Consumer Price Index (CPI) inflation in the December quarter overshot Reserve Bank (RBNZ) and market expectations.

The quarterly inflation rate fell to 0.5% from 0.7% in the September quarter. Meanwhile the annual rate remained at 1.4%, according to Statistics New Zealand.

The RBNZ in November forecast quarterly inflation dropping to 0.2% and annual inflation sinking to 1.1%. Economists from the major banks were on a similar, if not more pessimistic, page to the RBNZ, with ANZ economists the only ones forecasting higher inflation than the RBNZ.

At 1.4%, the annual inflation rate fell within the RBNZ’s target band of 1% to 3%.

The better-than-expected reading cements economists’ forecasts the RBNZ is unlikely to cut the Official Cash Rate (OCR) into negative territory in 2021.

Nonetheless, its easing bias is expected to remain.

The RBNZ’s Large-Scale Asset Purchase Programme is yet to run its course, while banks are yet to really start drawing down cheap funding via the RBNZ's Funding for Lending Programme. Both of these schemes are aimed at lowering interest rates to boost inflation and employment.

Consumer prices index

Select chart tabs

Commentary

Digging into the details, Kiwibank economists explained: "Domestic accommodation [hotels, motels, caravan parks and camping grounds, and privately rented accommodation like Airbnb] was much stronger than anticipated. Heavy discounting during the winter months was unwound into summer - suggesting solid domestic tourist flows.

"Home construction costs rose as expected, with the rampant run in the housing market.

"Used cars were also more expensive, with a lack of supply. The supply constraints at the ports are showing up already in the numbers.

"Non-tradables, the domestically generated inflation, was much stronger than expected at 2.8%yoy (up from 2.6%). And tradables, the imported inflation (or deflation), didn’t fall as much as we expected. Tradables inflation was down -0.3%yoy (we thought -0.9%)...

"We have changed our call on the RBNZ. We now expect the OCR to be left unchanged well into 2022."

ANZ economists noted: "Pockets of strength were evident in today’s release, relative to what is usual this time of year. This reflected cost pressures due to supply disruption and potentially some payback from lockdown-induced weakness.

"We expect some short-term improvement in inflation from continued cost-push pressures, but this is expected to be temporary and the RBNZ will look through it...

"Over the medium-term, the outlook is now looking more assured, reflecting better economic momentum, even as we face challenges ahead. Although some caution is needed... a stronger starting point for inflation is no doubt a good thing for the RBNZ."

ASB economists said: "Looking ahead, we expect annual headline inflation to ease towards 1% at the start of this year but to gradually firm thereafter, with more upside risk now accumulating to the medium-term inflation outlook.

"The economy is showing more signs of life than appeared the case, capacity constraints are firming, skill shortages are permeating throughout the economy and this could see pricing pressures stir. We also expect a modest positive, but temporary, impact from freight disruptions on retail prices.

"Nevertheless, the RBNZ is expected to maintain highly stimulatory settings until it is confident that economic activity and the labour market have turned the corner.

"Our view is that the OCR is unlikely to move up in 2021, but the resilient tone of NZ data is a reminder that the OCR won’t stay at record lows forever."

140 Comments

So basically, interest rates were lowered and future home owners screwed over and the future economy crippled by increased housing costs, and this was all for nothing.

Well, it was for something: it was done to keep the NZ housing Ponzi running.

The cuts were to maintain CPI within 1-3% band. 1.4% is still below target of 2%. Job well done Mr Orr.

I hope HeavyG you are keeping your rental increases between 1 - 3% pa .......if you are Job well done Mr G :)

Otherwise it's the taxpayer that's paying for it !

No beneficiaries in my rentals. It's a rule I have.

Careful - you could run foul of Bill of Rights if you discriminate based on employment status.

Credit ratings are all good, that's why beneficiaries can't pull out the bill of rights when the Mercedes dealership won't sell them a new car on credit.

Doubt it. Anyone over 65 or getting wff? They are beneficiaries.

Food, medical bills, housing and other non-tradables have clocked at the higher end of RBNZ's range (2.5-3.5%) for several quarters in a row.

We should be thankful for cheaper discretionary items such as TVs, phones and clothing that are offsetting the costs of the above mentioned must-haves.

It seems to me that those essential things should be weighted more heavily, and the discretionary items less

Wait until you start throwing in the effect of not adjusting taxes for the wage inflation that has already happened; the inflation accounts for the increases in living costs, but it also hides a problem of the amount of money people have available to put towards them. Perhaps someone with a better understanding of the CPI or economics could tell me whether this is adjusted for or not?

It’s the consumption of those that pushes the price of the others upward. (And property)

Housing story is simply a divergence in the types of CPI.

To QUOTE from today's Mike's Minute [God save my soul]:

"Then ask yourself the simplest of questions, what does “fix” mean? When is it fixed? Answer, there is no answer.

The same way there isn't a crisis, unless you want there to be one.

The same way a 10 percent drop in value might be a crash, or a correction, or an adjustment depending on who you are, and what your agenda is."

