The Reserve Bank is playing down the likely impact of restricting the borrowing capacity of first home buyers through debt to income ratio (DTI) tools, but says it enforcing a test interest rate floor for banks could hit first home buyers hard and this tool is thus only seen as an interim measure.

These issues are discussed in the Reserve Bank's consultation paper on its potential implementation of debt serviceability restrictions released on Tuesday. The paper floats the possibility of the Reserve Bank using DTIs or setting bank test serviceability interest rates for mortgage borrowers, which banks currently set themselves, if it believes financial stability risks warrant them.

An initial assessment of the expected impacts of implementing a DTI cap of six or seven times gross income, and of a test interest rate floor at 7% or 8%, is provided in the consultation paper. However, the Reserve Bank says these settings are illustrative and don't mean the tools would be calibrated at these levels if introduced.

Nonetheless the Reserve Bank says banks need to prepare their systems for the potential introduction of a regulated DTI limit no later than the end of 2022. It estimates a DTI restriction could be implemented by the fourth quarter of 2022, and a test rate floor could be implemented as soon as the second quarter of 2022.

The consultation paper down plays the expected impact of the introduction of a DTI tool on first home buyers. Debt serviceability restrictions, the Reserve Bank says, don't affect the fundamental supply and demand balance in the housing market and therefore any impacts are likely to be marginal.

"At a DTI cap of seven, around 1% of first-home buyers or other owner-occupiers are prevented from purchasing a similar property following the introduction of the restriction – they would either purchase the property at a lower price, and hence be financially better off, or be allocated into the speed limit. Investors are the most impacted in terms of restricting purchases of equivalent properties," the Reserve Bank says.

"At a DTI cap of six, around 5% of first-home buyers or other owner-occupiers are prevented from purchasing similar properties. By contrast, there is a material impact on restricting investor purchases."

A political football

Both the current and previous government were reluctant to let the Reserve Bank add a DTI to its macro-prudential toolkit alongside existing tools such as loan-to-value ratio (LVR) restrictions. And earlier this year the Government issued a direction under the Reserve Bank of New Zealand Act requiring the Reserve Bank to; “…support more sustainable house prices, including by dampening investor demand for existing housing stock which would improve affordability for first home buyers."

However, in August Finance Minister Grant Robertson finally approved the move, enabling the Reserve Bank to push ahead on arming itself with a DTI tool.

The consultation also estimates the use of a DTI tool could reduce house prices.

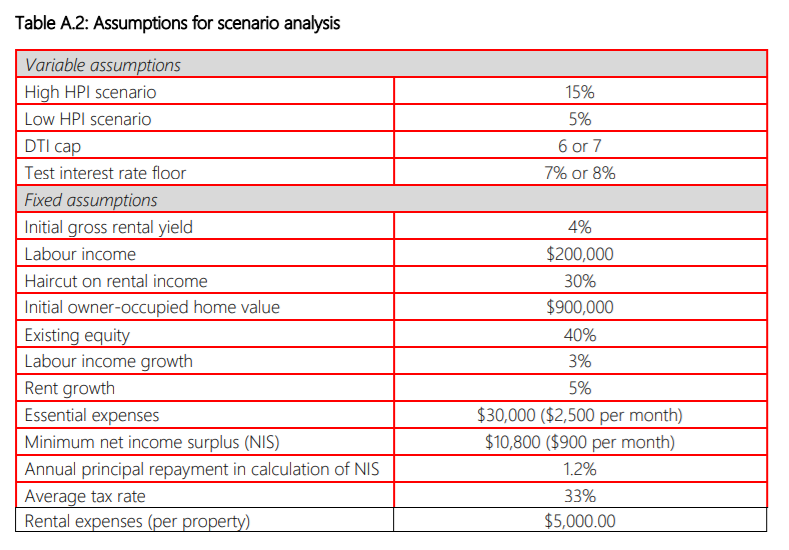

"We have assumed in our central scenario that house prices fall by 5% following the introduction of DTIs, relative to the status quo. We also consider scenarios in which prices remain flat and fall by 10%," the Reserve Bank says.

The central bank and prudential regulator's estimates of the impact of a DTI on first home buyers and house prices are more restrained than when it previously consulted on a DTI tool in 2017. Then it said restricting the DTI ratio of some mortgage borrowers could prevent about 10,000 borrowers from buying a house, reduce house sales volumes by about 9%, trim house prices and credit growth by up to 5%, and shave 0.1%, or $260 million, off Gross Domestic Product.

