Despite further escalation in the China/US trade wars over this past week, the NZ dollar and the Aussie dollar have held their ground at their respective lower levels against the USD.

Tumbling equity markets are sending a clear message to everyone that global economic growth will be lower when business firms do not invest or expand because they just do not know with certainty what the rules will be going forward on global trade.

US President Donald Trump has created this situation by imposing tariffs on goods imported into the US from China when the trade negotiations broke down a month ago. It is said that Trump’s view of the world and his view of his own success as a leader of the free world is determined by whether the Dow Jones Index is rising or falling on a particular day. The US sharemarket is now into a six-week retreat and sending an emphatic signal to Trump that the US economy is headed for a slowdown.

At some point very soon, Trump will have to come to the realisation that his own re-election chances in 2020 will be shifting lower as he has based his performance on the performance of the US economy.

Whether the message that Wall Street is delivering to him will change his trade stance remains to be seen. His latest bombshell to impose import tariffs on neighbours, Mexico to stop illegal immigrants entering the US has drawn codemnation from near and far. The Chinese are due to release their retaliatory tariff package against the US today (Monday 3rd June), which will result in more uncertrainty for businesses around the world wanting to trade and more uncertainty for investment markets wanting to price the future profits of those entities into equity values.

Against this rapidly deteriorating international trade and investment backdrop, both the Kiwi and Aussie dollars have displayed a resilience over this last week which indicates the previous selling pressures have been all but exhausted.

The NZD/USD exchange rate has held above 0.6500 and the AUD/USD rate has finally located some support at 0.6900. It appears that the hedge fund speculators who sold both currencies a few weeks ago on lower NZ/Aussie interest rates and the renewed blow-up in the trade wars, have considerably reduced their interest to add to those short-sold positions. Their reluctance to speculate further against the antipoddean currencies seems to be more about how the US dollar itself will now behave on global forex markets.

The USD has strengthened against all currencies over the last 12 months to above 98 on their currency index, based on rising US interets rates and a strong US economic growth outlook. Those market and economic conditions are now significantly different for the USD, with US interest interest rate markets now pricing-in future interest rate cuts by the Federal Reserve and the Trump’s trade gamble looking like it will backfire on the US economy and lead to a slowdown.

The currency speculators may soon start to look for other currencies to buy instead of the US dollar.

Could the “safe-haven” status re-emerge?

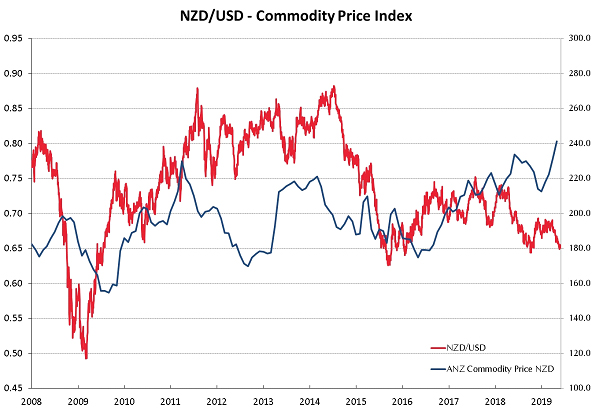

Back in 2012, the Kiwi dollar appreciated on capital flows moving out of a debt-ridden Europe which were attracted into the NZ dollar as we were seen as a long way away and a safe place to be in an uncertain world. The US dollar was out of favour at that time due to their quantitative easing of monetary policy to recover the US economy from the GFC.

The NZD/USD rate moved higher through that period despite our commodity prices at the time drifting off to lower levels.

Over recent weeks the Japanese Yen, Swiss Franc and US Treasury Bonds have been the recipients of global investment capital seeking out a safe harbour in a tumultuous world. It would not be too surprising to see both the NZD and AUD at these cyclical lower levels attract some safe-haven flows from the US and Europe.

There will be a reluctance to buy the USD as a safe-haven currency at its current elevated levels, particularly given the change with US interest rates and potential weaker US economic growth.