I don't usually read Mikes rants but he was spot on today.

Good heavens. When people gravitate to ignorance like this, what hope does NZ have? Would love to see the Hosk go up against Robert Shiller. The arrogance of the former would be embarrassing. But many NZers would side with the Hosk.

@J.C. .......always remember seeing "the Hosk" standing at the baggage carousel around midnight, at Dulles Airport (Washington DC) with his wife Kate in 2016 ....he looked like a "fish out of water" while Kate was confidently looking out for the bags . The Americans would eat him alive ......he used to really piss me off with his arrogance, now I just ignore him ...better for your health.

It seem to be a real issue in NZ where successful broadcasters become experts on almost everything. But if you listen carefully to what they're saying, you understand that's little more than a steady patter of twaddle. They really tap into the NZ psyche where people look up to the most opinionated around the water cooler without actually constructive thinking or debate.

That's our own fault for being a bunch of lemmings.

You forgot about retirees having to pull their TD's.

My mate has. few houses in Hastings, low decile. he has put his rent up from $270 to to $500 in the last two years, houses he paid 80-120k for in the early 2000's are now worth 460k +. He tells me every time he puts the rent up he hets a ring from welfare to confirm rent has gone up and the accomodation supplement is increased for his tenants.

The accomodation supplement is being used by landlords to put rents up above and beyond what people can afford on the wages they earn.

I talked to some other farmers this week and someone else bought up the 2000 Islanders in quarantine waiting to start on orchards. Wages on orchards and remember this is highly seasonal, are being rorted by large corporate orchards who account for %80 of the apples in Hawkes bay.

We have a massive poverty problem with poor people subjected to more violence, sexual abuse, poor home life, lack of education opportunities, no fathers, it's directly related to poverty and lack of jobs.

These orchards have now geared up and being built around the RSE scheme, these large orchards don't want a local near them. One in CHB intends to employ nearly 200 RSE workers. How did no one see this coming? We need local workers in well paid jobs, especially those short term seasonal ones.

The meat industry is seasonal and yet pays only a little above min wage, then it complains it cannot get workers.

Helon Clark started with Working for Famillies tax credits..... once a low wage earner pays no tax and still cannot afford the rent, they get an accommodation grant..... this is theft with only the private landlord winning

If we didn't have such rampant housing unaffordability, poverty would be greatly reduced. Deterring speculation in property in addition to public house building would help immensely. Your mate sounds like a top bloke putting up the rent nearly 100% in two years.

As a renter who does not qualify for one I find the supplement particularly detestable policy. I have to pay taxes to subsides others, I have to pay more rent to compete with this subsidy and as it helps landlord's pay even larger mortgages making the house price higher. Unfortunately it's to much of a shock politically to ever remove it.

It might help some families better compete with DINKs for decent rentals but looking at the news I am sceptical.

Its a discouragement to savers. $8,100 in assets and the renter (saving for a home etc) can't get asup.

Yet someone with a all their assets tied up in a home can. The craziest thing one could dream up. I recall Michael Cullen did this in preference to tax cuts.

Where are the brain dead msm on this? Too busy focusing on tweets from celebs.

It's a disastrous policy that has probably taken more wealth from the wage earner than any other over the last two decades. Anyone who does not qualify loses 150 to 200 a week for nothing. Home owners are also paying more to service their mortgages because they had to bid against investors. A small amount on the asup are better off as they can outbid a wage earner without it and get the rental instead. All the money ends up enriching those who are already wealthy. It may (Cullen is not stupid) have created with the best intentions, as tax cuts on min wage workers only have so much to give back.

But as Jacinda has informed us as it's a house price positive policy its expected the government does not make any attempts to correct it.

The only way to address a wind-back of our outgoings on the accommodation supplement, is to introduce rent controls alongside the building of more state houses (as they are rent controlled based on rent of 25% of household income already).

I agree that would work to help limit the homelessness. It would still put the property market at massive risk of collapse (due to negative investor sentiment and some returns), think banks failing and FHB negative equity. It would take some serious leadership and competence to successfully remove the supplement.

To me the housing crisis is due lack of government will to fix it (partially due to MPs and their peers having significant housing investments and partially due to short term economic shock effecting their next election chances) rather than any real systemic problems.

Rent controls would have no effect whatsoever on FHBs - unless you are implying a run on the housing market (i.e., mass investor sell up). I've modeled it based on a specific formula of control and the results suggest that the only rents that are way out-of-line in terms of affordability are those for the lower quartile (as per the tenancy.govt.nz) rentals.

So what might happen, is that, a lot of lower quartile dwellings - i.e., those typically purchased by FHBs or downsizers - would come on the market. No big panic as these houses for purchase by owner-occupiers are in high demand. So called 'under water' FHBs only encounter trouble if they want/need to sell. The Helen Clark Foundation has recently discussed a remedy for that.

What formulae? I don't believe the housing market is model-able to that (can be modelled by mathematical function) extent, it's way too sentiment driven.