According to the Reserve Bank, estimating the impact of debt serviceability restrictions on house prices is hard, especially because they haven't been used in New Zealand before.

"In our 2017 consultation, we estimated that, after allowing for the likelihood that some constrained borrowers would be replaced by low-DTI buyers, house sales [volumes] could fall by around 9% following the introduction of DTI restrictions at a cap of five, which in turn could reduce house prices and credit growth by 2% to 5%, relative to a status quo scenario without restrictions in place."

"Since the 2017 consultation house prices have continued to rise faster than incomes and DTI ratios have become even more stretched. We estimate that a DTI cap of six now would be roughly equivalent, in terms of the amount of lending constrained, as a DTI cap of five in 2017," the Reserve Bank says.

First home buyers in the firing line from a test interest rate floor

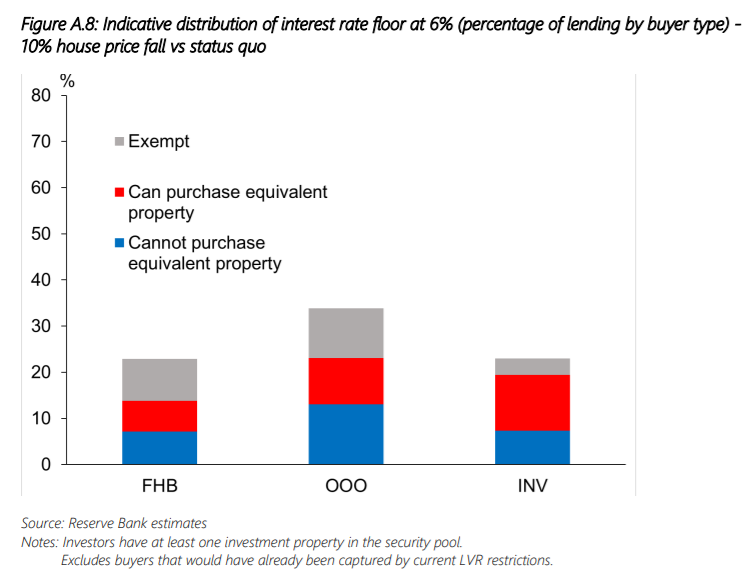

In terms of a test interest rate floor, the Reserve Bank says if one was applied evenly across borrower groups, it would hit first-home buyers the hardest because their surplus income is relatively low.

"It would also be likely to impact considerably more first-home buyers than a DTI restriction. Furthermore, a test interest rate floor is likely to impact investors the least as they have relatively high surplus incomes because they can adjust their expenses more easily than other borrowers," the Reserve Bank says.

"If we were to implement a test rate floor, potential negative impacts on first-home buyers would need to be considered carefully in light of the Government’s housing policy objectives. It may be possible to mitigate these impacts by applying a different rate floor to different borrower groups, or through the use of exemptions. However, this is likely to add complexity and lead to higher administration costs. This could potentially undermine the benefit of a test rate floor being straightforward and faster to implement than a DTI limit since it fits within banks’ existing systems for assessing serviceability."

"Our current view is that we would be unlikely to impose both a test rate floor and a DTI limit simultaneously. Rather, we consider a test rate floor as a potential interim measure that could be used to address short-term financial stability risks, while we work with the industry to finalise the design and implementation of a DTI limit. Therefore, any negative impacts on first-home buyers from a test rate floor are likely to be short term in nature," the Reserve Bank says.

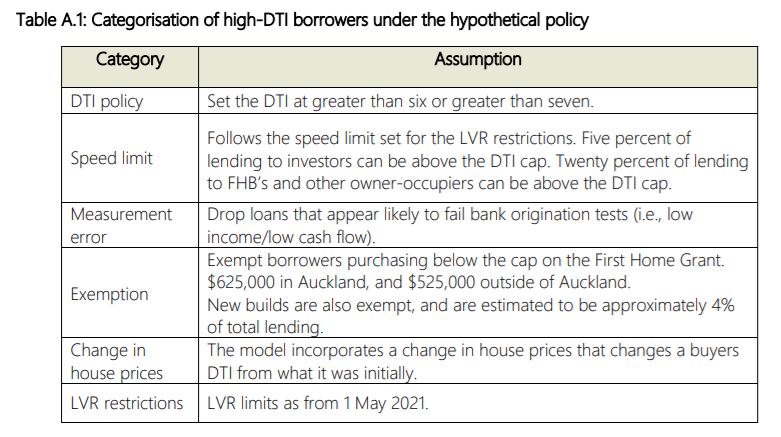

The model in the Reserve Bank consultation paper features a speed limit like with LVR restrictions, exempts borrowers purchasing below the house price cap of Kāinga Ora’s First Home Loan and new builds, and allows borrowers to reduce their DTI by buying a cheaper property.