The difficulty with the Kiwi and Aussie dollars potentially attracting safe-haven capital flows is that both economies are heavily dependant upon China and slowing growth in China would be a negative. Countering that argument is that China will always demand imported protein from New Zealand and higher iron ore prices suggest there is still plenty of Chinese industrial demand in that space for the Aussie and the AUD.

Comparisons to the October 2018 period

The NZ dollar was sold down to levels below 0.6500 in September/October 2018 due to rising US interest rates, US/China trade wars, a dovish RBNZ and falling commodity prices at the time. The Kiwi staged a dramatic recovery through November 2018, zooming up to 0.6900, when all those speculators holding short-sold NZD positions bought back their Kiwi dollars on a much stronger than expected NZ GDP growth figure.

The Kiwi dollar is once again back at 0.6500 and it appears all the negatives are fully priced-in to the exchange rate already. The trade wars and the dovish RBNZ remain, however US interest rates and commodity prices have reversed as influencing factors.

Over coming weeks, the local factors that will influence NZ dollar direction will be the March quarter GDP result on 20 June and June quarter CPI inflation numbers on 16 July. Both figures stand to be above market expectations and again could cause some re-assessment from the speculators about the performance of the NZ economy.

The Reserve Bank of Australia are certain to cut their OCR rate by 0.25% on Tuesday 4th June; however do not expect AUD selling as a result as the outcome is already fully price-in to the AUD/USD exchange rate.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

20 Comments

Roger, there is nothing safe about AUD and NZD. Your eternally bullish view on the antipodeans is now beyond just boring and inaccurate, it's desperate. You cling like glue to above relationship between commodity prices and AUD and NZD, but have forgotten the basic rule of correlation analysis - "all other things being equal". All other things are not equal at the moment - antipodean real estate is in a funk which is unusual. Real estate prices influence the 70% of our economy which is consumer spending, dwarfing the 30% which is commodity price influenced exports. Please interest.co.nz, can we have an unbiased currency commentator?

I don't agree with most of his currency views, but I see his logic on the safe haven call. NZ & Australia are beacons of fiscal and monetary orthodoxy when compared to Europe and the US where rates are mostly negative and central banks own up to 70% of sovereign debt. In the UK, the unfunded pension liabilities (public and private) alone render the country insolvent.

Yes this"eternally bullish view on the antipodeans" needs to be reviewed by Interest. It would be interesting to know what positions NZ$ Roger has open at the moment. It would also help the discussion if a counter view was published. I notice for example the ANZ has the EOY USD at 0.64 and the Aussie at 0.91 in their latest quarterly review.

NZD and AUD are not "safe haven" currencies nor are they candidates for safe haven currencies. In fact they're the opposite, which is why they've been easy target for the carry trade for too long.

'Both figures stand to be above market expectations and again could cause some re-assessment from the speculators about the performance of the NZ economy.'

Let's see. I'll be surprised if they are above market expectations.

A better indicator of forward USD strength can be found in the depth of negative quotes for both three-month euro and yen cross currency basis. The more negative the quotes, the more USD debt demand will be sought in the FX market via general FX swap loans - inevitably a deferred USD short. BIS claims - The outstanding amounts of FX swaps/forwards and currency swaps stood at $58 trillion at end-December 2016. Link

Nice to see someone has correct thinking. But NZD/CA Legs is one to look at. Rather than JPY outrights etc.

Without giving away all the lollies, try correl basis movements to free cash in NZ money mkt. You should notice the ESAS phenomenon as I did.

Run that past me again? Xccy basis swaps can indicate a number of things, more generally the current account position in the term market and the cash in the system at the shorter end.

What basis swap blow-out? Both Kiwi an A$ basis swaps are cheaper against the US$ YTD.

That's because NZ/USD cross currency basis swaps are less than a rounding error when it comes to hedged USD global funding demand, hence those currencies that engage in this activity on a truly industrial scale are better indicators of this demand. And yet an outbreak of demand for USD in the global FX market to square previously borrowed FX swap USD will impact upon the local NZ/USD spot rate. Unfortunately, FX swaps are just footnotes in the publicly declared balance sheet of banks etc, as they are off-balance sheet instruments.

