The Reserve Bank still has "expectations" that the country's banks will increase term deposit rates for customers - despite, at time of writing, no moves from major banks since the Official Cash Rate was hiked over a week ago.

After raising the OCR to 4.75% from 4.25% on February 22, the RBNZ made a big point of calling out the banks for lagging with their deposit rates versus what they are charging for mortgages.

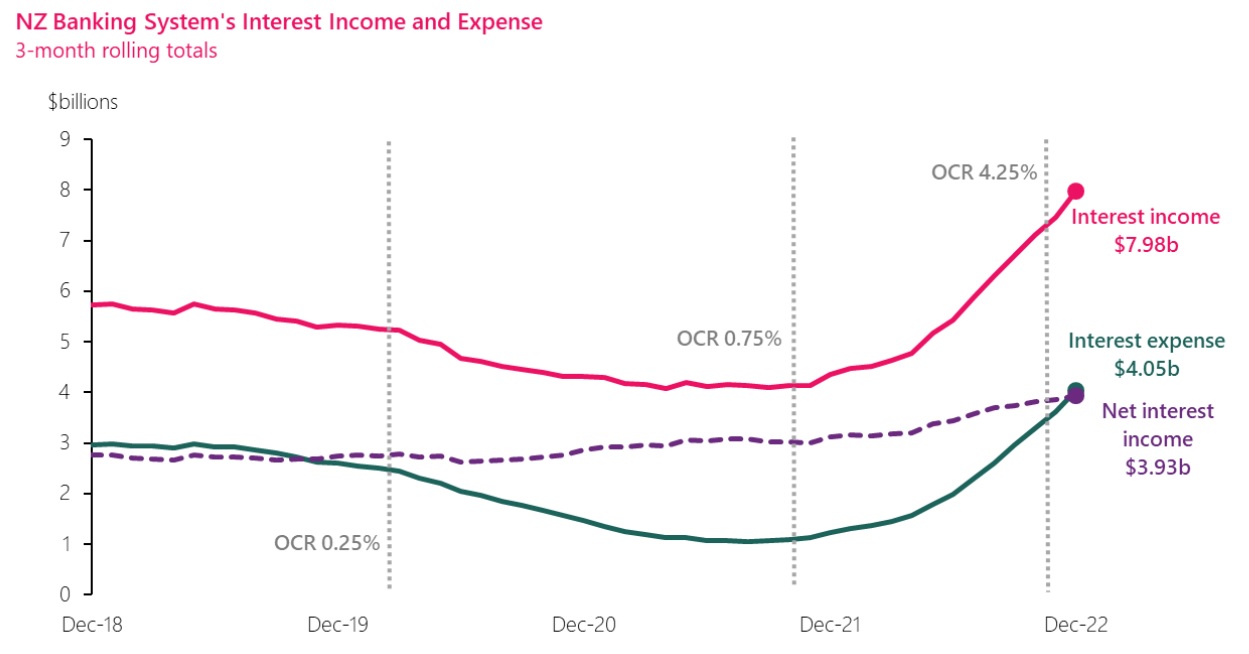

Earlier this week the RBNZ released the quarterly Summary Income Statement information from the banks for the December quarter. The figures showed the NZ banking sector's net interest margin (NIM) at an eight-year high.

The RBNZ defines the net interest margin as:

...the ratio of net interest income to average interest-bearing assets, where net interest income is income received less income paid.

According to the RBNZ figures, the bank sector's NIM was 2.37% as of the December 2020 quarter, up from just 2.00% as of December 2021. The 2.37% figure matched the NIM as of December 2014 - but before that you actually have to go back to mid-2006 to find a higher figure. The RBNZ data goes back as far as mid-1991, when the NIM was at a high of 3.26%. Figures of a bit over or a bit under 2% have been the 'norm' over the past 15 years or so.

RBNZ Assistant Governor Karen Silk, who is also General Manager for Economics, Financial Markets and Banking, said the banks are currently "sitting in a position where they’ve got very accommodative funding conditions".

These conditions included low credit growth, relatively high savings rates, and consumers "still with a propensity to leave money in very short term - on call or semi-on-call, accounts that are earning much lower interest rates".

Silk said that "all else remaining equal" about 50% of mortgages in the market will have rising rates over the next 12 months.

"A lot of the other lending facilities the rates are able to be adjusted in a relatively short time frame.

