Well, we've had the big save-up.

Will this be followed by a big spend-up? Or perhaps more to the point, will people be confident enough to at least keep spending reasonably 'normally'?

It matters. With no inbound tourism to fuel the economy the extent to which New Zealanders are prepared to now get out there and spend money will be important in getting our economy up and running again.

There's clearly been some 'relief' spending since we reverted to the near normality of Level 1 from June 9. But economists doubt that the spending will continue.

And so do I.

What is clear is that, denuded of ways to spend money in and around lockdown time, Kiwis have been stashing the cash. And how.

Credit cards were largely put away. Big time.

Reserve Bank figures show that, remarkably, advances outstanding on NZ credit cards plummeted from $7.368 billion as at the end of February to just $5.788 billion by the end of April. That's a 21.4% reduction in just two months and it took the outstanding advances figures back to levels last seen eight years ago.

There was a bit of a bounce back in May - as we started emerging from lockdown - with the outstanding balances topping $6 billion again.

Obviously, it will be real interesting to see what happened in June as the shackles were fully released. We will find out in due course.

Save, save, save...

And we weren't just reducing our debt while in lockdown. Oh, no. Save was the word. And when you are locked up, saving it seems is surprisingly easy to do.

As the latest RBNZ deposit figures for May showed, in that month we snuck away the most ($417 million) in term deposits since May of last year.

But that's not the even the half of it.

As at the end of May the total amount in deposits (including term deposits, savings and transaction accounts) stood at $194.046 billion, up by $1.363 billion in the month. This gave an annual growth in the total amount held in deposits of 7.6%, which was the highest annual growth rate since late 2017.

But that's not half of it either. In reality a vast portion of that growth was in just three months.

In the months from March to May a massive $9.56 billion (which loosely equates to around $1900 for every man, woman and child in the country) was added to deposit balances. Ker-ching.

Put another way the $9.56 billion rise in total deposits is a 5% increase in the total. And put another way again, this means deposits over those three months were growing at an annualised rate of 20%. So far as I can see, this would appear to be the fastest pace of increase in a three month period we've seen since the RBNZ started publishing such information in the late 1990s. Certainly in dollar terms the $9.56 billion increase in that three months is much the most for a three month period.

A big turnaround

And it all followed a time in which savings had been drying up noticeably.

In fact earlier this year the rates of increases in deposits were languishing at nine-year lows, with the annual rate of increase getting down to as low as just 4.3% in February - just before the March, April and May spike.

The low rates of increase in deposits were at that stage potentially a problem for the banks, as they were required by the RBNZ to maintain fairly high rates of deposits as part of their overall funding (the core funding ratio). In late March the RBNZ considerably relaxed these requirements giving the banks much more freedom to source funds from elsewhere, including overseas.

With deposits having poured into the banks since, this would seemingly put the banks in a pretty happy place in terms of their funding. It's probably worth bearing that in mind when dealing with them.

The question is when and if all this extra money Kiwis have been stashing will get spent. Saving is 'sensible' but it doesn't fire up an economy.