In modeling the potential impacts of a test interest rate floor, the Reserve Bank calculates an estimate of the borrower’s surplus income. This gives an estimate for expenses and a buffer for unexpected expenses, allowing surplus income to be calculated.

"For the buffer, we assume $700 per month for owner-occupiers and $900 per month for investors. We subtract tax, expenses, and the buffer from gross income, giving us surplus income that can be used to service a mortgage. We then calculate how much the repayment would be on the borrower’s debt, at the test interest rate floor, and compare to surplus income. If the mortgage repayment at the test interest rate floor is greater than the borrower’s surplus income, then the borrower is constrained and has to lower their current debt level," the Reserve Bank says.

Debt serviceability restrictions not seen replacing LVRs

The Reserve Bank goes on to say that debt serviceability restrictions and LVR tools address different aspects of housing market risk. Thus if debt serviceability tools are used, they'll likely be used alongside LVR restrictions rather than replacing them.

It also notes that while international evidence is mixed in terms of the impact of macroprudential tools on house prices, the majority of studies that do find an effect find that debt serviceability restrictions are more effective than LVR restrictions in moderating house price inflation.

"This is likely to be because debt serviceability restrictions link credit growth to income growth, which is more stable over time than housing equity," the Reserve Bank says.

"There is limited empirical evidence available in the New Zealand context regarding the impact of higher debt levels on probability of [loan] default, given we have only been collecting statistics on loan DTIs at origination since 2016. However, international evidence supports the view that debt serviceability metrics such as DTI ratios are important indicators of default risk, and that debt serviceability restrictions can help to mitigate these risks."

The consultation paper also mulls whether other types of debt held by a residential mortgage borrower, apart from home loans, should be included within the DTI calculation.

"Our provisional view is that total household debt would be the most appropriate measure, rather than only mortgage debt, since other types of debt also represent a liability for the borrower."

"We note that consumer debt, such as credit cards and personal loans, normally attracts higher interest rates than mortgage debt. Hence, if a total debt measure is used there could be a case for giving such debt a higher weighting than mortgage debt in the calculation," the Reserve Bank says.

"However, given that mortgage debt accounts for the vast majority of household debt in New Zealand, we believe that making adjustments for other types of debt could add unnecessary complexity to the DTI calculation. We therefore favour using a total unweighted measure of household debt. Banks would still be free to differentiate between mortgage and other debts when undertaking their internal serviceability calculations."

Exemptions etc

A further question floated is whether DTI caps should apply to all residential property in a borrower’s portfolio, or only to owner-occupied property.

"We note that some countries, such as the UK and Ireland, apply DTI restrictions on owner-occupied lending but regulate investment property lending in a different way. Our current view is that a broad DTI cap makes sense in the New Zealand context, since investors with multiple properties often cross-collateralise their properties, including cross-collateralising between owner-occupied and investment property, and use both rental and personal income to service mortgage debts."

"Two possible exceptions to the approach of weighting all household debt equally could be student loans and small business loans with residential property as security. Student loans are not currently subject to interest for borrowers based in New Zealand, and hence there is no additional serviceability risk as interest rates rise," the Reserve Bank says.

"In addition, if borrowers lose income temporarily, e.g. become unemployed, they do not need to continue payments on the loan during this period. Therefore, the risk of student loans contributing to a negative feedback loop in a downturn are much less than for other types of lending."

It wants banks to exclude student loans from total debt, but deduct student loan payments from income given that the repayment depends on income rather than debt.

In terms of business loans with residential property as security, the Reserve Bank says these comprise only about 1% of total mortgage lending, according to its LVR survey.

"As such, it could make sense to exclude this debt from the DTI calculations and rely on banks to make their own serviceability assessments with respect to small business lending. We are still working through this and would welcome feedback," the Reserve Bank says.

And, in terms of exemptions to DTI restrictions, the Reserve Bank is proposing these should mirror the existing LVR regulations wherever possible.