THE RBNZ makes fleeting reference to it's FX swap etc(section 10) activity to borrow USD etc reserves and to correct distorted implied forward interest rate differentials by injecting NZD directly into our own forward FX markets.

As simple as I can, I think about it as surplus CA funds are offered into loanable funds markets (USD) by nature, then banks/actors access USD market through the USD currency basis, if hedged unhedged etc

The CA basis cross pairs are a better representation of NZ funding conditions, at least in terms of offshore deposits in NZD, rather than the USD basis. I.e NZD/EUR basis, NZD/JPY basis. For proof, the short term yield on NZD deposits correlated with those too, not the USD basis. As the flow isn’t directly linked to the USD, but the CA pairs, even though there is no real market in practice for the spot or basis in those cross pairs.

This is for non-speculative flow, so actual physical deposits in surplus / demand, accumulated balances etc.

I can explain in more detail, and how it links to the ESAS system in terms of the halts that we saw last year and Jan this year in the payments system

lalaland, xccy basis swaps reflect the relative demand/supply of debt capital funding between nations. For example, if the demand for term funding in NZ outstrips supply, the basis curve will widen to reflect this. It will widen to the point offshore investors will issue NZ denominated bonds and repatriate the funds (Kauri bonds). The fact that the NZ/USD basis curve is well above par (0) simply reflects that NZ is a net importer of capital. Xccy basis swaps are the tool that facilitate cross-border borrowing and lending in public and private markets.

For example, NZ banks borrow Eurodollars in London, World Bank borrows NZ dollars (Kauri). To hedge, both parties swap borrowed currencies at the current FX rate over three or five year terms. The basis currently ~21 bps for the 3yr tenor is paid by the NZ banks which affords the World Bank sub-Libor financing costs at the agreed reset dates. Large currency moves in either direction evoke collateral calls. I call this paying tribute to a foreign banking entity.

In the nicest possible way Audaxes, I'm not sure you really understand what you're talking about (and I'm aware A$ axes means you may be in the industry)

I don't think I understand it, at least if I go talk to a commercial banker or the RB. But I can figure out what happens before it happens, the banks and the RB routinely seem surprised at what is obvious to me. Or pointing out preexisting correlations, people always seem surprised.

I don't know if anyone knows how it works to be honest, and probably not me.

I focus more on the movement of the overall market directionally, than what the commercial purposes of each item are. E.g the basis. I don't know the formal definitions of them that well, and haven't worked with them in a commercial sense, but study the movement and how they influence other areas where I am commercially active.

Its just theory developed in isolation on my behalf. Am a bit on the spectrum. It might be a bit of you say Tomato, I say Orange. We are both talking about fruit.

I understand what you say about the basis, but I focus more on why the lending/issuance stops in the first place, or starts, and what it does directionally to the market, or how it impacts onshore credit activity here. And how spot valuations deviate from intrinsic based on that. I fundamentally have a view that currency valuations are underpinned by credit activity, and do actually hold small amounts of intrinsic value etc

Safe haven? With our banks mortgage exposure debt level and over stocking in Auckland ?

I don't buy this for a second. NZD trades like an EM currency. If we have a global regression it's going to take a beating vs the USD but will be fine vs the AUD and no doubt the CNY.

If you want a safe haven JPY and CHF are the usual currencies of choice when the water gets choppy.

If I was gold I would be insulted that bitcoin was on the list of monitored currencies but I was not. Incidentally gold just went over 2000 NZD/Oz.

I think this is wishful thinking. The fact remains that the USD is the de facto reserve currency of the world now. It is also a fact that the EUR is fatally flawed and will likely be on life support for some time. European banks are nowhere near as strong as US banks. The ECB is the ONLY buyer of Euro govt bonds at ridiculous rates, and on it goes. The major capital flows - which haven't fully got underway by any means - will be heading into USD and US equities. I can't see how this picture is USD negative. I also cannot see how the NZD/AUD will rise against the USD in this unfolding mess, when the USD is still king? It's a bit like the gold bugs talking USD10k an ounce gold after 2008 (and still are)...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.