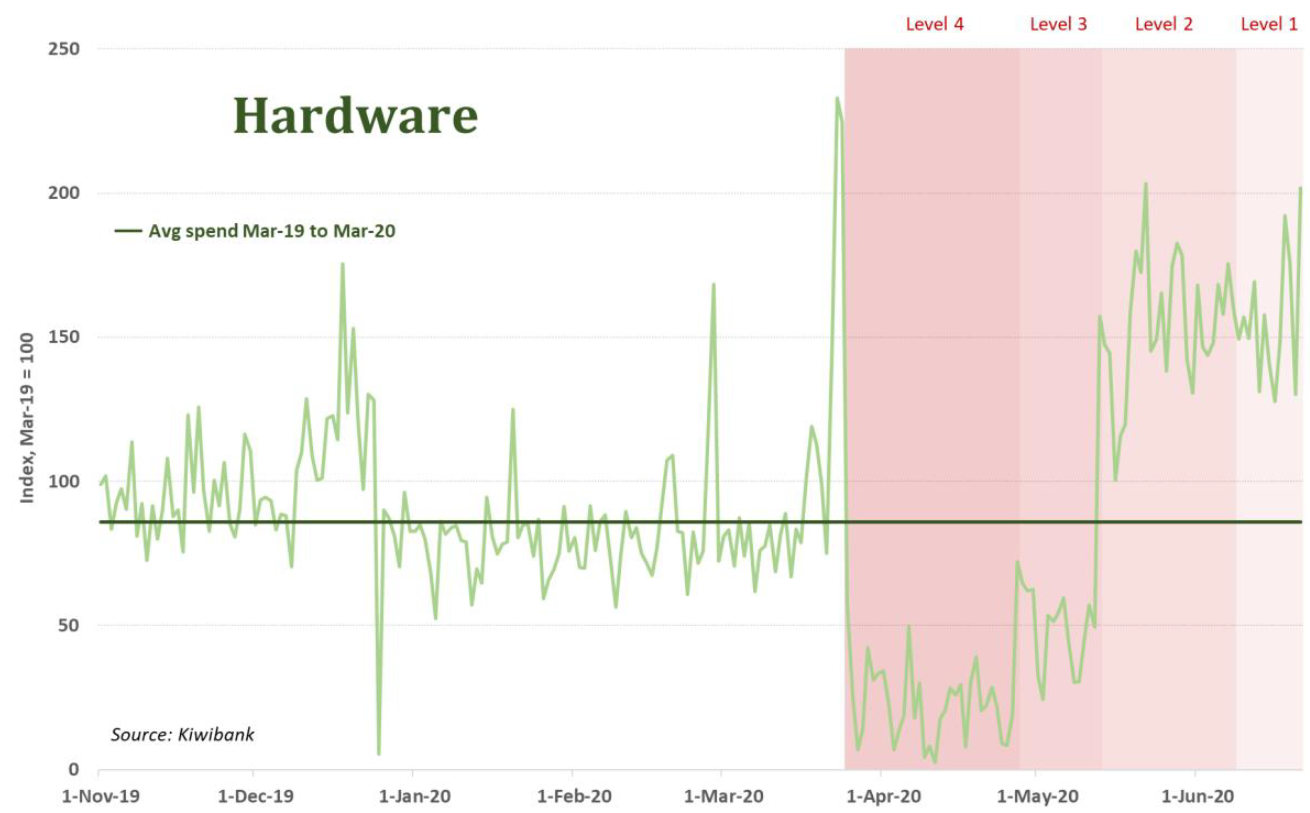

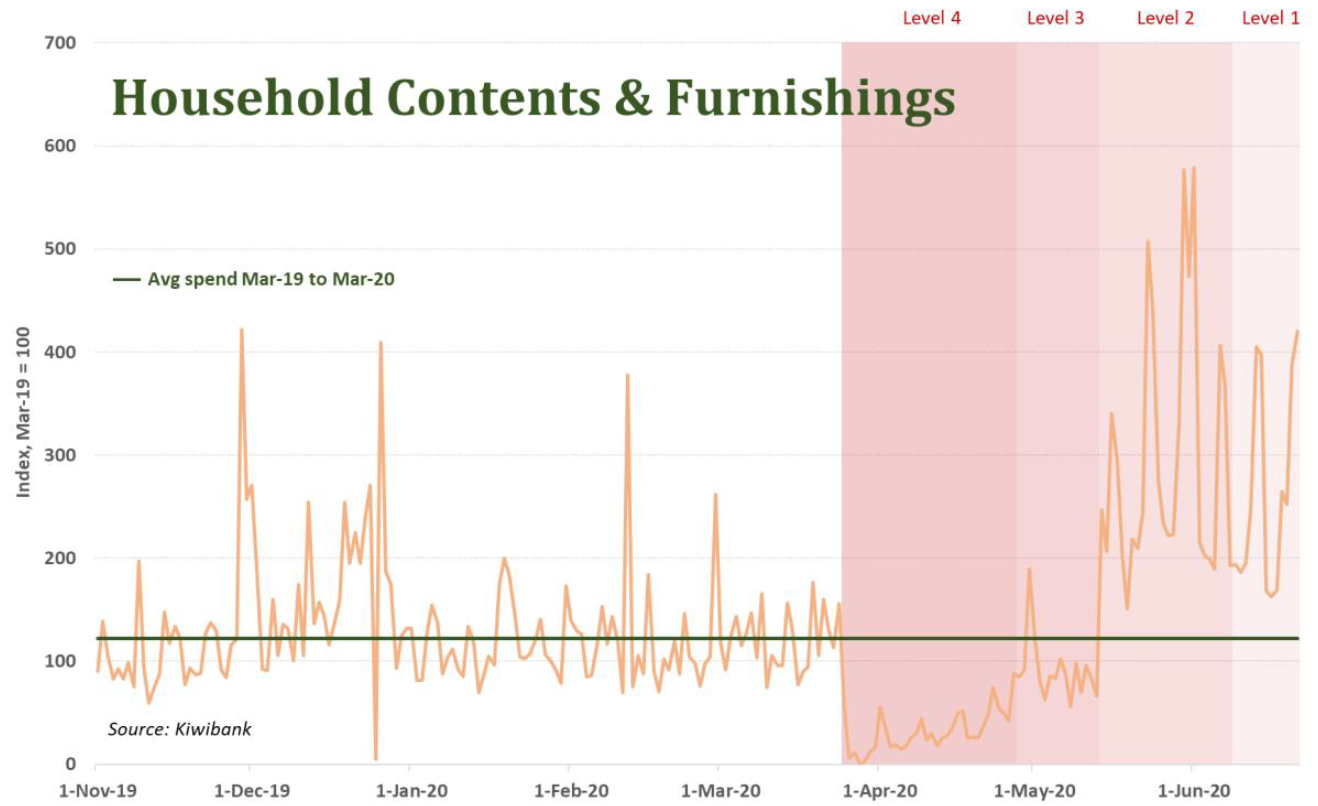

The economics team at Kiwibank have been putting together some interesting data based on the recent card spending of Kiwibank customers.

As the Kiwibank economists say once out of lockdown there was a clear release of some pent up demand (and spending of lockdown savings).

"We took a good, hard, LONG, look at our backyards, and decided we needed more. More of us ordered pools, fixed fences, laid pavers, and even bought pets. I guess we’re better prepared for more (forced) time at home."

Here's a couple of the accompanying graphs I found most interesting:

As the economists put it: "Out of lockdown, we got handy with a hammer. DIY is up with a surge in home renovations. And with our overseas trip now cancelled, we could do with a new pool, and couch."

The economists then pose the question, which is the question of this article. Can the spend up continue?

"We’re still wary of the damage done and the impact to activity," they say.

"The drawbridge into NZ won’t be let down anytime soon. Greater domestic tourism goes some way. But foreign tourism is a hard void to fill. And overshadowing all of this, is the rise in unemployment. The rise in unemployment may dampen future spending, and investment."

Well, exactly.

I do think we've done a great job, both of holding the pandemic in check (fingers still crossed) and in managing our finances during, let's face it a most turbulent and worrying time.

What happens next is vital

We are in good shape right now, but the next month or two will be crucial.

With the wage subsidy now coming off for many businesses and workers, now is the time when we'll get a clearer impression of just how many people are going to lose jobs.

If the next wave of job losses is particularly heavy then that will knock confidence and spending.

Then of course, in one of those not-nice feedback loops, if businesses (particularly retail and hospitality, perhaps) that have recently re-opened find that the spending dries up then they may well have to look subsequently at lay-offs, or even closing.

The reality is, it would be in the best interests of all of us if we do keep (within reason of course) spending. But that's easier said than done if you are worried about losing your job.

