The lowest unemployment rate in decades is a bigger headache for Reserve Bank (RBNZ) monetary policy than the highest inflation in 30 years, BNZ Head of Research Stephen Toplis argues.

In his preview of next Wednesday's Reserve Bank Monetary Policy Statement, Toplis says the RBNZ needs the unemployment rate to rise, effectively meaning it needs people to lose their jobs, if it's to meet its monetary policy targets.

Toplis lays out just how blunt a tool the central bank wields.

"The Reserve Bank’s task is clear. At its most basic level it has to get current annual inflation of around 7.0% down to 2.0% and it will require the unemployment rate, now 3.2%, to rise to around 4.5% to meet its maximum sustainable employment objective."

"The only way the RBNZ can achieve this is to keep raising interest rates until it gets the traction it desires. And so it will," says Toplis.

The RBNZ's Policy Targets Agreement with the Government requires it to target maximum sustainable employment alongside price stability when setting monetary policy. However, just what maximum sustainable employment is is somewhat vague. It is not a specific unemployment percentage.

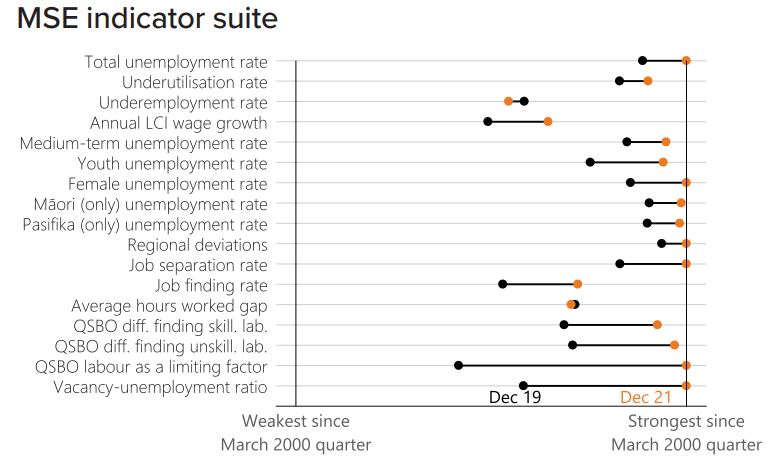

In its last Monetary Policy Statement the RBNZ said employment was assumed to be above its maximum sustainable level, as reflected in a wide range of indicators detailed in the RBNZ's maximum sustainable employment indicator suite below.

According to Statistics NZ, unemployment was running at 3.2% in the March quarter. That was unchanged from the December quarter and is the lowest rate recorded since the Household Labour Force Survey began in 1986. The Statistics NZ data shows 94,000 people were unemployed as of March. Annual wage inflation was running at 3%.

In terms of inflation targeting, the RBNZ must keep future annual inflation between 1% and 3% over the medium term, with a focus on keeping future inflation near the 2% midpoint. As of March the annual consumers price inflation (CPI) rate was 6.9%, according to Statistics NZ. That's the highest it has been since 1990.

Commodity prices hold the key to inflation

As big as it may be Toplis reckons the inflation task, at least initially, might be the easier one for the RBNZ.

"So much of current inflation can be attributed to rising global commodity prices, particularly oil. All it would take is for commodity prices to stabilise at current levels and the lack of commodity price inflation would have a marked downward impact on the local CPI inflation track. A modest correction could have headline inflation plummeting via its tradeables component. Stabilisation in commodity prices is a major part of our expectation that headline inflation returns to target in 2024," says Toplis.

"The bigger problem for the central bank is the state of the labour market. It is stretched to breaking and, consequently, wages are headed higher. Ongoing wage growth, coupled with rising inflation expectations risks making above-target inflation more permanent. On this basis, the RBNZ needs to see a marked softening in the labour market not only to meet its maximum sustainable employment objective but also to help ensure expected declines in inflation become more permanent."

"The frustration for the [Reserve] Bank is that labour market issues are currently more driven by supply than demand. Opening the borders and easing visa criteria are designed to help offset supply problems but we fear any respite will be limited. To start with, there will be a long lag between policy change and actual people flows, as folk go through the bureaucracy and then prepare for the big move. At the same time as the inflows improve, we expect the outflows to accelerate," Toplis says.

"There is already clear evidence of this, particularly amongst the key 20 to 35 year age group. If the supply response is as limited as we assume, then the only way the excess demand for labour can be moderated is if economic conditions reduce the need for staff. And bear in mind that the initial requisite reduction in growth will merely reduce the excess demand. It may take a substantial slowing in growth, or a recession, to generate the shift in the unemployment rate that will be needed to equilibrate the labour market in the eyes of the Reserve Bank."

