By David Hargreaves

When you really think about it, the whole thing is beyond odd.

Here we are still merrily clocking up seemingly ever more momentous-sized mortgages and yet the weight of these beasts is actually getting lighter - in terms of debt servicing requirements. The country's mortgage holders are becoming super heavyweight lifters.

This is counter-intuitive and it's all down to falling interest rates, which are easing the monthly burden even as the amounts borrowed get bigger. Just don't think of how much you've borrowed. Or how long you'll be paying it off for.

But these are strange times.

In the mid 2000s all seemed 'normal'. House prices shot up, borrowing shot up, and er, so did interest rates, leaving the populace up to its nostrils in debt that was, sure enough, getting markedly more expensive to service. And that's what's tended to happen previously.

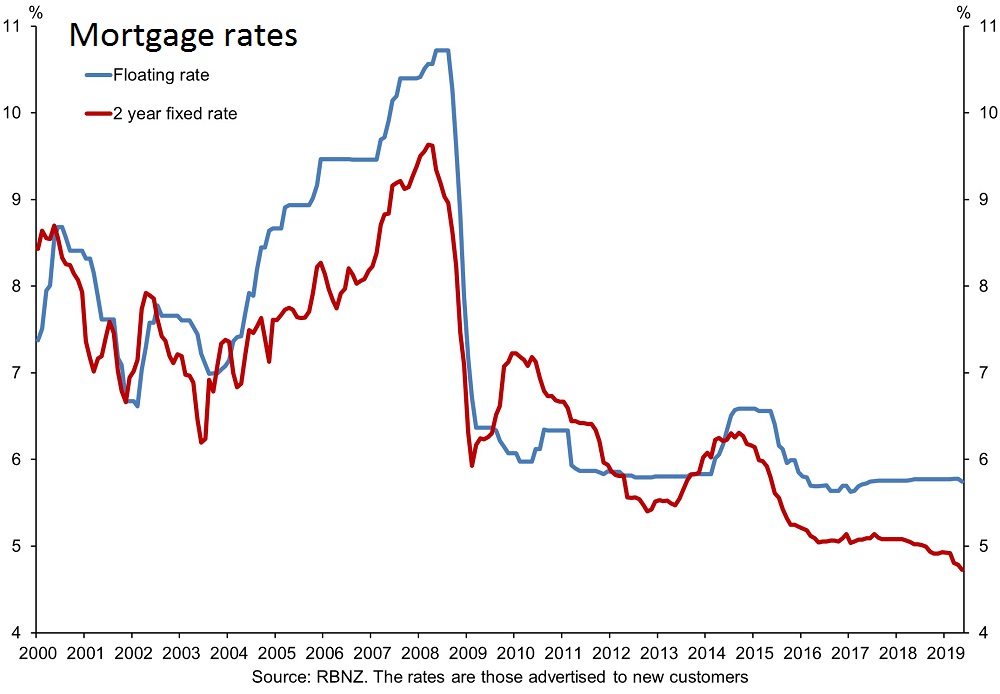

Between 2001 and 2007 (according to Reserve Bank figures) the average floating new mortgage rate for new customers rose from 6.7% to over 10.5%. A lot of people saved themselves pain for a while by fixing for quite long terms, but it all caught up in the end.

On an annual basis and again according to RBNZ figures, interest payments on mortgages (including for ownership of rental properties) took 8.6% of household disposable income in 2001. By 2007 this was up over 12.5% and was to go higher than that still, peaking at 13.8% at the end of 2008.

After the Global Financial Crisis of 2008 though the world is a very different place.

We've now gone through another period of rapid house price appreciation. Very different reaction. Barring the erroneous hiking cycle by the RBNZ in 2014, which saw the Official Cash Rate lifted by a full percentage point to 3.5%, interest rates have stayed down and indeed continued to fall. One significant reason is that this time around there was little secondary inflation generated by the higher house prices. Not like the previous time.

In mid-2008 the OCR was 8.25%. It then fell to 2.5% by 2013, rose from 2.5% to 3.5% in 2014 and stayed at that level till into 2015 before it started falling again. Now it's 1.5% and likely to go a bit lower yet.

Over the same time periods, according to RBNZ figures, the average floating rate on new mortgages for new customers dropped from 10.88% in mid-2008 to 5.87% in 2013, before heading back up to 6.71% in 2014 and then falling back again, dropping to 5.73% as of May 2019.

It's worth noting that the RBNZ figures show a 0.12 percentage point drop (from 5.85%) in the floating mortgage rate since April, following the 0.25 percentage point cut to the OCR in May.

That's floating rates of course and they've been rather more tardy in dropping than fixed rates.

The more detailed latest figures on average new 'standard' lending rates from the RBNZ highlight some fairly marked drops even from the start of this year, with the five-year-rate for example having been cut by more than half a percentage point since January (from 5.58%) to 5.04% as of May.