So, as I say, I think the next month or two will be very crucial. I'm certainly going to be keeping a close eye on the saving/spending figures for June and July as they become available.

Much as it is with the pandemic itself, it's a case of fingers crossed and maybe it all doesn't have to be as bad as we feared. A lot depends on us.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

127 Comments

It's game theory now. People will act in accordance of their beliefs of what other people will do, and of what the future holds. I thought the value of the NZD would go down, but so far I’ve been dead wrong. Maybe all my other assumptions are wrong too. Like the housing market declining to a low sometime around 2022. Or the NZ economy being in big trouble because of the 17 or so billion of lost international tourism dollars. I’ve got no hesitation to buy stuff because I think the economy will be force fed so much fiscal and monetary medicine that a tipping point could be reached where the desire to hoard cash turns into the opposite. At the moment my inclination is to get out of dollars into perhaps silver, mining stocks, or inflation linked government bonds.

Interesting. I wonder how many of us are thinking about the economy as divorced from our own situations. I’m salaried and have had no reduction in income and redundancy is not on the horizon (despite my expectation I would be likely be gone in June and definitely gone by September). Saving during the lockdown was close to 90% of income. I have not spent much of that on discretionary items to date, but the taps are opening, not because I have some sense of greater public good, but because money in the bank is boring. When I have spent, I have found prices unchanged and/or supply issues. I am paranoid about my savings losing value so have been moving in Physical cash, Kiwi bonds, TDs, Gold Coins, Rolex SS watches. I would prefer a 2 bed brick and tile in the Eastern Bays but am not seeing the drops in prices I expected. Maybe that’s all of our problem, in that we say what we would like to happen while ignoring the fact that it needs someone on the other side to cough up a property etc and maybe the pressure isn’t there.