"If we don’t see increases in terms of the funding costs that net interest margin within banks will widen beyond historic levels."

What can the RBNZ do?

"Continue with transparency and the market itself will drive accountability from a banking perspective," Silk said.

"The banks are aware that there is a social licence aspect to the work they do. The position they are in is in a very sound position as it stands today and they are well positioned to help their customers.

"Our expectations are that they will do. They’re certainly indicating that they are today.

"We are just waving the flag that all else being equal net interest margins may well widen from here if we don’t see deposit rates increase as well."

Silk said the RBNZ was noting to banks that they need to be considering their customers as well - "and customers are both sides of the balance sheet".

"Customers are deposit holders as well as mortgage holders and so we are making that comment in relation to that."

Silk said through raising the OCR the RBNZ was trying to do is encourage saving over spending "and so as interest rates on deposits increase that will lead to the right kind of outcome from that perspective".

"We’ll see more of a migration out of that on-call and into longer term savings and that helps to dampen inflation.

"I do think it will [happen] over time anyway and that’s just because funding conditions will start to change."

She said the banks will need to go to wholesale markets more over time and will turn to looking "much more closely at ensuring that they’ve got good stable funding out of their depositors as well".

"That drives up competition. That means that term deposits will start to increase."

Meanwhile, on the mortgage side of the equation, the RBNZ is estimating that by the end of 2023 interest servicing costs may be absorbing about 22% of household disposable income for those households that have a mortgage. This figure is up from only a bit more than 9% as at the end of December 2021.

(The RBNZ estimates, based on census figures, that around 39% of all households are servicing a mortgage.)

Silk said the projected rise in servicing costs is "not unexpected".

"That 22% is still below the peaks that we had pre-GFC but will sit above the averages that would have existed over the last 20 years."

The RBNZ estimates that the 'peak' level was just under 27% as of the September quarter, 2008.

Silk said it is inevitable there will be an increase in financial stress as we come off extremely low interest rates, but says the figures for those in distress are still low at the moment.

In terms of 'problem' loans that are 90 days in arrears, Silk said the latest percentage figure they had was 0.3% "which is extremely low".

"When you compare that to post-GFC peaks, which was 1.2%. So, really a quarter of where we’ve been in a worst case scenario historically.

"Banks will be watching that data themselves very closely and looking for early signs of stress with their customers."

She reiterated that banks are in a very sound, well funded position.

"They are in a good position to be helping their customers through the next difficult period."

Silk was asked about reports that banks are becoming engaged in something of a secret mortgage war in which they are offering rates below their carded rates in order to attract or keep customers.

"Banks make their own decisions around what they are doing. It is a low credit growth environment that we’re sitting in. During those periods banks do get a little more competitive in terms of some of the activity they do," Silk said.

"Carded rates are carded rates. I do know that banks discount against that and just as they pay cash - there’s this propensity in the market for them to pay cash as well - the market will do what it will do. What we are transmitting are our expectations of what we think needs to happen for inflation to come back.

"If you end up with a situation where there is significant discounting in market and a movement away from that then it just may take longer to get inflation under control and we will need to continue to hold a tightening stance."

At the moment the RBNZ is forecasting that the OCR will peak at 5.5% later this year and then start coming down only slowly in the second half of next year.

Silk said the RBNZ had been "pretty happy" with market reaction to the OCR increase last week.

"Everybody recognised that we were making a tough call at a tough time."

While there were some market commentators that suggested the RBNZ should possibly pause with the OCR hikes after the extensive cyclone damage, Silk said the bank hadn't received any negative feedback.

“To be fair we actually haven’t. Look as I say, we were having to make a tough call at a tough time. We recognise it is a hard time for many people.

"Right now we don’t still know the full extent of the damage or how the Government and other parties will respond.

"Insurers, banks, Government, local Government - they are the best placed to work more directly with those communities and the individuals that have been directly affected.

"We in turn are working closely with those parties to understand and support their actions to help others where we can.

"For us, controlling inflation is in the best long term interests of all New Zealanders, including those that were directly affected.”

Annual inflation remains too high “and it needs to come down”, she said.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

29 Comments

Who exactly is the RBNZ trying to convince with this farcical talk of 'expectations'?

We should just 'look through' the low term deposit rates.

All that needs to happen is for the govt-owned bank, a.k.a Kiwibank, to lead the way. Force competition instead of keeping it's snout in the trough. Of course, since the govt are major shareholders, they'd rather take the extra profit back.

