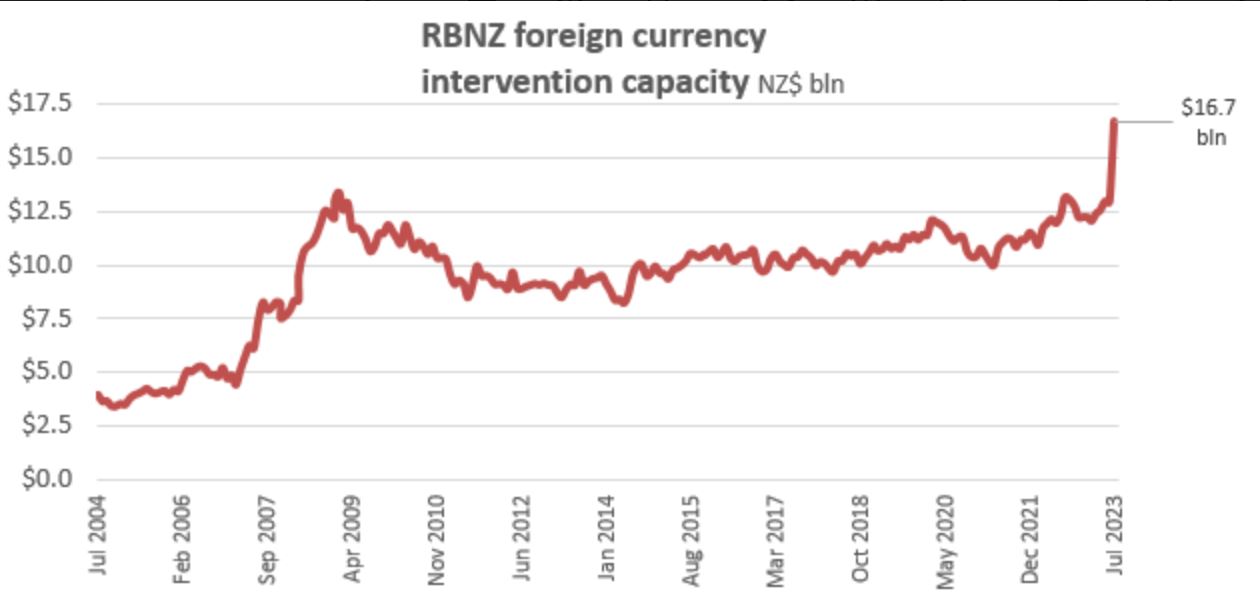

The Reserve Bank (RBNZ) ramped up its foreign currency intervention capacity by almost NZ$4 billion during July by selling NZ dollars in what was likely a move of unprecedented scale, according to Westpac New Zealand Chief Economist Kelly Eckhold.

This follows a January announcement from the RBNZ that it had agreed with Finance Minister Grant Robertson to a new framework for managing foreign reserves, which would see its holdings in overseas currencies grow. This, at least in part, reflects increases in the scale of both the economy and global financial markets.

Eckhold, who in a previous job managed the RBNZ's foreign reserves, said the RBNZ starting to build reserves is consistent with that announcement, and came with the RBNZ also receiving a $500 million capital injection during July to support such a move. The RBNZ's most recent annual report shows capital of $2.4 billion as of June 30 last year.

"There wasn't really any market chatter about this so obviously there was sufficient liquidity, and they've managed to execute it in a way that hasn't really leaked out," Eckhold said.

"Their objective wouldn't have really been to move the exchange rate. I don't think this is like foreign exchange intervention. The objective there is to accumulate your foreign exchange without necessarily changing the market that much."

The RBNZ's foreign currency intervention capacity rose to NZ$16.699 billion at the end of July, up from NZ$12.922 billion a month earlier. (There's detail in this story on the RBNZ's approach to intervening in the currency markets).

"I think you're on safe ground to say that [the NZ$4 billion RBNZ move is of unprecedented scale]," said Eckhold. (See chart at the foot of this story).

The RBNZ provides an update to its foreign currency assets and liabilities monthly, and Eckhold said it wouldn't be a surprise if when the next update occurs, in late September, to see the RBNZ further increased foreign currency intervention capacity during August.