Interesting to hear of other people in a similar position with similar thoughts. I also thought my job would be gone, but it isn't, and luckily my beautiful partner is a lawyer so that also takes the financial pressure off. I also reluctantly moved into cash, partly because I disgorged my P2P lending and stocks in late Feb. I don't have a rolex or gold coins but a little gold bullion acquired years ago. My partner and I want a specific type of 1980's build overlooking Rangitoto and ideally no more than a 5 min walk to La Forchette. As far as I can tell that market has been going down or sideways since the end of 2016 so I'm happy to be a spectator right now. To be honest so many stars would have to align for us to buy that house that I don't think it's likely. Both of us would have to get good jobs in NZ, and the Chinese would have to stay out of the market so that the price could decline a little further. Also the tsunami of QE that global central banks have unleashed will surely wash over that upper quartile market eventually, and if we haven't purchased by then... well, we're out, and we'll live our lives somewhere else. That's okay though. We’re both quite fortunate and will be happy wherever we are.

Some Rolexes e.g. Submariners, GMT, Daytona are akin to cash, anywhere in the World. The only thing is that you can’t wear them much or you risk devaluing them. Easy to walk through Customs wearing $20,000 on your wrist. Try that with cash. Gold is more difficult. I went with Royal Australian Mint coins which are sealed with serial numbers. Big margins to sell. I’ll likely leave them to the Children. Prices in the Bays are still close to 2017 CV so they’ve really gone nowhere for three years, but you are still looking at $2 million plus for a detached house. I’m intrigued what is so special about 1980s builds. La Forchette is great, as is Mushashi. If you lose your partner, find a new one at Mortons, apparently. Ugh.

ha ha I've heard from two people now that place is a Cougar bar. Interesting about the watches. Re gold, my understanding is spot +/- 3% on gold bullion if it's a decent amount. I mean 6% is still a pretty large round trip expense, but perhaps if you hold it for a long enough time it's not so bad.

Buying price for 1oz of Gold is NZD 2,592. 1oz Royal Australian Mint coin costs NZD 2,924. So the margin in and out is a colossal 11.35%. 1oz bullion from a local refinery is NZD 2,830 giving an in and out margin of 8.4% You would have to be mad to put significant funds in physical Gold. Silver Coin margins are even worse. Rolexes have a similar margin and you risk the sale to LVMH ramping up production because SS Sports models are sold at 133% of Authorised Dealer prices but I like the ease of crossing borders with them. Of course that’s apocalyptic scenario thinking. You have me craving a Crepe Citron now. Damn it.

You need to give the local refiners a phone call and get a good rate on 1 kg or more. A 6% round trip sounds like a lot but if you think about other investments it's not uncommon to get charged 0.5% pa on ETFs. Stocks in NZ are worse with high brokerage and custodial fees. Managed funds even worse. Just running some numbers on a spreadsheet, if you assume a 6% round trip on gold and compare to another investment with an annualised fees of 0.5% and assume a growth rate of 7% pa for both investments then the breakeven point is about 12 to 13 years. Gold always overtakes the annualised fee investments on a long enough time horizon. Of course it's not really an "investment" it's money, but not for everyone because there's opportunity cost of not being levered into property, there's taxes, there's manipulation of the market, confiscation risk, storage costs etc.

Good point. BTW: Someone got to a three year old Submariner before I could see in person. I hope I didn't shoot myself in the foot by mentioning it here.

This is how I understand it using generalities and the term token instead of dollar. Initially physical things and service have a current value in tokens. An increase in the number of tokens issued without increasing anything physical eventually drives the value in tokens up unless physical utility declines. Those holding unused tokens lose out because acquiring physical things requires more tokens than before. Owned physical things have more token value but no more physical utility. Those earning tokens for service lose out unless they can get more tokens per service. Inter country token values change to reflect the same.

The biggest losers are holders of tokens.

The biggest gainers are those who percentage clip the token exchanges for physical things and service.

The biggest puzzle is why people accumulate more tokens hoping to store value.

Exactly. The value the token has is us accepting it for goods and services we provide in anticipation of using them later on for other goods and services. If lots of tokens are created with the same supply of goods and services and we try to use them too quickly then the price of those in terms of tokens goes up. As a current holder of tokens exceeding my current consumption needs I’m very nervous.