"To put this in perspective, we think we would need around 18 months of zero employment growth to get the unemployment rate to rise to the RBNZ’s NAIRU estimate. All this being so, the Reserve Bank will have little option but to hike the cash rate a further 50 basis points when it delivers its Monetary Policy Statement next Wednesday."

NAIRU, or the non-accelerating inflation rate of unemployment, is a theoretical level of unemployment below which inflation would be expected to rise.

The key questions

Ahead of the May 25 Monetary Policy Statement Toplis says the big questions are:

· What will be the peak in the cash rate?

· How fast will the RBNZ want to get there? And;

· Will the RBNZ be willing to show a reduction in the cash rate toward the tail end of its forecast track?

"In the February Monetary Policy Statement, the RBNZ published a peak in the cash rate of 3.35%. We don’t see the need for this to change much. It is a model driven variable so some variation may occur. And we wouldn’t be surprised if it was nudged a little higher, say to 3.50%, but we doubt the RBNZ would push it so high as to match recent-past market pricing of a terminal rate of around 4.25%," says Toplis.

"Since the beginning of May, market pricing has moved closer to 3.75%. We don’t believe the Reserve Bank would want this pushing any higher at this juncture. At its April review, the RBNZ said that its 50-point hike was consistent with the interest rate track published in February. A further 50-point hike, which is what we expect, would not be consistent with that track."

"Consequently, the very fact the RBNZ will have moved rates 100 basis points over two meetings indicates a more hawkish stance. Moreover, we expect the Bank to produce a track which, effectively, brings forward the remainder of the tightening cycle from that which it published in February. Indicative of this, we think the Bank will have the cash rate at 3.0% by November of this year. Previously it took until mid-2023 to get to this point. If it does raise interest rates in this manner, the pace of increase will have been the most aggressive witnessed since the Bank began inflation targeting," says Toplis.

"Where the neutral [OCR] rate is perceived to be is a key factor in determining the future level and pace of increase in the cash rate. At the time of the February Statement the neutral cash rate was deemed to be 1.86%, or 'around 2.0%,' in the Bank’s words. It is plausible the RBNZ could shift this. But it could move it in either direction and history has shown us any shift is unlikely to be sizable."

The neutral OCR rate is the level where it's deemed to be neither stimulating nor constraining economic activity.

"The strength in core inflation that has been witnessed might indicate the neutral rate should be estimated as higher. In contrast, the extent by which current mortgage rates have risen already, the effective tightening in monetary conditions from tighter lending criteria, the observed impact these changes are already having on the housing market, lower population growth and heightened risk aversion (i.e. lower investment activity) might suggest a nudge in the other direction," Toplis says.

"Whatever the case, we doubt any such revision would see the neutral rate deviate substantially from 2.0%. This being so, a 50-point hike next week means the cash rate will be perceived as having returned to neutral. The RBNZ will, again, be leading the global central bank pack. It will be the first to contemplate what should be done with contractionary monetary conditions."

"As far as we are concerned, the response should become more cautionary once this stage has been reached. Given that the New Zealand economy is walking a tightrope at the moment, the RBNZ will not want to be the reason it falls off. The RBNZ said that its April 50 point hike was a stitch in time. That stitch will have been well and truly sewn when the cash rate hits 2.0%, so we see the RBNZ deferring to regular 25 point increases thereafter," says Toplis.

"Of course, they won’t rule out a further 50 point move at some point in the future. In particular, July will be seen as live. But it will be back to data watching in the interim, and in the period between now and the July meeting there is a very strong chance that: the global outlook will deteriorate further, in part as central banks elsewhere move their respective settings towards neutral; the decline in New Zealand house prices accelerates; and leading indicators remain in recessionary territory. This being the case caution should reign. When the Reserve Bank publishes its May missive, it will extend its forecast OCR track by an extra quarter, to June 2025. It is almost certain the peak in the cash rate will come a year, or more, earlier than published in February."

"This being so, there will be an opportunity for the Reserve Bank to publish a track which has the peak maintained for around 12 months followed by a quarter or two of rate cuts in 2025."

"We will be watching the tail end of the track closely. After all, the RBNZ will, at some stage, indicate that its actions have won the battle and that rates will need to start returning to neutral from the topside rather than the bottom. The Bank’s modelling will, by definition, drive such an outcome. Were the Bank to publish a small retreat in rates in 2025 it might be a good way to (a) reduce the chances that the market pushes its estimated terminal rate higher and (b) indicate that the RBNZ believes it has matters under control," Toplis says.

More overseas workers expected

In its February Monetary Policy Statement, the last one it issued, the RBNZ said it assumed labour market tightness would peak in the first half of 2022.

