There are fears the Reserve Bank’s (RBNZ) decision to keep the Official Cash Rate at 1% will see banks increase their lending rates.

The interest rate market reacted strongly to the RBNZ’s somewhat surprising decision on Wednesday to keep the OCR at 1%, rather than cut it further.

The two-year swap rate jumped 21 basis points in the immediate aftermath of the announcement. It is up 40 basis points from an October low.

Wholesale interest rates are back where they are were before the RBNZ made its shock 50 basis points OCR cut in August.

Kiwibank economists Jarrod Kerr and Jeremy Couchman say this reaction indicates lending rates are likely to rise "a little" from here.

The RBNZ wants banks to lower their interest rates so that people borrow more and spend more to stimulate the economy. If banks respond to the RBNZ’s decision to take a breather from cutting the OCR by increasing their rates, the RBNZ’s plan to stimulate the economy backfires.

Interest.co.nz asked RBNZ Governor Adrian Orr, in a press conference following release of the Monetary Policy Statement, whether he was concerned that the sharp increase in swap rates signalled a looming increase in lending/mortgage rates.

Orr said: “That’s going to be for the retail banks themselves to decide.

“There’s plenty of margin involved, and lots of business competitive decisions between the numbers you’ve quoted, both one: to how the OCR feeds through into market expectations and forward pricing… Two: about how that forward pricing feeds in to a competitive banking sector and what they do with their mortgage rates…

“What we’ve made very clear is that we believe monetary policy is very stimulatory and that we will have to keep it at that position for a long period of time, and if circumstances change, we will act.

“Really, they have to make commercial business decisions about what they want to do with their customers.”

Assistant Governor Christian Hawkesby made the point that markets constantly change their pricing.

“Markets are currently pricing a 20% chance of a [OCR] cut in February and a 50% chance of a cut by November next year, and we’d expect those percentages to move around with the economic data as it evolves,” he said.

RBNZ Chief Economist Yuong Ha added: “Over the year, we’ve actually had mortgage rates fall by between 50 and 150bps, so while we’ve had a bit of a short-term blip, we’re still providing a lot of stimulus through the economy and it has been feeding through to retail rates that households are facing.”

ASB Chief Economist Nick Tuffley pointed out the RBNZ was now starting its three-month, summer “hiatus” until the next OCR review with wholesale interest rates markedly up, and the risk that mortgage rates start to lift just as the seasonal spring upswing in housing activity hits its straps.

“Crucially, a lot of mortgage rate re-fixing will be happening in coming months,” he said.

“The associated balance sheet risk management of that re-fixing will in itself put upward pressure on wholesale swap rates, compounding the recent wholesale market pressures.

“Keeping the OCR on hold is not without its risks.”

51 Comments

This is the future for times to come.

Reserve Bank will have to keep the rates near around 0% in future and no action to reduce or even maintain will have negative effect forget about increasing.

Reserve Bank have themselves allowed to be blackmail by the economy.

Blackmailed by the 'economy'? No, by merchant banks. They, by the way, are not the economy. They profit off the real economy. The economy would probably like to see rates 'normalized' but thanks to the greed of merchant banks who peddled debt into the stratosphere, that's not going to happen, to the detriment of the economy.

Banks want interest rates to go up -- it helps their profitability, because they borrow short and lend long. The grandparent commenter had it right -- the reserve bank is keeping rates down because they've been convinced that house prices need to be kept propped up.

I wonder if they'd have a freer hand if fixing terms were longer. In the US they're also having difficulty raising rates, but it's at least a bit easier for them because they mostly fix mortgages for the lifetime of the loan.

Banks probably want interest rates to rise after a prolonged period of increasing loan book size. A bait and switch of sorts. Get everyone juiced up on low lending rates and then tighten up the vice on the balls.

Table mortgages will become a completely different beast. While the debt burden will decrease with inflation, a "normalization" of interest rates could see a P & I structure where the Interest amount in dollar terms doesn't decrease as the loan principal is reduced. So people could find themselves refixing at much higher repayment amounts just to ensure the loan is paid off within the amortization period.

'Fears'?

They might increase slightly, but no bad thing in terms of avoiding inflating the bubble further.

