Westpac New Zealand's economists are increasing their forecast peak for the Official Cash Rate (OCR) by 50 basis points to 3.50%.

The bank's economists, led by Acting Chief Economist Michael Gordon, see the OCR reaching 3.50% by the end of the year. Having been at 0.25% as recently as early October last year, the OCR's now at 1.50%. They argue the Reserve Bank's inflation targeting framework, guiding monetary policy since February 1990, is facing its greatest challenge yet.

"We now expect the Official Cash Rate to peak at 3.50% by the end of this year. Inflation has risen to a multi-decade high, and is increasingly a reflection of the accommodative monetary policy settings to date. The Reserve Bank faces a major challenge in threading the needle between imposing too much pain on the economy in the near term, and forcing an even harsher adjustment in the future," Westpac's economists say.

"The inflation rate surged to 6.9% in the year to March, from a tame 1.5% just a year earlier. What’s more, the seemingly relentless rise in prices is shaking people’s confidence in a return to low and stable inflation over the medium-term."

The Reserve Bank is next due to review the OCR on May 25, with Westpac expecting a 50 basis points increase on top of April's 50 basis points hike. The economists also expect additional 50 basis points increases at the July and August OCR reviews.

"We acknowledge that four in a row would be virtually unprecedented in the era of inflation targeting - but then, so is much of what central banks are facing today. We’ve also lifted our forecast of the peak OCR for this cycle from 3.0% to 3.5%. We expect that to be reached by the end of this year, with two more 25 basis points hikes at the October and November reviews," Westpac's economists say.

"Our forecast is similar to the 3.4% peak in the Reserve Bank’s most recent published projections, but it’s still some way below financial market pricing, which has implied a peak of well over 4% at times. Obviously we think that market pricing is overdone - the high degree of leverage in the housing market means that a little will go a long way when it comes to raising interest rates. Even so, our forecasts agree that more will be needed than we thought a few months ago."

BNZ's economists, meanwhile, note NZ swap rates fell by between 25 basis points and 35 basis points last week. They say financial markets have started to question the aggressive rate hike profile built in for the Reserve Bank given growing questions about the global economic outlook and further evidence of a sharply slowing NZ housing market.

"The two-year swap rate, which reached as high as 3.995% just over a week ago, ended last week at 3.55%. The market still prices a high chance of a 50 basis points hike at next week’s meeting, but the implied probability of 50 basis points moves at subsequent meetings has been pared back," BNZ says.

"The market is pricing a terminal rate for the Reserve Bank of around 3.75%, well down on the 4.25% levels seen a week ago, but still much higher than the 3% peak in the OCR we have pencilled in for later this year. We think there is scope for a further pullback in NZ rates if the Reserve Bank doesn’t validate the market’s elevated OCR expectations at next week’s Monetary Policy Statement and global rates can stabilise."

ANZ's economists see the OCR peaking at 3.50% early next year, with their ASB counterparts picking a 3.25% peak. Kiwibank's Chief Economist Jarrod Kerr is forecasting a 50 basis points OCR increase this month, and a peak of 3% in November.

"And that should be enough. With house prices likely to be off 10% by year end, and most of the mortgage book refixing between now and then, the RBNZ is getting big bang for buck," Kerr says.

Back at Westpac Gordon & Co believe March's 6.9% inflation rate will be the peak in this cycle. Nonetheless they expect inflation to remain above the Reserve Bank’s 1% to 3% target range until the middle of 2023, and to occupy the upper half of that range for a few years beyond that.

"Our forecast implicitly assumes that the Reserve Bank will successfully thread the needle between doing enough to uphold its credibility as an inflation fighter, while not overdoing it and sending the economy into recession. That’s going to be extremely challenging, and it will require a careful understanding of the factors that have contributed to inflation, how persistent they will be, and how they will respond to monetary policy," Westpac says.

The bank's economists also reiterate their forecast for house prices to fall 15% over this year and next year.

"The impact of interest rate increases to date is already clearly evident in the housing market, with nationwide house prices down 5% since November and sales now back around pre-pandemic levels. With the OCR set to continue rising over the coming year, we now expect that house prices will fall by 10% over calendar 2022, with a further 5% drop expected over 2023 (previously, we had forecast house prices to fall by around 10% in total over 2022 and 2023)."

"A 15% drop in house prices sounds large compared to history, but to put it in context, it would only take average prices back to where they were at the start of 2021. That illustrates the ferocity of the rise in house prices during what turned out to be a brief period of super-low interest rates," says Westpac.

