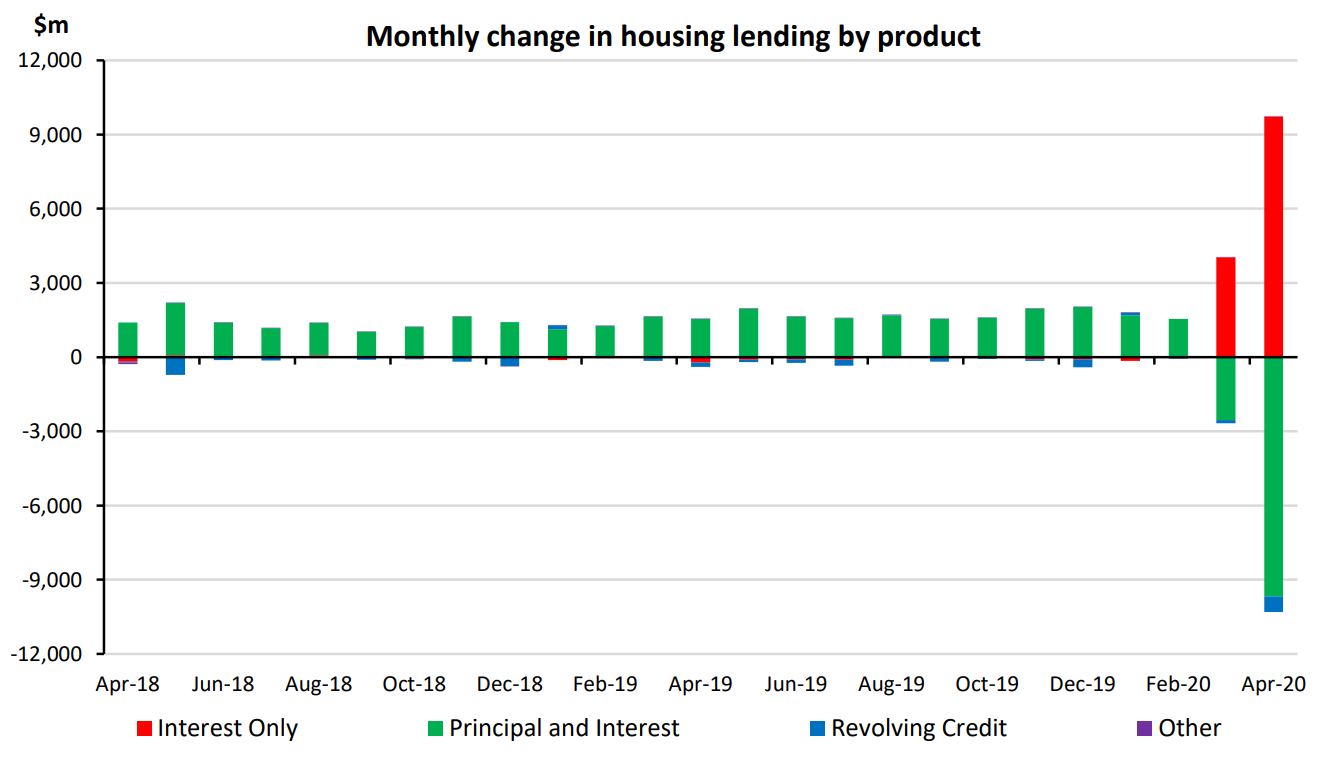

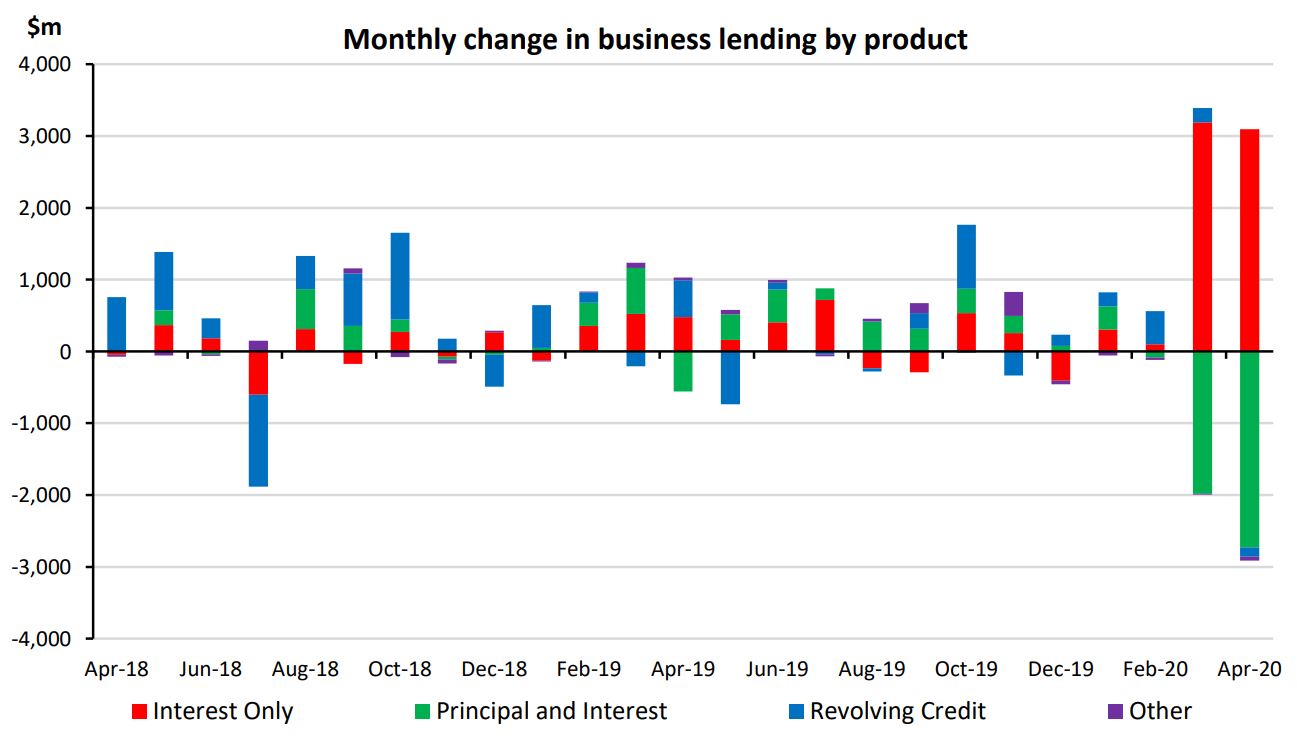

Borrowers shifted several billions of dollars of mortgage and business loans to interest only in April, as the country went into lockdown due to COVID-19.

As at the end of April, 24% of the $277 billion of housing loans borrowers had with banks were interest only. This was up from 21% in March and 19% in February, according to the Reserve Bank (RBNZ).

The portion of interest only business loans increased to 41% in April, from 38% in March and 36% in February.

The figures show borrowers largely rearranged their debt rather than borrow a lot more.

The value of business loans on banks’ books only increased by 0.15%, or $182 million, to $118 billion in April.

