A 4.0% Official Cash Rate (OCR) for Christmas is virtually signed and sealed. We just need to wait for it to be delivered.

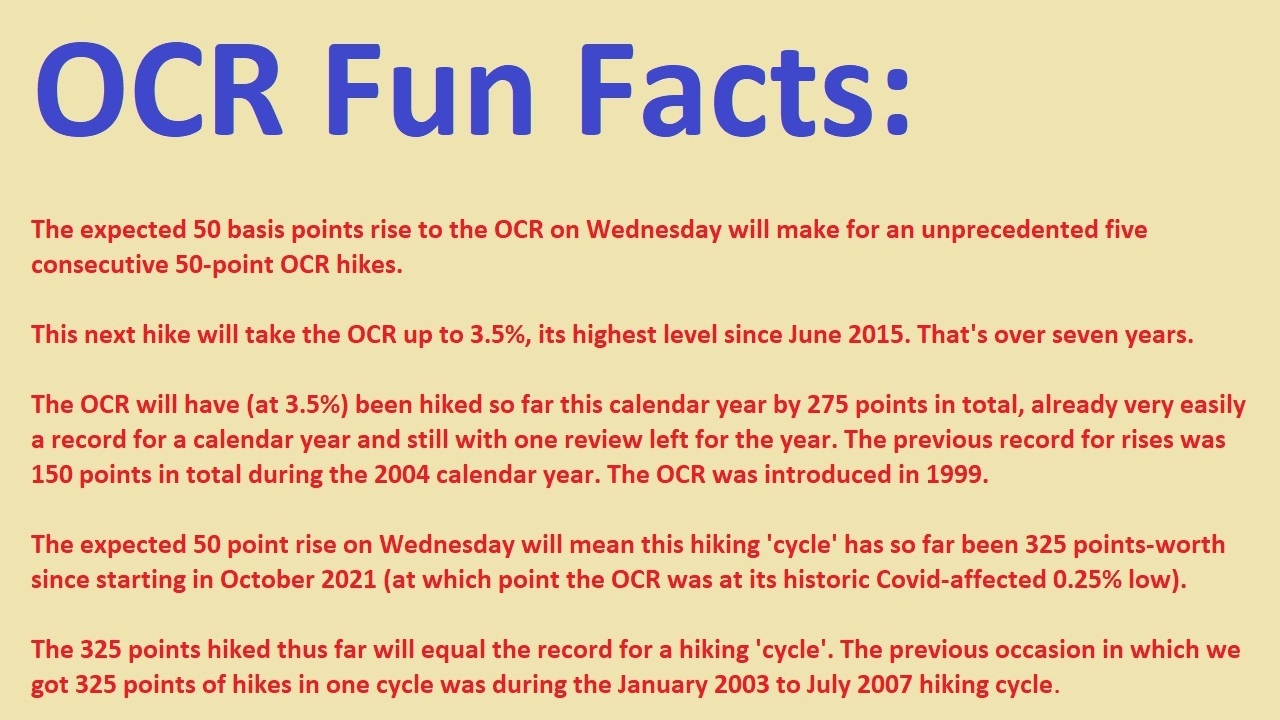

The first instalment will be in the coming week (Wednesday, October 5), when the Reserve Bank is universally expected to crank up the OCR by another 50 basis points (making FIVE such rises in a row) to 3.5%, unless something very untoward happens between time of writing and Wednesday.

(And of course, with 'untoward' events almost commonplace at the moment, we shouldn't rule out anything. Remember, in August 2021 the RBNZ's start of this OCR hiking 'cycle' was hijacked by the outbreak of Delta in Auckland. So, the first hike was in the end not till October.)

However, all things being equal, we will get the 50 point rise this week and another to follow on November 23 - which is the last OCR review for the year.

The first review for 2023 doesn't come till February 22. A long time between drinks, as they say.

I have carped previously about the fact the gap between the last OCR review in one year and the first review in the next year is now so long - I mean, three months, basically.

On THIS occasion, however, the RBNZ may well relish the opportunity to sit on the beach for a few weeks and watch what the world does before coming back afresh to decide whether it's up, down or sideways for the OCR next year.