And the figures for 'special' rates highlight the trend even more, with the five-year rate having eased from 5.07% in January to 4.46% in May. Just as some example, on a $400,000, 30-year mortgage, May's 4.46% rate would save the mortgage customer $47 a month compared with the January rate.

The RBNZ has also recently released its latest quarterly key household financial statistics. There's a bit of a lag on these figures and the latest ones are for the March quarter and so therefore don't include the impact of the RBNZ's recent OCR cut. It will be interesting indeed to look for the June quarter figures later this year and see how strong the impact has been.

The key household financial statistics series dates back to 1998.

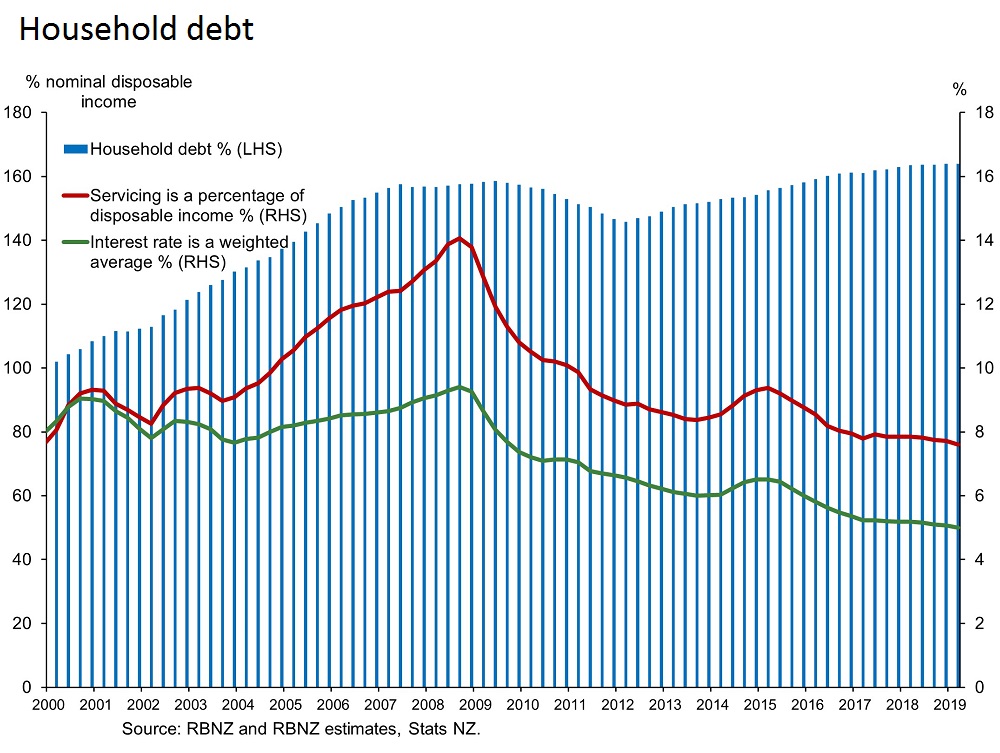

One of the statistics closely looked at is household indebtedness in relation to disposable income. There's two choices of figures there - either the percentage that includes rental properties owned by households or the percentage that excludes those, which of course is lower.

As of March, household financial liabilities, excluding rental properties, had risen to 125% of annual disposable income (a new record high) from 124% in the December quarter. At the start of this series in December 1998 the household financial liabilities equated to just 75% of annual disposable income.

Including rental properties owned, the percentage figure for financial liabilities to annual disposable income as at March 2019 was 164%, which is also a record high. However, the figure's now been the same for 12 months, which is good news if you can call it that. Sitting on a high plateau. Back in December 1998 the equivalent figure was just 99%.

So, our households are apparently drowning in debt. And yet. They are not. Not in terms of what they can 'afford'. We do have to bear in mind, however, that these are AVERAGE figures generated by dividing a total of household disposable income nationwide by the total interest paid on mortgages. So obviously within those broad figures some people will be seriously pushing the boat out while others won't in terms of commitments.

If you look at the crucial figure (and I will use the annual one to March 2019) of how much of household disposable income is going toward mortgage interest (and this includes rental properties owned) the latest figure is just 7.7%. So on average just 7.7% of disposable income going on interest payments. That's actually the lowest this percentage figure has been for exactly 19 years. Only in December 1999 (when the figure was 7.6%) has that figure been lower since the RBNZ started this data series.

I go back at this stage to how things were looking when the GFC bit hard and things were looking a lot more stretched on the disposable income to interest payments front - with that proportion of annual disposable income required for interest payments hitting 13.8% by December 2008. Remember around that time floating mortgage rates on new mortgages had been close to 11%. Yes, the monthly mortgage bill was looking a bit chunky.