"The housing market is a key influence on households’ wealth and confidence. And just as the recent period of rapid house price gains boosted spending appetites, the slowdown now in train signals a period of softer spending growth over the next few years."

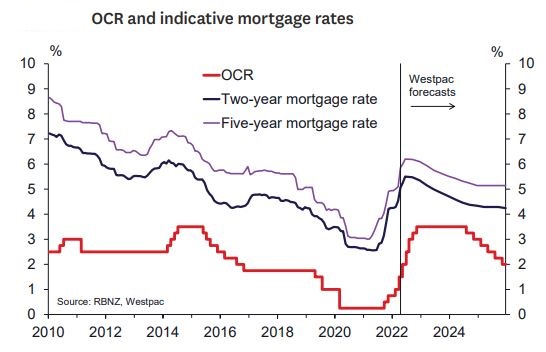

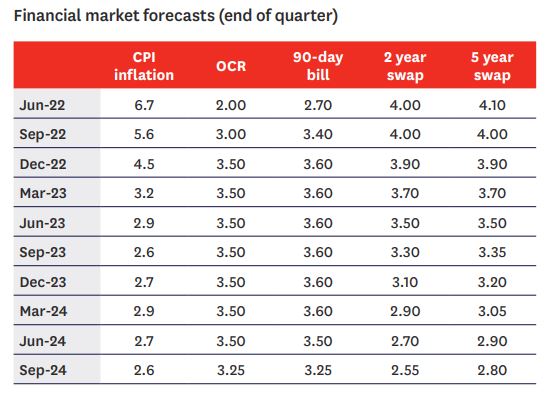

The chart and table below come from Westpac.

The link below will take you to Westpac's latest economic overview in full;

75 Comments

The economic slow down in NZ will be sharp and like housing will unravel faster than predictions. I hope we see an OCR of 3.5% and a decrease of 25-30% in property prices in the next 9 months. I still maintain that it’s the downward pressure on the NZD that will keep the RBNZ honest, not smart policy or a strong moral compass.

Bingo. But there will be no end to people trying to claim the credit, even when the PTA target is still being exceeded with little to no consequences (other than decimating household spending).

“With little to no consequences”

I suggest you actually read the PTA, and the RB act.

I can’t remember where it is since the review, but when the PTA was signed, under section 12 of the RB act, the RB can choose one, or none, of the economic objectives. Inflation, Employment, Housing stability.

They’re allowed under law to overlook inflation even if it’s 50%

You goons just don’t know what you’re talking about.

So how do you see all of this playing out then, JLM?

The five stages – denial, anger, bargaining, depression and acceptance – are often talked about as if they happen in order, moving from one stage to the other. You might hear people say things like 'Oh I've moved on from denial and now I think I'm entering the angry stage'. But this isn't often the case.

I can’t speak for JLM, but how it will play out is that the RBNZ will raise the OCR but halt once recession and rising unemployment arrives. Probably late 2022 / early 2023. And then cut the OCR in early / mid 2023. I have said this for the last 6-9 months, where I will be wrong is the OCR will peak higher than I predicted.

House Mouse - I doubt that whatever the RBNZ does it will have little if any effect on interest rates which are largely reflective of International rates that look to increase substantially as the Fed tightens and a liquidity crisis follows on top of a recession. Inflation will be impacted by the War in Ukraine and reduction on fertiliser and increased cost with planting already behind so the N Hemispheres production is likely to be down. The NZ$ however is more difficult as it may depreciate as risk off may become the norm so if our commodities remain in demand the trade gap may decrease and the tax take increase. I suspect NZ will be less affected than others but the tidal wave will still wet us and hard assets will be the best form of lower risk as the price may fall but the value remains.

Exactly.

I agree that the economic slowdown is going to be massive and much faster than seems to be being predicted.

Having recently rolled over a portion of our mortgage from an expiring term, we are now paying ~$100 per fortnight more so have less to spend at local businesses etc. But actually what this has done is highlight to us that we really need to cut out most of our expenses to clear as much of the mortgage before it comes off its next term which is fixed for 3 years...

So the net effect of the mortgage rate increase is actually that we are going to take out almost all of our discretionary spending out of local business at a time when the local businesses need the extra revenue to recover their costs which are being driven up in this inflationary environment. Everyone we know with mortgages is doing the same thing, so is there not a massive risk that in continuing to raise interest rates we are not waiting long enough to see if the medicine we have given the patient is having any effect before giving them another dose?

