The annual rate of household deposits growth for Kiwis has hit its highest level in nearly three years. However, lending to businesses has dropped off sharply.

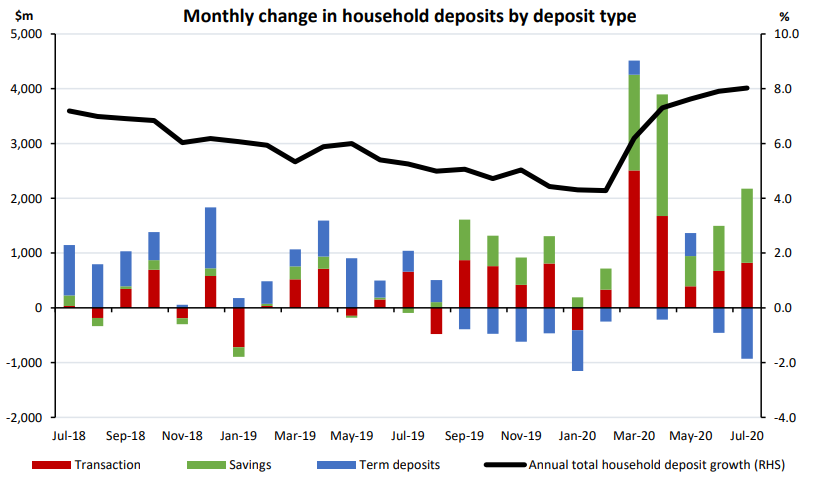

According to deposits data compiled by the RBNZ the amount held by Kiwi households in the bank increased by a further $1.247 billion in July, bring the amount sitting in bank deposits to $196.334 billion.

The annual rate in growth rose to 8%, which is the highest level seen since October 2017.

But those figures tell only part of the story, because early this year before Covid emerged, deposit growth rates were falling towards 4% on an annual basis, only to kick seriously up in March as we closed our borders and contemplated heading into lockdown for the first time.

In the past five months, household deposits have risen by a whopping $11.848 billion (a 6.4% increase in the total).

Whether that money will stay there with the wage subsidy drawing to a close remains a key question.

And while the overall total of deposits rose in the past month, it's notable that there was an around $900 million drop (to just over $100 billion) in the amount held by households in term deposits.

The increase in the overall totals on deposit for households came from a $1.353 billion rise in savings accounts and an $823 million increase in transaction account balances.

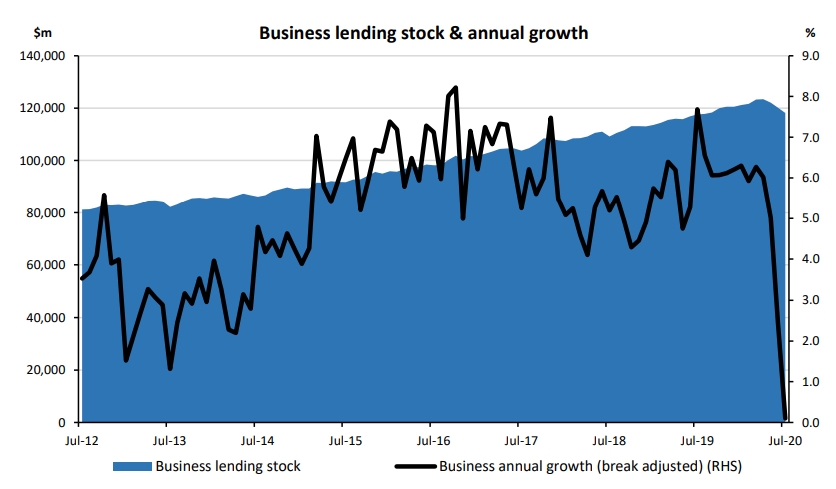

Looking at lending information, however, the figures for business lending make grim reading.

The amount of lending to business fell by $1.987 billion in July. Since April business lending has dropped by $5.229 billion - or 4.2% - to a total of $118.193 billion.