He views increasing foreign currency intervention capacity as a good idea.

"You're basically looking for that hedge, for that bad situation where the NZ dollar is very, very weak and there's a relative shortage of foreign exchange in the market. It basically gives you that additional monetary policy tool that you can deploy. Otherwise you end up with extreme overshooting of the exchange rate which creates monetary policy problems of itself. So I think that's a reasonable objective for the Reserve Bank to be thinking about," Eckhold said.

"There's also the crisis interventions motivations as well. If you had some severe economic or financial crisis going on when the exchange rate could get particularly hit, then you do get that extra cushion to be able to use to absorb that. That's a fairly common role that central banks play internationally."

'They seem to have got a reasonably good exchange rate'

A challenge for the RBNZ in these transactions is working out what's going to be a good exchange rate, notes Eckhold. That's because if the NZ dollar appreciates from that level there's a mark-to-market loss for the RBNZ, and it'd want to avoid a significant loss.

"They seem to have got a reasonably good exchange rate, if you look at the chart over the period that they likely did it. In that period just after the Official Cash Rate [OCR] review, the exchange rate briefing spiked up to around about US64 cents or so, which is obviously quite a bit better than it is today. So kudos to them in terms of getting that timing correct," Eckhold said.

He said the RBNZ's selling might have been a factor for short periods in recent NZ dollar weakness. However, the main drivers have been US dollar strength, significant upward revision to US interest rate expectations with a recession there seen as less likely, and weakness in the Chinese economy - key export market for NZ - and commodity price falls.

Eckhold points out the RBNZ has a combination of unhedged reserves, where they sell NZ dollars and buy US dollars and spread that around a basket of other currencies, and hedged reserves which you can see through the central bank's holding of foreign exchange swap commitments.

"The volume of those [swap commitments] has actually dipped down a little bit in the last couple of months...so they'll probably be looking to accumulate some of those long-term swaps over the next few years."

The RBNZ said its foreign reserves are mainly invested in government bonds, cash or short term money market instruments from major advanced economies

An RBNZ spokesman said the size of the increase in its reserve holdings and the RBNZ’s strategy to increase foreign reserves is considered market sensitive, thus it won't shed any light on its plans.

"Release of information related to the change in level of reserves may compromise our ability to effectively transition to the new target level and may also compromise our policy effectiveness in the future," the RBNZ spokesman said.

Another NZ$1.3b for the RBNZ plus a new NZ$5b indemnity

Meanwhile, a cabinet paper released by Treasury on Thursday shows the RBNZ's in line to receive another capital boost. Robertson took a proposal to cabinet in August to boost the RBNZ's capital by NZ$1.3 billion. Robertson said he also intended to provide the RBNZ with an indemnity covering potential losses of up to NZ$5 billion.

"This is aimed primarily at supporting interventions that the Bank may need to undertake to promote financial stability and financial market functioning, such as interventions in the New Zealand government bond market. Once established, I intend to terminate the existing Large Scale Asset Purchase (LSAP) programme indemnity. This would not terminate the liability for LSAP bonds purchased to date but would terminate this indemnity for future bond purchases," Robertson said.

"These arrangements will ensure the Bank has sufficient financial resources to intervene for financial stability purposes and to undertake conventional monetary policy, including some support to establish a negative interest rate if required. The financial backing also provides support for some risks already on the Reserve Bank balance sheet."

The Government agreed to indemnify the RBNZ for any losses incurred by the LSAP programme when it was launched in March 2020. The LSAP programme saw the RBNZ buy $53.5 billion of NZ government and local government bonds on the secondary market between March 2020 and July 2021. It did so to lower interest rates to boost inflation and employment, as well as to support smooth bond market functioning. The RBNZ's now selling $5 billion worth of these back to Treasury's NZ Debt Management unit annually.

The NZ$1.3 billion covers; potential support for any future use of negative interest rates as a monetary policy tool reflecting direct losses that would result on the RBNZ’s balance sheet if the OCR were to be taken negative; support for business-as-usual liquidity management and implementation of the OCR framework; tactical interventions to support financial stability and market functioning and; the RBNZ’s other risks relating to COVID-19 interventions already on the balance sheet, plus changes to other risk estimates.