100% agree with you. It’s that additional ‘save’ on top of the rate increase that could kill off many businesses. I’m the same, back to free fun only (hunting, diving etc) for the next few years.

Yeah lots of trips to the beach for us. I do feel bad for anyone with a business that relies on money leftover after mortgage/rent, food and transport costs.

It is one of the reasons I just cannot understand why they are looking at introducing congestion charges to Auckland CBD. Any restaurant/bar located there effectively has the added cost of parking, fuel and soon to be congestion charges to compete with their equivalent located out in suburbia

congestion charging is for the whole of AKL. It's just being rolled out in phases, with the CDB the first. A slim majority of people travelling into the city centre do not drive in, so the effect may be less than you expect

I'm the same - free fun and saving every $ I can.

back to free fun only (hunting, diving etc)

This is all I have ever done, have I been missing something?

free fun only (hunting, diving)

Hunting without any weapons and diving without any gear, KiwiTim, you are the man!

Haha yea ok you got me there, my bullet expenses are minimal though due to being a terrible hunter.

MidNZ did you not realise rates would go up from emergency levels and will probably go up considerably more.

DTRH I suspected the rates would come back up from the emergency levels, but having watched the housing prices go well beyond where they should have ever reached I did wonder if the housing market had become "too big to fail".

MidNZ RBNZ has to follow the FED or basically NZD will lose value and our housing market is tiny compared to world markets, unfortunately in my opinion and looking at other information this housing market is way over valued when a house in Auckland is 12 x average wage couples income, it hit the top end of 2021 and will spiralling down for a number of years. I know it’s tuff but similar downturn happen in uk early 1990 and it took house prices 10 years to recover this could be a lot worse as debt levels are so high.

DTRH don't get me wrong I absolutely agree with you.

If I had had the option of buying a house 15 years ago compared to when I purchased 7 years ago I would take that offer any day of the week and almost be mortgage free by now.

But for future generations I do hope that house prices plummet to the point where average people can buy average houses for living without having to take on crippling levels of debt.

Its just going to be a rough ride for the next few years...

Mid NZ - The 6% reduction in credit card spending confirms that.

7% mortgage rates.

-30% price drops by Christmas. Guaranteed.

Be quick!

Everything in this article suggest rates won't get to that point...

Don't expect them to come out and admit it's worse than it is - they know sentiment plays a major part in outcomes.

Best they can do is publicly forecast in a way that they don't look completely stupid when their projections are wrong.

They have an abysmal forecasting record.

You forgot to log in to your other account when you posted this..

Any sane person who has some basic understanding will know that 0.5% rise is must for the situation and one does not have to be an expert to forecast.

Also RBNZ is raising as is forced and can no longer fib about the situation. Give one slight excuse and RBNZ will be happy to use that to raise by 0.25%.

They have picked 8 of the last 2 recessions

Looking like 7% interest rates might not be guaranteed this year?

It feels like Westpac wrote that article at least a month ago. 6.9% inflation is not new, what is new though, is the big swap rate retreat.

It is actually over 7%. It was artifically lower because the goverenmtn decreased fuel tax, and they admitted this drove it lower than it would have been.

Hoping for some advice from the panel-

I am sitting on some cash and wondering on an effective investment strategy. Historically I have invested in commercial property but current cap rates of 4.5% don’t appeal.

Am I best to put in term deposits (and if so when) for 12 months and wait for equity/property markets to bottom out?

Zero interest in Bitcoin/NFT etc

I hope that anyone giving you advice will disclose their experience in the field in number of years and amounts of money made, rather than just giving you their "opinions".

Amounts of money made doesn't indicate a solid plan. Many people have made millions in crypto in the past few years.

Also, it's super easy to make millions of dollars per year. Start with a hundred mil, put it in a TD and you're done.

Hookers and blow.

Sadly cocaine is probably a better store of value at the moment than the NZD.

I personally am happy to sit in cash, and see how things play out (family members own their own homes). No long term equity holds, will still run mean reversion systems both long/ short.

If in term deposits I would check the level of government guarantee. Often a max amount at each institution will be covered, so may be worth splitting amongst multiple banks. If I had to pick one Kiwibank would likely be the safest in a banking default environment.

a max amount at each institution will be covered

When? I thought term deposit guarantees were still in just the discussion phase.