"High frequency jobs data suggest that employment growth is starting to slow and higher interest rates are expected to reduce demand over the medium term. More international workers are expected to arrive during 2022 as border restrictions are gradually eased. Net inward migration is expected to increase gradually towards its 20-year average over coming years, depending on decisions related to any changes to immigration policy currently being reviewed," the RBNZ said in February.

42 Comments

It'll be another "dovish 50" IMO. They will say they that interest rates are now at neutral and further increases will be slower.

Of course the BNZ & RBNZ are still stuck in academic theory Econ 101 from the 1980s & ignoring decades of real world evidence that NAIRU is a mostly flawed concept.

Nor do I see Labour campaigning on a 50% increase in unemployment.

I. don't see them campaigning on a fiscally balanced budget. Oh wait, they are banking on a tear or two from Jacinda at the right political moment

More wishful thinking and daydreaming. Get on with it and normalise monetary policy. The Ghost of Paul Volcker is calling.....

Just a coverup to hide the incompetency and failure.

Watching the blaming of the RBNZ is like hearing people blame the last batman in the second innings for getting out and losing the test match.

doesn’t happen

but I guess here the loss is more personal

... if not the RBNZ , then who was to blame for crushing the OCR into the dust ... triggering an insane spike in house prices ...

The problem wasn’t the lowering the ocr

It was the fact that when given credit at a cheap rate kiwis only know how to invest it in one thing

Let’s face we are talking about houses.

Not cnc machines, headrigs for sawmills, trucks, forkhoists…not research and development…not prototypes.

We don’t a financial crisis looming because every twenty something kid has bought a new Hass mill.

We didn’t buy any overseas companies or list anything on an Asian share market…no sir gummy bear hero

Oh no we blew it on houses our neighbours own and our kids can’t afford

and it’s been baked into our society for twenty years and we all just accept it

cause that’s how you get ahead

If the RBNZ's job was just to blindly raise or lower the OCR whenever a computer told them inflation was too high or too low, we could replace them with a computer and be done with it. In reality, the RBNZ's job is to understand the transmission mechanisms between interest rates and inflation in our economy, and use the tools at their disposal to keep inflation between the target band. RBNZ either understood what would happen when they dropped the OCR and did it willfully, or else they are so incompetent it beggars belief. Either way, they have their share of the blame.

Fair point but it is within the RBNZ's control to adjust the risk weightings for retail bank lending - so just because the OCR went down, if we had better regulation in place, then risk weights wouldn't have allowed banks to go crazy with the lending to residential property (and to those who already own property).

Unfortunately every push for change - even a reasonable sharing of the tax load - is met with shrieks of entitlement mentality and resistance.

GBH,

It takes two to tango, so while blame can certainly be laid at the RB's door, they didn't force people to take the cheap money and use to buy more property, boats and cars.

Lower interest rates have contributed to a stronger outlook for household spending. Household spending is supported by rising housing wealth. Stronger house price inflation is expected to support household consumption over the next year.

Quote is from the Feb 2020 Monetary Policy Statement when they dropped the OCR to 0.25%. The RBNZ didn't force people to take on extra debt, they just set up the perfect conditions for households to do so with full knowledge that people would.

It's not last batsman, it's the highly paid opener of the game who screwed up the series by scoring Ducks after Ducks by "hit wicket" in last 2 years and still paid with insane amount of world class batsman with pathetic and shameless performance.

And top of that giving feeble excuses of bad whether, light not good in ground and I can't see the ball it was too fast.

I think the root issue is that we have been killing our productive industries for many years, which caused New Zealand become less attractive for skilled migrates from overseas and to keep skilled kiwis. Just reflect on our industries for past years, how many people have quit their jobs and became property investors, real estate agents?

Exactly, good luck decreasing wage growth and increasing unemployment while retaining skilled kiwis. Im off to Auz at the end of next month, timeframe: indefinite.

Even a capable government can't possibly pull that off and here we have one that spent billions in protecting low-paid jobs in tourism and hospitality during the lockdown and, in the process, killed off productivity in the entire economy!

We also have a labour govt that printed 60million for every Covid death. How much tax does one person pay in their lifetime? Not 60million. Yes that's right, this has been a great trick at china weakening it's enemies without firing a single shot. And this left (but not communist left) govt took the bait

They are no good at anything else and were dropping in the polls until covid.

If you do root cause analysis you ask “why”five times to find the real reason

The financial industry has relied on lending to business backed by land as security

Cashflow and profitability are secondary considerations

Earning of export dollars or substitution of imports are no longer considerations

If you stand in front of a mirror and say "Candyman" five times, Adrian Orr will appear behind you and pin a 30- year mortgage into your back with a ballpoint pen.

We lost a newly qualified specialist in my field a couple of years ago to Real Estate. This is after a 4 year Scientific degree and 3 years on-the-job training in a very specialised role, on the skills shortage list.