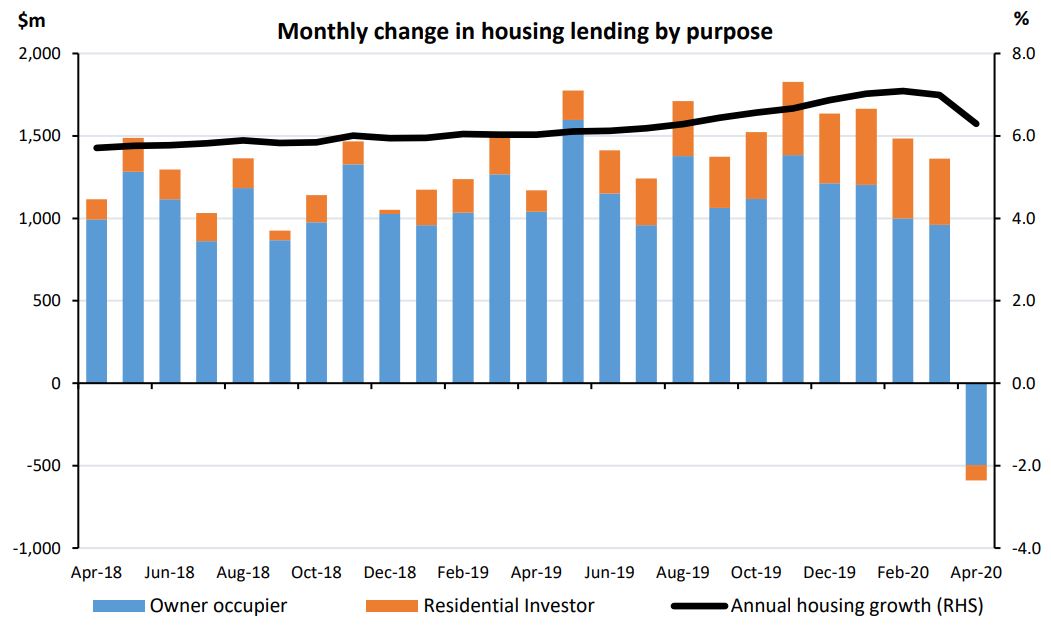

Meanwhile the value of housing loans fell by 0.2% - the largest monthly decline seen since the RBNZ started collecting this data in 1998. The lockdown meant the housing market essentially froze in April.

