Well, it's time to take the pulse of the nation again and see if that economy of ours really is recovering. In truth, we might not yet get a definitive answer.

Stats NZ will be releasing GDP figures for the December quarter on Thursday, March 19.

And, yes, we can trot out the usual complaints about these figures being very late, coming out as they will almost at the end of the following quarter.

But they are what we have and obviously what we are looking for is signs that the fledgling economic recovery is taking hold.

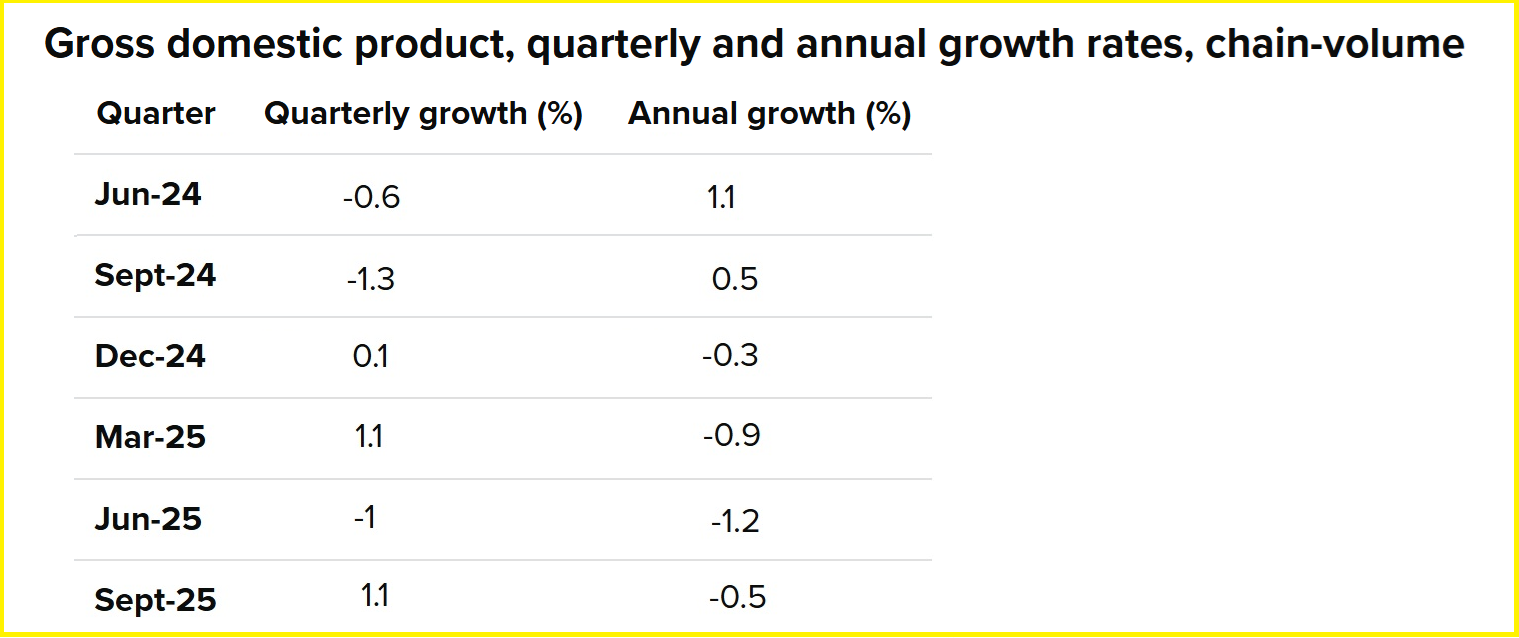

Our recent pattern with the GDP figures has been very up and down, with large swings from plus to minus growth between quarters.

Economists have their views about what might be behind this pattern, and it is clear that our GDP figures have for whatever reason become a lot more 'seasonal' - when of course they are not meant to be. The whole point is that the seasonal adjustment process is supposed to cut through the impacts of seasonal variation to give us and apples v apples comparison between the quarters.

I had only two of the major bank economists' previews in front of me at the time I wrote this (BNZ and ANZ), but it appears from what I can see so far that the latest (December) quarter may again show that up and down pattern. Indications are that the December quarter might - so far as these Stats NZ figures tell us - have seen the economy somewhat 'stall' again.

If we recall, the outcome in the September quarter (reported in December) was a strong 1.1% rise, following a 1.0% (revised) fall in June.