And it is fair to say that market thinking on this subject is now becoming quite spread.

The context, lest we forget, is an annual inflation rate that hit 7.3% as of the June quarter. That's a bit on the high side for a central bank attempting to keep inflation in a 1%-3% range, with an explicit target of 2%. According to the table of economic forecasts in the RBNZ's last Monetary Policy Statement in August, the central bank's not seeing inflation creeping back under 3% till June 2024.

Between its last OCR review in August and now, the RBNZ hasn't had too much major economic news to digest.

The GDP figures for June, released earlier this month, were a surprise (+1.7% for the quarter) to a lot of people - but NOT the RBNZ. It actually had a market-leading pick of +1.8%.

There's been no Consumers Price Index inflation figures out recently, but the August food price figures showed a whopping 8.3% annual rise. So, inflation is still very much with us.

As per the August Monetary Policy Statement forecasts, the RBNZ is picking a 'terminal' OCR of 4.1% by the middle of next year. So, at the moment, it is hedging its bets a little between a peak OCR of 4.0% and one of 4.25%, although Deputy Governor Christian Hawkesby subsequently conceded to media that a 4.25% OCR was certainly possible.

Of course, the markets are now running ahead. At time of writing the wholesale interest rate markets were actually pricing in an OCR of 4.75% by the middle of next year. ANZ economists are now picking a 4.75% peak, while other economists have also been moving up their forecasts, with probably the most common perception now around 4.25% - but with 'upside potential'. Fixed mortgage rates - which had eased back a little - have been rising again.

An unwelcome development in the past couple of weeks has been the rampant rise of the US dollar in reaction to an even more 'hawkish' than previously US Federal Reserve. Our gallant little Kiwi has been getting eaten alive, along with most other global currencies. At one point the NZ dollar dropped under US56, though at time of writing it was back up just above US57c.

A falling currency increases the cost of imports - and that leads to more of that nasty old inflation. So, the suddenly much weaker Kiwi dollar is unhelpful.

It was perhaps instructive that RBNZ Governor Adrian Orr directly referenced the decline of the Kiwi against the US currency in a speech in Wellington in the past week. In fairness, Orr seemed pretty relaxed about it, but the real point I think is that if an RBNZ Governor is talking about the Kiwi dollar at all then they are probably not comfortable with the situation.

For the moment though, Orr is maintaining that the OCR tightening cycle is very mature and "well advanced", with "a little more to do" before the RBNZ can drop to its "normal happy place" of watching, worrying and waiting.

These comments would appear consistent with a central bank at the moment still maybe seeing its work done with an OCR of 4.0% before the end of the year.

But I think there's no doubt that could change. The global situation is now looking even more volatile. And therefore the statement on Wednesday, October 5 is going to be heavily scrutinised for any perceived changes of emphasis.

Remember, this week's OCR review will not be accompanied by a full Monetary Policy Statement. For the next one of these, we have to wait till the November 23 review.

The key thing to watch from this week's statement will be any sign that the RBNZ is veering away from what it forecast in the August MPS.

I would expect the RBNZ at this stage will maintain a straight bat and make a comment along the lines that it is:

comfortable that the projected path of the OCR outlined in the recent Monetary Policy Statement remains broadly consistent with achieving its primary inflation and employment objectives - without causing unnecessary instability in output, interest rates and the exchange rate.

That last bit of text is actually verbatim from the RBNZ's July OCR release, when the bank was looking to convey that it effectively had not changed its forward projections for the OCR track.

I could be wrong of course. And the cat would be well and truly put among the pigeons if the RBNZ threw in a sentence saying the opposite of the above.

But I would be surprised. And if the RBNZ does want to change its mind about the future path of the OCR then it will likely want to wait till November 23, at which point it will be producing a full Monetary Policy Statement and can explain itself at length.

Another good reason for waiting will be that after the October 5 OCR review we will see the release of the September quarter inflation figures (on October 18) and the September quarter unemployment and wage figures (on November 2). Both of these things will be huge and will have an enormous influence on the RBNZ's thinking.

So, it is well and truly the time for keeping eyes and ears open.

For the week ahead we can anticipate a move up for the OCR to 3.50% from 3.00%, accompanied by a 'steady as you go' message from the RBNZ.

