By Bernard Hickey

Labour's Consumer Affairs Spokesman David Shearer has called on New Zealand's big four Australian-owned banks to "back off" putting pressure on heavily indebted dairy farmers, saying banks should instead dip into their record high profits to share the pain.

In a broad attack on the profitability of the big four banks, Shearer also said they had not passed on most of the falls in interest rates since 2008 to credit card customers and were not paying enough to term deposit savers.

He pointed to bank sector profits rising from NZ$3.6 billion to NZ$4.4 billion between 2013 and 2014 and that the profitability of the Australian banks in New Zealand was higher than their parents in Australia, and those of banks in other developed markets.

"The percentage returns as a percentage of assets is much higher in New Zealand than it is in Australia," Shearer told Interest.co.nz.

"These Aussie banks are making a mint out of New Zealanders," he said.

Shearer pointed first to credit card interest rates, which had only dropped to around 17.5% from around 18.5% in 2008, while the Official Cash Rate had dropped from over 8% to 3%.

"Credit card interest rates have dropped a measly 1% while the banks have made a cool 5% drop in the cost of the money they borrow," Shearer said.

"That's a massive hit considering there is NZ$6 billion on credit cards at the moment and NZ$4 billion is bearing interest payments," he said.

Charged an exception fee

Shearer said he had decided to look more closely at bank profits after he was personally charged a NZ$10 fee for three months running for accidentally exceeding his overdraft limit, "even though they knew I was a safe bet."

"I bet lots of other New Zealanders are getting hit as well," Shearer said.

"I looked at what the Australian banks earned in New Zealand and what they earned proportionately in Australia, and found the returns in New Zealand are much higher than what they are in Australia," he said.

"It seems to me that the Australian banks are literally using New Zealand as a cash cow to increase their profits, and I think that's wrong."

'Most profitable in developed world'

Shearer said research from the Parliamentary Library showed the big four Australian-owned banks made profits equivalent to 1.6% of assets in New Zealand, while their parents were making 1.28% in Australia. Their peers in the United States were making 1.1% and bank profits were 0.37% in Britain.

"Other than third world countries, it seems to be one of the highest in the western world. When the same banks in New Zealand and Australia have such different margins then it's pretty important," Shearer said.

He called on the Government to push the banks to not make such high profits.

"The Government doesn't want to get involved with this, but I do think they ought to be sending the banks some pretty strong messages," Shearer said.

'Cosy group giving each other winks and nods'

He said the big four banks appeared to be reluctant to compete hard by dropping their rates, apart from in specific areas such as fixed mortgages.

"The four big banks that take about 86% of the banking industry, none of them is going to be dropping their rates significantly and being an outlier, because everybody will end up dropping their rates and everybody will end up losing," he said.

"It looks like it's a cosy agreement between the four banks to keep looking like you're in competition around the margins, but they're actually all kind of giving each other a wink and a nod and making sure that everybody remains profitable," he said.

Shearer said he did not have any evidence of collusion or cartel behaviour, but he pointed to similar floating mortgage rates, term deposit rates and credit card rates, while competition was fiercer on fixed mortgage rates.

"The credit card rates all stay up around the same. The deposit rates, which are generally pretty low, mean that the banks are not paying out as much as they would otherwise do if they were really in competition," he said.

Shearer agreed that New Zealand's banks were robust and had strong capital levels, but the profit growth of NZ$800 million in a year had been too strong. He pointed in particular to ANZ's profit doubling to NZ$1.4 billion in less than a decade.

"That's taking it to extremes, and particularly now with farmers facing a real crunch with dairy prices falling, they should be taking a very careful look at how they respond to this," he said.

"It would look very bad if they started foreclosing on farms when many of those agricultural advisers those banks had put out there had been encouraging them to take on more credit."

Call for closer look from Govt and RBNZ

Shearer called on the Government and the Reserve Bank to take a closer look at bank profits.

"Those agencies should be taking a much closer look at our banking sector than they have been. I know Bill English has spoken to the banks about farmers, but he should be giving a pretty clear steer of what he expects from banks," he said.

"I'm happy for them to make a profit and be successful banks, but do they have to increase that profit year on year on year? It can only come out of the pockets of Kiwis who use those banks and they control 86% of the total banking sector."

More capital for Kiwibank?

Shearer said Kiwibank appeared in recent years to have joined the major banks in not competing aggressively across the board as the Government demanded it made profits and started paying dividends.

"Obviously Kiwibank has been told to make a profit and give a dividend to the Government, so there's not much pressure from Government to be more competitive," he said.

"By increasing Kiwibank's capital that would allow it more leeway to be more competitive," he said, adding however this was not Labour's formal policy.

NZ Bankers' Association responds

New Zealand Bankers' Association CEO Kirk Hope said bank profits were not high compared to other major companies operating in New Zealand and that returns on assets of 1.1% were the lowest of any industry.

"Bank returns on equity fall in the middle of the pack when compared to major companies listed on the NZX," Hope said, adding banks invested heavily in New Zealand and shareholder returns were needed to finance that investment.