This is the picture the Stats NZ figures are currently painting for the recent past of NZ's GDP:

You can see that things have been very up and down.

The economy had the stuffing knocked out of it during the 2021-23 period in which the Reserve Bank (RBNZ) was raising the Official Cash rate from just 0.25% in the pandemic to a peak of 5.5%. This was of course all in aid of getting rampant inflation, which peaked at 7.3% in mid-2022, back under control.

The RBNZ (having pushed inflation back into the targeted 1%-3% range) began cutting the OCR again in August 2024. It's fair to say though that for a lot of time after that expectations of a pending economic recovery ran ahead of the reality. Business confidence surveys kept suggesting that businesses were seeing better times ahead - but those times were never quite arriving.

As a nation we simply seemed to have got out of the habit of spending. And, of course, if we don't spend, the wheels of the economy don't turn.

By the middle of last year there was a clamour for the RBNZ to accelerate its OCR cuts, in order to provide more impetus for a recovery.

Regardless of whether you thought it necessary or not at the time, (and I have to say I didn't actually agree with the move), the RBNZ's decision to do a jumbo 50 basis point cut to the OCR in August last year did seem to cheer everybody up, which was the clear intention.

Less intended though, of course, might have been what happened after the November OCR decision, when the RBNZ did, yes, cut the OCR again, but also indicated that the cut was likely the last one. The subsequent sharp rise in wholesale interest rates, accompanied by some mortgage rate rises, certainly appeared to knock the stuffing out of the housing market at the end of last year.

A recovery without houses?

And of course, the housing market has been largely missing in action. And one of the emerging themes has been can New Zealand have a meaningful economic recovery without a housing market boom?

Anyway, notwithstanding some renewed hesitancy caused by the end of interest rate falls, the general signs in the economy have been good. There are signs of the return of spending. But it's all still looking a bit uneven.

The RBNZ in its February Monetary Policy Statement (page 40), forecast a 0.5% rise in December quarter GDP, followed by a 1.1% rise for the March quarter we are currently in. The RBNZ's economic modelling 'Nowcast' forecast was, at time of writing, forecasting a rise of just a little under 0.5% for the December quarter.

As usual, we've had some clues ahead of time as to at least the direction of the figures principally through the key three so-called 'partial indicators'.

It's probably fair to say the results of all three have been a surprise - one pleasant surprise, two not so. And that's what is leading me to think that the apparent momentum shown (at least by Stats NZ figures) in the September quarter may be shown to have nearly stalled in December. Here is how the three 'partial indicators' turned out.

• Retailers have had a tough time but things are turning for the better. The 0.9% rise in volumes in the December quarter followed a particularly strong 1.9% rise in the September quarter and provides further evidence that the under pressure retail sector is beginning to recover as the economy strengthens.

• The volume of total manufacturing sales fell 0.5% in the December quarter, following an upwardly adjusted 1.2% rise in the September quarter. Wholesale trade sales rose a seasonally adjusted 1.1% in the December quarter after an upwardly revised 2.9% in the September quarter.

• The seasonally adjusted volume of building work done in the December quarter fell 3.1% compared with the September 2025 quarter, with residential falling 1.1% and non-residential down 6.5%. These figures were definitely an unpleasant surprise to economists. Adding to the unpleasant surprise was the revising down of the September 2025 figures from an originally reported 1.5% growth to a rise of just 0.2%.

Okay, so what to make of all that?

The economists speak

Well, BNZ senior economist Doug Steel is picking a 0.3% rise in GDP for the December quarter.

"It isn’t particularly strong, but it would be the second consecutive quarter of growth and support our thinking that a modest economic recovery was getting underway in the latter part of 2025," Steel said.

"If we are right then Q4 GDP will be softer than the 0.5% that the RBNZ projected in its February MPS.

"This would add to a theme of growth indicators looking softer than the RBNZ expected, while inflation indicators are looking higher than the Bank [RBNZ] projected. And, of course, all this is before the recent mayhem in the Middle East erupted, which is likely to reinforce the theme further. It presents a difficult balance for the Bank to assess from a policy perspective."

ANZ senior economist Matthew Galt is picking a 0.2% rise.

"The sectoral data released over recent weeks has come in weaker than earlier leading indicators had suggested, prompting us to revise down our forecast to 0.2% q/q (from our preliminary forecast of 0.7% q/q)," he said.