Then on November 23 we will see the OCR moved up to 4%, accompanied by, I suspect language that will leave the door open for at least a 25 basis point rise in February.

And then after the RBNZ's had those weeks at the beach the fun all starts again next year. What is the global situation going to be looking like at the start of 2023? Do we really want to know? Which way for the OCR? Up? Down? Or sideways? Oh, decisions, decisions.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

121 Comments

So if a special certain prophet is a good boy for the rest of the year, they might wake up on Xmas morning to their very own shiny new 7?

Santa going to deliver early on that to avoid the Christmas crush and supply chain disruptions

It's the prophet's birthday on Xmas morning. He will get double the presents.

All comes down to inflation. Latest sept quarter due out this on the 18th im picking still high at over 5.75%.

Hard to see a significant reduction in inflation due to NZ$ depreciation of 20% and oil price falls less than 20% so the oil price spike will be some way ahead before the higher values drop out the stats. Lower $ good for exports which look stable but unless imports are reduced the trade balance will be uncomfortably negative putting further pressure on the currency. Mortgage cost increases now look worse will a 3 year rate at 7% likely and the pain and diminished spending will have a domino effect and increases in unemployment. Stats NZ currently quote unemployment at 3.3%= 90,000 - job seeker benefits are 100,086 per stats NZ so the real unemployment figure is 7% and rising.I pray for a recession as I fear a depression.

So, OCR decision on the 5th and CPI data on the 18th.

Dumb question - why don't they have the OCR reviews AFTER the CPI data, so they can base the decision on the data?

Decisions are made irrespective of data

Dgm, it was that way in 2021 when Orr ignored the rampant house inflation to unsustainable levels, seems everybody else saw it arrive 12 months before he acted.

CB's seem to do what their counterparts do.. rbnz just followed blindly..

There are families paying for their errors, yet they are not accountable

It's a double whammy for the nation to have both our most incompetent government ever , at the same time as the most incompetent RBNZ ...

... Tane Mahuta's doing just fine , apparently ... I'm glad something is OK in Godzone ...

The government has tweaked the RBNZ every year it has been in power. Adding maximum sustainable employment, instruction to consider house prices, switch from governor decision making to committee, mandate to keep house prices sustainable, replacing technical members of RBNZ committee with political appointments… when you say the RBNZ is incompetent, if is basically having its legs knocked out from under it before it can even recover from each of the previous blows!

Without a PHD in thickology you will never understand the thinking of Orr or Robbers son.

It should be minimum 75 Basis point rise, if not full One as time is now - what happened to Mr Orr's LEAST REGRET approach.

NZ$ below US$ 50 cents could be a reality.

https://www.macrobusiness.com.au/2022/09/new-zealand-housing-crashes-in…

Best scenario is another 10% fall from here on.....by itself is gloomy........

This is when 56% of mortgages are in for refinance from appox 2.6% to 6.6% plus as will only know in future based on where Fed stops raising interest rate.

Wait and Watch

Might rush out and drop 900k on my dream Auckland home. You cannot beat the vibrant nouveau kiwi lifestyle.

https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

Ashley 'Snake Oil' Alexander told me that it will double every seven years and Tony 'Combover' Church says 5% this year because zero rates are here to stay.

I'm very fortunate to have the PIJF funded NZME "property experts" to provide such superb financial advice from honest unvested interests.

Look at all the DGMs above and below. Wouldn't know a trailer home fit for a millionaire if it bit them on the backside.

Good news, Brock - homes.co.nz has that property at a cool half mil, and given their estimates are usually way too high, you should be able to pick it up for something starting with a 4.

That's down over $100k since January, and $20k less than what the current owned paid for it in June last year. You can spend some of that $900k at Costco furnishing your 93 square meters of suburban paradise instead, just avoid the temptation to spend it on a nice new Tesla - there's no garage to charge it in, and the off-street parking might still be too far from the router to download the software updates. Don't want that handbrake randomly activating on you!

Take it from Tony and Ash and get in quick.

That will be the bare carpark price before the trailer home was delivered.

It's only an hour's drive from Costco with yesterday's traffic in that area.

And then wait in a queue for an hour.

