Economists at the country's biggest mortgage lender are saying it makes sense for borrowers to "think about how exposed they are" and to consider fixing "at least a portion" of their mortgages for longer terms.

In a new ANZ Research NZ Insight publication ANZ senior strategist David Croy says it would be prudent for households and businesses "to plan ahead for the possibility that higher borrowing costs are on the cards".

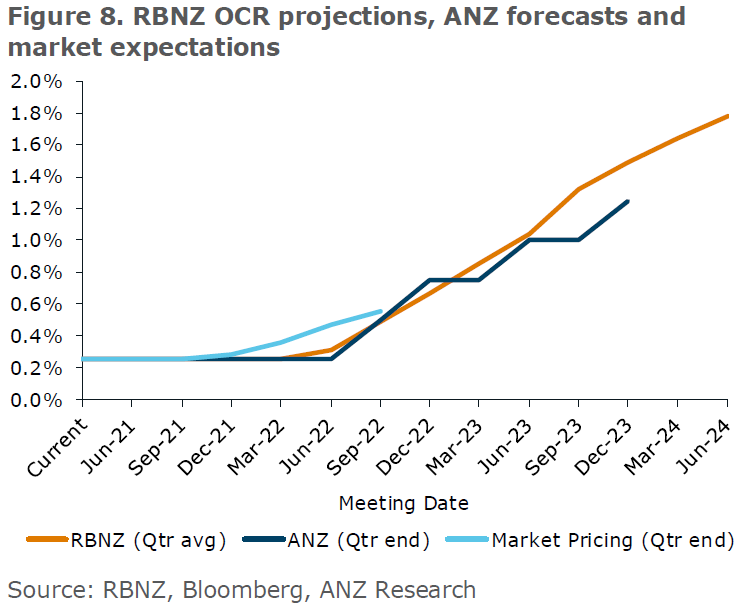

The new publication from the ANZ economists comes in the wake of the Reserve Bank's recent decision to reintroduce Official Cash Rate projections in its Monetary Policy Statement. The projections (which the RBNZ stresses are very conditional) imply a first OCR rise in the second half of next year followed by a series of hikes, taking the OCR up from its current 0.25% to 1.75% by the middle of 2024.

The RBNZ made those projections despite its belief that the current inflationary pressures that are being seen (and emphasised again by the latest ANZ Business Outlook Survey), will prove to be temporary.

ANZ's Croy notes that high inflation is "around the corner".

"We are forecasting headline inflation to peak at 3.0% in Q3 2021. This largely reflects persistent (not permanent) factors, including Covid-induced shipping disruptions, which are feeding through into higher costs and prices in New Zealand, as well as a tighter labour market. For good measure, there is some transitory stuff in there too, with base effects as weak inflation in 2020 drops out of the annual calculation, and a large minimum wage rise in Q2 all helping the headline number reach 3%."

'Crucial for borrowers'

Croy says exactly how transitory or persistent (or even permanent) the lift in inflation proves to be remains to be seen, and there are plenty of mixed views out there.

"And it matters crucially for borrowers given that the RBNZ’s other objective is to get inflation sustainably to 2%. And things are going well (almost too well) on this front. Indeed, it’s looking like inflation is at more risk of overshooting than undershooting at this point. While we are yet to see actual CPI outturns above 2%, the survey data suggests this is just around the corner."

Given the strong inflation and employment backdrop therefore, Croy sees the risks as skewed towards higher interest rates.

"But there are reasons to think that this cycle won’t be like the boom-bust cycles of old, where interest rates fell a long way, which then stoked a recovery, which the RBNZ then leaned against with higher rates, with the goal of engineering a soft landing at 2% inflation (and now full-employment). That didn’t always go smoothly - if we take the 2004-2008 cycle as an example, back then, the RBNZ had to take the OCR from 5% to 8.25% before the economy slowed (and when it did, the [Global Financial Crisis] saw it collapse – which, we should add had nothing to do with the RBNZ).

'Sensitivity to interest rates a lot higher now'

"This time around, the starting point for the OCR is lower (0.25%). On the face of it, that suggests the OCR could go a lot higher before it gets back to more ‘normal’ levels (it was at 1% pre-Covid). That makes logical sense, but given the growth in household debt since then, the economy’s sensitivity to interest rates is a lot higher too. The household debt to income ratio has risen significantly over recent years. In simple terms, more debt means more sensitivity to a change in interest rates. That will likely mean the RBNZ has to hike by less to cool spending."

Croy says households also have less time-certainty with regard to how long they have locked in fixed mortgage rates for.