"Construction and food manufacturing activity over Q4 in particular fell short of our expectations. This may be down to a combination of house prices staying flat, lags in building activity, and quarterly volatility in meat processing. Indicators for a few services industries, such as professional services and wholesale trade, were also weaker than we had expected.

"However, the broader suite of sectoral data points to moderate growth across other parts of the economy in Q4, underpinned by rising spending in response to lower interest rates, solid farm incomes, and growth in tourism."

Galt said "a downside surprise" to the RBNZ’s GDP forecast of the size that the ANZ economists are forecasting would have only have a small impact on the RBNZ’s thinking.

"GDP data is lagged, telling us how the economy was during the October to December period (now three to five months ago). It has also been volatile lately and is prone to revision.

"What’s more, it covers a period well before the current conflict in the Middle East broke out and oil prices spiked, which is the biggest uncertainty in the economic outlook right now."

Bring on the next one...

Okay, if we assume the December quarter GDP figures do show slight growth, but slower than the September quarter, what of the current March quarter?.

As per its February MPS forecast, the RBNZ was expecting good things this quarter with its 1.1% growth pick. But the open question is how much the Middle East conflict has knocked and will continue to knock things back.

Ultimately it all depends how long the Middle East situation rumbles on for. Certainly with our annual inflation having been sitting at 3.1% in the December quarter - so, outside the RBNZ's 1% to 3% target range - we've got little room to move.

The other side to that though is whether the uncertainty may just cause people to go back in their shells again and causing the economic recovery to wither.

And if the December quarter GDP outcome turns out to be not particularly good, will that cause a knock to confidence and hesitancy with spending?

The upshot is that our economy is, for the moment, actually looking in reasonable shape (finally) for a decent sort of recovery to develop. But this whole Middle East situation is once again a stark reminder of how small we are and how easy it might be to blow us off course.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

71 Comments

Oh well just bouncing along the bottom then. Historically though nz doesnt really get moving again until housing does. Without construction and turnover picking up, gonna be hard to see where our sustained growth will come from.

Housing value is to meet the basic human need for shelter. Owning the home is the cost of providing shelter for oneself and loved ones. The price one pays to own the home is not the value, it is the cost. The inherent value lies in the shelter and protection it delivers.

It is a fool's errand to expect continual growth in the cost of buying a home. Such growth is not lineal, it is exponential, the growth compounds year on year. $1 invested today at 4% compounding over 50 years grows to be 6.8 times the original $1. Put that in realestate terms, the $900,000 house you buy today would cost $6.2 million in 50 years time. Or at 2% compounding would cost $2.4 million. On that 2% compounding and the house is a rental, then at a rental rate of 6% of capital cost, the rent would grow from $1035 week today, to $2740 per week in 50 years time. And if rental cost is 30% of household gross income, household income would need to grow from $3,462 per week now ($180,000pa) to $9,134 per week ($475,000pa).

It's not sustainable.

The government of the day needs to develop and implement a cross party supported 30 year strategy to grow the productive economy. That will include incentives that ensure the great innovations that are developed in NZ are retained in NZ, maintaining employment here, and returning export dollars into the NZ economy, rather than continuing supporting the innovations only to see them sold offshore with the long-term income streams feeding into offshore economies.

30 years ago Treasury caste the agriculture sector as a sunset industry with the future of NZ being the knowledge economy - sounded terrific but dulcet tones and pretty words do not pay the bills. That sunset agricultural industry survived through some extremely tough years at uncountable human cost to the farmers at the coal face. Yet here we are today and that sunset industry continues to do the heavy lifting in export income generation, to keep the lights on here in NZ.

We dont need compounding house prices forever, as nz basically had flat'ish prices from the late 70s to the early 90s.

Hoqwever, housing is still one of nz major growth engines, and we’d probably be unwise to ignore that, even if it probably shouldnt be the only one long term

Housing is still one of NZ growth engines.

It should not be, flat.

That is like giving up your seat in the titanic lifeboat, staying with the ship instead, because the manufacturer said it was unsinkable.

Moving away from house price inflation as an economic driver (not construction - more people need shelter as population grows) is a must do. There will be pain - as farmers in the 80s and 90s experienced, and those who bought with low equity at peak house prices are experiencing right now. It's depressing, it sucks and the impacts on willingness to spend/take risks linger for a long time at the individual level - I speak from lived experience. My parents were children in the 1930s depression era, a particularly painful period for many, many, Kiwis. It shaped their conservative attitudes to borrowing and spending for their entire lives. Did they live a dreary life? Absolutely not.

