New Zealand's economy grew 1.1% in the September 2025 quarter, according to Statistics NZ.

This big rise follows a revised drop of 1.0% in the June quarter (0.9% first reported).

The 1.1% September rise even outstripped the gains forecast by the market.

The big banks had forecasts in the 0.8% to 1.0% range, while the Reserve Bank (RBNZ) had forecast just 0.4%, but this was in its November Monetary Policy Statement (MPS) ahead of the release of more timely information suggesting a higher figure than that. RBNZ's frequently updating economic modelling 'Nowcast' forecast was forecasting a rise of just under 0.9% for the September quarter.

'Elephant in the room'

Commenting on the quarterly 1.1% rise in GDP, ASB economist Wes Tanuvasa and chief economist Nick Tuffley said "the elephant in the room" is the tightening of financial market conditions, (accompanied by rising mortgage and deposit rates), seen since the RBNZ's November Official Cash Rate (OCR) review.

"Swap yields have advanced sizeably, and financial markets are now pricing in [OCR] hikes by around September 2026, deviating from the RBNZ’s November guidance of early 2027 policy normalisation," the economists said.

"While we acknowledge that today’s strong GDP may spook markets further, we must stress how noisy GDP data are, and that GDP is only one of a myriad of inputs that influence the interest rate outlook.

"GDP alone is unlikely to be the silver bullet to bring hikes forward – although markets seem to have already moved. This looks to be an example of how important clear central bank communication is. A lack of clarity constrains the passthrough of intended monetary policy. Therefore, we are not surprised by Governor [Anna] Breman’s recent comments earlier in the week, which have attempted to calm markets down. We await Q4 CPI inflation in January 2026 for signs that hikes could be brought forward," Tanuvasa and Tuffley said.

What about revisions to previous GDP figures?

Back to the GDP figures themselves - there has been much interest in what revisions there would be of previous quarters - and it's fair to say the revisions that have materialised will raise eyebrows - particularly that the second quarter 'June swoon' has been revised down to being even a bigger drop than it was. Also surprising is that the March quarter has been revised up from a 0.9% rise as previously announced to a now 1.1% rise. More on this further down the article.

What about the detail of the latest figures?

"GDP rose in three of the last four quarters, but fell 0.5% over the year ended September 2025 compared with the year ended September 2024," Stats NZ economic growth spokesperson Jason Attewell said.

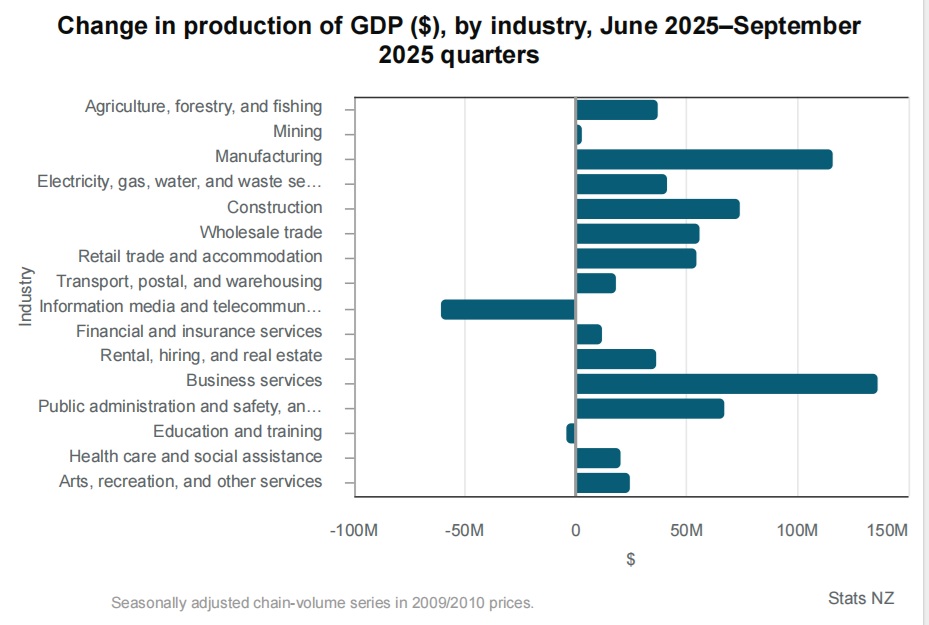

"The 1.1% rise in economic activity in the September 2025 quarter was broad-based, with increases in 14 out of 16 industries. This is in contrast to the June 2025 quarter, when GDP decreased in 10 industries."

Stats NZ said business services were the largest contributor to the overall increase in GDP, up 1.6% in the quarter. This was driven by a 2.1% rise in professional, scientific, and technical services, such as computer system design and related services.

Manufacturing was up 2.2% in the September 2025 quarter, driven by food, beverage, and tobacco manufacturing.

"The 2.2% increase in manufacturing this quarter follows a 3.9% fall in the June 2025 quarter, when it was the main driver of the 1.0% decrease in GDP," Attewell said.

Information media and telecommunications was the largest downward contributor to GDP in the latest quarter, down 2.1%.

