By Roger J Kerr*

Short-term movements of the NZD/USD exchange rate continue to be totally dominated by announcements and developments in the escalating trade wars between the Trump administration in the US and China.

Over this past week the Kiwi dollar has been buffeted downwards, upwards and downwards again as the global FX markets react to each fresh piece of trade wars news:-

• President Trump playing hardball threatens another $200 billion of tariffs on imports from China – USD strengthens, and the NZD/USD rate falls away to 30-month lows of 0.6505.

• US Treasury Secretary Steven Mnuchin signals new talks with the Chinese in attempt to get negotiations going again – USD weakens, and the NZD/USD rate lifts to 0.6590.

• President Trump tweets that he is instructing his officials to proceed with the $200 billion of tariffs, despite Mnuchin’s attempt to restart talks with Beijing – USD strengthens a tad, and the NZD/USD rate drops back to 0.6550.

The financial markets are well aware of Trump’s swagger and bluster to adopt an extreme opening negotiating position to force a response from the opponent. It is yet to be seen whether these tactics will work with the Chinese who are the US Government’s major creditor (holding US Treasury Bonds).

A growing chorus of global economists, politicians and business leaders see no benefit to the US economy or the global economy from the protectionist tariff regime of Trump.

Trump must believe that there are votes for the Republicans from the tariffs in the upcoming mid-term Congress and Senate elections. If that proves to not be the case, the US dollar is widely anticipated to weaken on the political risk factor of the Congress going to the Democrats.

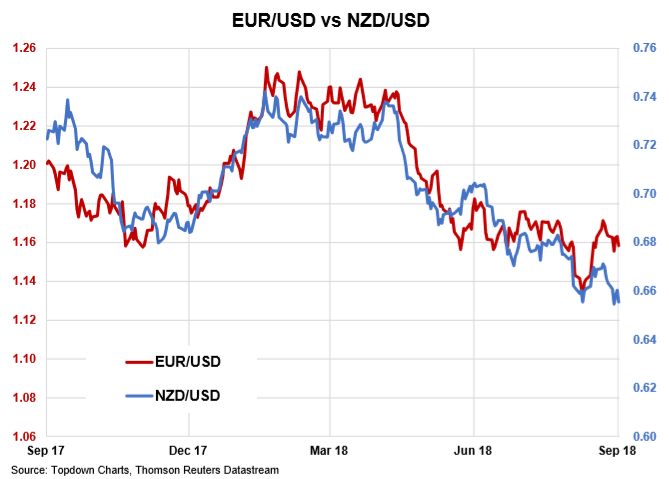

It is significant that the EUR/USD exchange rate has not moved below the $1.1500 level despite the escalating trade wars generally being viewed as positive for the USD. Should the US trade negotiators make progress on talks with the Chinese and Canadians over coming weeks, expect to see the EUR/USD rate climb to the $1.1800 level as the USD weakens.

It is also very instructive that the USD has not strengthened in response to the probability of a December rate hike by the Federal Reserve has increased from 60% to 80% on continuing strong US economic data. It is clear that the currency markets have already fully priced-in to the USD value the fact that US interest rates will increase another 0.50% this year and a similar increase in 2019.

The NZD/USD exchange rate has maintained a tight correlation to EUR/USD rate movements over the last 11 months after the October 2017 election result pushed the NZD down on its own accord. However, over the last three months the Kiwi has depreciated by another three cents on its own, related to a tumbling AUD, lower business confidence, an overly bearish RBNZ, trade wars and emerging market meltdowns.

The EUR/USD rate has remained stable through this period. Against the very positive economic fundamentals of record high export commodity prices and GDP growth being aided by fiscal expansion, the Kiwi dollar must be viewed as under-valued at 0.6500 if the aforementioned negatives do not repeat.

The NZD/USD rate certainly has some catching up to do on the EUR/USD rate and commodity prices. It is difficult to see the RBNZ becoming even more bearish on the inflation outlook when this latest bout of currency weakness is set to increase imported product prices in the September and December quarters.