Most Imortant data to watchout is UNEMPLOYMENT data.

Also how much more government is going for QE for varuous subsidiea.

According to local car dealers, builders & real estate agents, people are out spending pretty well.

As you say, the $10-15k overseas holiday is off, the term deposits are on .5%, who knows what other global disasters may be in the pipeline - people may as well enjoy their fragile lives right now - is the thinking.

The new post election government is sure to keep printing and helicoptering money as long as it takes to keep the economy propped up.

Do you mean eat drink and be merry for tomorrow we die. NZ needs an anti-fragile economy, not one based on extend and pretend. While I don't think things are going to be as bad as some predict, for some there is going to be pain.

Odd...car dealer staff I know are saying its very, very slow. New cars, not second hand.

The Future is in our wallet

Wrong

The Future is in government debt / wallet

Which is also our future bigger wallet

The govt has no wallet. It gets money of us.

Exactly the government is us

The paradox of thrift. I always found this quite amusing in an age when young people spending for avocado on toast and iPhones has been seen as extravagant. But things have become a lot more serious.

Wait for the headlines in a few months

"Greedy millennials aren't spending at cafes! Millennials are destroying our local economy"

Turns out the avocado on toast and flat whites was quite useful!

Everyone always picks on the millennials but we are the reason for change eg WFH, work/life balance etc in this competitive environment. We (generally) are also why work places can be so efficient...creating tools/automating everything. We love learning new technologies and continuous improvement. It is seriously painful to watch someone print and type data into a spreadsheet.

Looking forward to the backlash

Have just saved a boomer colleague from 4 hours of 'hard work' a week with a simple vlookup. He couldn't believe it could be done so simply.. I couldn't believe he'd never looked for a better way to do things!

It seriously kills me... read my comment below re nepotism. It's not just disruptive tech that is going to change workplaces/efficiency also. Its time that we start to have a more productive economy rather than relying on primary non value added industries eg dairy, farming etc (which is also dependent on factors like uncontrollable factors like weather) etc

And they'd rant at those millenials for that while expecting to live off the debt that will be passed to those same younger folk. Generations living off money they haven't earned but that has been transferred to them via poor governance and central banking.

"The willingness or otherwise of Kiwis to keep spending in coming months will be a key factor in how well our economy recovers."

And the governor of the RBNZ said similarly in 2019, "The future of the banks in NZ depends on the willingness of the NZ public to step up and borrow."

So, if we don't either spend up big with our savings or borrow like mad, what's going to happen??

I was gonna buy and leverage up a House, but someone beat me to it.

I was gonna put all my eggs in one basket, but it cracked under the strain.

I was gonna buy Air New Zealand shares, but they do not give fly-buys anymore and the Taxpayers are in short supply too.

I was gonna buy a farm in Hawkes Bay and go for broke, but the rains came back.

I was gonna buy a water feature in Awkland, but Waikato splashed that idea, so I decided to bottle it and send it to China, for free.

I was gonna support the Government with a few dollars, but they borrowed up to the hilt, so no sweat, no need, so why should I work my butt off paying tribute to Society.

I was gonna pay last years taxes due, but the Banks stole it cos they wanted it back with interest and I was not interested in that, even if tax deductible, business wise. All work and no play, makes Shane Jones a spendthrift, without it.

I was gonna borrow and buy some land and leverage up an air-b-n-b, but not a capital idea anymore as I live in Paradise, without Tourism, so it ain't all bad.

Go figure.

those savings will soon start to evaporate at the end of the year when the gravy train hits the buffers,no double winter energy payment,end of mortgage holidays,wage subsidies.new govt will turn the tap off till next election year.

With deposits having poured into the banks since, this would seemingly put the banks in a pretty happy place in terms of their funding. It's probably worth bearing that in mind when dealing with them.

From where did they pour?

Collectively, bank deposits were down for the month of May 2020, same as total balance sheet factors -view RBNZ S10.

Maybe they "poured" in from retail stock trades as the market tanked and now they are pouring back out as the market recovers. I'm sure all here are aware of the massive increase in retail trade volume over the period March to May. It would be interesting to see any correlation between the two - retail stock trades vs bank deposit levels. As you posit Audaxes - From where did they pour?

Retail share sale proceeds which find themselves in bank transaction accounts are offset by depleted buyer's bank transaction account balances.