Per capita and expenditure rises

GDP per capita rose 0.9% during the September 2025 quarter, Stats NZ says.

The expenditure measure of GDP rose 1.3% during the September 2025 quarter, following a 0.8% fall in the June 2025 quarter.

Exports were up 3.3%, with increases in travel services, dairy, and other services, including insurance.

Gross fixed capital formation, up 3.2%, also contributed to the rise in expenditure GDP.

"Businesses invested more in physical fixed assets in the September quarter. There were increases in transport equipment and plant, machinery, and equipment, supported by imports of related capital goods and motor vehicles," Attewell said.

Household consumption expenditure rose 0.1% this quarter. Expenditure on durables rose 2.0%, while expenditure on services fell 0.1% and non-durables fell 0.2%.

The increased spending on durables was driven by rises in audio-visual equipment (such as televisions, computers, and mobile phones) and motor vehicles.

More on those revisions...

The September quarter is one that does usually have a lot of revisions anyway because it is the time of year in which annual national accounts data is incorporated. In laypersons terms this means better and more accurate information becomes available, so, previous figures may well be changed, but they should be more accurate. It means we now get the definitive view, which could be quite a bit different to what we were earlier told.

The author's very early reading of both the September quarter figures and the revisions is that they will not end the debate about how our economy has actually been performing. It's fair to say there was some expectation the 'June swoon' would likely just about disappear after revisions - while its actually increased. Likewise there was some belief the March quarter bounce as originally announced would likely be watered down - but it's been increased too.

If we recall, the official figures for the June quarter showed GDP falling 0.9%. When released in September those figures prompted a strong public reaction and a fair bit of 'woe is us' sentiment. But in its latest Official Cash Rate (OCR) review in late November, the Reserve Bank (RBNZ) politely dismissed those figures, saying there were "a lot of one off factors and statistical quirks". Westpac senior economist Michael Gordon had earlier offered a compelling explanation. The upshot is that nobody really believed our economy shrank 0.9% in that quarter.

Well, now we are being told the economy actually shrank 1.0% in the June quarter. So, as said up top, the debate will go on.

21 Comments

So positive GDP and inflation at the upper limit of the mandates band and trending up..no idea why the RBNZ are still cutting interest rates.

By my calculations, this means that in the six months from March to September, net growth was 0.1%. Essentially we are back to where we were six months ago, but hopefully with some forward momentum.

Real conundrum for the RBNZ if growth remains low but next inflation read is >3%

That will be the real litmus test to see how serious the new RBNZ leadership is on their focus on keeping inflation low.

Inflation slightly above 3% and economy growing is better than inflation at 2% and economy shrinking. The RBNZ know that, but they have to pretend they don't because their mandate says otherwise.

Yeah well that is what Adrian Orr was thinking in 2021 as well by saying the rising inflation was transitory. And we all know how that worked out.

The temptation if the RBNZ operates how you describe above is that you don’t act on rising inflation when you should because you’re more focused on maintaining positive growth instead of nipping rising inflation in the bud when you should and when it would be easy to contain.

Its is a juggling act, and Orr got it wrong.

They need to trust their projections. If their projections show inflation continuing to increase, then yes an OCR rise would be needed.

Why should they trust their projections when they are often so wrong? They should act upon the measured data (GDP and inflation) instead of their own projections

May as well just sack them and use an algorithm in that case.

Looks like the economy's holding up. Time to raise rates, right?

"Businesses invested more in physical fixed assets in the September quarter. There were increases in transport equipment and plant, machinery, and equipment, supported by imports of related capital goods and motor vehicles," Attewell said."

I wonder how much of this is investment bought forward to take advantage of the Investment boost credit that will be absent from future investment?

Not sure I understand how the annual figure is possible?

Last 4 quarters: 0.1, 1.1, -1, 1.1

Yet annual is somehow -0.5 ??

I know you can't just add the quarters together due to compounding effects, but shouldn't it be within the ballpark? Added together is +1.3%

Your maths gives (approximately) a comparison between 2025Q3 to 2024Q3. I'd guess the - 0.5 is based on comparing the latest 12 months to the previous 12. Which will be a less volatile measure of growth, but also more lagged.

Politically speaking this might, repeat might, take a little heat of the government going into the holiday break and starting the new year. Just hope though that it is not over trumpeted, it’s not much more than would you get from looking at the old barometer on the wall.

It will probably work out quite well for them. Before the election that bad quarter will drop out and it will look like really good annual growth, even though 1% of that growth was actually just catching up on the quarter before.

Incredible that if you let spenders keep more of their money, and reduce debt servicing costs for businesses, the economy picks up. It's like magic.

We could all be rich by setting the OCR to -100%

Now you're being facetious!

Or, landlords see spare cash and up the rents to soak it all up. Can't be letting the hoi polloi have a chance can they (sarc)

As long as they have the stuff they need to buy

OK so the economy is still going backwards on an annualized basis. The RB really needs to tidy up its communication to the markets given that the jump in fixed rates is clearly premature. Hopefully they'll drop back again at the next review in February.

where is that Cote de junior guy... he will claim 4.4% growth annualized here....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.