In order to save $300 on $1000 worth of shit you didn't need.

and even worst, Costco is not even cheap compared to PnS and Countdowns.

Except everything I've seen posted is either much cheaper, or at least slightly cheaper on a per unit basis. What are basing your claim of not cheaper on?

You'll be sorry you didn't buy that tidy home today at today's cheap prices. Talk to me again in 5 years when today's prices look like... I don't know, children's toys.

All these armchair economists have never owned a home and never will. The envy is real. People are jealous at us and our winning ways. Sour grapes much? You wanna be a winner? Join the winning team. House prices always go up in the long term. This is an opportunity! You'd be a fool not to take it. Don't try to time the market. Nobody can predict the future. house prices always go up. Nobody can predict the future. House prices only go up. Nobody can predict the future.

Yeah, you definitely sound like a 'winner'.

I wouldn't agree with you there, predicting from now to Christmas is not looking very difficult, odds on house prices are going to fall further and at best will be flat. Two more OCR rises of an insufficient 0.5% because that's what the RBNZ "Signaled" near the beginning of the year to give the 60% of mortgages that were falling due this year time to re-fix at at least a 3 year term. No the really big question is where this is all heading come Feb 2023 and if inflation is not steadily trending downwards by then we are in the crapper.

yes still a lot of mortgages yet to roll over and double.

The prophet had the answers. He was cancelled for our sins.

...And the banks have still access to the FLP money!

What did you smoke this morning?

... dunno what he's smoking , but dont we all wish we could get some of it ... a coupla puffs , and you're an instant comedian ...

I think this is an instance of Poe's Law.

In this case I believe it is parody due to the last three sentences where the writer claims you cannot predict the future, predicts the future, then reiterates you cannot predict the future.

... ah , I am informed ... thank you ...

One certainty when it comes to house prices in NZ is that the future isn't what it used to be ...

Smoked granite

Crushed up and snorted methinks. The smoked part was for flavouring.

Careful with the sarcasm, SG. You might fool people.

Nice slab of concrete, too. Development potential?

I love how all those windows have magnificent views of the neighbor's wall.

"...unless something very untoward happens between time of writing and Wednesday."

David, RBNZ under Mr Orr will only look at any untoward incident, if it favour raising by less than 0.5%.

Untoward is already happening for him to raise by more than 0.5% but will he...you too knows so can easily predict what RBNZ will do.

to Infinity and beyond

if it is slow and steady and another 50 basis points on wednesday,there might not be a fairytale ending to our tortoise and the hare method.

Why all the beige pictures all of a sudden... hidden meaning? Seeing life in beige?

0.5% OCR rise is baked in, and look where the Kiwi closed on Friday - 0.5598 - with that next OCR already in that exchange rate.

Doesn't that tell us that if we want to avoid 0.5000, or lower, then 0.5% on Wednesday isn't going to help one iota?

Via Mauldin this morning:

With the Fed on a path to get us to a 5% fed funds rate, the other central banks need to recognize this. Powell is not responsible for fixing the chaos that passes for monetary policy in Europe.

yes chance of 0.5% rise this week is 99.9% in my book

Orr was quoted as saying his work hiking the OCR is nearly done.

I think he will stop at 4

I dont think he can stop at 4 next year if inflation is still over 5, I think Zollner ANZ may be right again. I cant see a quick end in sight with Putin, it may be slow and painful, oil , fertilizer and food to stay high.

If it’s not much over 5 % then it’s really not the end of the world, hardly worth tanking the economy for. Sure if he hadn’t just increased the OCR quicker than ever before then he should rise, but there is no point in pushing the brake pedal through the floor just for 5%.

I disagree JJ, 5% inflation is not accepted by central banks of stable economies, the inflation wage growth spiral is feared by central bankers (and employers!!)

It’s not acceptable in the long term. But do they keep pulling the emergency brake if the train is already slowing to a stop? At some stage the emergency brake will catch the whole train on fire.

True JJ. RBNZ is seeing the emergency brake coming off 'mid 2023'. Yes, next years OCR meetings will be interesting because they will not be foregone conclusions like the next two.

Orr was quoted as saying his work hiking the OCR is nearly done.

He has however been known to change his mind occasionally!