If you take a look the current market (say Tauranga) $400 a week gets you a poor quality family home, 500 gets you a decent place and 600 is a really nice place to live. I believe this is due to the accommodation supplement setting a min rent.

I am suggesting that almost all rents will decrease by at least $100 a week and most by at least $150 if the accommodation supplement is removed. This would be a 30 percent gross yield decrease for landlord collectivity. After expenses i would except a lot to be struggling to justify owning a house.

Most renters will only be willing to pay $100 to get that step up rental quality and if the poor quality houses are now cost $250 the current renters of $500 properties will compete with them unless their rate drops to $350. Just to throw some arbitrary numbers at this. There is no way rent control and removal of accommodation supplement will not spread though all but the very upper end of the market.

I'll have a look at Tauranga next. I was wanting to do two different locations in my modeling - so far I've done Hutt Valley (both Lower and Upper Hutt).

The weekly rent maxima formula that I am testing is [(RV/1000) +/- x%] with 'x' being set based on how unaffordable (or not) the local market is, such that when 'x' is applied the lower quartile rents align to affordability at no more than 30% of household income for the area/region.

For the Hutt Valley it presently looks like 'x' would be zero - in other words, RV/1000 looks about right. Based on that formula, the average weekly rent decrease on the asking prices for all properties listed since 21/12/20 equates to $98.00/week.

Here's some made up numbers that I think are reasonable: I can afford my rent (as I have no dependants) but I would quite like it to be cheaper. I think I am paying a $100 premium to rent the better home and I consider it worthwhile but I would not pay a $250 premium.

Have a look at the upper quartile of the Hutt Valley rentals. I would assume they have a gross yield less than lower quartile, thus your formula works.

If the entry level houses decrease by $150 I would be applying for those rentals as I could have $250 extra a week to spend. My current landlord would have to drop his price by 150 to have me stay.

You can't drop the lower end of the rental market without effecting the rest of it. The supplement has distorted the market. This is an issue with rent control, far more people than can only afford the rent controlled properties will be wanting to only pay that rate.

far more people than can only afford the rent controlled properties will be wanting to only pay that rate.

All properties would be subject to rent control based on the formula - in other words, the formula would be applied universally. What I've found so far is that it is the lower quartile properties that are charging a higher than the weekly maxima based on the formula - yet the higher quartile properties are charging less than the weekly maxima based on the same formula.

I assume the reason for that is that those that can afford the higher end/higher rents are not recipients of the accommodation supplement - and therefore rents are listed at prices based on what that household/market can pay.

You know the expression 'slum lord' - it exists because the poorer in society have fewer choices and hence will pay a higher proportion of their limited income than those on higher incomes will pay.

Your missing my point, I think. Are you intending people not currently receiving the accommodation supplement to be disallowed from applying to rent rent controlled properties?

The lower income tenants will not automatically get these rent controlled properties, they will have competition from tenants who can save significantly more than they use to by moving to the cheaper housing. The market will adjust from the bottom up.

I don't know how to explain this better.

Are you intending people not currently receiving the accommodation supplement to be disallowed from applying to rent rent controlled properties?

No. All properties are rent controlled and all people can apply to rent any property they like just like now. The upper quartile properties, such as this one:

https://homes.co.nz/address/upper-hutt/brown-owl/10-diamond-grove/QYGXE

Which just rented on 12/1/21 for $600/week was already asking below my proposed weekly rent maxima. And that looks to be the case for all the upper quartile properties (i.e., recent, modern, well located properties) - they are all renting at or below what would become the rent maxima.

Sure the person who rented that at $600/week could always choose to rent this one instead;

https://homes.co.nz/address/upper-hutt/ebdentown/5a-clouston-park-road/…

For $440/week based on my proposed rent maxima.

The current asking rent difference between those two places is $40/week - one is a new build - one is a property built in the 1970s. One is on its own section - the other is a townhouse which shares a section with two other dwellings. Can you see how the lower quartile rentals are currently over-priced?

I think any formula would also have to look at the population in the region and also the number of rentals available, not to mention what you can earn locally. I now live in Tauranga and can tell you the pay is poor and the number of available rentals are low, the two are no doubt linked. In terms of housing affordability to income, Tauranga would be a shocker. How does it survive ? loads of wealthy Aucklanders coming down here to retire with money left over to put a new Ford Mustang in the garage.

It survives on the Accommodation Supplement and Working for Families. And yes, the formula would be set locally in much the same way tenancy.govt.nz derives its estimates.

You know what happens when you introduce rent controls; it no longer becomes profitable to build and people start burning down existing properties. People also become statehouse lifers, though, we already have the latter.

You know what would lower rents, cut working-for-families, cut the accommodation supplement, stop statehouse-lifer-policies. This would need to be coupled with a year amnesty for fixed tenancies, that is to say allowing tenants to give 3 weeks notice due to the aforementioned welfare changes.

it no longer becomes profitable to build and people start burning down existing properties.