So, what a difference the low interest rates make and thank goodness for them at the moment. (Though investors aren't saying that, and therein is a different story).

The fact remains though that there's a lot of debt. People, particularly first home buyers, are having to borrow heroic amounts of money. According to RBNZ monthly mortgage figures, the average sized mortgage taken out by FHBs is running at over $400,000.

How comfortable can and should we be that we are almost now in a situation where people could be encouraged to get even deeper into debt based on what the current debt servicing costs are?

Rates are still going down

Interest rates are down and likely to be down for the foreseeable future. Indeed, I'm convinced the RBNZ has not finished cutting the OCR this year and will, probably in August, cut again, to a new low of 1.25%. And who knows there may be another cut on top of that early next year. Certainly the ANZ economists think so.

For how long though should any would-be borrower rely on interest rates staying down? Well, there's a question. And I would not even begin to hazard a guess - which is all it would be.

What if the house market does show some signs of turning up again? Remember it's still ticking over okay anyway in some parts of the country. Auckland of course is flat though.

If people see house prices getting away again then the temptation will be to get into the market at all costs, with costs being the word.

A 'new normal'?

The key question is, do we believe interest rates at this level or only slightly higher are now a 'new normal'? If so then at current levels of serviceability it actually makes sense to borrow to the hilt to get a house. It's borrowed money that's as near to free as we've ever seen.

But, ohhh. It wouldn't take long for any even fairly small rises in rates to start causing real pain. Just as a very quick example if you added two percentage points to the current floating mortgage rate for a $400,000, 30-year loan, this would add $530 to the monthly interest bill. THAT would be noticed by the customer.

The trick for particularly first home buyers at the moment would surely be, okay, if you think it's what you really want, get on to the ladder, and enjoy the low interest rates. But stash every extra cent you can and start paying that mortgage down as soon as possible so you can start raising your equity in the house.

Generally I don't think anybody should plan for serendipity. Therefore it still worries the hell out of me that the current low interest environment potentially sets us up for big problems later if we do at some point start to see interest rates revert back to what we used to regard as 'normal' levels.

Planning for the worst may seem a rather joyless way to go about life, but it tends to alleviate nasty surprises. Here's hoping for a surprise-free few years. But I'm certainly not counting on it.

83 Comments

This last drop in interest rate was surprising to me. Using up the ammunition prior to it really being needed in my view.

DP

Interest rate will continue to drop as the world needs zero rates to keep the oil pumping. It's as simple as that.

only until the next GFC

"People, particularly first home buyers, are having to borrow heroic amounts of money." Heroic ? Frightening more like it! The capacity to endure rising interest rates is slim to nothing, so any turn in the money markets could be literally catastrophic for the individual as well as banks in general. Banks must be either really confident they can manage the risk or supremely stupid and complacent about the level of risk they have taken on. Or do they perhaps have designs on being the largest property owners in NZ? Possibly believing the Government will allow them to flick on mortgagee properties to foreigners if they get saddled with lots? The other belief they will have is that they will get bailed out by the Government and the taxpayer. this is why they need to be robustly regulated.

"Banks must be either really confident they can manage the risk or supremely stupid and complacent about the level of risk they have taken on"

I think both statements are true.

Peri - That statement could easily be applied to those taking on these huge mortgages too! Extremely confident or extremely naive. A conversation I had recently with a first time buyer would suggest the latter! No idea about where we are in the property cycle, along with no concept that their home could reduce in value!

Yes agreed and that's the thing. Some FTB's might not realize how the NZ property market got to such extreme price levels in the first place. Though I have found that most of my younger friends have figured it out and are prepared to wait until the market drops further, rather than take on the extra debt to keep up those higher prices generated by all that money laundering and overseas buying that was going on especially for Auckland. I can also tell you that those GenX and Millennials are very cheesed off with the way that their Boomer parents, who were quite happy to sell their future off to the highest bidder. So lower interest rates can only really help to a certain extent.

"What if the house market does show some signs of turning up again? Remember it's still ticking over okay anyway in some parts of the country. Auckland of course is flat though."

Auckland isn't flat ~ its declining. Mortgage rates are declining because government yields, which drive swap rates have plummeted. This isn't good news as the bond market is telling us to expect no wage growth or inflation for a decade ~ yes, a decade.

Why is this news being overlooked and instead we get a plethora of articles on lower rates ? Anyone would thing this is a good news. It's not ~ good news would be real wage rises, diversification of the economic output of the country and yes ~ RISING rates as this is what you get when an economy is GROWING at a decent rate.