Fundamentally, banks are building a store of QE derived interest bearing reserve assets at the RBNZ and letting the private banking system wither. Take note of section Assets ($M) 2. Deposits (with depository institutions) in this link.

Yeah. I guess I overlooked that first point. That link certainly shows some interesting trends. The question then remains - where'd all the cash come from?? People/businesses stashing the wage subsidy?

We are missing many transactions in the sequence of real world events when sanitised national bank balance sheets are presented to the public. A wild guess would be government transfer payments finding there way into citizen bank accounts after new government debt has been monetised by banks. Banks keep the bonds until the RBNZ buys them, the government is in receipt of newly created deposits to spend into the system. And we must not forget significant T bill issuance which is not part of QE.

Government spending creates new currency, the government never spends in any other manner, taxation and borrowing are never used for financing the governments spending, it is the sovereign issuer of the NZ Dollar, that is where our currency comes from. Economist Dr Steven Hail acknowledges NZ as a sovereign currency issuer here.

https://independentaustralia.net/politics/politics-display/modern-monet…

What's this exercise undertaking if not raising funds to underwrite government deficit spending?

- Final orderbook at NZ$14.278b at the final level

PRICED - NEW ZEALAND GOVERNMENT NZ$7b MAY 2024 NOMINAL {NZ} ***

Issuer: Her Majesty the Queen in right of New Zealand

Issuer Rating: Moody's Aaa (Stbl) | S&P AA+ (Pos) | Fitch AA+ (Stbl)

Instrument: New Zealand Government Bonds ("NZGB")

Amount: NZ$7 billion

ISIN: NZGOVDT524C5

Launch: 15 June 2020

Pricing: 16 June 2020

Settle: 23 June 2020 (T+5)

Maturity: 15 May 2024

Coupon: 0.50% s.a

Margin: NZGB 5.5% April 2023 (mid) +9bps

(NZGB 5.5% April 2023 - FIS01 on Reuters, ICNG01 on Bberg)

Yield: 0.4275% s.a.

Price: 100.2796388105% plus 39 days accrued (0.0529891304%)

Denominations: NZ$1 million (Primary subscriptions)

Selling Restrictions: Offshore Selling Restrictions (refer IM)

Bookrunners: ANZ (B&D) | DB | JPM | WBC

Embargo: There will be no 15 May 2024 nominal bonds offered for tender prior to September 2020

Documentation: IM (25 March 2020)

https://debtmanagement.treasury.govt.nz/sites/default/files/information…

Product Disclosure Statement (25 March 2020) (where used in compliance with the Financial Markets Conduct

Act 2013, available on request. See section 6 of the IM)

Other: NZClear/Clearstream/Euroclear; NZ law; Not listed.

And the market wanted more

Economist Prof Bill Mitchell explains here why they do it.

Part one. http://bilbo.economicoutlook.net/blog/?p=45106

Part two. http://bilbo.economicoutlook.net/blog/?p=45108

All these Macro thingies are meaningless to the Joe Blogg. He is interested in his income, meeting expenses, and saving for a house or holiday. If these Macros help in his Micros then good. If Macros go to help only the One Percenters that is another Epic Scam on the population. Repeat of what happened after GFC, though the recovery helped Joe Blogg, but not as much as the One Percenter.

Macro understandings are important when the following statement remains unchallenged.

With deposits having poured into the banks since, this would seemingly put the banks in a pretty happy place in terms of their funding.

The banks are in need of balance sheet liability items (deposits) to balance the reserve assets claimed on the RBNZ balance sheet declared in section 7. Liquidity management operations as Net Large Scale Asset Purchases here.

I claim a segment government transfer payments gained from swapping bonds for bank deposits is the key to this necessary balancing act- see my comments above..

The money that the government spends into the economy creates a spending chain, it doesn't just stay with the initial recipient. It changes hands many times until most of it will have been taxed back again, a percentage will be saved or used to reduce debt. An explanation here.

http://www.matchesinthedark.uk/spending-chains-sankey-diagrams/

Another very interesting link, however what happens when the money is non taxable to start with (as in the case of the MSD payments) the entire lot is placed in the share market (at minimal (.2% ) commission) and the seller of the shares does the same thing (reinvests) at the same low commission rate and the process repeats ad infinitum. There is no CGT. I get that eventually the Govt gets the the money back but it may take decades or a change in Tax policy (an introduction of CGT). In my example, would it not take over 1500 transactions to get the initial sum back? It might not come back at all if the investor decides to leave the country permanently.