Robertson noted many of the RBNZ's tools, such as conventional monetary policy, prudential policy settings, supervision of individual financial institutions and managing the payment system, have a relatively limited financial impact on its balance sheet. However, in other areas its actions could have financial costs or bring financial risk on to its balance sheet.

"For example, when undertaking large scale asset purchases in 2020/21, the Bank purchased fixed rate [government and local government] debt and issued floating rate liabilities. This exposed the Bank’s balance sheet to rising interest rates. Past and expected future losses on the Bank’s balance sheet as a result of LSAPs are approximately $10.5 billion. The Bank are reimbursed for these losses through an LSAP indemnity issued under the Public Finance Act 1989."

"These risks can be managed either through additional capital or through an indemnity under section 65ZD of the Public Finance Act 1989 to offset potential losses. Providing financial backing to the Bank, either through an indemnity or capital, would not impact net [government] debt. This is because the Bank is consolidated onto the Crown balance sheet: at a whole of government level the transaction is eliminated on consolidation. However, gains and losses on the underlying activity the Bank undertakes e.g., bond purchases, will impact the Crown balance sheet," said Robertson.

"To ensure the operational independence of the Bank to intervene for financial stability, I propose to provide upfront financial backing of an indemnity capped at $5 billion of losses. This has been set at a scale that the Bank consider would be sufficient for interventions primarily for market functioning purposes. It would not provide for a future LSAP programme of the scale of the 2020/2021 programme. This means the financial backing will be put in place to allow the Bank to intervene to a limited extent without seeking additional financial resources from the Minister of Finance."

"Once the new indemnity is established, I intend to terminate the current indemnity for LSAP, which was granted in August 2020. This would not terminate the liability for LSAP bonds purchased to date but would terminate this indemnity for future bond purchases. The Bank would be able to rely on the new indemnity discussed above if they needed to intervene for financial stability purposes," Robertson said.

28 Comments

The timing of this speaks volumes.....

RBNZ sells NZ dollars, making the value of our dollar go down, creating inflation, which they raise interest rates to control.

Cool and normal.

"You're basically looking for that hedge, for that bad situation where the NZ dollar is very, very weak and there's a relative shortage of foreign exchange in the market. It basically gives you that additional monetary policy tool that you can deploy"

"I think you're on safe ground to say that [the NZ$4 billion RBNZ move is of unprecedented scale],"

RBNZ are positioning themselves to defend the currency by selling foreign currency. Its for when things truly hit the skids. We are nearing that part of the cycle.

The RBNZ is a minnow in a small boat in a large ocean - China, India and Japan are struggling to support their currencies in an environment extremely short of eurodollar credit.

My water cooler mates don't know (but you will) that China and Japan are the leading buyers of U.S. Treasuries. Obviously has had little influence on the strength of their currencies, even though we know both countries seem to prefer and not be bothered by weaker currencies.

The shortage of Eurodollar is now making complete sense to me.

All fiat currency leads to failure, we're watching it slowly implode. Too bad they want to continue the circus

The Reserve Bank of New Zealand's currency intervention involves buying or selling NZ dollars to influence its exchange rate, aiming to stabilize the economy or address specific economic issues.

So do they know something which we do not that they need to make a chest for intervention?

RBNZ working with fish and chips shop has really screwed up the kiwis.

Although the ratings agencies say everything is fine at the moment, will a change in government alter their outlooks, and we get a ratings downgrade in November/December??

Absurb.

RBNZ should not be seeking to intervene in the FX market.

Your NZ Dollar Aint Sheit, Cause of Rich Men south of Levin!

The RBNZ and NZ Govt know it, and are betting on it exactly with billions, by the rampant selling of our devaluing NZ peso.

If you not moved your NZD$ to a safer location already ......well you get what your dollar pays for and it worth Sheit.......and increasingly so!

The RBNZ and NZ Govt know it, and are betting on it exactly with billions, by the rampant selling of our devaluing NZ peso.

Yes. Most people are not equipped to play the game except the ruling elite. The little guys just take the blows and their welfare is not taken into consideration.

Yes most get blown along with the brambling tumbleweeds. NZ been growing some big ones in recent years.