"when an economy is GROWING at a decent rate"

Growth was always going to be a temporary thing. We managed it for about 200 years, not a bad effort. We were running an extract/consume/excrete process - entirely linear - and exponentially increasing the rate of same. In energy terms, we start with low-entropy energy and end up with high-entropy stuff (low-grade heat, mostly). We're heading for ever-more entropic resource-collections, too. Malthus, on this point, was entirely correct - he'd have probably predicted the trend to zero and below, of interest-rates. As it is, only us energy and systems types seem to see it.

Essentially, we were drawing-down a finite bank-account - Natural Capital plus energy. Those were not - contrary to the ignorant claime - fungible with 'technology', 'capital', 'labour' etc. Without them we simply have nothing. As we go over the Peak, of course interest-rates will go zero then negative (if they don't, someone else is getting disadvantaged by the interest-charger). What this article misses, is the ever-decreasing opportunities to pay off the collective principal.

This is why Steve Keen (who gets) suggests a debt jubilee. It's the only way left, to fit the obligation with the dwindling opportunities left.

A 'debt jubilee' would make me absolutely, beyond apoplectic.

It gives a free pass to rank stupidity and waves a white flag to moral hazard writ large.

I don't like the idea either but how do you see debt unwound otherwise? I'd be happy with a crash which could be seen as a "comeuppance jubilee" in someways. We are stuck in a spiral which will have to end naturally or unnaturally at some point. What options do we have?

More debt (and then a crash) OR a crash.

Debt/money is just a token for a future energy surplus

If there is a shrinking energy surplus per capita (ie a hard Physical limit), then purchasing power will decrease.

Playing around with energy tokens was only ever a temporary solution.

As far as a jubilee, taking more tokens off the table changes nothing about the physical limits. It just acknowledges the number of viable consumers (and therefore producers) is massively overstated. And this undermines economies to scale / globalization & supply chains in every way.

"As far as a jubilee, taking more tokens off the table changes nothing about the physical limits." Correct and nor should it. I think your conflating the coming financial crash (a result of our money system) and us running into energy limits (our desire for a higher quality of life).

conflating yes - because the financial system is how we (currently) direct energy flows. There is no other purpose for having a financial system

The alternative is some sort of war/slavery - energy flow direction under a different form of duress

Hmmmm, saying that the financial system (money) is what directs energy flows is like saying a hammer directs nails. Both money and a hammer are tools used by people to achieve outcomes (money is a medium of exchange). Our financial system definitely unfairly directs wealth to certain sectors however it is still up to those sectors as to what they use it for. It's still a tool.

I hope it doesn't appear like I'm splitting hairs here. I'm trying to deliniate the separation between the two because if you blame one (money) for effecting the other (energy) when it's not the cause then nothing will come of changing it in relation to the outcome you want for energy.

Not sure of your point - but energy underwrites money (not the other way round)

All exchange is ultimately for products of energy (why would we bother exchanging money if it wasnt redeemable for anything real..?)

Basically no amount of issueing more credit tokens changes physics - it just temporarily SUSPENDS FAITH that the future can deliver ever greater amounts of surplus energy... because if we dont believe the real economy can grow the debt must decline in value

(eg would a bank lend me $$ to buy a farm if I told them my production would decline 10% per annum indefinitely ?)

Its also pretty obvious now the money supply is way outstripping real growth and issueing further debt is losing its ability to provide any stimulus

"but energy underwrites money (not the other way round)" - Not really. Money is a medium of exchange that we agree to use that purchases products of energy. See the difference? Money can be traded for energy and vice versa but that doesn't mean they are intrinsically linked. Again, money is a tool, it is what humans CHOOSE to use that tool for that has an effect on energy and our use thereof.

What you have an issue with in relation to energy and physical limits is human behavior and not money itself. The money system is flawed absolutely but if you want to change how energy is viewed or consumed you've mistaken our financial system as the culprit.

Yes infinite growth of our financial system is impossible. However, even if we had a sound money system we would still try to consume more than is sustainable, it is human nature, greed and lack of education that is to blame. Both need to be fixed but blaming one for the other is incorrect.

Im not sure where you get this whole blame / culprit thing?

The cause; declining energy surplus per capita

the symptom; a financial system about to implode

Energy underwrites money, I repeat.

ask yourself, would we "wealthier" if

a) we doubled the amount of money in the world?

b) we doubled the size of the world?

The money is irrelevent. Its just a system of allocating energy flows

and we have been gaming the system since 08 ....

"Im not sure where you get this whole blame / culprit thing?" - To quote yourself back to you - "because the financial system is how we (currently) direct energy flows. There is no other purpose for having a financial system." - Your blaming the financial system for directing energy flows when it's human nature.

"The money is irrelevent. Its just a system of allocating energy flows" can be changed to "money is the medium of exchange we use to direct energy flows. Again, it's not the money that directs energy. It's what we choose to do with money.