Why do people burn down existing properties?

Historically [other countries] rent controls are coupled with increased renter's rights.

Due to rent controls making building unprofitable; governments and municipalities soon make new builds exempt from 'rent controls', therefore landlords burn down their old building, collect the insurance and build 'rent-control-free' buildings.

The inability to evict unprofitable tenants coupled with expensive legal requirements has seen the burning of properties too - It happens.

Under a policy that applies universality (all rental properties are subject to rent controls) that problem (i.e., cause and effect) you mention does not happen.

Universality is key and would apply to new builds (that are purchased to let) as well.

Yes, I've been calculating rental yield for all the newly listed properties in the Hutt Valley. I've calculated those yields based on purchase price. Shocking really the yields being made on so many of the rental properties - 30-50% yields are not uncommon. But it is likely that many of those investors purchased additional properties based on the unearned capital gains on existing holdings - and so yes, they then 'claim' lower yields based on net present values.

It's a scam/ponzi of epic proportions in NZ - and it's being funded by taxpayers via increased accommodation supplement and increased social housing costs.

30-50% yields are not uncommon

Surely I am not the only person here thinking that perhaps you are miscalculating yield, Kate?

Yeah, is it meant to read 3% to 5%?

It *could* be true on some properties bought say 20-30 years ago

Yes, particulary multi-story flats built circa 1970.

Here's an example with a 37% yield;

https://homes.co.nz/address/lower-hutt/boulcott/9-37-mills-street/09rNn

I use this calculator;

https://www.propertyvalue.co.nz/buying-and-selling-advice/tools/rental-…

Okay. You sure you have been using it correctly?

Yes, I think so. I get the rates off the council websites - for a multistory flat I divide the rates by the number of units in the complex.

In the example above I assumed $500 for insurance (again guessed overall insurance for the complex and divided by the number of units) and $500 for maintenance - and a 50 week occupancy.

For standalones and townhouses, I use $1000 for insurance and maintenance.

Yields of course decrease based on year of purchase - the older the purchase, the higher the yield.

What property value did you use?

Okay. Let me rephrase this again - Do you know the difference between yield and return?

Yield is calculated on the current period value. Not the current period and some arbitrary previous period.

LOL - well, yes I know that. And of course it's a convenient/orthodox accounting crock. A example of the mess we've got ourselves in based on the FIRE economy.

That needs unwinding.

Audaxes put up some info, %60 of bank lending is to a small cohort of people owning multiple houses, that because banks lend against equity and as prices go up the more houses you have the more equity = the more you can borrow, same in farming.

Exactly. And the longer we stay on this FIRE-designed hamster wheel the worse it gets.

I'm starting to think that only real, structual change, is the way forward. Complete rewrite of how the RBNZ is managed etc. Anyone with half a brain can see the current course is a broken model and the money printer does not work.

But We can't even (politically) introduce minor changes. See current govt who campaigned originally on fixing the issue but have done nothing but make it worse.

We need a big course correct.

Here's a good example - a house we purchased back in 1983 for $78,250.

https://homes.co.nz/address/paraparaumu/paraparaumu-beach/8-ngapotiki-s…

Would rent now for $673 based on tenancy.govt.nz - but add my (average) 12% increase for recent rentals onto that and you get a weekly rent of $765.

Rental yield based on my purchase price would be 44% for a 12 month fixed term contract.

Using the current property value, recently sold $765,000. Yield would be 5% +/-

No, I don't need to use that value - because, if I still owned the home, I didn't pay that value. My accountant for sure would use that value - LOL. If I wanted to be in such a business, that is.

You do, because you don't own the house any more LOL.

Yes, hamster.

Why don't you look for a house built in the 60s, then you can claim a yield of 70, 75%....against purchase price.

Why didn't I think of that?

Kate's into something here... teleport yourself back in time 30 years.

Only thing with her scenario is.... what about inflation on all the other costs associated with housing.

I know, I'll try asking my plumber if I can pay him based on 1983 prices since I bought a house in 1983.

You are using the cost to the owner rather than the value of the property. Yield is calculated on value not cost. e.g. if owner paid $100k for a property worth $1m and renting for $30k a year the yield is 3% (30k/$1m) not 30% ($30k/$100k). If an investment opportunity came along offering 10% return the owner would be incorrect in saying no thanks, I am making 30% currently (they are in fact only making 3%).

LOL - you FIRE addicts are all really 'stuck' on the same record.

If owners were unable to remortgage and borrow based on unrealised capital gains based on their new valuations - all that would matter is the cost to the owner.

Just try to imagine a world without leverage and you'll get my point.

Why would that matter? If you bought a house 30 years ago for $60k and you now rent it for $60k pa YOUR "yield" calculation would be 100%. What's the point of that calculation?

Your probably right Kate.we've bought two blocks of units.one seven years ago and the other four years ago and are yielding 11 and 12 percent on them.if you increased the rent by ten dollars on each unit that works out at $160 increase.hard to increase $160 on a single dwelling like you can with units.