Good caveat David about ‘untoward’ things. It’s certainly a time that caveats are a wise thing to use.

putin has had another embarrassing defeat….

September quarter inflation figures will include the big drop in fuel prices. Fuel must be down over 10% from well over $3 at one stage. On top of that the September quarter from last year was huge and will drop out of the yearly inflation. Could we see a big drop to say 5% annual?

The last 3 quarters add to 4.7%. So anything less than 0.3% this quarter takes annual down under 5%. Could the big fuel price drop take this quarter down to this level? Sounds feasible to me.

Not at my fuel station, most of the drop in barrel price has been lost to the US/NZD exchange rate drop. Without the temporary govt subsidy, fuel is still about $2.90 a litre.

Even with the subsidy it was over $3 last quarter in Auckland, pretty sure I can remember paying about $3.20 at one stage. Now down to about $2.65, over 10% down.

The gull after Tokoroa had it at $2.21 the other day! $2.22 now according to Gaspy.

JJ the inflation analysis is year on year, this time last year it was $2.30, sept quarter this year at $2.65 is still over 10% inflation 'year on year'.

Yeah I get that. But last quarter it was up over 20% and we had 7% total inflation. With it now up “only” 10% that 7% total will be a lot less.

True

Petrol prices make up around 3.57% of the CPI index - so a 20% fall would have a negative 0.714 impact on CPI. However, it is the knock-on impact of high oil / fuel prices on other goods that really matters. For example, fuel, plastics and fertiliser (all driven by oil prices) are key drivers of higher food prices, which make up 18.72% of the CPI. Hence, that 8% of food price growth adds 1.5 percentage points to CPI. Over the last 20 years, changes in petrol prices have been highly correlated with changes in NZ CPI (correlation is 0.88!)

When / if oil prices come down, this period of inflation will stop and we will be left with the usual suspects driving the usual background levels of CPI (e.g. rents reliably contribute 0.3 to 0.45 points to CPI, house building costs another 0.25 percentage points, local govt rates another 0.14 etc).

Best thing the Reserve Bank could do to tame inflation would be to directly finance a transition from fossil fuels and a huge increase in publicly-owned housing. Alternatively, they could wiggle the OCR around - pretending that their little orr can steer an international oil tanker.

CPI is annual average so it takes months for highest figures to drop out.

That’s one of the reasons I think annual inflation will be quite a lot lower by autumn 2023.

Not only fuel but other things such as build costs (as the construction sector tanks, plus supply chain pressures relieved) and rents.

I think even food cost inflation may have moderated by autumn 2023.

probably wages too, given there was a big hike this year in April/May.

But what do I know, almost everyone thinks inflation will be 5+% in 2023 and beyond.

Anecdotally there’s also been big hikes in hospo this year, I don’t think further hikes can be sustained.

Just an anecdote, a couple of Chinese and Vietnamese joints that we frequent have hiked their mains from circa $15 to circa $18-20 over the past two years. We frequent them much less, and would hardly frequent them at all if their prices went up further.

Wow those prices are tough for a guy by his own admission is on $200K plus a year. I can recommend the "Spicy Thai" Fantastic Noodles as a substitute from your local supermarket.

That’s snarky.

Just because I earn well doesn’t mean I am

silly with money.

The point was an anecdote about inflation in hospo.

Trust your car is like mine. Honda 2002 with 180k on the clock. I like parking between my work colleagues SUVs and the odd Euro car.

Drive the cheapest car your ego will permit. My ego is about $1500 :-)

200k isn’t much these days depending on the mouse family’s situation.

Meeh, the 18-20$ meal is the new 15. Just like few years back it was around $12.

You will still go there next year even at $22 because it would cost you $30 per head by buying the ingredients at the supermarket and doing it yourself.

I will go there far less if it goes up another $2 per meal…

I agree further hikes may not be sustainable but probably have to continue anyway because the current economic/financial model cannot be sustained.

Here's the kicker though. For economies to work best money needs to flow and cycle around much like oil in an engine. Money pooling into the FIRE industry/wealth accumulation at the top and being artificially pumped in via debt creation at the bottom is literally seizing the engine. In addition the quality of fuel/energy is also lacking and/or leaking at many points, the plugs and injectors are fouled, nuts and bolts are loose all over, and the computer diagnostics are also faulty. Oh, the radiator might be bung too.