Hope pointed to NZ$6.6 billion contributed to the New Zealand economy in 2014 in wages to 25,000 employees and other spending, along with NZ$1.8 billion paid in taxes.

"As businesses supporting our economy, banks needs to make a profit to stay strong and keep investing in New Zealand. Most New Zealanders welcome the fact our banks are strong," Hope said.

"The alternative, if you look at the banking sector in countries like Greece, is pretty catastrophic. We had no bank failures or bailouts during the GFC. That’s down to our banks’ strength and good management," he said.

Hope said banks were working closely with their farming customers to provide options including funding working capital in times of financial stress.

"Ask most farmers about how banks are supporting their business and you’re likely to hear a good story. It’s easy to take pot shots from afar but the reality is that banks and farmers are working together closely to get through what is going to be a challenging season or two," he said.

Responding to the criticism of credit card margins, Hope said the lending was unsecured and the higher risk was reflected in the higher interest rate.

He said between 1% and 3% of New Zealand credit card customers paid just the minimum each month, which was significantly lower than in the United States and Britain, and over 50% of customers paid off their balance in full every month. In the United States only a third of customers paid off their balances in full.

Hope rejected the idea that banks had a 'cosy' agreement.

"Our banks operate in an intensely competitive environment, not least because of the requirements of the Commerce Act, but also because of the business they’re in," he said.

"We see that in practice with mortgage rates falling recently and the way in which banks have moved quickly to retain and build their market share," he said, pointing to higher customer satisfaction ratings for banks than other service industries.

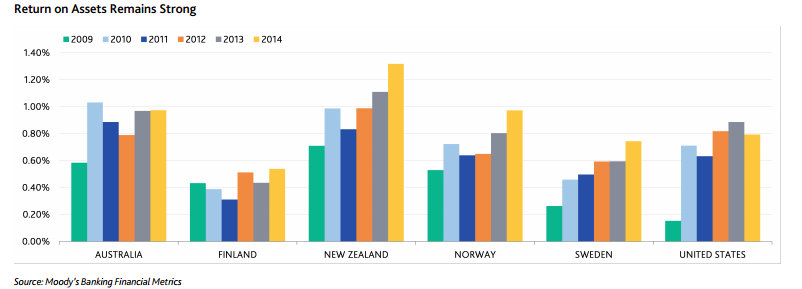

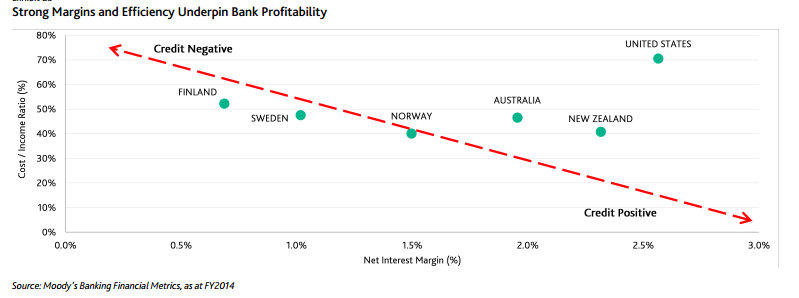

Moody's points to strong 'pricing power'

Earlier this week Moody's Investors Service pointed to the strong profitability and pricing power of New Zealand's biggest banks as a factor supporting its stable outlook for the sector.

"The banks' strong market positions have supported their pricing power, allowing them to achieve strong returns compared to the relatively low risk profile of their business models," Moody's said, adding however that competitive pressures remained high, particularly in housing lending in Auckland.

"On the other hand, competition for deposits has softened as deposit growth remains strong, while banks have met all regulatory liquidity and funding requirements," it said.

Moody's said it expected profitability to remain strong as efficiency gains and lower funding costs would offset pressure on loan margins and credit costs.

"We expect profitability to remain strong, but to stabilize after recent improvements. The profitability of New Zealand banks improved steadily from 2011-14 and compares strongly to their peers," it said, referring to the charts below.

"New Zealand banks boast above-peer margins and operating efficiency which reflect the industry’s concentrated structure and banks' considerable pricing power."

(Updated with NZBA response, Moody's comment and charts)

27 Comments

so.. is he asking banks to stop being banks?

Why exactly a bank has to share farmer's pain but not other borrowers' pain? Why are farmers so special? Many potential voters amongst them?

What they should do is clearly separate the commercial bank from investment bank and not to risk deposits when gambling in the same way as what they lend is not depositors' money

I was outraged when I was charged $25 for depositing $5,000 in cash on Monday .

Handling cash deposits is what the banks are there to do for goodness sakes !

The entire transaction took under 45 seconds , I used my card at the teller and he ran the cash through a counting machine , printed a receipt and I walked out .

Done in under 1 minute , that equates to a charge -out rate of about $1,500.00 per hour .

Nice work and its a captive market

Why? I have never been charged for depositing money.