I would gladly spend the Helicopter Money. Waiting for it to hit my bank account,thanks.

You do understand you will have to pay it back through taxes?

Interesting theory, wheres the evidence?

Taxes are there always. If I can have some free money to ease my way to paying them, why not ?

People across the globe have grown up with 'borrow and spend' as the norm for 40 years or more. It's pretty much the only System we have known - and it's worked! So why change it, is the thinking? "Let's get back to normal as soon as possible!"

And in that hope might lie the trap.

Recent history has been the outlier; we've all be fortunate to live in the economic environment that we have. It's been changing though, and we didn't notice. It suited us to not notice.

If we are brave enough to go outside and look around us, we know it's not working well.

And that's why we are all saving like mad, and not spending - we know 'something nasty' is coming and the last 6 months has been a sharp reminder of what it might look like.

Yes, change is coming. But to what we had on 1st January 2020? Let's hope not, because we can only cannibalise the next generations for so long until there is no one left to eat.

I will not be spending a penny over what I need for survival. If the rest of the world just accepts the virus and lives with it then what are we going to do? We could be prolonging the inevitable which will cause long term pain for us. Essentially, our economy will be lapped before we even leave the starting blocks.

Spending patterns will not be uniform and the details are yet to be revealed. Sample questions:

1) Will all the people who learned to cook during lock-down continue to do so?

2) Will the trickle of Kiwi ex-pat COVID refugees become a flood and how long will it last? This could be our new version of the population Ponzi scheme.

A very good piece David.

"from March to May a massive $9.56 billion was added to deposit balances."

That matches both the date and amount of the first wage subsidy scheme pretty closely, coincidence? Did possibly many not really need these subsidies?

I think you may have it in one Yvil. Unfortunately (or fortunately, depending on how you look at it) the criteria was so wide and easy to meet, it was a truly "gift horse" moment.

The subsidy was paid in advance as a lump sum. So no surprise that we have a jump in cash deposits. It will be depleted as it is spent over the subsidy period.

Sectoral Balances tell us that the government sector and the private sector are a mirror image of each other. Households can only increase their savings and reduce debt when the government is running deficits. An explanation here.

http://heteconomist.com/short-simple-15-the-sectoral-balances-identity/

The choice for this year and the next few is as much about thinking on which product you spend your money as much as actually spending it.

Look at where the products you are buying are made and make the choice to buy from liberal democracies.

Supporting totalitarian dictatorships is yesterday's trade.

Laudable sentiment Glitzy but with the current dysfunction regarding labeling laws that choice is very difficult to make. I'm not sure many people have the time or inclination to do that sort of research.

Yes, one often reads on food labels - 'made from local and IMPORTED ingredients'..

Correct! and that's just food. The other day a friend was doing some work on his newish Harley. He opened the instrument panel and found... "made in China". The bike had been imported new from the US. My point is, it's pretty much impossible to avoid buying anything that doesn't have some links to regimes we don't agree with.

l agree with you. It's harder and harder to do because firms are removing country of origin on products where labelling is not legally required (like food and clothes).

But it is possible, only one country is removing its name from product made in that country. And that's the PRC.

Haha, that's probably because PRC is making all the components and outsourcing the assembly hence it's no longer "Product of PRC" I think you'll find most of the processing chips in today's electronics are made in China. In fact Wuhan is a major industrial area which produces a lot of electronic components. China is also the world's largest supplier of LED products and they're pretty big in battery tech as well. The horse has bolted to be replaced by a big bad tempered dragon.

Bugger what are the boomers gonna ride now.....Hondas?

You (Toyota) Wish...

Need the locally manufactured price to come down then, but I agree with you.

We got a flyer in the mail today... reject the ccp.

From our place I can tell you that discretionary spending has more than halved (from March to July inclusive). Okay, we're a bit older than some but there are some fundamental thinking shifts inside of this. I'm sorry to inform you that if the NZ economy is relying on us to keep our spending habits up, they may be disappointed. And we don't think we're the only ones. A lot of boomers may be here or hereabouts, as they review their sinking retirement funds. It's up to you younger (<55yo) ones now. Good luck & God bless.

Yes. We are a consumer economy and the GDP composition is largely about how individuals / h'holds spend on goods & services (approx 65%). Now what I think is interesting is that COZVID-19 exposes what NZ is really all about. It relies on many people to spend up to or above their ability to earn for the economy to be running optimally. The cost of goods and services is relatively expensive compared to other countries and relative to income.