The transition needs to happen now and it needs to happen at pace.

As many farmer's found, there is life after the farm was sold by the bank. It's not the end of the world (although for some, sadly, it was). It's just different and it is what you have the courage to make of it.

So we are now year 4, into the biggest property crash, since the 1970s. It's good to see this slide not letting up soon, until DTIs are back towards 3 or 4xDTI.

- Many people have dropped the blinkers on "houses doubling every 10 years" and looking to invest into the productive side of the economy, where we export products and services. Real GDP growth via increased exports, is our only way forward.

This stupid, pre 2021 fixation, on selling homes to each other at higher and higher prices is now dead and buried. Those currently hold high debt grenades will feel the increased pain, as higher and higher mortgage rates ease the pin out.....

Holding your fellow Kiwi to ransom, on higher housing and rental costs, was very parasitic and glad that story is now a pre-2021, historical anomaly.

Cheap or at least competitive, reliable energy, has to be a Govt priority from here and increased FF drilling, while building new Hydro "quickly" should be incentivised by the Govt. We really need another giant gas field like Maui.

Drill, Blast, Dam baby!

Yeh exports are important but nz has been saying we’ll pivot to the “productive economy” for about... ummmm 30 years or so now.

In the meantime housing and construction still end up doing a lot of the heavy lifting.

But that housing side does no lifting other than to indebtedness. It does not introduce new money into the economy as export income. Construction rotates money that is already in the country but is a net drain on export funds because of the amount of inputs that are imported.

Labour is the largest input, and as the materials have to be to specific NZ standards, their production is a lot more indigenous than imported.

It is one of the only indigenous manufacturing sectors we have left.

It does do a bit of lifting tho, as construction still employs a lot of people and tends to drive a fair bit of action around the place once it gets going

Agreed, I specifically excluded construction in my comment.

The government of the day needs to develop and implement a cross party supported 30 year strategy to grow the productive economy. That will include incentives that ensure the great innovations that are developed in NZ are retained in NZ, maintaining employment here, and returning export dollars into the NZ economy, rather than continuing supporting the innovations only to see them sold offshore with the long-term income streams feeding into offshore economies.

That's what they need to do, but it's very easy to say, and much harder to actually define.

How do you incentivise a company to not leave for much larger addressable markets, or produce where it's much cheaper?

You mentioned agriculture, but the reason that survived and thrived is because the government stopped subsidizing it so heavily.

And you can't pack up the paddocks and relocate them in another country.

Incentives? Implement land taxes or some capital gains tax on residential land. Reduce corporate and personal income taxes. Strengthen rules to reduce or eliminate transfer pricing (limit transfers of non taxed revenue to 10% of gross revenue, investment incentives as a repayable advance attracting interest if sold offshore within say 15 years.....That's just off the top of my head, not thoroughly thought through.

And you can't pack up the paddocks and relocate them in another country.

You definitely can't, but you can do that with any secondary or tertiary process once you've produced the raw materials.

Incentives? Implement land taxes or some capital gains tax on residential land. Reduce corporate and personal income taxes.

Just moving tax levers won't necessarily resolve the sorts of issues that have NZ businesses outgrowing New Zealand.

Productivity is a very difficult thing for a government to "incentivise", because if you have a sound plan to dramatically improve productivity it's generally self funding.

You could fix that and the healthcare system with 1 stroke of the pen. Make NZ a tax haven for medical research with the proviso that the companies sink X% of their research into NZ.

The government of the day needs to develop and implement a cross party supported 30 year strategy to grow the productive economy.

Listen to Uncle Phoenix. Or even better, Richard Werner:

Werner disaggregates credit into:

- Credit for GDP transactions: financing new goods and services, working capital, productive investment.

- Credit for non‑GDP transactions: financing existing assets (property, land, shares, M&A, etc.), which do not directly increase current GDP.

Only the first type drives real growth; the second mainly drives asset prices. Once credit growth to property slows or reverses (due to tighter regulation, rising rates, or balance‑sheet constraints), the process runs in reverse:

Falling property prices weaken collateral, forcing deleveraging and credit contraction. Banks face rising non‑performing loans and tighten lending, amplifying the downturn. Because so much prior credit went into non‑GDP property transactions rather than productive investment, the Aotearoa economy is left with high leverage / h'hold debt to GDP but limited new income‑generating capacity, making economic growth at an aggregate level harder or impossible.

https://www.stuff.co.nz/home-property/360949468/so-you-bought-peak-now-…

Apparently, the younger generation do not see housing as the be all and end all of investment. Will make it a bit more difficult to unload the 4Br house bought at the 2021 peak.