Other key points noted by the RBNZ in its month-end figures, included:

- Housing lending stock rose by $1.9 billion (0.7%) to $285.6 billion in July. This included a $1.4 billion (0.7%) increase in owner occupier and $0.5 billion (0.7%) increase in investor lending.

- Further movement into principal & interest (P&I) lending from interest only was noted in July as interest only housing lending fell by -$2.0 billion (-3.0%), while P&I lending rose by $4.1 billion (2.0%). Of all housing lending 22.6% was interest only as at the end of July 2020.

- Total consumer lending fell by -$199 million (-1.3%) to $14.9 billion in Jul. This included a -$124 million (-1.3%) decline for banks and -$75 million (-1.4%) decline for non-banks.

- Total business lending witnessed another large drop in July, down by-$2.0 billion (-1.7%) to $118.2 billion. Annual growth also fell sharply to just 0.1%. Business lending has declined by -$5.2 billion (-4.2%) since the end of April 2020. The shift back in to P&I lending continued in July as P&I lending increased by $786 million (2.4%), while interest only lending fell by-$1.2 billion (-2.4%).

45 Comments

It's not just us - it's pretty much everywhere, and all for the same reason:

"Household savings balloon as Aussies fear recession"

It’s exactly why we won’t get inflation anytime soon

Hey folks! I already asked this question in different post , but this one is more appropriate as it show average NZer has started to save.

Serious question , you might see it as trolling ,but unfortunately no jokes.

What are you saving for?

I have a little kid (2 y.o.). I myself was always taught to always work hard and try to save as much as I can, don't engage with suspicious investments, cannabis is bad etc. etc. etc.

Given that this govt (I mean not only the current one) and RBNZ broke all my understanding of how things should work in this world and really letting me down day after day, shall I just start the polemic in my family , e.g. stop saving , throw as much money as you can in as riskiest "Investments" as possible (e.g. Cannabis ETFs etc , maybe even "heroin" ETFs soon if suddenly it becomes legal), you should not worry about house price, just buy!!! because by the time you are at my age the OCR will reach -20% just because RBNZ is not seeing asset price rises as inflation. Apparently the cucumbers and potato need need to jump 20% so that they stop printing

Seriously, I'm a bit lost in how to talk to my kid .

What are you going to teach your kids?

I assume you (still) have a job.

When or if you don't, all your questions will be answered.

For any number of reasons, unemployment is going to soar.

It might not feel like that's a problem today (?) but it's going to be.

When your children reach the jobs market in 16 years or so, and there's nowhere for them to go to get paid, that's when your savings ( if you have any left) will come in handy.

But, I sense your frustration. "Normal" finished in 2008 - and it's not coming back. What we've had in the meantime is going to end at some stage, and then what we should have had back then is going to enter stage right - but bigger and worse; much, much worse.

given that RBNZ is doing something they know is not going to work out (Japan example and the rest of the world since 2008). how exactly do you see "What we've had in the meantime is going to end at some stage, and then what we should have had back then is going to enter stage right" . Why would they stop QE and OCR decrease. We can easily have -115% OCR by the 2075 and what would be wrong with that? You would just have on average -3000 NZD monthly salary but don't be afraid of the "-" sign. You wold still be able to pay your mortgage (oh , the RBNZ would do that for you) . You would be able to buy the car (it would cost $-10000 ), so you would need to "save" for it for a couple of months . Sorry, I might be exaggerating, but this is just ridiculous

Andreas

Fantastic post.. It is ending soon. People do not understand the fed and central banks are coordinating a global takeover. They want to control everything. Soon the banks will be out of business and everyone will have a rbnz digital bank account. $1400 a month each UBI no questions asked. You have to spend it all or you don't get paid. You will have to have the chip and vaccine to qualify.

do you think the current Real Estate agents will be the future "KGB" agents :-) ? and we'll have Gulag somewhere on Stuart Island for those who "disagree to buy a house at current price even if RBNZ pays for it" ? And it will probably be "Unlawful but Justifiable" ?

Why not just declare only property owners can vote?

probably because no one will need to vote, RBNZ would be the sole power and it would not matter NAtionals or Labors anymore

I like your posts.

Adds lightness, colour and another perspective.

That's a brilliant idea!