To offer an olive branch, I get how you can see financial system that largely requires exponential growth to function (technically no, but in practice yes) as being underwritten by energy as it will require expansion forever. However, as you correctly point out. 08 was a big moment in the gaming of the system. It was people who chose to interveen and keep the system pumping. This is what I mean by it is human nature. Our financial systems should have crashed many times over well before 08 but due to continued intervention by people propping it up they haven't.

Regardless of the financial system, our behaviour needs to change. That is the key and the crux of the issue.

I dunno, some consequence for being reckless/naive/ignorant to the risks & obligation you took when you assumed that debt - and contributed to the inevitable downturn that will hurt everyone else:

- Bunkruptcy (a given);

- A 'sentence' (we could call it) that places restrictions on the amount of leverage particular people can take on in future. Worst 'offenders' can not leverage up for anything other than their family home ever again, and minimal leverage is available for that family home (<3x DTI). These are people that have demonstrated that they are not competent with free access to debt, so no more sugar bowl for them;

- 'Sentence' could also include total restriction on setting up a company or trust, being a director, shareholder or beneficiary of a trust - any and all interests post debt jubilee must be held in their own name and it applies to related persons.

If we're going to have a 'debt jubilee' which, let's face it, is a nuclear option then let's make it so the radioactive fallout hits those who caused it. And hits them hard.

Well there goes the political class!

The idea is everyone gets a fixed amount of money, say $100,000. If you have debt, it pays off the debt first. If you don't have debt, then you get it as cash.

That way everyone gets the same benefit and no-one is disadvantaged.

so not a debt jubilee -- more like a Debt injection (money IS Debt!!!!)

so we get more money (Debt) chasing the same amount of resources.

Sounds like inflation (a devaluing of what money can buy)

Nice try.

The money could be brought about with no debt obligation so that would alieviate one issue but yes, it would be inflationary. Does anyone have any thoughts on the "Chicago plan?" Similar-ish idea but different method.

All money is a promise (a debt) .... it relies on the faith that it can be exchanged for something REAL in the future

The other not so simple issue is Does every person on the planet get $100,000? Just the West? Just those above 16?

It sounds like inflation would kick in immediately

I disagree. Money is debt if it was brought into being due to a loan that has to be repaid. Hence the debt obligation comment. The definition of debt is "a sum of money that is owed or due."

The fact that money is an agreed medium of exchange does not make it a debt. Relying on faith that it can be exchanged for something in the future also does not make it a debt either (unless your talking about something like a futures contract, then your argument could be made). These are other things entirely.

If money is not a debt, is it any use?

Yes, it saves us from bartering. That was the original point of it. Remember for that the overwhelming majority of history, money wasn't fiat or debt. This debt money is a relatively recent invention.

I didn't say money isn't debt now. It is (or at least 98% of it is). I'm saying that money CAN be brought into existence without a debt obligation and that it has not been fiat or debt money for most of history.

ok sure - then its the 98% bit thats the concern

I know, I bang on about it all the time. Glad we agree :)

Withay you know the barter thing never happened dont you. It's always been credit. Barter is a ridiculous way to run an economy. Even a very basic one..Anthropology reveals the barter idea to be a fantasy. See Graber's book Debt the first 5000 years. The value of fiat money is that it is the only thing you can pay ird with.

Yes, the purchasing-power of 'money' would be severely diminished - grotesquely so.

But it's the only way to shoehorn the existing system into the real world.

The alternative is a crash. Which would be followed soon after by die-off, warfare and chaos. Unfortunately, I suspect this is what will happen - the debt method is one way of managing some sort of coherent transition.

Does shoehorning the system in any way then stop a further deflationary spiral ?

Probably not

It goes against economies to scale - Its is basically like telling (eg) Toyota/spark/fonterra/shipping lines/retail , the total market for your cars/phones/milk/freight services/retail is now only 25% what it was.... how would those supply chains ever stack up?

I understand the point you are making. Was the idea of a debt jubilee ever intended to apply to Auckland residential mortgages ?

Great article David. I totally agree with your concluding paragraph:

"Generally I don't think anybody should plan for serendipity. Therefore it still worries the hell out of me that the current low interest environment potentially sets us up for big problems later if we do at some point start to see interest rates revert back to what we used to regard as 'normal' levels."

I hope FHB - or someone else with a large mortgage - note this and will be paying down principal as much as possible during this what is an abnormal period of low mortgage rates continues.

There is the complacency that $25,000 at 3.8% is costing less than $1,000 bucks a year which pales compared to interest on the credit card, so that deck, overseas holiday, or new car is really affordable.

I don't think its all doom and gloom. Interest rates will probably only go up if there is inflation. Inflation normally includes pay rises.

Hi David, I'm interested in what measures you considered when defining the Auckland market as 'flat'. I would generally consider a market as flat if it was keeping level with inflation.