Hard to see an upwards "recovery" in house prices any time soon.

Around now the government should be urging some rationing of fuel like they are in other countries. But that will depress GDP even more. 50 days of supply will go quickly. Heard an interview with Willis where she used her chirpy voice and said: "we just gotta get the Strait of Hormuz open!".

If that doesn't happen we're cooked!

Yeh 50 days of local stock. With shipments already on the way its prob closer to around 100 days of supply.

I think its 50 days including the shipments on the water.

"The Ministry of Business, Innovation and Employment reported, as of Thursday, New Zealand had a total of 52 days fuel stock.

This was made up of 30.3 days in the country, and 21.7 days en route."

Looking forward to the 1pm press conferences and the Podium of Truth

At the end of the day some countries will have to reduce demand and it won’t be the wealthy countries like us, it will be poorer countries in Africa. But it will increase our prices and inflation. And our debt once the government bows to public pressure and subsidies it.

Price is not the only constraint here...supply is also an issue that wealthy governments will also have to contend with.

Demand needs to reduce to match the supply, 20% reduction I believe. That should be achieved by price. Unless stupid governments don’t understand this and start to subsidise.

Correct and we don't hold much say if someone else is deemed a higher priority than us for our supply it seems. There's a lot of hope out there that Trump will cave etc but I don't think he has as much say as everyone would like, especially if Iran sees the impact the closed Strait is having it'll be in their interest to keep it that way for a while.

Updated every Wednesday....once a week. Sailing time from refinery to NZ ports is around 20 days....onshore storage appears to be around 30.

We are one missed shipment away from shortage, nevermind the panic buying underway, and states (including those who supply us) are imposing restrictions.

Ah right, thought the 50 days was domestic storage only. Didnt realise that already includes fuel on the water

Cheers

They're probably a bit wary of going hard and early in case they get criticised by an inquiry in about 6 years time.

If 4th quarter GDP underwhelms, the ice under Luxon will become that much thinner.

It will be this quarter and the next that will really tank if this war continues. Next quarters GDP must come out around election time. He’s Nationals icon for economic recovery, if it doesn’t happen they’ll have to swap him out.

Paying the price for not investing in infrastructure in year 2.

December quarter: jobs yoy still negative, private sector earnings fell in real terms, while reduced debt servicing costs supported businesses to increase profits and pay down debt. Investment is still low. Weak domestic demand for imports and higher export prices closed the trade balance a bit.

All of the above will translate into a slight quarterly increase in gdp. But, don't be fooled. GDP is simply measuring a change in the flow of money. Some of the cash that was flowing from businesses and households to savers and bank equity holders, is now flowing from businesses and households to company owners / shareholders. Businesses are still paying off more debt than they are taking out.

This is NOT a recovery, it is a flatlining economy. Now, enter stage right, a clueless Govt intent on holding to their fiscal plan, and, far right, a Trumpian doomsday oil price and supply shock. We are so screwed.

NZs economists and commentators must be world leading in their continual putting of lipstick on a pig, which is our economy. The rediculous property bubble has finalky burst and the only drivers we have left, are the growing of grass and our weak currency, which attracts curious people to venture down to the bottom of the globe to have a look at a scenically beautiful country and a genuine hermit kingdom.

Yes true there never really has been any genuine statistics showing a recovery, just little glimmers of hope in amongst some pretty bad data too. Although to be fair the stats are so late the economists do have to guess.

A genuine and true NZ economic commentator would rather stab out their own eyes than observe the existence of fiscal policy and it's real-world significance in a fiat currency based economy. That's actually incredible but right on script. No mention of the job and business destruction that has occurred at record setting pace and level. The largest employer, investor and spender in the economy has been in contraction mode - in real terms - for 2 and half years and this has sucked demand out of every level of the economy. Fragility and stagnation is the very predictable and obvious outcome.

Let's add $4/litre petrol into the economy and see what happens. Maybe if we had kept incentivising small fuel efficient cars this wouldn't hit to hard.