TD is a virtually guaranteed return (some might argue with that), but still in the negative when adjusted for inflation. Kiwibond has even worse returns.

I think in the current environment you should aim to minimise your losses, at least until next year.

That said, dollar-cost-averaging into the stock market has a proven track record over long terms (10+ years). I'm 90% into TD, 10% into US stock market at the moment (negative returns on both this year, adjusted for inflation). I'll keep buying commodities derived funds and reverse indexes.

Safest of all is Kiwi bonds.

Sure, our money has always been safe in bank term deposits in the past... but these are unusual times.

Are you more focused on getting a return on your money, or a return of your money?

Short term the Aussie Banks in NZ are probably safe with the $Billions of profits, mortgagee sales however would concern me if they relate to recent purchases and prices fall 20% + as mark to market may have unexpected results - unsure what % of a Bank loan book would have to be in default to trigger a mark to market of the mortgage book?? Any suggestions from our Banking Gurus.

If I was looking for "classic" form of investment I would probably short the German Bund, right now, with a leveraged instrument. ECB is late to the party and it is extremely unlikely that it could go the other way.

Shorting is considered an aggressive for of investment... so well, up to you. That is what I would do with my money if I wanted look at it.

Currently I am doing dual investments on binance, but you said that you are not interested in that :D

Invest in residential housing before the end of the year ...

interested in forex trading? showgirls dollars are looking strong

Cast your net wider. Commercial should get you closer to 8-10%.

Just be careful if you need a long term tenant who they are and what they do.

No way the OCR peak is going to stop at only 3.5%. The peak will be at around 4% if not over and beyond it. And if the RBNZ does not intervene with extreme swiftness and determination, they will be forced to go even higher. Inflation is truly out of control, and only an aggressive tightening will be able to control it in the longer term.

fortunr, NZ certainly needs to reset and I hope we get there - I just don't see Orr having the constitution to face the wealth effect being washed away as housing passes through a 25-30% drop. If the economy goes into reverse as folks here are posting then that's just the excuse he needs to plateau and even sneak back 0.25%. Heart hopes for 4%, head says it'll peak for a month or two lower and be wound back slightly to try and buoy the markets - Covid, Ukraine, supply chain issues bla bla bla all being wheeled out.

A 25-30% house price drop is already baked in.

Just look at the Westpac graph above. Two year mortgage rates are ALREADY back to where they were in 2015. That is not an estimate or a projection. That is real-world, right-now mortgage rates.

The house price drops may take a little while, but they will happen much faster than most people realize.

You simply cannot have 2021 house prices with 2015 mortgage rates. House price falls of at least 25-30% are inevitable at this point (although no doubt the govt will attempt to throw the kitchen sink at propping up the housing market).

Be quick.

Wages have increased somewhat since 2015 as well. Consumers can afford to carry more debt.

Certainly. That's why I was careful to not say that prices would go back to 2015 levels. But they are heading in that general direction ⏬.

Lots of other factors play into it too, like animal spirits, cost of living...

Squishy - 2% extra on an average mortgage of $500K is $10,000 after tax i doubt those on $100K + have seen a 10% salary increase.

If you are making 100 K and contributing 3% to Kiwi Saver. You are taking home 71 K. You need a 16% pay rise to 116 K gross to take home 81 K and not go backwards to cover an additional 10 K of interest expense.

With world events and the way NZD is being pushed down 50% too 60% house price drops are more likely over next 18 months.

12 out of 10 Economists would disagree, add in bank economists and its 15 out o 10 anyone suggest the number if central Bankers are included??

I find it hard to see how the CPI will track down come March 2023.

We're not going back to global supply chains pre pandemic ever, let alone next year.

China's covid response is a massive failure in terms of getting back ever to a low inflation global economy. Good luck with that.

Moving to renewables is going to cost. Europe, US, everyone.

The forecasting above assumes going back to the old normal next year.

Because New Zealanders have $320,000,000,000 of mortgage debt. 500,000 of those mortgages were written since March 2020 at historically low interest rates. Now all that debt is being repriced. Every day hundreds of households are facing big increases in mortgage serviceability costs. 1.5% rate increase on 320 billion is 4.8 billion. a year or $13 million a day or 2.8 million flat whites a day.

... puts the supermarkets to shame , doesn't it .... banking is where the rivers of gold run wide & deep .... .... good for Australia !