What would he know? He's just a Doom and Gloom merchant.

When collective experts, diagnosed a terminal cancer cells already spread & predictably calculated the remaining life span of patients? - also the same by worldwide standard data, you don't want to know. Hey, they're just an Oncologist specialist merchant. Only two outcomes for it: Death or remission for now. The rest is speculative, expensive trial/forever testing technique. For long time this Debt ridden/passing it between countries, younger generations etc.- it's just simply a remission method/borrowing time. The beneficiary generation try to avoid the painful death situation. We can deny it, pretend it's not there but oh boy, when it hit.. there's no mistaken about it.. slow,prolonged,painful & torturing - We knew & can feel the cry of it, when us/young a rental generations.. have to wipe.. the slowly seeping life from them, yea sad.

(From your link)

Central banks, he said, are in a lose, lose, lose situation. "They can't do more because that is becoming counter-productive, they can't go back because that risks causing market instability..

Well summed up. It should never have gotten to this stage, but it has, and I'll suggest he's probably right about what's coming. And when it starts to look grim, what will 'they' do? More of what hasn't and won't work, of course...

(NB: Any of us who have had a big 'position, gone bad' know how hard it is to ditch what you were so certain was going to work. That fear that "But this could be the bottom; a bit more time and I'm sure it'll all come right" takes over. So much has been committed in time, money and reputation to 'this is going to work' that it's hard to see any other course now except - more of the same)

your'e NB comments sounds like specuvestors who entered in the last few years!

"It should never have gotten to this stage, but it has" well thanks to 30 years of neo-liberal economics of Thatcher and Ronald Raygun we are indeed in a pickle. However I cant help but feel that the "right wingers" who wanted a "free market" are now those whinning its a "mess".

"big position....hard to ditch" indeed so I exited many years ago, too early as it goes by a long way but I am out. Now all I have to worry about is those still in do not drag me down into the poop with them (causing OBR events) which is highly likely.

Quite a few with serious credibility calling the same.

... thanks for posting that , Chairman ... always enjoy El-Erians thoughts ... he's not always 100 % on the money ... but usually close enough to warrant paying attention to ...

2.4 Bn

and 2 Tn

Not to shabby hit rate, for not always being on the money, I will take that strike rate.

Chairman Moa,

I think he is right on the money. When he says that there is a better than 50% chance of a repricing of stockmarkets,I agree. I have gradually been lifting my cash to some 16% of my total portfolio in anticipation of just such an event.Despite that, my shares are still worth more than they were 2 years ago.

Well blaming the low rates for this mess is not correct.

So in other words, banks and punters ran far ahead of themselves in pricing in a "cut to zero" cycle from the RB, mortgage rates plummeted.

Now the reserve bank has paused, taking some juice out of the forward curve and entailing a probable corrective uptick in rates (but still from an extremely low level).

And we're still getting squawking from sectors of the population who view it as their God given right to borrow (almost) free money.

And we're still getting squawking from sectors of the population who view it as their God given right to borrow (almost) free money.

While at the same time sticking the boot into others who receive free money from the government. Some are just more deserving of free money than others.

Amusing in the extreme, it proves as I've always said about doing business in

NZ, there is NO middle ground on business confidence, its binary and often irrational simply lurching from one extreme to the other, little wonder the country fails to acheive its potential.

The RBNZ wants banks to lower their interest rates so that people borrow more and spend more to stimulate the economy. If banks respond to the RBNZ’s decision to take a breather from cutting the OCR by increasing their rates, the RBNZ’s plan to stimulate the economy backfires.

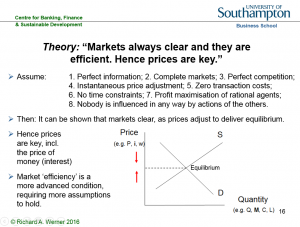

If there is no empirical evidence for the interest rate narrative, it is reasonable to ask where it came from in the first place. In other words, what is the origin of the idea that interest rates are the most important economic policy variable? We have ascertained that it did not emerge from empirical facts. Looking into its origin, one finds that it is a claim deriving from theoretical economics. The theory proposing the special role of interest rates can be derived from the central – some say only – graph in economics that shows demand and supply: it consists of an upward-sloping supply curve and a downward-sloping demand curve in price-output space. Under a number of assumptions prices are said to move so that demand equals supply.