Yeah maybe 3 years of subsidies would have cost less than this will cost in terms of worsening economy and/or excise cuts.

Imagine if they’d employed an extra 30,000 people on $100k instead of the $3 billion in tax cuts! In fact those people also pay PAYE and don’t collect the doll, so maybe they could employ 60,000 people for the same cost.

Those people don’t need to be sitting around with their finger up their bum, they could be laying pipes or building hospitals.

I said this at that time that we’d probably end up better off without that $20 a week and I suspect that’s already played out. A couple of years of a growing economy instead of a shrinking one would probably have increased the average wage by more than $20. Unfortunately the average NZ voter ain’t too bright, they love a good election lolly even if it is bad for their health.

Any views on what the RBNZ will do?

If 91 prices are still over $3 at the next OCR review (April 8) she has to hike doesn’t she? And probably by 0.5%. CPI out of band and rising, there is only one option. And that option will destroy any green shoots.

And if 91 goes over $3.50, that’s an emergency OCR review? The RBNZ got a good lesson on inflation just a few years ago!

Any views on what the RBNZ will do?

Hard to say. All central banks have known for decades is linear growth based on the world being a certain way.

We're looking at fuel prices and going "better get the rates up, inflation is on the rise". But what's underpinning the rises has very strong recessionary indicators that have the potential to exponentially worsen.

The worlds now going another direction, and with it economics will need to be reconsidered.

She is in charge of inflation and the OCR is pretty much her only lever. Surely she has to give it a good yank. Or is it transitory again?

She is in charge of inflation and the OCR is pretty much her only lever

If you watch the RBNZ, they can and do roll out additional tools in addition to the OCR, often to resolve topical issues.

Instances include introducing an LVR (loan to value ratio), capital policies, that sort of thing.

Do they have something else to tackle inflation? The LVRs etc only help house price inflation. They can do quantitative easing to allow money to flow but that would only cause inflation.

I think the OCR is her only option. But it will come at a significant cost.

They won’t hike. We have no wage pressure and this spike in prices will be largely on necessities so will act like monetary tightening. So their models will be seeing the drop in activity overwhelming the shorter term price spike.

I don’t envy their job here it’s really a lose/lose scenario cause we know they will get criticism in hindsight regardless

Exactly. The OCR is used to increase or decrease the demand side. We're not seeing a demand increase pulling prices up. The RBNZ has no control over the price of oil, it's refining price or the price of transporting it to NZ so expecting an OCR increase to have any impact there is a strange one. This is an issue for the government to intervene in not the RBNZ.

If the OCR is used to increasea or decrease demand - why did we keep dropping interest rates when we were importing deflation via cheap goods/foreign labour?

How does creating more mortgage debt (the result of dropping the OCR) solve the deflationary impact of using workers in China and Vietnam to manufacture our goods and services?

It doesn't - but we did exactly that for the last 30 years.....resulting in very high private debt vs GDP. Meaning that inflation shows up, we can't raise rates without destroying the economy as too many people would default on their private debt.

We've been running an extremely daft economic strategy for a number of decade now and I think our chickens are coming home to roost.

As below. I think if it gets bad enough with fuel prices rising due to production/importing costs/supply then there'll need to be subsidies via the government. It'll stop most of those costs getting passed on through the economy until, hopefully, some normality eventuates. Because once consumer prices rise they won't come down bugger all again. Best to stop the rise in the first place and in this instance I don't believe the OCR will prevent that if the core issue is fuel supply. The economy is in the dog box as it is. There's no heat in it to try to control. Whacking extra costs on credit isn't going to help prevent costs being passed through due to fuel prices. It'll cause more businesses to close and unemployment to tick up.

I agree with all of your points regarding our economy up to this point in time. Especially regarding house prices as I've been singing from the same sheet just not on here as much. We've boxed ourselves into a corner well and truly. But this event that's happening I don't think can be considered in the same light as a progressing/regressing global economy. It'll require some different actions. As Yves keeps saying here as well, the OCR can take up to 18months to start having an effect. In this instance we don't have that sort of time frame to make an impact.

Why then haven't we been putting tarrifs on goods and services made in foriegn countries when they were causing us to import deflation? (if our answer to importing inflation is for the government to fix the problem, not the RBNZ?)

The response to importing deflation for the past 30 years was to lower mortgage rates so we could create more private debt and higher house prices (aggregate demand) but in the process destroy our production/manufacturing base.