The HPI shows Auckland prices are falling 4.4% yoy, on very low sales volumes. Personally I would struggle to define that as flat.

We are in a multi decade trend of descending interest rates. It amazes me that for all the commentary on this few people ask why this is. I will go further and say any comment that ignores this canary in the coal mine is critically deficient. But hey we have free speech, and even an apparent democracy, where you can pretend you know something and comment anyway.

Agree on risk here.

Not on "flat". What is a "market". Is it just price?

Surely it refers to buying and selling.

REINZ website shows apartment sales in Auckland down 44% in May compared to 2018.

Also, it shows sales lower in first 5m of 2019 than they were in 2008.

That is TOTAL sales, not simply residential which is why REINZ puts in its press releases.

Average mortgage of FHB is not for Auckland.

RBNZ is under-counting because they take figures form individual banks and do not consider that people are borrowing multiple loans. SO risk is far higher.

"The key question is, do we believe interest rates at this level or only slightly higher are now a 'new normal'?"

- It's simple. We have inflation targetting in NZ. To achieve this increase of money supply we go to our favourite mechanism for introducing new money - home loans. Now, ironically as home loans aren't really that productive and we don't generate any extra income to help pay our debt so we now rely on inflation targetting to eat away the value of the loan. To achieve this inflation, we go to our favourite mechanism for introducing new money - home loans.

And so the cycle repeats. What we see is higher house prices, longer mortgages, lower interest rates. This cycle will repeat until it can't anymore and then pop (or at least some very creative and destructive policies from the party in power at the time to keep the cycle from breaking down).

We aren't exactly setting ourselves up for the future here...

Well put. It's been a case of betting double-or-quits on the future. All the while, the future is being mined by the present. There is no alternative to a massive correction - whether it be a Weimar-like reduction in purchasing-power or a straight-out run on the banking system.

I agree, with a crash or run on the banks etc. we will be getting our future back to a certain extent in a weird way. I do fear though, that when the opportunity to change presents itself due to a crash, we will blindly pass it up and carry on the way we have been. More "stimulus," more debt, lower rates and more of the same.

I hope a politician can craft a clear and honest narrative about why our money system has failed us so that the general population can understand and good ideas can finally get some cut through politically (or at least we can stop the bad ideas).

"I do fear though, that when the opportunity to change presents itself due to a crash, we will blindly pass it up and carry on the way we have been. More "stimulus," more debt, lower rates and more of the same."

That's happening now and of course that will continue to happen. Whoever is in power wants to stay in power so crashing the economy is an absolute no-go.

The increase in indebtedness is Phil Twyford's fault (with help from Auckland Council).

Auckland is not flat in the traditional sense, it is undergoing a cost reduction phase with increased building activity (caused by the 2017 onwards land availability). If Phil Twyford had carried out Kiwibuild as he promised to, there would have been a greater cost reduction in the Auckland market and further increased building activity. This would have meant increased wage growth, improved economic performance and lower housing costs.

But because Phil Twyford is a completely useless lying politician, it has now become necessary to slash interest rates and consign a generation of home buyers to monstrous debt loads.

Since the indebtedness starting increasing (turning around from a sharp downward trend) around 2012, it's only fair to give some credit to the previous government as well.

They are responsible for this trend, and the current government is guilty of maintaining the status quo.

U-C - let's stick to the truth, eh?

This is indeed an all-Party failure, and a societal one as well, given that we vote them in.

And, unaha, it is largely an Awkland problem, but having said that, it has bled outwards into the Tauranga-Hamilton and Northland adjacent areas as well.

Because (but of course) Christchurch has had no appreciable bump - which is down to the LURP release of lotsa serviced sections (prices start with a 1), lotsa house+plot deals (prices start with a 3) and a generally flat median price trajectory.

Now it can be argued that Christchurch is Speshul, because of the liquidity injection ex insurance, EQC and so on. But this is no different in type from - say - Tauranga - where the cash injection is from a different source - cashed-up Awkland refugees. It's still a massive cash injection into a localised market. But the Tauranga effects are wildly different - constrained serviced land supply has led directly to a bidding-up of prices as all that Munny has to find a Home near the Beach.

Which rather bears out your contention: supply-constrained areas have suffered the most.

Various fantasies, Reserve bank is independent, there is no inflation

Facts government is drowning in debt, local government is drowning in debt, many households are too and a good proportion of farms and businesses.

Solution fiat money and keep interest low to avoid the house of cards collapsing. At the same time any real money stored by prudent savers should be eroded by low interest rates.

Savers prop up high geared debtors. The new normal is a construction by the financial sector and politicians treading a high wire and no safety net. Within this fiat money is laundered and mixed with real money and the scurrilous perpetrators get great bank balances.