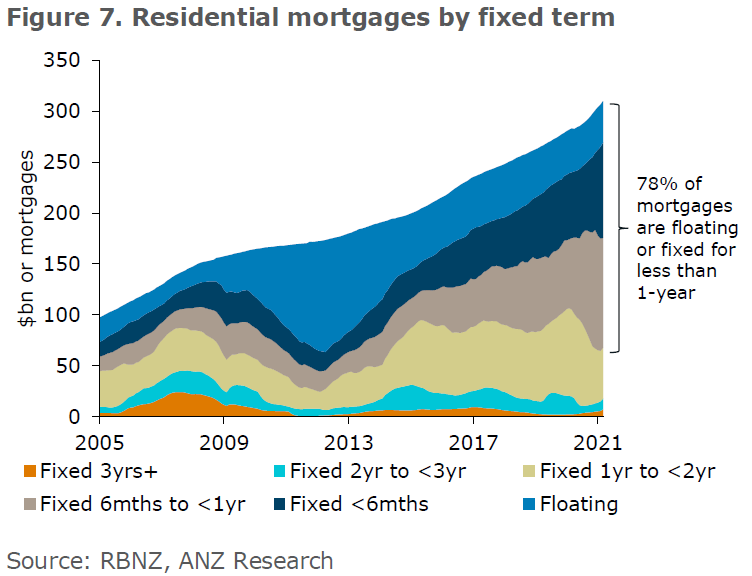

"Data for April showed that around 76% of mortgage debt is either floating or up for rollover within the next 12 months. Less than a quarter of mortgage debt is fixed for more than 1 year, and that’s low by historic standards (figure 7). It means that when the RBNZ does start raising interest rates, it’ll bite sooner for most people. This traction will likely lessen how much they have to hike by, but it’ll come at a cost to many individuals.

"A lot of forecasters, including the RBNZ and ANZ, expect the OCR to go higher next year," Croy says.

"Most forecasters also expect global interest rates to rise as central banks in other countries move into hiking mode eventually too. Right here, right now, there is certainly a lot of talk about higher interest rates in policy circles, across financial markets, and in boardrooms. As we progress down the track, the outlook could change, and it does seem likely that where we will end up (in terms of the level of interest rates) will be lower than in past cycles. But that’s no reason to be complacent, or worse still, reckless when borrowing.

"...There are reasons to think OCR hikes may come sooner than August next year, but there are also reasons to think the upcoming hiking cycle will be more muted than earlier ones. So there is give and take, and it comes down to a question of what risks you can live with.

"Given the possibility that interest rates do rise over coming months, we think it makes sense for borrowers to think about how exposed they are, and to consider fixing at least a portion of their borrowing for longer terms. The converse is true for term deposit and bond investors, who are likely to benefit from higher interest rates over coming quarters if they hold off investing for a while. But again, no guarantees! Hedging your bets is generally advisable with financial risks of any kind, and in this context that’s splitting up your mortgage or your capital and putting a bob each way.

"With leverage at an extreme, inflation rising and interest rate sensitivity very high, even if we are fairly confident that we have seen the lows in interest rates, we would caution against blindly extrapolating interest rate trends. Rather, we think it will be important to have a balanced perspective of the near-term risks while also recognising that there are structural issues that will constrain the level of interest rates over the coming decade."

12 Comments

Well there's a narrative with a few subtle messaging hooks there:

"it makes sense for borrowers to 'think about how exposed they are'"

"But that’s no reason to be complacent, or worse still, reckless when borrowing"

In a more common vernacular: "Don't say we didn't warn ya. We're not a bleeding charity. You're on your own buddy if it all turns to custard".

For a rockstar economy where house prices only go up and everyone wants to live here, they sure do put out a lot of disclaimers......

I have read the full ANZ report, I think it's very good, it explains in plain english the various factors and risks affecting interest rates. I hope some of the bank haters on here can put away their prejudice and read the report with an open mind.

But that's often the source of my anger. Bank economists saying watch what you borrow, while the same firm, ably backed by constant marketing, pumps out as much cash as possible.

"Data for April showed that around 76% of mortgage debt is either floating or up for rollover within the next 12 months."

Interesting stat, clear signal that kiwis think "she'll be right mate"

Scaremongering to lock people in for higher rates as soon as ANZ can. I'm not convinced the one year rate will rise anytime soon.

I have a daughter who has just bought her first house age 35 and she locked in for 5 yrs. I think it is a smart move as it gives certainty regardless of what happens.

Exactly! It’s about what you can tolerate and I think that’s Anz’s point. If you have borrowed a lot, then you can’t afford the risk so take out a five year fixed rate as insurance. If you are not so highly geared, then you could take more of a calculated risk and play the 1 year roll over.

Congrats to your daughter Hans.

I only fix my loans for a maximum 12 months,the kick backs from the banks, .75% back in cash or grocery vouchers, we haven't paid for food in 15 years. I love this concept of the banks tendering for my loans 1.99 from anz plus kickback- Can't beat that.

I always regarded debt as dangerous, and got it down as rapidly as possible.

Worked well. Equity and cash gives you options and control. Eg making a cash offer is much more attractive.

LOL, I did the same and my mates that leveraged up to the eyeballs are now much more wealthy than me!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.