tax and monetary policy. I have sympathy for FHB caught between a rock and a hard place...faced by the prospect that the Reserve Bank might make them permanently unable to obtain housing security if they waited.

Having created the problem through their ongoing wealth transfers to assets, it's perfectly reasonable for renters and FHB to demand some measure of justice if the whole thing blows up. E.g. per the Aussie New Libs' plan.

what if that was their only choice? You say there choice, but choosing to live in a tent or a run down house is not really a choice, or it shouldn't be. We have such a broken market due to lack of supply that many people can't even rent a house if they want to not because they can't afford it, but landlords would rather rent 4 bedroom homes to "professional childless couples" than families and they can do that because the supply is not there.

I don't actually care if house pricing drop, they need to. But it needs to be because of increased supply not because you have bankrupt and made large number of people homeless through large mortgage rates increases.

The truth is the market was broken 20 years ago, and because both Labour and National governments have delibratory chosen not to do anything it's now probably broken beyond repair. The time to fix what was broken was 10 years ago. Now the reserve bank is tasked with burning it all down which is sure going to help the WEFs Global Reset, you know "You will own nothing and be Happy" by 2030 slogan.

Okay So you want hyperinflation to happen in the near future and NZD to become paper? Do you think inflation is going away by itself?

Think big picture, not just about houses which is what most kiwis only have in their heads.

Demand destruction will deal with inflation. Money gets expensive = people spend less.

demand destruction works when people have excess money. But when we are talking food, fuel and housing, both those things are inelastic, people have to buy them no matter what. You can only cut back so much of what you eat and heat your home before you stave and freeze.

People are going to cut back their spending if they can on things like, eating out, streaming service, buying electronics, furniture, clothes and insurances. So of those businesses will close adding more economic pain.

None of that is going to have an effect on food prices as example. Take farming as example, there costs as increasing massively because of government regulation (alot of it climate change stuff, but also labour law changes ie minimum wage), fuel, fertilizler costs and now interest rates etc. They are not going to drop there prices because New Zealanders aren't buying it because its too expensive, they are going to sell it overseas or if for some reason they can't do that they are going to quit and sell up. So that means we will have to import at world prices and paying a higher price and probably for a lower a qualitity product.

Electricity - prices are increasing due to government intervention and climate change but also because generators are quite happy to dump excess capacity to keep prices high.

Fuel - increasing interest rates will only decrease fuel costs if the NZD goes up against the USD, but that doesn't always happy, in the early 2000s it went the opposite way.

House prices may drop, but the actual cost of owning a house will cost more because of higher rates so houses are actually more unaffordable. Rental prices are going to continue going to the stars.

Things for housing only get more affordable if serval hundred thousand people leave the country, which is highly likely giving the way we are steering down the barrel of some really hard economic times.

The government needs to focus on fixing supply change issue first and also decide whether fighting climate change is worth economic damage to our country when the worlds biggest polluters don't give a shit and will cause global warming no matter how much we cut our emissions.

Again if you can explain to me how raising interest rates is going to fix inflation open to hearing an explaination, but I just don't how raising interest rates are going to stop inflation on things the matter to average New Zealanders, food, fuel and housing.

Interest rates rising seem like a blunt tool that hurts everyone to so degree, but those who are affected most and people who live week to week any way.

Again if you can explain to me how raising interest rates is going to fix inflation open to hearing an explaination, but I just don't how raising interest rates are going to stop inflation on things the matter to average New Zealanders, food, fuel and housing.

I'm with you on this. Increasing the OCR will have marginal effects on CPI inflation. It will help keep the NZ dollar strong which will help a little in terms of the cost of imported goods.

As JFoe has mentioned several times, raising the OCR can potentially have some inflationary impact, for example on rents (as mortgage rates increase for landlords).

Yes and the central bankers being the robots that they are, will then go 'oh look, more inflation!' and then raise rates even more!

(look at the relationship between CPI and effective funds rate over the last 50+ years....)

Higher interest rates will also give people with deposits more income (even though its negative return in real terms)....which they may feel inclined to spend....increasing demand. And there are plenty of boomers sitting on a large amount of term deposits. Talking to relatives and neighbours etc who are now entering retirement...sitting on hundreds of thousands (some 500K +) of term deposits. Raising rates will make them feel wealthier with the possible consequence of increased consumption.

exactly, its just going to continue the wealth transfer from everybody else into the hands of the 1%.

Even if those boomers take a bath of 15% on their property investments and go and put that money in the bank the person who's buying that house is still paying alot more than a year ago because of higher interest rates.

This is why we need the entire system to change, particularly the tax system, which encourages speculative investment on property. As you all state, doing anything simply flows money up to the already wealthy because that's the way the system is designed.