It appears that local USD importers did not hedge to 100% of 12 months payments in April when the Kiwi was 0.7400 (as this column recommended at the time). As currency hedging runs out over coming months, inflation will increase beyond RBNZ forecasts as importers are forced to increase their prices and these are passed through to consumers.

Exporters in USDs have been increasing their hedging percentages since 0.6800.

No-one really knows where the bottom will be in this Kiwi downtrend. What we do know is that exporters who budgeted USD export receipts at 0.7000 and above now have the opportunity to significantly reduce future currency risk and lock-in company profitability over several years.

Exporters who are persuaded by the doomsday brigade that the Kiwi dollar is headed to below 0.6000 need to remind themselves that they should be managing risk, not punting the shareholder’s funds!

The current NZD/USD exchange rate of 0.6550 is more than 13% below its seven-year average of 0.7550. Several of New Zealand’s very successful manufacturing exporters have adopted an exchange rate risk management policy of hedging up to 50% of receipts three to five years forward when the NZD/USD rate is at such cyclical lows based on historical rate averages.

The local financial markets will be looking to next week’s GDP growth and employment data for the June quarter as a pointer for the next Kiwi move.

The RBNZ’s quarterly GDP growth forecast is for a 0.5% increase, one bank forecasts as high as +0.9%. The provinces and primary sectors are humming in New Zealand (despite the Coalition Government creating more uncertainty than certainty!) and thus a GDP growth result well above the RBNZ number would not surprise.

Daily exchange rates

Select chart tabs

*Roger J Kerr is an independent treasury Management advisor. He has written commentaries on the NZ Dollar since 1981.

9 Comments

Sorry Roger but it is still far too early to be locking in a hedge and sacrifice the profits from further falls in the $NZ - it's only going one way and there is nothing to signal a medium term recovery. Below 60US cents by the end of the year is where it's heading.

40 cents by the end of 2020.

I wouldn't joke about that.

I'm not sure if it will take as long as that. The NZ dollar has a history of spectacular collapses and we are now more heavily 'debt-stacked' than ever before. Budget assumptions will be out of the window by the next review.

Market is short on the Kiwi currently and if Trump comes out and resolves the China issues - it will rally hard.

However until then it's better to be cautious - noting that the currency has not be able to break through 65 as yet.

One thing I love in these sorts of columns is the certainty that the currency will do certain things - be it rally or decrease. Whenever I read these columns first question I ask myself does the person actually have any skin in the game?

Then my next question - if he is so smart and knows where the currency is headed - why hasn't he set-up a Hedge fund and punted the currency and made a zillion dollars. Because if he is so smart - he can generate a lot more money running a hedge fund vs. advising companies on where/when to hedge exposure.

Till then - I look for any viewpoints around technical support/resistance levels and ignore the opinions - as he is just another talking head who realistically has no clue if the currency is going up or down.

There's always a sentence or two in any of Interest's articles that pique ones - er - Interest.

It appears that local USD importers did not hedge to 100% of 12 months payments in April when the Kiwi was 0.7400 (as this column recommended at the time). As currency hedging runs out over coming months, inflation will increase beyond RBNZ forecasts as importers are forced to increase their prices and these are passed through to consumers.

This to my untutored and no-skin-in-game eyes, another small straw in the wind that says there is gonna be some cost-push inflation coming at us all in the months ahead. And the labour component of cost-push is already having its wicked way with business confidence: the combination of strikes, Gubmint kinda-sorta-support for Mo' Woiker Moolah via top-down IR changes, will be causing some earnest C-level discussions about next year's budget (September/October is usually when Next FY budgeting starts to get attention). And pricing. And automation. And exit strategy....

Sure hope it has changed since my time when your importers used to suggest, demand actually, that you could now lower your CIF price(s) as the NZD fell. Used to always happen to when Muldoon and others, sprung their devaluations. Sure hope it has changed.

Unlikely. Actually a reasonable possibility

Why does Roger constantly call the bottom in the Kiwi? I sit and wait for his articles like clockwork.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.