No wonder the price of Bitcoin has risen substantially this year!

On the article about where put term deposit money one of the suggestions I put forward was investing the money in mortgage payments. It works as a part of a diversified portfolio, and the return is acceptable. Despite there being greater returns elsewhere having a large pile of debt is a risk. The debt is denominated in NZD but the interest payments are a percentage. The 11% of the past caused a lot of people pain and they struggled to pay. Whereas I was on the other side collecting healthy interest payments.

While the rates are low now it only takes a currency issue to create massive inflation problems which leads to high interest rates. For example when sanctions hit Russia over their invasion and occupation of Crimea they had massive currency problems. I believe their interest rates climbed rapidly to 14%. Given the large number of $500,000+ mortgages and then apply 11-14% you get a large amount to pay and most likely a lot of defaults.

Take advantage of the low interest rates to invest and comfortably pay down debt.

"But, ohhh. It wouldn't take long for any even fairly small rises in rates to start causing real pain. Just as a very quick example if you added two percentage points to the current floating mortgage rate for a $400,000, 30-year loan, this would add $530 to the monthly interest bill. THAT would be noticed by the customer."

That's the crux of the article for me. Just eyeballing the historic mortgage rates graph, it's clear to see that rates can blip up and down by 50 to 100 bips over short time scales. The effect of such changes is much less at high rates than at low rates. So the vulnerability now that low rates seem - Seem - to be semi-permanent, is now heightened.

Average size mortgage is $400,000? Yeah right! In Auckland the mortgage sizes most are taking on are anywhere between $600k and $800k for first home buyers. The RBNZ have been getting their averages from mortgage portions, not the total amounts so the data is misleading.

When I caught up with a mate in the banking sector he was quite surprised at how small my mortgage was despite buying 5 years ago.

I still remember a Banking adviser telling me I had "only a Baby Mortgage" of ~$400k.

That was in 2015.

I was like, really?

I earned probably 3x the median wage at the time and it was a lot of money for me.

HI Adam BNZ

Correct mate.

The Average size of a ‘loan’ is not the aggregated loans that actually form the complete mortgage or total household debt exposure. The number of loans to first home buyers does not match the number of purchases they are making. The average is actually significantly higher than this.

Take a look at ‘Wanted First Home Buyers - Your Country needs you.’

I have since had this confirmed by a contact at the RBNZ. Loans are not total mortgage debt same as in Australia where this fraud has recently been uncovered by APRA, with a little help from external research - hence the higher capital requirements that will on there way there too!

It’s a dangerous situation, but we are complacent. As you say “our households are apparently drowning in debt. And yet. They are not. Not in terms of what they can 'afford'” at the moment. NZ housing values are still sky high in world terms. We only need to look at recent history to see what could happen, and we won’t be prepared for it: Ireland, Spain during and after the GFC, or Japan since their 1980s property (and stock market) bubble and bust. Interest rates could stay low, and go lower, and we’d still be in a lot of trouble because of our debt. The housing market is declining a lot in Australia, and their interest rates are historically low and going lower. We’ll be right though, eh?

The outcome will be falling home ownership rates whether mortgage rates continue to fall or if there is a sustained increase in mortgage rates. As GDP has been distorted by the sectors that support rising house prices and rising house sales for two decades, as one or other or both decline, growth will slow, the OCR will continue to fall. The group that will benefit the most from a rising OCR will be the very same group that benefits substantially at present.

I see Stephens at Westpac is talking up house price rises next year off the back of falling interest rates. But I fail to see how a cut here or there will have much impact.

Different story if the OCR is cut to zero, of course.

He makes me laugh!

Yeah. And he's a bank economist. I am cynical about economists anyway, but even more so when employed by a bank.

He comes from the same brain dead economics brigade at the ECB, Fed, that thought lowering interest rates would increase borrowing, growth, inflation. Their two dimensional thinking doesn’t take into account confidence, rising taxes, etc. So, while they chase the flawed EMH and quantity theory of money that the muppets still teach at varsity, the real economy continues to slowly burn to the ground while these thinkers drive our economic policies. When interest rates get close to zero and taxes/rates keep rising there will be NO room for anything to go wrong (which of course it will sooner or later). I guess that’ll be the point that the RBNZ starts buying all NZ govt and council debt...happy days.

Really well put

Indeed. From my experience of similar situations it is often those in the banking sector that take on the biggest mortgages in the good times.

I fail to see how if it will make an impact if, allegedly, everyone is still stress tested at 7%.

While I managed it somewhat, my focus was never on interest rates. But I sure spent a few decades obsessed with paying down principal.

Boy has it worked for me. No debt means high cash flow income, low anxiety and not being just an agent trying to chisel a small margin as they pass money on to the bank.