Banks and social licence - we have a winner for the Oxymoron World Cup

Absolutely! I find the term "social license" increasing used as some sort of threat implying that the bank or supermarket operates at the government's pleasure! Banks are subject to registration but surely within defined statutory limits,..not because they are making too much money. But of course governments, particularly socialist ones seem to believe we are the servants and they are our masters.

"How Tāne Mahuta can explain our financial system

Māori oral traditions tell us that Tāne Mahuta dug his shoulders into Papatuanuku (earth mother) and used his legs to push against Ranginui (sky father), separating them and letting the light into the world. With that light, Tāne Mahuta, guardian of the forest and birds, enabled life to thrive."

https://www.rbnz.govt.nz/about-us/tane-mahuta-and-our-financial-system

they dont even understand how stupid this woke rubbish is - what's next a tik tok video

The whole cabal need to be given the boot

Agree. Māori were one of the few not to discover the wheel and they had no currency or banking system or any functioning real economy. Now somehow they have some “world view’ which is relevant to international banking. It’s utterly ridiculous and needs to stop before some actual real damage is caused.

If Orr tried to do the job he is actually paid for and started to pay real attention to the fight against inflation, rather than wasting his time on these stupidly woke slogans, then the NZ economy would probably be better off.

Banks have to pay their handlers and for 90% of banks and shareholders are not based on NZ. So they give two fingers or one finger salute to this social license. They do not care what NZ or their public thinks

They only care about their bottom line and their margins. Hard cold cash profits like any other person or business in your country.

Do RE agents have social license feel?

Do super markets have social licences feel?

Totally correct. And Orr's talk about 'expectations' points very directly to the RBNZ's unwillingness or inability to regulate them into doing what is needed. If Orr is so strong on the banks social licence, why doesn't he right it into the regs governing the banks on how they operate?

Its a bit rich for RBNZ having destroyed their social licence to now lecture banks

You'd think with the huge pay rise, Orr would have carte blanche to make the big calls and pull the banks into line. Instead he waits on the sidelines with minimal OCR hike in Feb expecting all the mortgage bite to do the hard work over the next 12months

I expect many NZ pension, saving and investment funds own Ozzie bank shares so a tiny bit of it will be coming back onshore.

Anyone know how many?

Banks are interested in themselves. More profit, less overheads vial less branches (rent) and less staff (wages). To highlight a higher mandate/social license without legislation and a way to externally measure that is a tui add surely?.

Just had a call from my bank asking what I want to do with a TD maturing at the end of the month. I told them I'm short of cash which is true so probably wont re-invest it. Getting these calls regularly now since I started moving my money away from them chasing better rates at other banks. My balance with them is only 30 % of what it used to be.

Genuine question, has anyone ever been called by a bank to be told aboutspecial account types for those with (insert large number) bank balance? This happened in the UK a few years back to a friend who came into a solid inheritance, was wondering if this occurs here also.

The major banks all have a Private Banking department that caters for high net worth retail customers. Anyone with something like a 7 figure sum sitting in a savings account should already have been approached. The more your custom is worth, the wider the options.

Nope but got called late 2021 to see if I wanted to borrow a million against my family home, and start buying some investment properties as rates were only 2.5%...said no just want until first part 2022 see how the economy goes...well glad I did that, thanks to a few commentators on this site, FOMO nearly got me.

Jeepers, really? That's some absolutely terrible financial advice. Will come back to bite whatever bank that was, when the ponzi comes tumbling down. Can I ask which colour bank?

It's a lot harder to get much of a special rate these days and when we do its minimal, there was a time we could also part withdraw from terms without penalty.

Really?

Let the property market crash and take the banks with it.

Pick up the pieces, look after the worthy folks and start again.

Annual saving to the country $6 billion.

and while we are at it let us explode a nuclear weapon over Auckland. We can build a much better planned city on the site next.

The gap increased post Dec21 which is when our inflation grew. The banks are passing on inflated costs to their customers, like everyone else.

Ah, a satire post.

Are they tucking a bit aside in case of an increase in defaults?

Ummm...maybe they aren't increasing deposit rates, as they have enough cheap money.... that Adrian gave them via FLP.

There is only one way to make this happen, regulate. The banks have made it very clear, they are morally bankrupt.

Let’s see if the banka gangstas walk the talk.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.