It's hard that people can't get this through their heads. That's why we need to vote for something that doesn't just advance the status quo.

So what do you suggest RBNZ do in regards to inflation? transitory and will dissipate by itself?

Keep the rates the same? Cut rates?

Or does it even matter since the interest rates are more affected by the swap rates and the US Fed has signaled seven rate hikes this year

well, that's the thing, the Government is making inflation worse so now the RBNZ is being left holding the can. The only tools they are are basically weapons of mass destruction.

The world is going to be forced into a recession maybe even a depression to burn everything down and we are going to get a new economic system out of it.

The global elite want their own digital currency similar to what China has (which is more like a ration card than a free currency). It was all the talk the World Government Summit in Dubai a couple weeks ago, our own Treasury even released a white paper on replacing the New Zealand dollar with a new digital currency. Just another thing that will be force down our throats with no democratic discussion. (have seen no mention of any of this on NZ media).

Sorry about the rant.

This is how I see it playing out, reserve bank is going to increase rates anyway, as earlier posters mentioned if the Fed is increasing because we are such a small market we have to increase to.

As people have less money to spend because housing costs are going to continue to increase regardless of what the Reserve Bank does and food pricing continues to increase due to climate change policies, war etc, fuel and electricity are only going up too, many business are going to shut as people stop spending money on things they cant afford, people then loss their jobs, well its all down here from there.

Basically stagflation from hell. Wealth will continue to transfer from the middle class into the hands of the 1%. All bad news I'm afraid.

Interesting views/posts…

I dare say that you will be labelled a doom goblin very soon by the protectors of the property ponzi, if not already.

Good luck 😂

The only things that will be left for the middle and would-have-become-middle classes will be to march, unionise, demand change, force change etc.

Unless government begins to represent the interests of average citizens making average wages and trying to build a life, things will continue to get worse and we'll more resemble a developing country where people hide in gated subdivisions rather than sharing any measure of wealth.

Goldman Sachs warns that Fed may raise rates above 4%

https://www.forexlive.com/centralbank/icymi-goldman-sachs-warns-fed-may…

https://www.1news.co.nz/2022/04/10/ocr-rise-likely-amid-runaway-inflati…

80% to 90% as per 1news feels that should go up by 0.5% BUT can vouch knowing Mr Orr's .......will be 0.25% and even that as is forced.

.25% for sure its called "Virtue signaling" and NZ is becoming an expert in it.

1% increase on 500k mortgage is additional interest of $96 per week. 2% is $192 week. For 1 mil it is $192 week for 1% and $384 week for 2%.

Every 10k in salary over 70k puts about $120 a week in your hand. Hundreds or mortgaged households are taking huge disposable income hits every day as they are forced to roll over their 2 -2.5% mortgages onto new rates +4%.

This will not end well.

The government may give tax cuts to counteract it, and then borrow to make up the shortfall. They can't let the housing market crash as that will crash the economy. They let the bubble occur despite warnings. I wonder if they are regretting printing all that money which inflated the housing market, and used the housing market inflation to help make people feel rich and get them out spending. This is the hangover

They need to go 50 if not higher, as they previously didn't raise it enough. Inflation is only continuing to rise, and it is far far higher than it should be. Isn't it expected to be over 7 -8, and real world inflation is even higher than that.

Even 1.5% OCR is really low. I would hope to see it at 2% by mid year. They aren't even getting inflation to slow down at the moment.

You need to understand, its obvious the RBNZ are protecting the housing market. How many either zero or 25bps rises is it going to take before everyone gets it ? 60% of all mortgages were due to roll over this year, the RBNZ is buying time for EVERY home owner to fix for 3 to 5 years before the shit hits the fan. If everyone can fix at the current rates there will be **** NO HOUSING MARKET CRASH ****.

The cost of debt is climbing quickly all over world US 10 year up too 2.77 ( 4 year high) If anyone can fix quickly it would be smart as RBNZ will not be able to control this.

Also understand that NZ is a dot on the global ocean of fiance. Any real perception that Orr controls retail rates is somewhat Illusionary. If the US raises rates aggressively (as they announced they plan to) then ours will follow regardless of the RBNZ. Not wanting to over use the number 7%, but I think there is a real possibility of some rates being higher in the next 12 months

The banks will just make mORE profit, while ORR fiddles. As they are doing currently.

But wasn't the only thing they were supposed to use the OCR tool for, was to control inflation?

Increasing interest when inflation caused by supply issues, not increase in consumer demand, will only add more costs to businesses, such costs will then be passed on to consumers causing further spiral rise in inflation. Micro policies need to be applied to target factors that cause inflation, ie., tax subsidies to increase wheat production locally if imported wheat prices had gone up due to overseas supply factors such as production affected due to covid 19 in production countries.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.