This seems eminently reasonable at first glance: after all, if prices are too high, excess supply will be left unsold, resulting in price cuts and hence a fall in prices, until demand equals supply. Likewise, if prices are too low, excess demand will quickly drive up prices back to the “equilibrium” level – the point at which demand equals supply. This story is told about virtually any market: in the case of the labour market, the price is the wage. In the case of the money market, the price is the interest rate.

On our planet earth – as opposed to the very different planet that economists seem to be on – all markets are rationed. In rationed markets a simple rule applies: the short side principle. It says that whichever quantity of demand or supply is smaller (the ‘short side’) will be transacted (it is the only quantity that can be transacted). Meanwhile, the rest will remain unserved, and thus the short side wields power: the power to pick and choose with whom to do business.Thus the theoretical dream world of “market equilibrium” allows economists to avoid talking about the reality of pervasive rationing, and with it, power being exerted by the short side in every market.

Thus the entire power dimension in our economic reality – how the short side, such as the producer hiring starlets for Hollywood films, can exploit his power of being able to pick and choose with whom to do business, by extracting ‘non-market benefits’ of all kinds. The pretense of ‘equilibrium’ not only keeps this real power dimension hidden.

It also helps to deflect the public discourse onto the politically more convenient alleged role of ‘prices’, such as the price of money, the interest rate. The emphasis on prices then also helps to justify the charging of usury (interest), which until about 300 years ago was illegal in most countries, including throughout Europe.

However, this narrative has suffered an abductio ad absurdum by the long period of near zero interest rates, so that it became obvious that the true monetary policy action takes place in terms of quantities, not the interest rate.

Thus it can be plainly seen today that the most important macroeconomic variable cannot be the price of money. Instead, it is its quantity. Is the quantity of money rationed by the demand or supply side? Asked differently, what is larger – the demand for money or its supply? Since money – and this includes bank money – is so useful, there is always some demand for it by someone. As a result, the short side is always the supply of money and credit. Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky. Link

{kind=link}

Banks may take the RBNZ action of passing up on another panic interest rate cut (witness RBA) as a sign of a more stable economic environment into which it they can profitably lend.

Only house buyers spending more.

Giving boost to housing sector only, which I thought everyone was trying to calm down but I guess everyone realized that the only real economy in NZ is housing ecenomy

Came across quite a few people who have entered into development business (house) at this stage, their reason, that it is better than sitting and doing business, hopefully for them it works but if get stuck for any reason are screwed.

If I have met many, it must be the new trend now.

How do we get people to spend money that doesn't exist? Lend it into existence. Instead of retaining the billions of dollars repatriated every year by foreign banks and other multinationals, we fill the void via lending growth off the back of reducing interest rates. As soon as lending growth starts to recede what happens to the economy? Particularly when we run a current account deficit.

Instead of retaining the billions of dollars repatriated every year by foreign banks and other multinationals, we fill the void via lending growth off the back of reducing interest rates.

LLoyds Bank in London, back in 1989, fell over themselves to lend me and others money at 14%+, to dabble in residential property speculation. Thereafter, property prices doubled by 1997.

To some degree the current account deficit is funded by banks' borrowing hedged foreign currency.

Banks’ offshore funding is typically issued in foreign currency. The banking system currently has around $100 billion of foreign-denominated debt liabilities, primarily in US dollars and euros. Banks use derivatives to hedge their foreign exchange (FX) risks. Around 95 percent of their offshore FX borrowing is hedged, with most of the remainder ‘naturally’ hedged with foreign currency assets. FX risk is largely eliminated by these hedges, but risks can emerge in some circumstances (see box A). Link page 14 (20 of 48) PDF

The NZD hedging currency is X CCY swapped from these offshore NZD borrowers - here and here.

Audaxes,

"What is larger-the demand for money or its supply? Your knowledge here is much greater than mine,but where does that leave QE? The Federal Reserve increased its balance sheet hugely through several rounds of QE, but much of that went nowhere as the banks just left it with the Fed.We have seen QE in the UK, Europe and Japan so there is no shortage of supply. It has by and large not gone to the productive end of these economies,but has served to boost asset prices. The BOE reckoned that it had boosted asset prices by 20% and that was some years ago. To me, the short side may well be credit, but not supply.