And the instruction manual/economic theory was not only written for an entirely different machine and never updated, but also in a language the mechanics can't understand.

Mwaaaahh!

NZ$ cost of oil still higher than before the reduction.

Under Mr A Orr's leadership, in the first year of COVID, the OCR was slashed by 75 bps. A good move then, and now.

Not too sure about LSAP.

Unhappy, today, that the RBNZ did not act in 2021, when inflation was running away and house asset inflation was hurting NZ.

Today, methinks that RBNZ is too cautious, comes a point when we have to face the storm.

With NZD tanking this will raise inflation, NZD dropped 2.3% on Friday if FED and rest of the world are raising rates we have no choice but to follow or inflation will never go. If the NZD is not protected it will be like blood in the water and the sharks will destroy the NZD then we will have to raise rates very quickly and much higher. I think 1% rates raise next week would be wise.

Is Orr wise, or just interested in protecting his banker mates and upper class's wealth?

Yes it was that way in 2021. Orr still has a strong inclusion of the investment side of things, as we knew from his days at NZ Super Fund. There are many (including former RBNZ staff) who would prefer a more conservative governor. Im sure he now regrets his 2020 comments virtually giving financial advice for NZers to "find other forms of investment",ie into the asset bubbles.

It is the banker's bank and not the people's bank.

Agree. Quite worrying that there's effectively no review over three months - I wonder how many Fed reviews there will be in that time and how low the NZD-USD can go before RBNZ steps in for an "extraordinary" review. I expect we'll see that calendar reviewed this week.

I hope so. It really is perilous. If the $NZ was taking the kind of hammering the GBP has this week and the RBNZ were sitting on their hands because 'it's not on the calendar', well... It would be the most Wellington thing ever.

Yes the gap between nov and feb is a long time. We should review the OCR once a month bar january, its not difficult and markets can adjust easily with modern technology.

Not to worry we get the last of the cost of living payments today, all is forgiven, pretty sure its still enough to buy a bottle of Moet.

Audaxes.

What are you trying to imply?

This is a normal scheduled fortnightly meeting and the expedited procedures of the meeting are also standard - all of those meetings this year and last year were under those procedures.

KeithW

So are you bearish on inflationary pressures?

Or you are just posting this to provoke

Probably inflation.

The decline in the NZD has been occurring against all major currencies, not just the USD. More recognition of this would seem appropriate.

KeithW

... correct me if I'm wrong , Keith ... but the $NZ has held up against the British £ , the Japanese ¥ & the South Korean ₩ .... which are major currencies .... and significant trading partners of ours ...

Most global trade transactions are invoiced in just a few currencies – most often the US dollar, sometimes the euro – regardless of the countries involved in the transaction

https://cepr.org/voxeu/columns/patterns-invoicing-currency-global-trade

Correct. But the TWI is weighted according to source and destination countries and not to invoicing weights. And the TWI has been declining markedly this year albeit with volatility. Much of this is yet to flow through into NZD prices linked to inevitable lags which are further increased by exchange rate hedging.

KeithW

GBH,

In recent weeks we have declined significantly against the GBP and the yen, as well as the euro, the yuan and the AUD. And of course the USD. We are out there on our own right now. And we can see this in the TWI (trade weighted index).

There is no easy solution to the depreciation of the NZD. This is because the problems are profound. Just like medicines, there are almost always side effects.

The last 20 years have been remarkable for NZ because it has been a remarkable time to be in the 'food business'. It is still a remarkable time to be in the food business, but NZ's economic building blocks are not in place to currently take us forward as a nation. To simply place the blame on one government or another is to misdiagnose the problem, although the RBNZ has miscued very badly. But the overarching problems are more fundamental.

KeithW

Keith : I cannot recall a time when previous governors of the RBNZ came out and openly criticized the current governor as Orr has been rebuked ...

... nor can I recall a government who've racked up so much debt , yet with so little to show for it .

Exciting times ahead : luckily for us , folks gotta eat , and our produce is very cheap for them now .