Categories of lending exempt from the LVR regulations include: Kāinga Ora First Home Loans; refinancing with another bank on the same terms; loan portability; bridging finance; construction loans; remediation loans; combined collateral; and loans granted in error.

DTI restriction would hit investors hardest, RBNZ says

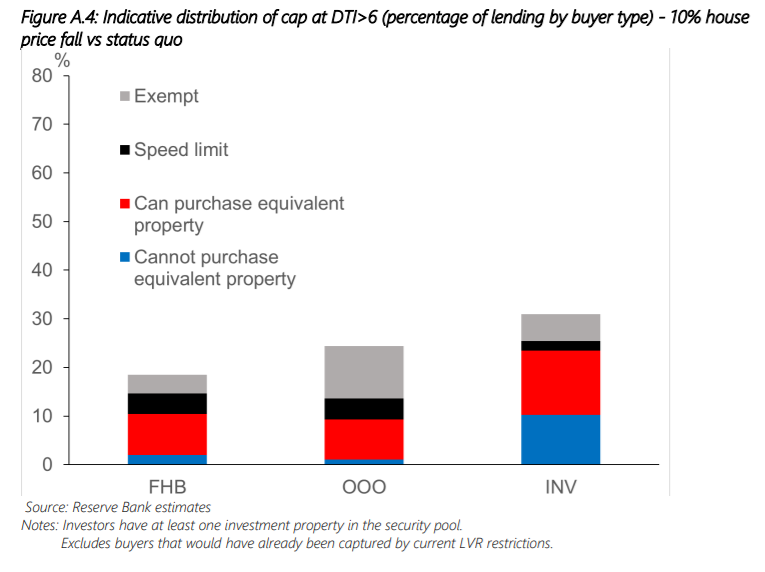

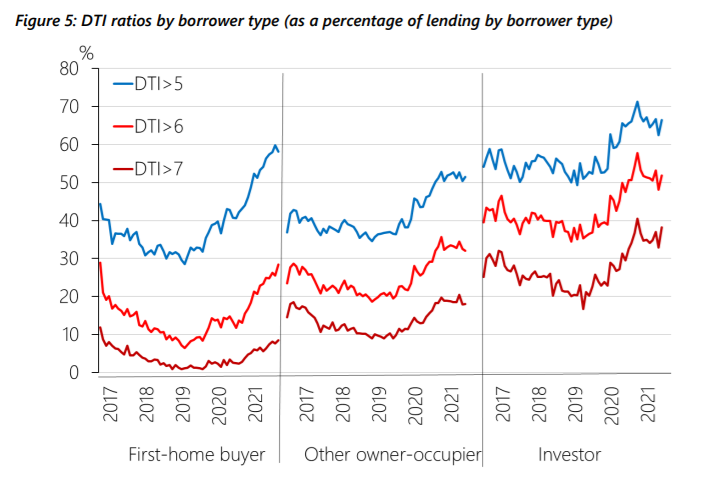

The Reserve Bank says its modelling shows a DTI restriction would have the largest impact on investors, followed by other owner-occupiers, with first-home buyers being the least constrained by the cap.

"This is because investors borrow at higher DTIs than other groups on average, so would face a larger decrease in what they could borrow [see figures A.4 and A.8 below]. In addition, the use of speed limits and exemptions would further mitigate any impacts on first-home buyers. This suggests that DTI restrictions align well with the Government’s housing policy objectives of dampening investor demand for existing housing stock whilst minimising negative impacts on first-home buyers."

"Our assessment indicates that DTI restrictions are likely to be the most effective debt serviceability tool that we could deploy to support financial stability and sustainable house prices [because] DTI restrictions link credit availability to income growth and are likely to be more effective in constraining debt levels over a longer period than other tools, including interest rate floors and LVR restrictions," the Reserve Bank says.

(Note FHB is first home buyers, OOO is other owner-occupiers, and INV is investors).

The Reserve Bank is seeking feedback by 5pm on February 28.

24 Comments

Labour income growth: 3% -> haha.

Couldn't see this in the article. But what a load of rot if they're suggesting that credit creation growth is in line with income growth.

It's in the provided table.

Labour income growth: 3% -> haha.

Why not?

Even if you're only getting 2%, every few years you'll get a promotion or change jobs, so +2 +2 +2 +2 +10, which is more than 3% annualised.

In practice a lot of people don't get this choice and don't even get a salary raise every year. Averages can often be misleading and assumptions this big should not something we should be seeing coming from the RBNZ.