That's a confused post AndrewJ

Firstly it doesn't relate to the article, then you talk about a mate, rents, then Orchards, someone "buying" overseas workers...

inflation is hurting low wage earners and the government is a big part of the problem.

I'm with Andrew on this, there is something deeply unpleasant about the ability to source seasonal workers. There would be no labour shortage if the market was allowed to clear, almost certainly at a living wage for locals. Are the apple growers on their knees? I doubt it very much.

Demonising the unemployed/Maori for not working in these low-paying back-breaking jobs is a right-wing trope. I really hate this about NZ.

Benefit abatements are largely to blame. Those on Nat Super can pick fruit and keep it all (les some tax). The beneficiary looses 60%+ of earnings.

They are not all lazy...it's just not worth the effort to go off and do this work.

Deserves more than just a single up tick.

And this government could scrap the abatements for job seekers who take on non-permanent/casual work tomorrow. There would be heaps of people taking up the work.

Abatements and stand down periods too. You work seasonal work then when the job ends you can't claim the benefit for how long? 10 week or until all of your savings are depleted? Totally messed up.

All the incentives are a mess. What Kiwi could survive on these wages for short periods of time, moving around, living in poor accom. Maybe the Govt should just subsidise the wages up to a living wage?

Yes to all the above. Talkback types really don't think about the practicalities of taking on a job that involves moving into the countryside away from home and family, working on different sites, for a short season, for a paltry wage, and knowing that you'll likely end up financially worse off because of abatements.

UBI. Problems solved (and many others)

The Govt subsidize their wages? Why not expect employers to pay the costs of running their businesses without relying on foreign slave labour?

Teachers, police, nurses care workers could all say the same -- not worth it for the abuse etc -- but they do -- nobody should have the right to CHOSE to not work when there is work available - and then be supported by the taxes of others --

I agree totally about the crazy tax and abatement systems -- and would change them in a heartbeat to encourage people back to work -- but even if it did -- these same workshy people would not be rushing out to work in any industry

How many teachers, nurses or cops would we have if they were paid minimum wage, moved from site to site every few weeks, and only offered those jobs for a few months a year?

OK. If the only work available was in a (legal) brothel, do you think you should have to take that job rather than get the benefit?

People, it may be hard to have our cake and eat it too...

See, if you want cheap goods/fuel/capital you engage in global trade. Its a two way sword, you cannot source the benefits of trade without having the purchasing power from production of goods/services your trading partners demand. We have competitors, some with advantages over us.

I think it's pretty relevant. The article is about inflation and he has addressed rental inflation among other things.

His posts cover a lot of ground, also the weather farming tales... it all relates, somehow. I like the stories but you just have to go with it brother.

"The accommodation supplement is being used by landlords to put rents up above and beyond what people can afford on the wages they earn".

Correct, and it is high time to stop wasting public money on this landlords' welfare.

People need to learn that once you start a supplement, you cannot simply pull it. In fact that supplement only ever starts to go up instead of down. Should never have been started in the first place, now its too late. Everyone in the "Chain" starts to rely on it instead of trying to wean themselves off of it. Landlords simply cranked up the rent and it was of no help to those it was targeted at.

My understanding is the RSE workers often have their incomes clawed back through various dodgy means. (One example: Four bunks in a room and paying $200pw each. And you have to live there)

I guess there are some brown paperbags of cash passed around as well.

Thats what I hear to, fly them in charge full fare, mini bus to work charged, rent max, food max, $100 a week allowance for pocket money, i talked to a Samoan guy and after 8 months he got to take 10k home, which he got when he finished for the season, he said at home he's lucky to get $2 a hr.

Local told me that she couldn't keep up with the Islanders, who were basically getting min wages. Gave up and got another easier job at min wage.

Andrew... you do know that if a Samoan takes 10K home after a seasons work that he could live for the next 2 or 3 years without lifting finger.

thats what he told me, but a kiwi family only has a few months.

Yep, I have been raging about the bats*$t crazy accommodation supplement (landlord welfare) as well as WFF (productivity killer) ever since they were introduced.

If you own one or multiple houses in this country (i.e. have high equity), you can literally buy a new house and have the taxpayer pay it off for you via the accommodation supplement. And I am certain there are people that are doing that, because I have talked to some of them. They do exactly as Andrew's mate has done - put the rent up to on their rental property to whatever amount they want, because they know their tenants are on the AS and that will be increased by the same amount. And why wouldn't you?

WFF has caused massive productivity woes for this country at the same time, causing ever increasing amounts of AS to be paid out. The gubbmints ridiculous solution? Put up the min wage! Way past time all of this was thrown out. Please note: abolishing all this bull and replacing it with a UBI would be more cost effective, destroy landlord welfare AND encourage unemployed people to work.