To me, the short side may well be credit, but not supply.

There were two major evolutions in money and banking that seem to fall outside the orthodox narrative. The first was a shift of reserves and bank limitations from the liability side to the asset side. The second was the rise of interbank markets, ledger money, as a source of funding rather than required reserve balancing: replacing the old deposit/loan multiplier model. Courtesy of J. Snider from Alhambra

The empirical tests rejected the financial intermediation and fractional reserve theories (Werner, 2014a, 2015) and showed that banks do not need prior savings, nor central bank reserves or other deposits to lend. Instead, banks create new money when they do what is called ‘bank lending’, and add it to the money supply (see Figure 1). Bank loans thus do not transfer existing purchasing power, but add net new purchasing power. The banks’ lending creates 97% of the money supply. Bankers’ decisions about how much money is lent – and thus created and added to the money supply – and given to whom for what purpose quickly reshapes the economic landscape and affects us all. Sadly, no regulator has asked banks to ensure they lend for productive and environmentally projects – over two thirds of UK lending is not for productive purposes that creates jobs or boosts GDP, but instead for assets, causing asset price inflation. (same in NZ) [my bold] Link

This is a function of the BIS imposed risk weighted asset regime of bank regulation favouring bank loans collateralised by residential property, explained decisively here.

Furthermore,

Why hasn’t quantitative easing produced inflation? The answer is rather simple: quantitative easing is nothing but an asset swap. It doesn’t change the total amount of government liabilities in circulation. It only changes the form of the government liabilities that must be held by the public. Link- scroll down to 'How to needlessly produce inflation'

6-9 months before it all turns to custard. Orr just wants to feel he still has some ammunition left.

Banks should look after business clients, its crazy that housing gets better rates.

Crazy is the new normal.

You should visit the Adult Mental Health facility, then observed when those with 'conditions' interact each other, took longer period to pile them into same level of rehabilitative groups, limited options to release/discharge them. But you're felt odd sanity within their 'normal alike'.

Whats the default rate for businesses compared to the default rate of mortgages? And then what collateral do they all have when they default? It seems like they are pricing for risk, not a crazy strategy in my opinion...

I have called crisis hitting in 2021/2022, but it could be sooner.

When it comes, the NZ housing market will be toast.

Looking to Australia, NZ bank parents.

Here is the case being made that RBA has, has been rescuing the banks, there has been a banking event, and on the way to unconventional measures.

The trouble with rate cuts reminds me of a saying ..

'The more you keep doing something thinking it is a necessary evil, in course of time, it becomes more of a necessity and less of an evil'..

Aug-Sept-Oct-Nov : borrow, borrow, borrow - spend, spend, spend - Is this advise to the grown up?

Aug-Sept-Oct-Nov: at the time we advises, created wealth/money awareness for kids education, same advise?

Oh dear, now Nov - Four more bullets to use, economic warfare still staring in the front. Use it or..?

Oh may be? - If no more bullets, I can borrow it? from those fighting in the front.. akh such dilemma.

How do I/we fix this? - when the same theoretical worldwide herd actions doesn't work - do the opposite? that I can be more unpredictable 'independent' things eg. raise that OCR to 5% just for 1-3mths before drop it again - Sucks $ from those speculative passive inflationary productive growth promoted by the Banks. That will be a more sudden notification to them compare to those 'proposal, consultation..of capital adequacy requirements. - BUT hey, I used to be a banker myself - I wouldn't do it to the hands that feed me for years.

Really its only delaying the inevitable. Everything is cyclical and the next crash will be bigger and harder than the last one because we made it that way. Interest rates should have been kept where they were a few years ago.

A big Crash is inevitable . Can be delayed but not avoided and more the delay, bigger the bubble will burst.

No escape from the crash.

Now from 1% to 0% - if it continues should be by end of next year or 0.25% than WHAT ?? Even antibiotic are useless if given over a prolong period of time.