So to be clear - you think the government should step in when we import inflation, but do absolutely nothing when we spend decades importing deflation?

Its ironic or hypocritical to think the government should subsidise society when fuel costs go up so that businesses don't close because of higher inflation...but we've just spent decades destroying businesses around the country by not fixing a deflationary problem where we allowed foreign businesses to out compete our local industries and create deflation in our economy.

Don't you see how crazy and imbalanced this thinking is?

The wage pressure will flow through when people demand more $$ from their employers in order to pay for fuel and groceries. You guys are thinking in first order effect (ie current conditions) - not the consequence of what is probably going to happen if fuel prices don't come back down within the next month or two.

Didn’t the last bout of inflation start with fuel prices?

I don’t think they’ll sit around while inflation is above CPI. Inflation was above target before fuel prices went up, but they said it was going to fall back in band later this year. That seems very unlikely if fuel prices stay high.

Another random thought - the best thing the government could do right now is whack a $0.50 a litre extra fuel tax on. That will reduce demand and help our supply last longer. But I suspect they will end up doing the opposite, because even the blue side conveniently forget the rules of supply and demand when it suits.

Which according to your above post would have an inflationary effect and require the RBNZ to lift the OCR by 0.50%? How is lifting the OCR going to increase the supply of fuel which is what would be effecting the price rather than demand.

Yep it will also mean the RBNZ has to hike even more. But if we are actually going to run out of fuel, the only other solutions are carless days etc, probably a worse hit on the economy.

It’s always better to use price to ration something than arbitrary rules. Price rationing will mean the most valuable trips can still take place.

"Yep it will also mean the RBNZ has to hike even more."

Is this theory correct in a stagnating economy though? Price increases from fuel that flows into other sectors will punish consumers as it is without having to get whacked with higher credit costs as well. Those fuel price increases aren't going to change depending on where the OCR is if it's a supply side problem.

Your last sentence might not make much sense if it's supply constraints we're faced with rather than a demand increase. In that case then restrictions on fuel use will be the only option to prioritise critical needs.

If fuel goes up then the CPI will too. Unless of course other prices go down, which I highly doubt. The RBNZ only has two options that I can see - either consider it transitory (which didn’t work for them last time), or raise the OCR.

As for rationing, if the price goes up people will stop taking less important trips; going to the mall etc. But it will still make sense to drive to work instead of staying at home. It would be hard to use rules to implement anything as good.

"Sorry I should have been clearer, I meant if fuel is indeed going to run out."

Raising the OCR won't increase the supply of fuel.

Raising the price of fuel won't ensure critical services have priority to needed fuel. It'll just cost those service providers more for no benefit.

The core issue is supply, your argument above. Trying to fix the downstream effects of that with an OCR hike which won't have any effect on supply isn't going to help. If you're worried about inflationary effects the government would be best to cap/subsidise fuel price increases like they should have over covid. As well as rationing fuel so it's used where it's needed first. This is obviously if we are going to run out or have a very restricted supply as per your point above.

Did dropping the OCR increase the prices of goods and services in the CPI basket we imported using cheap foreign labour from China and Vietnam?

What was the plan then for the past 3 decades of dropping lending rates to counteract the deflationary impact of using cheap foreign labour to fund our lifestyles?

It means that if we start importing inflation, we absolutely have to raise rates. Because you can't spend decades dropping rates when you import deflation but then decide to not raise rates when you import inflation. It will immediately show how badly we've been living beyond our own means of production (and how bad our private debt has become relative to our productivity (GDP)). Inflation will spiral through the economy as people demand more in wages to put fuel in their cars and buy groceries from the supermarket (all which will go up as transport costs rise).

All those factors happened over a time period measured in years not days like the current situation. Seriously, how soon do you expect an OCR change to make an impact? It's usually 12-24 months not a couple of weeks. This isn't an issue that needs to be sorted by the RBNZ.

"This isn't an issue that needs to be sorted by the RBNZ"

Well then the same argument must be made that the issue of importing deflation from cheap labour in foreign nations cannot be solved by the RBNZ either (because it cannot/could not be). And yet we spent decades doing exactly that (and now have many problems in the economy because of that - one of which is very high private debt vs productivity/GDP) . But you seem to be okay with that like it is normal or okay - but that in fact is just confirmation/recency bias where you believe what has happened recently is how things are or how they should be. This isn't true (in my opinion).