That’s not the way the accomodation supplement works pal. The maximum anyone can ever get is $350 and you’d have to be in area 1 for that.

https://www.studylink.govt.nz/products/a-z-products/accommodation-suppl…

The 1 - 3% range is not fit for purpose. Can you imagine the kind of house pricing surge that would need to trigger 2.5% inflation if this we only got 1.4% off the back of the December Quarter? How is this still a relevant or acceptable band of operations? At what point would it start to ring alarm bells?

We are heading towards our second winter with closed borders. This time people may find they have far less money to spend in tourist towns with no overseas tourists. This could start to unravel very quickly if we keep trying to use a playbook from the early 2000s.

Because house prices aren't included in CPI, rents are...........

House price's are included. It is land that is kept out.

Some housing costs. It has been rejigged to capture more in the last couple of years, but it's only weighting them as small parts of spending.

Yes, housing costs (including rates and utilities) have been rejigged to equate to 27% of the 'basket' of goods that we all purchase.

They are living in some other world, for sure.

The average rent in Auckland is surely over $600 by now. What does that make the average after-tax income available to buy the basket of goods each week if even just the rent alone is only allocated 27% of the basket?

Name an Auckland suburb and I can answer that question for you. You'll soon understand why the foodbanks are experiencing a never before seen increase in demand. Saw one article that quoted weekly rent costing between 50-80% of the typical foodbank-users after-tax household income.

all because the RBNZ keeps pulling on a lever that is causing a lot of pain for lower income earners, meanwhile enriching asset owners especially the top quartile and those with multiple rentals.

And the government stands by doing nothing of any serious consequence.

All NZers need to realise that we can't state welfare our way out of this housing crisis. In fact one article from a welfare service provider called it housing chaos - given it's gone beyond a crisis.

https://www.rnz.co.nz/news/national/427292/housing-crisis-now-housing-c…

Why is the government subsidising landlords? when clearly the rent is beyod the tenants means

It's just perpetuating and incentivisting a vicious cycle of ever increasing rents and house prices

Landlords welfare must be discontinued immediately. The same must apply to the favourable tax treatment of parasitic housing speculation, to the unbalanced risk weighting of residential housing on banks' books, and to the excessively loose monetary policy.

@ Uh Oh TOTALLY ! .......and it's because the Government does NOT want to see ANY change of the current status quo ....end of story.

Not just the Government but the land and home owners - lots of frowns and head nods but behind closed doors lots of smiles and bubbles.

You got it. And (in my observation) no one in the MSM or in government want to address rent controls.

You have to take into account that fiscal policy has been very loose. Government may decide to return to a balanced budget sooner than previously forecast.

Globally the rate of progress on vaccine deployment is far ahead of any schedule we could have dreamed up even six months ago thanks to the scale of resources spent on rapid development and testing. That likely substantially changes New Zealands economic outlook as long as we can deploy vaccine rapidly and normalise local industry. Incidentally the Johnson&Johnson vaccine New Zealand has ordered is expected to go for approval in the next few weeks and be make available from next month in the UK.

The property party continues! Who would have thought it; certainly not Mike Kirk and his band of DGMs!

I agree B727 but to be fair I predicted it HAD TO END with Covid-19, I mean if that didn't kill it, nothing would and yet here we are. So the big question is when will it end ? Taking a step back but looking forward I see no end to it now, just the usual house price doubling in 10 years time. Sounds impossible doesn't it, but its not. you just end up with even less home owners and more renters. Wages are not keeping up, but it doesn't matter because the top 10% of New Zealanders could end up owing 80% of the houses. I now see the new Zealand housing market as unstoppable and it with take some sort of catastrophic world event to stop it and you had better be careful what you wish for because it would be bad for everyone.

Interesting.

If wages don't rise much then by that logic a property worth $1 million now will be worth $2 million in 10 years. Say the rent pw is 500 pw now, that's a gross yield of 5%. To maintain that gross yield at $2 million the rent needs to be $1000. Yet net income for an average family may only rise (say) $300, and the costs of other goods and services will increase.

So yields will have to drop further. That then means investors will be buying not for yield, but for capital gain. In which case they are speculators not investors.

Or, that $300 wage increase will be entirely captured by landlords, and renters will be forced to make cut backs to let them compete for an insufficient number of rentals (and houses in general). Maybe sprinkle in either an expansion or increase to the accommodation supplement from a government (of whatever colour) that has to be seen to be doing something.

NZ's combination of comparatively weak protections for tenants and ongoing housing shortage means landlords can and almost certainly will continue to squeeze every cent they can get from tenants (and, indirectly, from taxpayers).

The flow on effects of all this are going to be nasty - lower consumer spending and increased inequality will hurt businesses and reduce growth, and any increase in government spending (for rent subsidies) will need to be paid by someone...

Good points.

And as you say, this will not only have inequality impacts but also consumer impacts if a growing segment of the population (renters) have less and less discretionary income.

Simple math.

Not sure why people don't think the house price doubling will not continue, I mean it has continued right up until yesterday so why will it not continue ? Ok so it may not be 10 years, it may be 12 years but the trend has been unstoppable, you can bet your house on it.