I'm a simple guy and decided to hedge somewhat and get into some company's doing work in the US and Aust.

Always had a few stocks and know they can get blown around too, buying dividend payers and diversifying into everything, is the best hedge.

NZers have thought that loading up, all they have, into NZs second hand, dilapidated housing, is the only safe so called "investing" option.

I only have the one house and its exposure enough, to this illiquid asset class.

Always thought the constant stacking of houses, like pancakes, was foolish and a dumb money thinking. Not to say how destructive it has been for NZs society and future.

This 'positioning' of the RB for future events says it all really. It's pretty unstable out there both locally & globally. Too much debt/greed.

It is quite possible that RBNZ will have to start dropping interest rates early 2024 because the economy will be tanking - especially if NACT start cutting public spending. Our challenge will be that the US will not be reducing rates as early - their economy is nowhere near as sensitive to 5% interest rates as almost all of their household debt is fixed rate for term.

In this scenario, we could see a very unsettled NZD. My guess is that this is what RBNZ are preparing to counter.

NZ public about to score a major own goal at the voting booth. We all get a lolly mixture from the dairy as a treat

Property is our god and sacrifices must be made.

If RBNZ fails to keep pace with US rate increases, I doubt that an additional $4B in foreign reserves is enough to offset the downward pressure on the NZ dollar. If that is the intention it seems bound to fail at those levels.

Interesting looking at https://goldprice.org/ There's a clear inflection point in 2019 wrt gold priced in NZD. From 2014 to 2019 gold was compounding at ~ 5.4%pa. Something changed in 2019, and it now it's compounding at ~ 11.3% pa. I remember Jim Rickards saying in one of his books saying that any anything >10% could be regarded as hyperinflation.

Rickards and Jim Rogers both seem to believe that a gold bull market started in 2015. Rickards is on record as saying the gold price is heading to $15,000 by 2025.

2019 of course is an important point because the monetary response to Covid followed relatively early in 2020.

Wow and people on here think property Spruikers are bad. Gold has gone pretty much nowhere, its been $1700 $1800 for as far back as I can remember, it recently almost clipped $2000 and its fallen way down again. You cannot really include currency fluctuations, it does that anyway and you could make similar amounts just trading fiat, you don't need a highly illiquid gold thats not paying you a monthly return.

Wow and people on here think property Spruikers are bad. Gold has gone pretty much nowhere, its been $1700 $1800 for as far back as I can remember, it recently almost clipped $2000 and its fallen way down again.

No. You don't understand. Rickards and Jim Rogers said that the gold market bull run started in 2015. Rogers said that the gold bull run would not start without at least a 50% crash - that is entirely consistent with the peak of the 2000-2011 bull run in gold compared to 2015.

XAUUSD is up 90-100% since 2015

XAUJPY is up 100-120% since 2015

XAUNZD is up appox 100% since 2015

You cannot really include currency fluctuations, it does that anyway and you could make similar amounts just trading fiat

Nonsense. The hoi polloi would have been far better off holding gold proxies than their own currencies and pretending that they can trade currencies.

JUst pointing out a mathematical reality A=P(1+r)^n The compound inflation plain as daylight. I've never been called a gold spruker before. What blows my mind is that in the 80s a barrel of oil was over 100 usd.

the PREFU must be bad

Question not asked is why is there considered to be a risk to NZ dollar? Could it be because China exports cratering and USA is winning trade war and chip war?

No wonder Lab has no sweeties to give away when giving big moolah to RB

wait until Wednesday.

While we know China and Japan are dumping U.S. treasuries, so is Saudi Arabia. That's quite a reduction.

Feb 2020: $184B

Jun 2023: $108B

https://twitter.com/Mayhem4Markets/status/1700627526874234964

RBNZ have access to information that the public doesn’t have. If you were a listed company this would be called Insider Trading.

To short NZD with such a huge amount of money speaks volumes about where NZD is heading.

The markets are likely to punish NZD for RBNZ losing faith in NZD.

Watch NZD to fall further from here. NZD/USD falling to 0.55 seems a real possibility now.

RBNZ should stick to its knitting and keep out of currency trading.

Remember what happened to Barings Bank when a trader got it wrong.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.