The outlook for export prices once converted to NZD is reasonably strong, although a global recession will not help. The problem is that import prices have further to climb.

KeithW

Nor can I recall a society who've racked up so much debt, yet with so little to show for it.

Ya missed one.

Our folks gotta eat and our produce is very expensive for them now.

I do enjoy your comments Gummy. This ain't a dig at you.

The yen? It’s been yo-yoing between 82 and 86 for months.

Yes. But two weeks ago it was around 87. And right now it is just under 81.

That supports the reality that the decline of the NZD in the last two weeks has been profound.

While it is clear that the financial reef fish have moved specifically against the NZD in the last two weeks, and that this move is not just towards the USD, one can never be sure in which direction they will now head as they dart hither and thither. But the current 'thither' does seem to be more than the usual volatility.

KeithW

I can attest to this. Car I won at auction cost me $1,500 when I was invoiced for it a few days later. It would have been $3K cheaper a few weeks before that. This is all inflation that will come down the line to us and it isn't priced in yet. Buckle up, everyone.

Even a few months ago it was down around 82-83 at times. I know because I follow it closely.

You make it sound as if there has been a significant slump in the NZD against the yen when there hasn’t been. It’s been yo-yoing around.

I have no fixed view as to where the yen will go relative to the NZD over the next few months. Japan beats to its own drum. But I am saying that the decline in the NZD in recent weeks has been consistent across most of the major currencies. Therefore it is not valid to say that the overall fall in the NZD can be attributed simply to the strength of the USD.

KeithW

In the last few weeks we have slumped against the Yen. It was Yo-yoing but it's been all Yo lately. We have previously had divergence against NZD/USD when it comes to NZD/JPY but now they are moving together. The drop-off in April was nowhere near this fast. I have to go back to Feb 2020 to find a similar drop-off in the chart shape over a similar period of time. Given the prevailing circumstances since then, I think the current one is noteworthy.

The BOJ openly intervened a week or so ago to stop the YEN from getting crushed more (against the USD). The drop back down to 80-82 is correlated.

So, another pandemic can halt RBNZ from hiking ?

My guess is they will hike (to "do something") and then spray money around to the problems that seem worst at that moment. This is what being trapped comprises.

BOE flopping to QE, moments after they were about to start QT, because the bond market shat itself (because of years of rate suppression being released) reveals their true colours - all of them.

It ends in currency destruction, regardless of their OCR/price fixing attempts.

There is never any discussion in the media as to how the Reserve Bank actually controls the OCR and it is not done simply by an announcement of what it will be. There must be a financial control placed on the banks to achieve this and this is done by adjusting the levels of central bank reserves which the banks hold in their settlement accounts through the issuance or repurchase of government bonds.

Reserves are created in the first instance through the governments spending and which will cause interest rates to decline and so bonds are issued to reduce these reserves again and so borrowing is a monetary procedure and has nothing to do with financing the governments spending.

Standard and Poor's describes here how it works.

https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

Treadlightly,

Actually a change in the OCR is simply an announcement.

Some effects of this are automatic - for example the interest that banks earn on their settlement accounts at the RBNZ will change in line with the OCR change. Similarly the interest that the banks pay on their FLP funds which come from the RBNZ will increase.

Beyond that, the changes that occur are in the financial markets and depend on the behavioural decisions of those who play in those markets. Typically, if the OCR rises, then short term interest rates will rise but not necessarily by the same rate as the OCR. Medium term rates may also rise but typically by a lesser amounts. The direct effect on long term rates of say two years and beyond is relatively minor.

No, a change in the OCR is not accompanied by any financial control mechanism placed on the commercial banks.

Totally separate from the OCR mechanism are decisions by the RBNZ to either sell Government bonds that it holds (a process of quantitative tightening) or to purchase bonds that would otherwise be in the market (a process of quantitative easing).

The RBNZ does not issue its own bonds. However the Government does issue its own bonds, with many of these having been bought by the RBNZ, which is how QE operates and with this increasing the money supply.