//

what they really don't understand that Russia before 1917 was exactly the same capitalistic country as Germany, UK, NZ etc. and all those events in 1917 led to where it has been since then. Are we expecting huge socialistic (read communistic) revolution in the US and later all over the world ?

Yes. A big lurch to the Left is what I've been expecting for years (not everywhere all at once of course). It will continue to drive money to hide, but the march of automation is what really matters, not these cycles of wealth redistribution and optimistic greed. About 3m driving jobs in the USA are about to evaporate.

Over this century I think "developed world" populations will split into two main groups: Many UBI funded entertainment seekers, and fewer tech nerd robot builders.

Yes, covid has brought forward what was going to happen anyway in the next ten years.

Great post andreas, it's great you're questioning the old way of thinking, keep these posts coming

given that RBNZ is doing something they know is not going to work out (Japan example and the rest of the world since 2008).

If you liked this post but don't think there's good logic for a global currency with immutable rules like Bitcoin, I don't know what else I can do for you.

Good question. I have been a saver all my life. Always try to buy as cheaply as I can and always drove a cheap car although I could afford new. Have totally changed my thinking as a result of recent events. Now I am buying whatever I want and have updated everything. Only problem is I have saved too much and have run out of things to spend it on. I have told my wife that anything we make in the business gets spent. Don't save any longer....

Just buy yourself a nice watch. I recommend a Patek Philippe Grandmaster Chime. That should soak up a bit of your spare cash.

We're doing the same, a bit more spending after a lifetime of not spending. Quite an insight but old habits die hard and spending is harder than I thought.

Well, that's exactly what the RB wants you to do.

So their plan is working.

How to run..............

Fact is andreas, even with all the DGMs around, what your parents taught you holds true now.. perhaps more so than ever. Don't be trapped or coerced by the latest "fad", keep your head down and focus on the end game and don't follow the herd. There's an old saying - God give me the courage to change what I can and the wisdom to accept what I can't change.

People are saving for the rainy day but there's another saying - there is no bad weather only poor clothing (old Inuit saying) so in other words, it's better to have some disposable funds than none i.e. in a rainstorm a leaky raincoat is better than a bikini

Well , according to J Powell last week (the US Fed's Chiar ) they will now target 2% average (e.g. allowing to overshot it) . Do you know what that means?? That means they can easily burn your savings in inflation within 2 years or so . Sure next RBNZ's move will be in line .

Maybe so, I'm not privy to the RBNZ thinking. The thematics of my post still hold true imo - especially the bit about not sweating what I can't control

Someone at RBNZ said as much today. The big question is if they can actually generate any cpi (as opposed to asset price) inflation which they can then "tolerate".

I can't see the CPI moving upwards in the near term. Having said that, what constitutes the CPI could (and should) be revisited, it has some very odd constituents, eg rental car prices and airfares.. those two alone are not necessarily part of the "basket" of average consumer outgoings

Not reviewing the CPI has been one of the best ways of keeping it down. Otherwise you'd have to reflect the increases in people's actual living costs, and then the sham that is NZ wage 'growth' will be laid bare.

Nothing has changed. Savings in the bank and debt reduction = more options. You can then choose leverage as an when it suits, ie just after a market crashes.

Though personally I have been slightly reducing the cash I hold in the bank in favour of shares that pay dividends.

Well, don't get too comfy...Adrian's got a plan.

Reverse Robin Hood to the Rescue.

This is explained by sectoral balances, as they tell us, a government deficit equals a private sector surplus and vice versa. Some further explanation here.

https://www.economicsjunkie.com/sectoral-balances-and-private-saving/

https://gimms.org.uk/fact-sheets/sectoral-balances/

Long, long ago in a different world, a strange beast emerged from the jungle-the QE. It was said to be able to produce something called money in huge amounts and that it would help regenerate the economy by handing it over to something called Banks and they in turn would lend it to something called companies. At a stroke, lots of people would be employed to make stuff and soon, we would all live happily ever after.