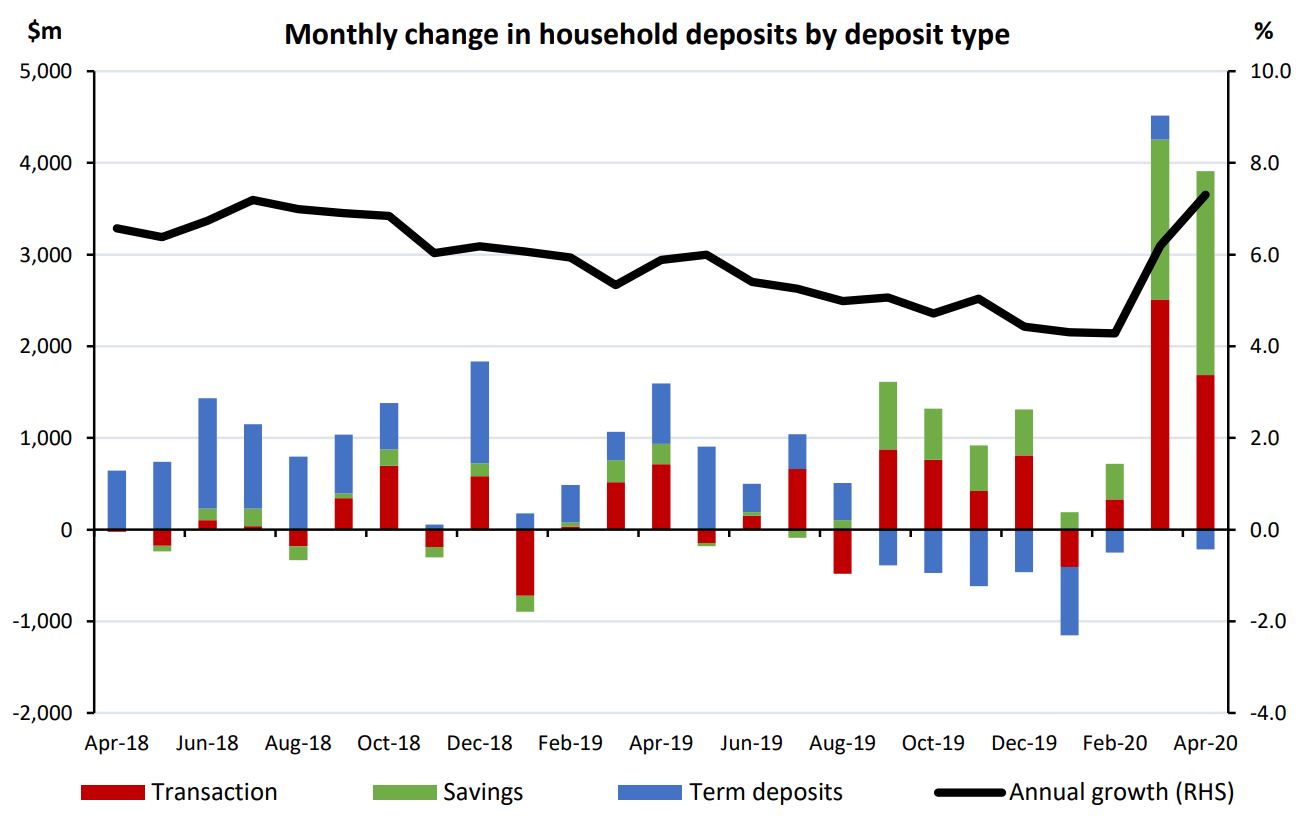

The value of deposits held by banks increased again in April - up nearly $5.6 billion, or 1.5%, to $385 billion.

It’s worth noting the Government injecting about $11 billion into the economy via its wage subsidy, which affected these figures.

Of this $385 billion of deposits, $193 billion were made by households. The value of their deposits increased by 1.9% from the previous month.

The increase in household deposits was all in transaction and savings accounts, with term deposits down.

41 Comments

Note the correlation between credit growth and house price growth...if credit growth decreases or even is flat house prices fall. Next few months are going to be interesting.

I wish more people understood that relationship.

Correlation is really too polite a word for the relationship. Credit growth IS house price growth. NZers are broke. Statements like this "New Zealand households’ collective tendency to spend more than their income" should be terrifying.

The hysteria of the comments by people on this site promoting expanding asset prices says it all. They know they have no capital and nothing to offer. If the machine goes in reverse their life is over. I would be scared too if I was in their position.

And economic growth in New Zealand = Credit Growth.

Doesn't imply negative capital gains. Implies inflation adjusted losses, probably similar to the early 1970's downturn in NZ.

Volume collapse has been likely for about 2-3 years now.

I.e expect inflation to spike heavily, 15-30% upward from here.

Always remember the real inflation adjusted returns of residential are low, in the 1970-1990 period they were 0.5% a year. The main issue with the property market is the real returns since 1990 were enormous, it went from around 100% of gdp, to 420%~~, you'd need money supply growth to double to triple from here to make sure the property market didn't wipe out the banking sector and cause severe deflation.

The property market when it outpaces money supply growth just leads to future inflation.

Say hello to large inflation and a flat to down property market for the next decade, there is a huge issue in the property market that is unraveling.

Wait a minute wasn't the Big Four Ozzy banks meant to be shifting people off "interest only" mortgages? To try and end the debt spiral and shore up the banks???

It was propaganda in retrospect, built on poor underlying financial foundations.

Remember those ads of the mid noughties where the banks would go on about their good work in the community?

You'd nearly laugh at it now.

You'd rather they didnt help families affected by COVID?

What a precipice! Yet some are arguing that residential property prices will increase.

Our totally unbiased experts at OneRoof are saying that it's boom times.

I dont get why the media ask for Bindi Norwells input when shes a bonafide lobbyist.

Because the companies that advertise with the media (remember RE companies are the Heralds biggest advertisers) want her to spread the good word on property.