Yes they should never have gone this low. Rates this low should be kept for crisis, not moderate downturns

We really need to stop "stimulating the economy" with debt. Everyone knows the bigger the debt bubble the bigger the pop. Credit cycles are obvious. The way to stimulate the economy is to expand your consumer base that is currently choked with debt. A UBI would enable far more spending and get money flowing in the economy again.

... we haven't succeeded in stimulating the economy with ultra low interest rates ... merely created a wealth gap as house prices have ballooned ....

But , if that market pops a few folks are gonna witness how quickly " reversion to the mean " kicks in ...

... and the debt remains the same ... that doesn't go down when a market crashes .. .

Money is the lubricant in the economy. The oil.

We've got a massive leak going on via multinational corporate/banks extracting profits but rather than fix the oil leak we'd rather go down to Repco every weekend and buy another 4 litres of oil on our credit card that we can't afford to pay off because our expenses exceed our income. The credit card has a limit though.

Agreed. I like the oil analogy... An engine has an oil pump and oil galleries to ensure all working parts get served.

Nobody wants to understand that analogy. To do so would also require questioning the accumulation/hoarding of money, the illusion of price "growth", "value" and equality.

Every single component of an engine contributes to the overall functioning. You can't really place more "value" on any one item from the lowly nut to the high performing camshaft.

Take it a step further to really throw a spanner in the works. Remove money from the system, remove all the numbers and what's left? Everything still exists. It's only our relationships to each other, to the world around us that is real. Money didn't create anything. Everything good or bad was/is created by people.

We've created a system that is now a function of money/debt. We are serving it. The illusion is that it is serving us.

Another scare tactics by the banks ? Or trying to get a relaxed ruling on capital provisions ?

Strong Cartel and blackmail is the word. Will also succeed as will be supported and promoted by many vested experts and media.

Guaranteed - will push pressure to reduce LVR and RBNZ may or may not have done but now with lobbying/pressure is bound to reduce. Wait and Watch.

adrian has a tough job ahead,the economy is bent out of shape.some of us are queuing up to borrow big dollars to buy a house while others can have that amount in savings and now qualify for a community services card on low income.

https://www.fullers.co.nz/commuter-hub/senior-travel/

Senior citizens can travel for free on selected Fullers360 ferry services in Auckland, after 9am weekdays and all day weekends and public holidays with an AT HOP card loaded with a SuperGold public transport concession.

Well at least it's only free after 9 am on Weekdays and on Weekends, when it's considerably cheaper to operate a boat.

Still no real inducement to move to Awkland, but.....

Question for all you knowledgeable people. So at this point is it better to take a 2 year fixed rate or have the majority of the mortgage fixed at 1 year?

Looking at buying a house so needing a bit of advice, thanks :)

Float some, fix some. But please, ferchrissake, don't take the advice of my dog 'ere, who's managed just the one coherent phrase and to the best of my knowledge is not a Certified Financial Advisor.....Woof!

Fix 100% for 1 year.

This is a plateau and by next November the OCR will be even lower.

My pick 0.5% OCR.

As banks lend for longer periods on larger debt (mortgages) they make MORE money at lower interest rates.

It is interesting that Aussie banks are minting it for last 7 years, compared to EU banks.

EU did not have benefit of being propped up by Chinese printing in 2009-13.

Except for German car exports of course.

Interest rate cuts are a sop to try to cover deficit of demand in economy.

Deficit of demand is due to the top 10% sucking up a greater and greater % of economic wealth of countries as a result of asset inflation induced by central banks and concentration of house ownership and leverage opportunity for rich. Plus all savers income getting screwed.

As Adam Smith and Ford said a while ago, workers need enough to buy all stuff capitalists want to sell them.

Capitalists too stupid not to screw workers, so State has to intervene.

Which it did in OECD until 1975 after which it went on to favour capital and finance all the time.

When rich get money they do NOT spend what they do not need to spend, it gets parked and thus more money has to be printed.

About $32 trillion is parked in tax havens it is estimated, where it stimulates ZERO growth.

Meanwhile all governments suck up to rich in case they take their money elsewhere and foreign exchanges crease the currency. WHY do they not all get together and say, no we are not going to play this game of yours any more?

How much debt are NZ banks and financial institutions holding? How is that split between national and local Government debt, and public/private debt?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.