Currently all I have to manage is some rolling term deposits which are awaiting a building project.

Ditch the debt as best you can. Cent by cent if that is the way youhave todo it.

Including rental properties owned, the percentage figure for financial liabilities to annual disposable income as at March 2019 was 164%, which is also a record high. However, the figure's now been the same for 12 months, which is good news if you can call it that. Sitting on a high plateau. Back in December 1998 the equivalent figure was just 99%. So, our households are apparently drowning in debt. And yet. They are not. Not in terms of what they can 'afford'.

Maybe? The RBNZ had this to say:

The proportion of risky borrowers in the household and dairy sectors appears relatively high. Around two-thirds of households have no mortgage debt, but nearly 40 percent of new mortgage loans are to borrowers with DTI ratios above five. In the dairy sector, 35 percent of debt is to highly indebted farms, defined as farms with more than $35 of debt per kilogram of milk solids produced annually. However, less than5 percent of loans to the commercial property sector are to particularly risky borrowers,1 suggesting debt is fairly evenly distributed across the sector.

Moreover, the households with mortgages DTI(disposable) ratio increased marginally to a record high of ~320 percent at the end of 2018 (figure 2.3). Link-page 8 (14 of 48) PDF

Your first sentence is incorrect.

It's not odd. In a bubble (yes it's a bubble when prices appreciate faster than average wage), you need at least the same amount of credit expansion by percentage per year to keep inflated asset prices up. Even a drop in the rate of increase leads to dropping prices. This is all you need to know if you want to understand the falling OCR and interest rates.

The RBNZ and merchant banks don't want mortgages bigger than the value of the property they are written for. They don't want affordable housing. And they want more people to 'step up' and borrow. They will do everything to defend sky high property prices, and they've just about done everything they can to do it, bar allowing Chinese money back into the NZ ecosystem. If the temperament of New Zealanders is anything like Japan, people will become averse to borrowing huge amounts of money even at record low levels of interest. They just won't borrow. Or can't. Interesting times.

Very well articulated Mr Knight. I think you may have hit the nail on the head.

I've been watching you and Martin like a hawk :)

Good stuff. I thought you might be the same Jedi.

Of course if interest rates went up 3% or more it would be carnage on the streets, that's exactly why they're not about to rise. The RBNZ (and other RB's around the world) are fully aware of this and they are not interested in precipitating the next recession/depression, so interest rates will stay low for a long time and go even lower.

Until all you debtors are being margin called because deflation goes through the floor.

What do you mean? We’ve had 50 odd years of inflation, so it’s safe to predict another 50yrs ahead of the same right? Much like the climate change models predicting that whatever trend is in motion will stay in motion. All those previous cycles in economics, climate, etc, over the last few thousand years are not relevant anymore, right...?

Exactly guwop, the banks do NOT want their debtors to fail and they will do everything possible to avoid this situation, rates at 0%, money printing, government spend up...

"One of the statistics closely looked at is household indebtedness in relation to disposable income"

Here lies the answer to your conundrum (and the mistake) it's wrong to compare financial position (debt or liabilities) with cashflow (income). Any half decent accountant knows this. Isn't there an accountant amongst our commenters?

I have given this example multiple times before; let's assume for argument's sake that an DTI of max 5 is acceptable. Today John has debt of $500k and earns $100k = DTI of 5. Today he pays 4% interest = $20'000pa. Let's assume interest rises back to 8%, John will then pay $40'000pa a very significant difference and he may well struggle. How much has his DTI changed? Not one bit, because it's wrong to compare D with I.

But the whole idea of looking at DTI is to mitigate the implications of potential interest rate rises going forward. Once you have a DTI of "x", you're essentially locked in. There's 3 ways to adjust your DTI. Pay it down, get a pay rise or sell the house. It's not a current "affordability measure", it's a potential future liability/risk measure.

By the way, why would John struggle? Don't the banks benchmark at 7 - 8% interest rates? Regardless, if John were to struggle on 8% (roughly the historical average) then surely in hindsight/lack of foresight a DTI of 5 is too high.

Or it could mean that a debt to income ratio of 5 was too high to begin with.

This time its different :)

With the signals being more OCR cuts, expect things to carry on the same. Most people are not going to put their life on hold for years waiting for a property crash, they are getting on with life and just buying a house. When was the last time interest rates were this low ? thats right NEVER. Also I cannot remember a time that the signals were for even more cuts. Yes its propping up the property market, but like I said when Labour got in, nobody wants to crash the economy on their watch so its everyone's best interst to keep the party going. Unfortunately no government can shield us from an external shock.

David, do some research. You'll find that the average interest rate over the last 300 years is around 3.8%.

Hint, start at Gilt yields, they have a long series. The 1970s-1990's were the anomaly, not the norm.

No need to say thanks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.