More money to be made selling houses apparently.

Not necessarily a profession with an automatic pot of gold. My colleague is a successful REA with no tertiary qualifications. Exceptional sales skills. He definitely made hay while the sun was shining and focuses on the top end of town. A REA license and cheap suit are not enough to guarantee success.

MDF - Not any more, I would bet. The number of agents is now very high but the number of of house sales has plummeted. Lots of agents will be struggling to get ladles and will be leaving real estate as a job. A few really good and experienced agents will survive this downturn, which I suspect could last for quite a while.

mfd,

He/she will be back shortly.

"Where the neutral [OCR] rate is perceived to be is a key factor in determining the future level and pace of increase in the cash rate. At the time of the February Statement the neutral cash rate was deemed to be 1.86%, or 'around 2.0%,' in the Bank’s words. It is plausible the RBNZ could shift this. But it could move it in either direction and history has shown us any shift is unlikely to be sizable."

Hmmmm..

This RBNZ paper focusses on the neutral level of the nominal 90-day bank bill rate. This is a market interest rate that is a common benchmark for many financial products in New Zealand, and is largely determined by the level of the OCR. Currently ~2.16%

It is the real neutral rate that is most relevant for the setting of monetary policy – that is, the nominal rate less the long-term expectation of annual inflation. Currently 2.7% median, 2.1 average

A slightly negative real neutral interest rate. No?

Neutral rates are unobservable. Cash rate is irrelevant.

And?

by Audaxes | 18th May 22, 8:34am - Link

He (Powell) added that “if that involves moving past broadly understood levels of neutral we won’t hesitate at all to do that” and noticed that the American economy is strong and well positioned to withstand less accommodative, tighter monetary policy. [my bold]

The infamous unobserved economists’ R*, or R-star (natural/neutral rate), is a fiction. It’s one that they came up with after-the-fact to try to explain why their policies didn’t actually work the way policymakers had initially promised. While in public, officials still speak glowingly of each QE, one after another after another, in private they know it deserves absolutely no praise.

Study after study has shown basically the same thing (this pulled from a 2012 IMF research paper):

This reads like Powell saying that they have no problem crushing financial and housing market/s in order to get inflation under control.

"On this basis, the RBNZ needs to see a marked softening in the labour market not only to meet its maximum sustainable employment objective but also to help ensure expected declines in inflation become more permanent."

In other words, don't hold out hope of getting pay rises to ever catch up with the petrol we poured on the fire because we need you all to earn even less relative to inflation, or else the inflation we caused might get hard to manage, even though that's our literal job and we're bollocks at it.

Financial repression is required as payback for avoiding a depression back in 2020.

Rates will obviously be raised. Whatever RBNZ does it has to comply with FED wishes. Only troubling aspect is NZ has pushed up house price’s so far beyond average person affordability for them to purchase house the whole market has to crash and will over next couple of years. If 95% of people are locked out from buying who will especially in Auckland where price’s are 12 x average wage couples income.

Well, we all know that this is bs. The 'Real' unemployment rate is 11.2%. So good ole Sta's NZ's corrupted data and methodologies strikes again.

It took 1,000 years for Nicolaus Copernicus's view that the planets orbited the sun to take over from Aristotle's stationary Earth at the centre of the universe view. I am not sure that we should wait that long to move on from neutral rates, inflation expectations, NAIRU, sustainable employment... and all the other complete guff that many economists spout.

999.9 years to go...small comfort that Toplis is actually acknowledging (endorsing) that the boosting the unemployed buffer stock is the crooked doctor's only prescription for 'curing' inflation.

Mr Toplis may not have heard but the "phillips curve" has been debunked. Unemployment does not have to rise. With real incomes declining due to inflation the goal is achieved.

charlieandme,

Unfortunately, the Phillips Curve is like Dracula. No matter how often the stake of reality is driven through its heart, zombie economists revive it. It's all they know.

I cannot see that New Zealanders get higher wages is a problem. That should be a prime national goal.

WITH SO MANY YOUNG LEAVING THEY ARE FUCQED

I would be surprised if they have any idea of what their priority actually is. Remember this an organisation where being an expert prevents you from applying for a job.

Clearly they are going to flood the place with immigrants again.

We may fix the inflation crisis but will just make our long term low wage low productivity economy and impossible house price problems worse. I don't think that NZ is capable of addressing these problems. Those of you hanging round here, hoping that things are going to get better. Forget it. It is never going to. Your only option is to forget these foolish hopes, put them behind you and leave New Zealand.

Immigration typically suppresses wages in New Zealand. Government seem to be lowering the bar again so I image rising wages will not be an issue for long.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.