The Herald is so horribly compromised. You see their reporters doing some good work - Simon Wilson is great - and then half of their website is outright property industry propaganda, which they probably can’t refuse without collapsing financially. Awful situation.

It's not like they were refusing it before the crisis. Only going to get worse.

"Extend and pretend" as they say at European banks.

I do wonder, hypothetically, if bank called the 41% of business loans that are paying interest only and forced them to repay the loan what % is actually recoverable? My guess is that many would be insolvent and banks would get cents on the dollar. It would be interesting to see if banks caved in on writing down loans if faced with that scenario because it may be a way out for small businesses.

Extend and pretend

Poor old Queenstown has lots its sparkle. Big auction today and it sounds like it was mainly attended by lots of tumbleweed ; )

https://www.rnz.co.nz/news/national/417893/covid-19-auction-tests-deman…

Yowzers...crickets on 8/21 properties

I'm quite surprised by the result. Five sold under the hammer, another eight got bids and eight had no bids. This result would not have been abnormal in Auckland last year.

Lot 1 was a circus of $50k jumps and a back room $950 Sold result. Have been hounded by an agent all weekend saying I'll make an easy $50k... irony, most of that is his if we need to sell it, so an easy nothing. 6 months will be worth the wait!

Why do you say poor old Queenstown?

I would’ve thought it was totally the opposite.

Was down there for a few days last week and yes it was quiet for what it normally is, but it will bounce back and is busy this weekend.

You really think domestic tourists can take up the slack of a collapsed international tourist market? Absolutely no chance, especially as 1000s of kiwis are losing jobs and the ones that don’t will be watching their finances for fear of losing their own.

Tourism is 20% of our export earnings. Completely goneburger for at least 18 months. That alone would be enough to drastically change our economy in a normal day. This isn't a normal day.

A2020 - Local tourism will go a long way to filling gaps, I see for example Hamner Springs are booked out for the long weekend and we tried to get into Omapere Hotel a large complex and it's full too !

yes first long weekend for months after lockdown -- rates about 50% or lower on everything -- so its booked out for three days!

thing is -- that all tourism to operate at high levels of occupancy tue - friday next week - and the next 20 weeks till Labour weekend - which simply wont happen = At teh moment - a good few people with disposable income and job security wil take advantage of the prices but not every week and certainly not weekdays --

on off -- try booking next weekend - take your pick!

Exactly...it’s one thing to be busy for a long weekend after an extended lockdown, but to suggest this will continue for months to years in the future is madness. Did anyone see the news report of the waitomo caves tour? The owner just spent $3million on a new facility which was completed 1 weeks before lockdown. He’s just laid off all his staff.

I showed a house for a relative to some of the people going to that auction. They were clearly not serious buyers. There is a weird phenomenon in NZ of people dressing up and looking at houses.

The property in question would have sold in minutes earlier this year at the price it is being offered at. Virtually no calls at all and zero serious inquiries.

With everyone looking left and right, but feeling safe due to rediious rates in the banks is anyone surprised?

Most of you just don't get it. There will be no housing market crash. Prices will slide down in a few places. But mark my words, prices will be up at least ten percent from where they are now, by Christmas next year. It's not even three months since we shut down and already the NZ stock market has clawed back two thirds on the drop.

There is so much money sloshing around, the property stall will be just a splutter.

By the way, I have no vested interest. I want nothing more than to see prices down by thirty percent. But sadly it just isn't going to happen. You will need to steal yourself for that. It'll be hard, heaven knows I'm struggling with it, but it is was it is.

You're right you know. No housing market crash. Everything is going off the cliff at once. There's nothing for the housing market to crash into on the way down. Houses will be worth $5m. But so will a loaf of bread.

If you don't believe me, look at this house... Crashed economy, but....

Bread maybe you right... Houses will besubstantially more...

This house is going for 19 Billion shi* bits. Almost 800k$

https://www.property.co.zw/listings/4-bed-garden-flat-for-sale-greyston…

Hope the economy recovers within 6 months to cover the returning principal payments.