Carlos67.... I have been bullish on NZ property for many years and as a direct beneficiary of the good times am well aware of the past returns. However, there are many reasons I feel the capital gains will not continue in anything like the way they have in the past and huge, long term losses are a distinct possibility. You are right, the trend has been unstoppable but current indicators are much more important than the past. As Taleb said you can look at your life and say I have never died so therefore I will live forever. Or Taleb again, only a fool thinks a 5000M mountain does not exist simply because he has never seen one.

In the short history that is NZ property we have never seen total calamity (and that clouds our perception of the future) but odds are one day we will.

A good number of the best risk analysts in the country are concerned. I have a good knowledge (and long personal investment history) in NZ property, can assess risk as well as (almost) anyone, could buy a handful of rentals tomorrow (with no mortgage) but am choosing not to. I may be making a mistake but it may be wise to consider why I am taking this position. Time will tell (and I really hope I am wrong).

Weak protectors for tenants... that all changes 11 Feb.

Housing crisis 2.0 about to hit. Ain't seen nothing yet.

Please visit your archive and its see when you had any balls to do any forecasting and compare it to what all economists and gov was believing and saying in last 16 months.

Carping

.....and what happens when the CPI (inflation) goes up ......interest rates go up .....there goes the property investors wet dream of the bank having to pay them to borrow money .....and their other favorite "interest rates will NEVER increase and be low FOREVER"

It's time the taxpayer stood up and knocked the accommodation supplement on the head ! ...after hearing Andrewj mates story from Hastings, it just sickens me !

While all the PI's out there are saying FHB's don't save hard enough for a deposit ......while at the same time quietly increasing their rents ...I wouldn't give a $#%$@ !!! if this wasn't taxpayers money, as "real market forces" would kick in and they couldn't charge those rental increases.....let alone the current rents !

Time for action !

I find it curious that they haven't caveated for more covid lockdowns.

In my opinion there is at least a 50% chance of more lockdowns this year.

Don't worry Fritz ..... your average property investor probably likes "lockdowns" ...as they know the Government will cough up somehow and in some way, as even they don't want a downturn of any sort to the PPP !

But lockdowns would be deflationary.

You're right, chances of at least a level 2 lockdown in one major city this year should be at least 50%. And that risk is front-loaded to the first half of this year also, given vaccines both locally and globally and likely reduction in inward migration as the year progresses due to the same.

For Fed read RBNZ Funding for Lending Programme (FLP)

Question: What sort of projects do the Fed encourage with negative real (after-inflation) interest rates, that can’t even jump the hurdle of a zero real interest rate?

Answer: Only projects with negative real rates of return – primarily those that destroy capital and harm economic productivity. If these marginal projects aren’t worth doing unless the real interest rate is negative, then by definition, they are incapable of producing the same amount of real goods and services that is required to initiate them.

The monetary dogma of the Federal Reserve seems to view the U.S. economy as one big demand curve that always benefits from low nominal interest rates, and negative real interest rates. It is exactly the dogma that produces repeated economic cycles driven first by yield-seeking speculative bubbles, and then by financial crises that count on the bailout of private losses with public funds.

Before these bankruptcies and defaults emerge, understand this: bankruptcies are mainly packaged restructurings, and bank failures are mainly purchase-and-assumption transactions. What amplified the Depression was not bankruptcy and bank failure itself, but disorganized and piecemeal bankruptcy and bank failure. The public shouldn’t support bailouts. We should instead support quick restructurings that preserve corporate assets, jobs, and business activity, but also appropriately wipe out the equity and debt of companies that have been managed irresponsibly. That’s how risk-taking works. Why use public money to absorb losses that private investors willingly agreed to take the moment they bought corporate securities? Link

Much more likely up, if the CPI embedded those figure portion to service another 20% increase RE costing that must be repaid eventually.

"Expected to be temporary and RBNZ will look through it" (ignore)

Here we go, caught on hop by bloody obviously coming increase in trade and transport costs.

Trading nation has unexpected increase in trade costs. Joke

No interest rate cuts then: = end of Ponzi. No road left to goose consumption and house purchasing, meanwhile primary and export sectors have to face increase costs.

Hence, mid February, as forecast (YES by me!) economy shifts to downwards.

Dollar way too high also, despite RBNZ deluded boost to banks from FLP.

Neither RB nor govt appears to have first clue as to what causes inflation

2008-19, CB around world failed miserably to produce over 2.5% inflation.

That was because QE did not get to consumers.

In mid 2020, NZ covet and RB threw kitchen sink at supposed and forecast deflation forces.

So, we had huge extra govt spending (and pipeline ) plus huge monetary stimulus.

And yet we had RB and Mr Robertson still seeing deflation.

Printing is pulling forward future consumption.

Debt in private sector is same.

Earnings to justify this and protect currency from exports will be hit by costs of freight and declining demand from markets other than China and Australia.

NZ economy is on cusp of significant downturn which no economists can state.