GBH - I wonder if Robbers Son has thought of a windfall tax on banks & fuel co's I would suggest a levy (note I am moving away from calling it a tax) starting at 50% on top of Corp tax, would certainly help swell the coffers so grunter can dream up more ways to waste. Sarc - or perhaps not!

Is that popcorn burning that everyone can smell...

Rates are at very low historically with inflation high double digit rates would be the norm. People will have to understand they paid way too much for house as old values will not be coming back for years could be decades unless inflation keeps raising at which time petrol will be $15 a litre.

A deep recession will be pretty deflationary.

...leverage in the housing market means that a little will go a long way when it comes to raising interest rates.

I'm not sure if housing will have the impact many expect given house prices (or proxies thereof) aren't included in the CPI index? This hypothesis seems predominantly driven by the idea that house prices are somehow connected to consumer spending. However my observation was that house prices only seemed to have a very marginal impact on consumer demand when rates where dropping and prices rising.

Much as to say most consumer spending is done whether their houses are valued at $1 or $1m, people view their house as the place they live an not an investment.

House prices are connected to consumer spending in that higher house prices are likely to lead to higher mortgages.

Higher mortgages with increasing interest rates leads to less money leftover to spend as a consumer after paying your mortgage

Inflation hits twice for a mortgagee. So as you say, the higher interest rates cause less money left over for consumer spending, and inflation means that money left over doesn’t go as far. At a point, the pressure of a high CPI push down on the ability to service debt as a larger portion of income is needed to cover the basics.

Well said Malamah

RBNZ's research paper into the housing wealth effect:

Household Leverage and Asymmetric Housing Wealth Effects- Evidence from New Zealand

Our main empirical finding is that, on average, the elasticity of the consumption growth to housing price changes is 0.22%. This corresponds to 3 cents out of one dollar in terms of marginal propensity of consume out of housing wealth. In addition, we find that the housing wealth effect is asymmetric with respect to positive and negative housing wealth shocks. The housing wealth elasticity is 0.23 for negative shocks, as compared to 0.13 in response to positive changes in housing wealth. We contribute the asymmetric housing wealth effect to the influence of household indebtedness. The intuition of the finding is that leveraged gains might mostly be used to pay down debt (precautionary saving effect), whereas leveraged losses have a more direct bearing on consumption (collateral effect).

Contributing very little on the upside, but having a more pronounced effect on the downside.

https://www.rbnz.govt.nz/research-and-publications/discussion-papers/2019/dp2019-01

Interesting, thanks for sharing.

I saw recently bank of England predictions of inflation at 10% , I wouldn't be surprised at similar results here. A few tradies I know are charging rates undreamed of $80/hrs plus citing their costs such as fuel etc. This is hard to see as sustainable, borders will open soon and wages will no doubt be forced down again. The predictions of economists has fairly consistently been on the downside as not wanting to frighten with reality .

Howdy everyone, finally opened an account and decided to participate in the meme that is now the NZ Economy.

I'm curious, how many of your friends are still confused about the direction of the market?

Seems people are still banking on migration inflow without looking at outflow and lack of "supply" (Cheap Credit) are we this stupid or just in denial?

Denial.

It's been such a golden run for speculation those leveraged up just cannot believe it can go the other way. Though leverage does exactly the same math in reverse, the actual decrease is often more dramatic.

Yip, couldn't agree more Averageman. I consider my peers fairly intelligent, but the rose tint is so strong along with the short term gains which are about evaporate.. One comment I heard was, it'll be a short term blip, 10% at most. This was after the May REINZ report smh. (They purchased last year)

Why not both?

A bit of quick maths suggests the supply of credit (based on interest rates) is down nearly 30%.

- $800k mortgage at 2.5% (2yr) over 30 years = $729 per week

- $573k mortgage at 5.25% (2yr) over 30 years = $730 per week.

I would make an allowance for wage inflation, but CPI has taken that.

Sounds right. Lots of middle class people we know are already hurting and cutting back on their expenses (especially those with investment properties). I remain quite stunned most people seem to have sleepwalked into this.

Maybe we should take a leaf out of the Americans book? https://www.cnbc.com/2022/04/22/nearly-25percent-of-us-students-have-ac…

Agree.

So someone who was borrowing $800000 (Assuming Million dollar house with 20% deposit) and can repay $730 for mortgage, can now afford to buy house upto $725.00.

So a Fall between 25% to 30% is possible. Even if buyers stretches themselves with FOMO memory - still fall of 20% to 25% is forgone conclusion.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.