The knock on effects of this are going to be huge in the coming 6 months. It is going to be the winter of doom and depression if we don't watch out. The knock on effects of people losing their jobs and then people trimming expenses will cause other business to fail. It is like a domino effect.

24% loans on houses interest only.

Presumably investment made with a view to capital gains. That's going to be a hard call by the investors. Should the market fall, they will be left somewhat out of pocket.

The tourism industry without foreign tourists, prepared to pay big bucks, set the earning level for the industry. It's hard to see domestic tourism being able to match that. The housing market reflects this, in as much as the loss of income leaves the housing market totally reliant on the domestic market, with no income from outside. Properties that are Airbnb rentals are used to much higher monthly income than longterm rentals.

But yeah, that's right, Adrian and Grant are already buying anything that is in danger, topping up everybodies bank accounts, and promise everyone that interest rates will be near zero for a very long time.

Will they, and most other central bank/govt double acts around the world get away with perpetuating the lie yet again?

I see General Hububs point, and certainly agree, apart from the fact that I think a global reset boils down to war between major factions, and I think this will favour the producer economies, not the consumer economies.

I think people have forgotten, or were unaware, that the price of oil went to negative $37.60, not because of covid 19. It was a war on oil, in particular the American oil industry, and maybe not many are watching, yet there are bankruptcies like has never been seen, and the resulting credit crunch hasn't even started to show through yet.

We haven't even mentioned CMBS (commercial mortgage backed securities).

The dominoes are all nicely lined up, and the fed is printing like crazy to fill the space between the dominoes.

The msm may be able to paint a happy picture in NZ, yet when set against the actual backdrop of currency wars and trade wars, the situation looks somewhat different. Personally I think that those that are invested to the point they would prefer to remain in the dark, are better off in the fairytale they are living in. There is not much they could/can do to change their circumstances, they would only worry. Better to let them carry on enjoying themselves right up to the moment that it all stops.

"Take therefore no thought for the morrow: for the morrow shall take thought for the things of itself. Sufficient unto the day is the evil thereof."

I remember people saying the same thing years ago about NZ. "If people really knew what the situation was they wouldn't be able to sleep at night". But things never turn out as bad as people fear, usually they turn out far better.

With interest only loans it makes sense for a landlord to have a rental that's cash flow positive to have one of these mortgages. It's a nice business partnership with the bank. The bank gets interest and the landlord gets what's left over. If the landlord accumulates a bit of cash he may pay down the mortgage a bit on the next term to improve cash flow.

ZS - Indeed I've been a property investor for 37 years and only ever had interest only !

That strategy only works if you can keep the rental tenanted which is not guaranteed in this economic environment. Already we are seeing rental listings rise dramatically. Coupled with a lack of demand from no immigration and international students, tenants under financial pressure and a likely significant drop in house values one could be up sh$t creek before they know it.

There is not a single positive indicator in the markets anywhere except the false rise in the US stock market. The USA is the country to watch as it will affect little old NZ no matter how well we try and pull out of this dive. Its looking like the engines have stopped in the USA and they are getting 2 million new unemployed a week and that is leveling off at 2 million and not dropping. Its going to be catastrophic over there and the election timing is perfect for civil unrest, its the perfect storm. We are underestimating the possibility and size of the negative shockwave on this one. Some of the outcomes from this are still incomprehensible by most people.

We offer a wide range of financial services which includes: Business Planning, Commercial and Development Finance, Properties and Mortgages, Debt Consolidation Loans, Business Loans, Private loans,car loans, hotel loans, student loans, personal loans Home Refinancing Loans with low interest rate @2% per annual for individuals, companies and corporate bodies. Get the best for your family and own your dream home as well with our General Loan scheme. Interested applicants should Contact us via email: (clintonkenloanfirm@gmail.com)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.