I think it's a crock that the new housing component of the CPI excludes land value, when increases in land value have been the main factor behind house price inflation.

Does anyone have any views.

It would be good to see an article on this.

The prevailing argument will be that land prices are not the price of something consumed because they contain the value of current housing consumption but also the capitalized value of future housing consumption. Consequently rent is seen as a purer measure.

I've often wondered how accurate the CPI basket is overall. Like if you believe CPI "Local authority rated and payments" are actually almost 10% lower than three years ago? Similarly their data on rents indicates rents have only risen 10% in three years? CPI has always been only a very narrow window on our economy and it's an opaque one as well.

Yes that's the reason I have heard. Do you agree with it?

Surely it's a crock. People buy a house which comes with land. So you consume both.

I don't get it. In the abstract it kind of makes sense but it's also nonsensical.

It's easy to be cynical about the basis for it too.

Inflation would be significantly higher if land was included.

I understand NZ does it this way because it is an internationally accepted approach.

Again I think it merits an article.

It means state benefits tied to inflation don't cost too much.

The problem isn't really CPI itself, it's that we use it although it where a measure of inflation across our economy. It would be like trying to judge when you car needs servicing by only looking at the engine temperature gauge and ignoring every other instrument available.

“When a measure becomes a target, it ceases to be a good measure.” - Goodhart's law. :-)

But it is the problem isn't it?

If land value is counted then inflation would be higher, meaning less pressure to cut the OCR and stimulate the housing market.

Yay inflation! That means we are all getting paid more too, right??? Oh...

The year end blip looks more like a pent up demand from all that cumulative lock down and restrictions. There's a likelihood of a dot-com styled bust in the stock market that will force RBNZ it's hand. If the current blip is anything, it actually helped RBNZ achieved it's inflation target. Looking forward, maintaining the 2.5% will be tough. I see RBNZ cutting it's interest rates when global consumption erode further till at least the end of 2021 with it's recovery taking years. The probabilities of further cuts on interests rates are high and raising it are almost none according to what I see.

Not so fast PMI down 13% MOM, people leaving more than coming.Wealth being exported, poverty imported. Funny how this never makes the headlines. Housing prices UP UP UP.....

1,800 more have left in the last 30 days. (going on provisional data on stats page)

student visa's down, less working visas.

At least there is Bitcoin

For stocks, substitute word housing and then read

https://wolfstreet.com/2021/01/21/time-to-worry-about-stock-market-leve…

Size of debt locked in, interest rates not.

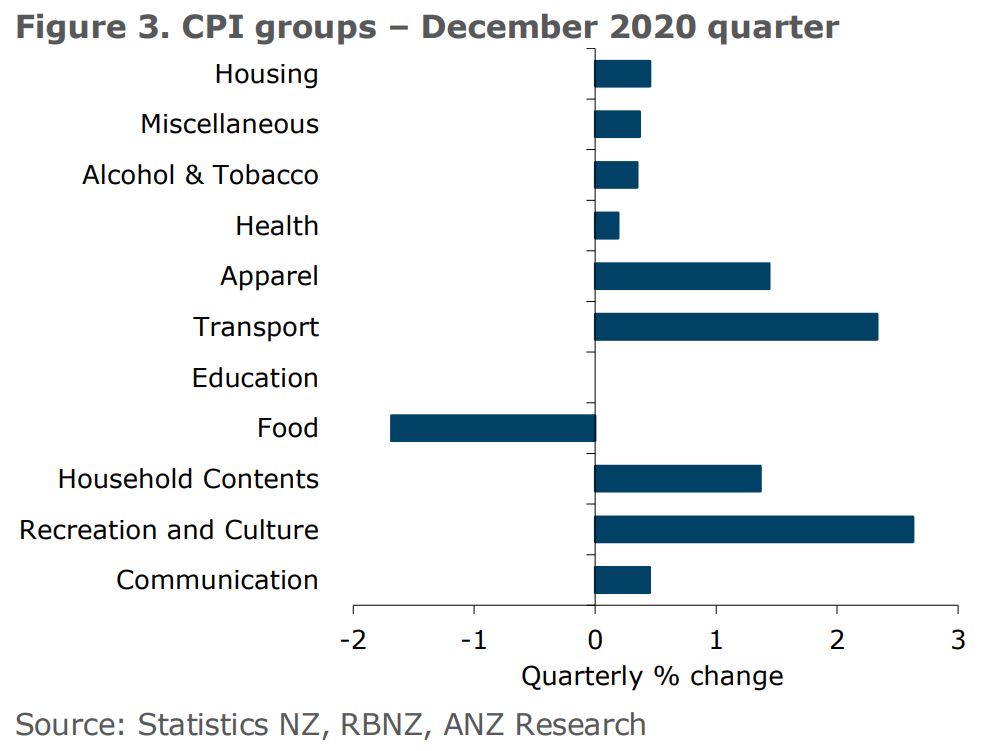

How are food prices negative when they have been going through the roof lately?

Yes, I was genuinely surprised by that too.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.