You do if you have large amounts of cash (cash handling)

and Westpac tried it on for paying off Westpac Credit cards sometime ago (but got reminded that those pieces of paper say "legal tender" for a reason; a reason that would see them answering to the banking ombudsman if they tried to charge for me paying money to them

Excellent point. Legal Tender it is. Banks are afraid of cash. They can't count it and update thier stupid facebook page or twatter feed while sipping thier even stupider Latte.

the charge was from back in the day when they didn't have machines to count. It meant that people had to be taken off counter to count and recheck the numbers. That it was so high was just a price gouge.

Remember, you're paying "for the service" of counting, not actually being charged for a transaction.

Rules were brought in so it was a "per day" total ($3000 used to be the line) to slow people just writing multiple deposit slips. I believe that the banks also used to wear a fee if they had to declare/move large amounts of physical cash (eg a maximum on-site holding limit for security) so large deposits meant they had to schedule special pickups early.

The flipside is obvious, on withdrawls the bank has to order in specially extra "float" if someone wants to make a large withdrawl so often they charged a "counting" service on that as well.

It was a charge specific to you Boatman.

it''s a counting fee. check your cash limits and ask for the manager to have the fee to be waived.

I've transferred similar amounts and amounts as large as 100K and never had to pay for the privilege. Always electronically though. Even if it were cash, I would not accept the $25 fee.

And if Interest.co.nz wants to see a printout of the transaction charge , they are welcome

' banks should instead dip into their record high profits to share the pain'

OMFG, that is like robing a prey from the mouth of a predator.

Don't get me started !! ...the "BIG 4" Aussie banks are on the "luxury gravy train" with the NZ consumer ....best thing I have ever done and still do, is never pay interest on my credit card repayments....apparently I have heard on the inside that the "banksters" call customers like me "freeloaders".....I bet though they probably have a far worse name !

Cue Grant A to come to the banks rescue .....

Bit rich that they can repatriate these huge profits, while we have had to have OBR introduced in case of a banking crisis due to lack of sufficient capital, putting depositors savings on the line.

Why not make them keep the profits in NZ. Refinance the casino, build a bit of resilience into the system.

Instead it looks like the shareholders are asset stripping the banks and making off like a robbers dog before the SHTF.

They're not called banksters because they're angels.

The banks do what the RBNZ allows them to do. RBNZ could require all banks to set aside some of their profits as protection for depositors, especially for the Australian banks who currently are able to expatriate all profits off-shore.

A simple scheme to retain (say) 10% of declared profit in NZ for a period of five years - investing in NZ Treasury (so the banks retain ownership of these funds and receive interest) - but should OBR be implemented these funds would be to support the bank before NZ depositors are taken to the barbers for their haircut.

The RBNZ needs to start regulating banks more diligently. There are only 25 banking licenses they have issued - and they can require prudent protection of depositors.

An invocation of OBR will be an abject failure in their responsibilities - and likely to escalate into something more than a single bank failure.

How come dairy is being singled out again . Maybe if they had lived in the real world they wouldn't have taken so much debt on in the first place

Rearing calves for sale would help by cutting supply and providing stock for the dry stock farmers who won't be getting grazing next autumn

Simple solution, let the market do its thing!

That is, move your banking to a NZ owned bank, eg TSB, Kiwibank etc.

Even if they do make profits, at least their profits stay in NZ

I have. Moved all my money to Kiwibank as ASB wouldn't give me a mortgage (I'm a contractor).

Kiwibank have been incredible, very happy.

All very fine to be comparing with other industries but we all know specific industries have their own specific risk profiles. If these banks are some of the most profitable in the world then they have room to move with their customers.

"Responding to the criticism of credit card margins, Hope said the lending was unsecured and the higher risk was reflected in the higher interest rate."

I think Mr Hope is being a tad economical with the truth....a quick check of the fine print of ones mortgage will show the mortgage secures all obligations, including the credit card debt.

Well, depositors are unsecured lenders, OBR underwriters and yet get very little, if anything at all, when it comes to risk adjusted returns.

And yet there's no end to those willing to queue up and lend to them. It's 'safe', after all.

There was a good bank called bank of nz somehow it got sold. Who sold it and why they even forced me to sell my shares in it ?.

Mac123 - the BNZ got "sold"because it wasn't a good bank - its got into severe financial strife back in the early 1990's from memory, and had to be sold by the Govt to NAB - another Solid Energy type great Govt asset. Since then the bank has been returned to profitability and would now fit your description of it.

The book "Daylight Robbery" by Ian Wishart includes info on, as google books says "Ten years ago Ian Wisharts Daylight Robbery on the plundering of the BNZ and other state assets became an instant bestseller. "

Irrespective of the BNZ situation in the last 80's and early 90's, we needed to own a bank Marty ?

History repeating itself ????

Ten years ago Ian Wisharts "Daylight Robbery" on the plundering of the BNZ and other state assets became an instant bestseller.

Now, a decade later, asset sales (partial this time) (same thing) are again on the cards as Prime Minister John Key seeks a controversial mandate for privatisation

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.