The general lack of focus in the financial media on the QE/QT issues of the RBNZ in comparison with the intense focus on the OCR is indicative of poor financial understanding. The RBNZ should be receiving much more scrutiny in relation to its very modest plans to undertake QT by reversing the excessive QE undertaken in 2020 and 2021, and which still continues through the FLP programme. My own judgement is that getting inflation locked down so that it stays blocked down is not feasible without significant QT, and with this being greater than currently planned.

KeithW

Very well said and I agree fully with your comment about the NZ financial media! And on top of it is, that the final determination of any interest rate lies with the overseas investors in how far they are prepared to fund our continuous account deficit! A lot of people don't recognize this as an important factor how at the end the final interest rates are set.

I guess that Paul Sheard, Chief Global Economist and Head of Global Economics and Research at Standard and Poor's had no idea what he is talking about then? Perhaps this applies to you below.

A Little Knowledge is a Dangerous Thing. https://profstevekeen.substack.com/p/a-little-knowledge-is-a-dangerous

And you might like to reflect on what Paul Sheard was saying some 14 months ago.

https://www.bqprime.com/global-economics/the-great-inflation-debate-bac…

How did he get it so wrong?

KeithW

Because central Bankers think they are signal men and can pull levers to determine were the train goes, the levers have been disconnected from the points and the train will go wherever the passengers decide, to quote an old saying - " You just can't beat numbers" so if sufficient numbers decide to stop spending because they perceive the RBNZ and Govt are clueless no amount of preaching will change their decisions. I strongly suspect many such decisions were taken some time ago and are now being implemented.

Reserve Bank is universally expected to crank up the OCR by another 50 basis points...

I expect at least a FED equalling 75bps. We can't keep throwing consumers under the bus to protect borrowers.

My wife and I have had interesting conversations with two people recently. The first one is around 40 years old and he has sold all his commercial properties. He believes it is only going to get a lot worse for us in NZ economy wise. The second person is aged 50/51 and has a huge commercial portfolio that is fully tenanted and not highly geared. He is usually very positive in terms of life in general including the economy. He believes our economy is going to be in a very sick state of affairs next year. Further that many people will be in trouble over their debt levels and not just in housing. If the RB puts the OCR up to 4.5 per cent or more these two very successful investors might just be correct in their thinking.

Some good opportunities coming for those with spare equity, low debt, good cashflow and clear heads.

Agreed. I am seeing some evidence that some of the big boys and girls in that situation are currently focusing again, or in some cases for the first time, on dairy farm purchases. This will mean even more consolidation.

KeithW

...Or by looking at the MyFarm website into carbon farming. My personal choice would be an established Kiwi Gold orchard.

But will the number of buyers outnumber the sellers or vice versa. It obviously matters in terms of where values will go.

To a certain extent, you're still limited by how much people can borrow. Say for instance rates go to 10% I might spend $1m, and I won't have all that much competition in that range, whereas someone capped at $750k will have considerably more competition. It may not work out that way, but we won't know until mid-2023 I guess. I'm picking at 7% 8%+ and unemployment increases there will be increasingly more motivated sellers.

So rinse and repeat, BAU and nothing changed or solved?

To be fair they are property people, they probably aren’t going to do well. It might be the turn of the good old PAYE earner with such low unemployment.

"...RBNZ may well relish the opportunity to sit on the beach for a few weeks and watch what the world does before coming back afresh to decide whether it's up, down or sideways for the OCR next year."

Could the price fixers please take this opportunity to permanently sit on the beach?

I wonder if all of this is easily explained by the boomer demographic. Asset prices going up as they all buy in, wages going down as the workforce size is at its peak, then a sudden switch as they leave the workforce and want to cash up those assets.

It's funny, early boomers buying investment properties competing with their own children buying first homes 20 years ago, and now late boomers and their children wanting to load up the next generation with greater amounts of debt for an item that has not improved in real value since we moved out of caves.

It's free to live in a cave, for good reason.

A nice tents a few hundy.

Haha yep but where are the holidaymakers meant to stay when the campgrounds are full with residential living?

And there's a long list of restrictions on freedom camping let alone freedom living.

Are you offering a spot on your back lawn for me to pitch a tent? How many hours a week would I have to do around your property to cover the ground rent?

You're making it sound like there's additional costs for the ability to park up somewhere permanently.

You should read 'The 4th Turning' Jimbo

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.