Well, we all like fairy tales, though many have a dark side to them and this one is no exception. For it turns out that the QE was never intended to get money productive businesses, but to pump up things called assets-houses and shares- and then another magical beast might appear, the trickle down effect. Sadly, this beast is toothless and thus ineffectual.

So there we have it, as interest rates on deposits vanish before our eyes, people are saving more and companies are reluctant to borrow. A cautionary tale indeed.

QE only raises the levels of bank reserves and as banks don't lend their reserves it has little effect on anything other than interest rates. Banks create money when they lend and they are not constrained in their lending by their levels of reserves.

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Au contraire.. the Equities market is going gangbusters, driven by homeless money (who would have thought?) Sure it might be a house of cards - and probably is, but there's no denying it's current gains. That is the true "strange beast".

must be part of the huge debt the gov't is taking on.

Just change the terminology from 'government debt' into 'private savings', they are the same thing. The opposite sides of the same coin. For every deficit there must be an equal surplus somewhere else.

and people expecting a low growth, no inflation, no opportunities. environment.

Treadlightly ...

If the Govt funds the deficit with money printing , does that really increase private sector savings in a "real" way.

You make it sound that Money printing is beneficial to individual savers... You imply Govt deficits are a wonderful thing.

In my view, the impact of money printing is akin to the impact a counterfier might have, in his community. He prints money and exchanges it for assets/resources . Asset prices go up as he prints and spends more and more money. He is generous and gives money to his Mates..etc ( as one does), who also buy assets and live the good life.

There is a cantillon effect thou... Winners and losers. Initial beneficiaries are those that received the printed money early on. The biggest losers are those that never got any and had all their "savings" stored in money rather than an asset.

The savings of the community appear to skyrocket as the quantity of money skyrockets....BUT that increased quantity of money still can only purchase the same amount of stuff as it did before the counterfeiter came along.

Can one really argue that the communities saving level has increased..?? I dont think so.

Doesnt real savings require an economic component ?.. eg.. the deferral of consumption, surplus production..etc.

( A squirrel saves nuts by accumulating more than he eats. This requires both WORK and THRIFT , on the squirrels part, as well as the production of nuts on Natures part

(Squirrel also shows that saving can be stored in different forms of asset, and not just money). in fact money is a poor store of value.

As u say, in double entry booking keeping, everything nets out to zero.

AND...Double entry booking keeping is a derivative flatland kinda reality... It derives from the real world of relationships, transaction, resources etc..

I think its dangerous to use bookkeeping logic , unless it is part of that bigger contextual understanding.

This is just my view... and I'm open to criticism.

Savings require an increase in the money supply otherwise we end up with deflation and economic contraction as savings remove money from the economy as it is no longer being spent. Keynes called this the paradox of thrift. What is the purpose of the reserve bank cutting interest rates except to try to increase the money supply through private borrowing, banks also create money but they can't create our savings, only the government can do that. Taxation deletes money as does repaying bank loans.

“What is the purpose of the reserve bank cutting interest rates except to try to increase the money supply through private borrowing”

But when there is a fall in the economy brought on by pandemic what is the point of increasing the money supply. It is not the supply of money but the DEMAND for money that is the issue and QE and lowering interest rates are unlikely to stimulate the real productive economy, only leading to higher asset prices. Reducing taxes for all would be more beneficial.

That is why monetarism has been an abject failure leading us to near zero interest rates and overpriced houses. Who but the banks have benefited from this though while all the time our governments try to run budget surpluses and so doing just exacerbating our low levels of savings and high household debt.

To blame all this on monetarism is nonsense, in my view.

Is Mmt going to do away with the private banking sectors ability to create credit ?

How will Mmt influence house prices ?

Will Mmt use asset price inflation as a reason to increase taxes ?

Business lending cratered.

Because & as there is no Business Investment.

Can you please break that down so the RBNZ and the Government can understand that no jobs are created when no businesses develop.

Are the banks still using their water tumbling computers to model the effects of inflation? I suggest they need something new for QE in NZ: a collapsible bucket, that can keep expanding to hold as much as you put in it. Over time, it becomes so heavy that the rest of the structure collapses in on itself, and all the buckets end up empty. Shouldn't be too hard to add into the model.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.