To summarise what has been happening in the last few decades: "Hey the CPI basket has lots of goods and services in it using cheap labour in Asia meaning prices aren't really going up - RBNZ - we need you to create more aggregate demand in the economy by lowering interest rates to avoid the country going into a deflationary spiral - 'ok no problem' Oh look because rates are lower we can create more private debt even though we are offshoring all our jobs to foreign countries. But isn't that a bad thing? Oh no don't worry about it...But what happens if we ever start importing inflation again? Won't we be a sitting duck in a very vulnerable situation? Don't worry about - we are all getting rich right no so who cares. If inflation appears we will just look through it because we can't service our private debt levels if we have to raise interest rates".

"How is lifting the OCR going to increase the supply of fuel which is what would be effecting the price rather than demand"

How has dropping the OCR helped to stop the deflationary effects we've experienced the past 30 years by offshoring manufacturing and production using cheap foreign labour?

All it has done has increased our private debt to GDP.

So you can't decide for 30 years to drop the OCR because you are importing deflation but then decide when you import inflation to not increase the OCR. Otherwise you find yourself in a banana republic that exists only for the benefit of bankers and RE industry, who benefit when more private debt is created as the OCR is dropped.

That's a bit disingenuous IO. You expect the RBNZ to make a bad decision now because it's made bad decisions in the past? A (potential) fuel crisis like now isn't standard market dynamics so conflating it with China becoming more of a capitalist society over the last couple of decades isn't a comparison but I do agree with the thrust of your argument.

The OCR, as you'll agree I'm sure, probably shouldn't have been lowered as any demand they wanted to stimulate ended up in larger mortgages not captured by the CPI, rightly or wrongly. But all that was a demand issue. Private spending did increase with credit that wasn't measured in the CPI. This time it's not the private sector/consumers driving the price changes.

You're letting your disdain for the RBNZ and FIRE sector (which I completely share) cloud your view on this particular issue. As I said above, if there's to be any changes (which there will have to be if we end up in the scenario JJ is talking about) then it should be a government input not a RBNZ one.

"You expect the RBNZ to make a bad decision now because it's made bad decisions in the past?"

Of course. A leopard doesn't change its spots. Do you expect a fool to suddenly act with wisdom?

"You're letting your disdain for the RBNZ and FIRE sector (which I completely share) cloud your view on this particular issue"

That is your opinion. But look at the facts. How else did we end up with such high private debt vs GDP? And why is this a problem? And how do we resolve this? And what happened in the 1970s with inflation when oil prices spiked? Perhaps you're letting your disdain for my comments cloud your judgement on this particular issue.

You can't run a system using a set or rules, but then disregard those rules when it no longer suits you. That is how corruption occurs and systems break down (you can't spend decades lowing the OCR when you import deflation, but then decide you are not going to raise rates when you import inflation).

Right, we're talking at cross purposes here, at least to my eyes. I agree with everything you're saying regarding how the OCR has been used and should be etc. But you're talking about the long term issues. What I've been talking about here is to do with JJ's comment regarding running out of fuel or having a limited supply and the effects from that. The effects are going to happen over a very short term so as I've said, there won't be the time for the OCR to have any effect and it won't fix the supply issue. No disdain for your comments but I've been reading what you write for quite some time so I know what your views are on the overall economic system.

This isn't about changing the way the RBNZ uses the OCR, just that it won't have an effect on the current problem.

More realistically this calls on the government to use it's balance sheet to absorb the inevitable private-sector destruction that an energy price shock will cause. The government needs to use expansionary fiscal policy as a counter balance - fuel rationing and subsidies would be top of the list. And a massive government funded investment in roof-top solar and rapid, large-scale electrification of our current logistics fleet.

No-one has mentioned that NZ's gentailers stand to make an absolute killing if the cost of inputs like gas and coal rise significantly - remember the highest cost input into generation is what sets the price of electricity in NZ. And not the abundant and low cost option of hydro.

Sorry I should have been clearer, I meant if fuel is indeed going to run out.

In theory, increasing fiscal spending while inflation is rising will only make inflation worse.

And free public transport?

Good luck with that with the Nats in charge. But yes if they were going to subside something that would be the way to go

I don't think free is necessary , I think $5 at first step on free for the rest of the day would be enough.

While GDP may be moving around, the per capita GDP is a better indicator of how efficient and competitive we are - and it is is only infrequently cited.

https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?locations=NZ-AU

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.