Sounds ok. Bring in a DTI of 6 at the end of the month.. job done.

…Orr shall we procrastinate some more.

Never seen such a bunch of hot air specialists in all my life.

Job done and retire on huge pension

This RBNZ is either blind or just mind numbing dumb.

Sorry wait no no. They are just highly paid bureaucrats who have never left their chairs to see how a poor man makes the money, feeds the kids or pays the rent.

These are rich idiots who have no idea how to make a dollar because they get paid unreasonably high salaries by tax payers.

We should collectively tell them that we do not need you or your analysis. They should work on making a road and then learn how to make real money.

"RBNZ talks down the potential impact of the DTI political football on first home buyers"

"Nonetheless the Reserve Bank says banks need to prepare their systems for the potential introduction of a regulated DTI limit no later than the end of 2022"

Have shifted the goal post from early 2022 to end of 2022 - that is 18 months from the date that they got DTI tool and WILL IT NOT CREATE MORE FOMO among FHB...........

Are they helping or screwing .........With friends like that, who needs enemies

Surely banks would be starting to test at 7 or 8% now regardless of RBNZ mandates??? Surely as interest rates rise significantly they would be adjusting accordingly.

Remember this quote the next time an investor cries crocodile tears for first home buyers over the proposed introduction of DTIs:

"At a DTI cap of seven, around 1% of first-home buyers or other owner-occupiers are prevented from purchasing a similar property following the introduction of the restriction – they would either purchase the property at a lower price, and hence be financially better off, or be allocated into the speed limit. Investors are the most impacted in terms of restricting purchases of equivalent properties,"

"At a DTI cap of seven, around 1% of first-home buyers or other owner-occupiers are prevented from purchasing a similar property following the introduction of the restriction – they would either purchase the property at a lower price, and hence be financially better off, or be allocated into the speed limit. Investors are the most impacted in terms of restricting purchases of equivalent properties," the Reserve Bank says.

"At a DTI cap of six, around 5% of first-home buyers or other owner-occupiers are prevented from purchasing similar properties. By contrast, there is a material impact on restricting investor purchases."

I mean this is dumbfounding. They are getting upset at protecting people that shouldn't be leant to in the first place (i.e. a DTI of 3-4.5 is more appropriate), because it risks the financial system, so are setting the bar so high, they are putting the financial system at risk. It's like they haven't even read their mandate!

This will effect a structural change in the market with long term price upside.

Just out of curiosity. Is there any news which isn’t “price upside” in your eyes?

In other news, someone I know just got this in an email from an agent, complete with typos.

Note the advice to Be Quick, for both sellers and buyers - haha!:

The Real Estate Market was definitely changed in the past couple weeks. As the front runner, we realised the number of buyers are less now, the main reason is the bank lending amount decreased, also the interest rate is increasing. It is not a good sign for the industry, so we strongly recommend if you wanna to sale, get it quickly done, if you gonna to buy, the same!

Every family needs a home - and this Govt have pushed the rental prices up sky high via their anti- landlord policies. So where can they live, now the FHBs are the next enemy of the RB, Banks & Govt?

A LL effectively cannot remove an unruly tenant, the risk level went up several notches as a result. The fruit of the new tenancy laws is becoming more and more obvious. All good jacinda and co., it will be your legacy

RBNZ talks down the potential impact of the DTI political football on first home buyers

If their is no much impact on FHB, why the delay or is it just another fib like Transitory Inflation.

FHB'ers need saving from themselves. Speculators and tax avoiders need a kick in the nads.

Yes, blame all the market participants.

Keep the QE cash gifting Govt and ZIRP RB out of the blame game.

I hear about lots of people being turned away by banks at the moment even though they are paying more in rent than the mortgage they are applying for. Suggests to me that restrictions on affordability might be hindering access to credit.

Bring in DTI of 5 and correct things quick! Seriously, based on the foreshadowed options, I think they’ll settle on DTI of 6 - hits investors hard and barely touched FHBs. Also, when it comes to government bodies choosing a policy: the considered, thoughtful choice is usually the option in the middle of the menu.

This may be obvious but would a DTI of 6 or whatever they settle on be based on your pre tax income? Post tax income? Post tax income minus e.g. student loan repayments?

What a lot of padding trying to show folk the difficulties of something they simply don't want to do. Thankfully the market's overheating has overtaken matters and it won't now be necessary.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.