Things are probably a lot worse than people as individuals subjectively understand at this point. The extent to which will become more obvious over time.

Great comment. Imho the issue is that the mainstream has difficulties thinking long-term. Which is 30 years + in the mind of an investor. But the majority already has trouble with envisioning life two years down the line.

If it's up to the younger ones, maybe it's time to consider whether NZ wages and NZ expenses are going to pass muster.

NZ wages certainly won't! Remember NZ is actually considered a "low wage economy" Unfortunately to have higher wages we need higher skills base, for that we need better education systems. I was gobsmacked when I read the other day that learning how to balance a chequebook and getting a driver's Licence actually counted as NCEA credits.. really???

Cheque-Book? LMFAO, 1762 called and want their financial innovation back.

haha, ok ok a slip.. but you get my point

How to balance a cheque book - they are going to have to up date that now as a lot of places no longer take cheques. A friend owns a service business that has govt owned agencies supplying same/similar services, in the same place. Their business has boomed since the govt agencies have stopped taking cheques, to the point they may need to employ a 0.75FTE.

I rent. I have no interest in buying property in NZ at the current prices given the properties on offer.

I have no interest in buying new furniture for a rental. I have no interest in the lame boomer bars here in ChCh.

So yeah, just convert NZD to Bitcoin, Gold, Silver and selected equities.

Unfortunately NZ has blocked many younger people form having a stake in NZ. So yeah, quite a few of us are actively checking out of the NZ economy into the digital economy.

Act was looking hopeful, unfortunately their coalition partner National are fuddy duddies, especially on younger person industries like cannabis.

Labour are pretty useless, etc, etc .. the idea of investing in NZ is pretty much pathetic, unless your on the government tit or benefiting from million dollar rot boxes.

So NO THANKS. The NZ government can do what they want .. younger people like myself have already checked into the new global crypto banking system and are laughing at the rest of you.

It's as if your trying to communicate via Morse code.

Unfortunately NZ has blocked many younger people form having a stake in NZ. So yeah, quite a few of us are actively checking out of the NZ economy into the digital economy

I recommend watching this interview with Mike Novogratz and Raoul Pal (Mike Novogratz and Raoul Pal on 'the Single Greatest Brand' of the Last 10 Years). Now if you don't have time, you can watch from 20:00 about how younger people are pretty much screwed in terms of investing / saving in traditional asset classes. Your attitudes are very well summed up and elaborated on by Mike and Raoul (ironically both of whom made their money from the institutional investing world).

Yes I agree - we have created an 'everything bubble' - shares, property, bonds....and the only thing keeping them all inflated now is QE. But I just think its giong to keep making our problems worse down track. Yields are getting lower and lower and our capacity to push capital prices higher is falling now we're pretty much at zero in terms of discount/interest rates.

Now what....? Is Dalio right and we have a lost decade ahead of us?

A lost decade? Right

And then what?

What magical fix appears at this point?

Good for you! What they really fear is that you and your peers all up and go to Oz or elsewhere. Then they have nobody to charge rip off rents to, they have nobody to work for them for minimum wage and they have nobody to tax to give them a happy and rich retirement. The majority of well off kiwis were either born into it, were lucky through rising house prices or worked in a country that pays a decent wage and then come back rich. Do yourself a favour and emigrate, free yourself from their clutches.

I'm just speculating, but I think emigration will become more difficult going forward. Australia perhaps for NZ citizens. But important to remember that the Aussie is not necessarily the land of milk and honey it once was. All the issues hanging over NZ exist in Australia too.

Agreed. In some cases more so

Any smart young kiwi has invested in mobility in the years prior to this mess. If you are now starting with your preparations, it is frankly too late. The exit gates have closed.

Spoken like a true shallow self centred millennial. You'll be pretty keen on the NZ Govt to pay for your slot in the retirement village when you get there. You say you have been blocked from a stake in NZ, the problem is you and your digitally focussed mates want everything NOW and like petulant spoilt children scream and throw a tantrum when you don't get it. Ever heard of the Hare and Tortoise fable?? Thinking of which.. heard of Cryptopia? Their clients aren't laughing too much.

Spoken like a true shallow self centred millennial. You'll be pretty keen on the NZ Govt to pay for your slot in the retirement village when you get there. You say you have been blocked from a stake in NZ, the problem is you and your digitally focussed mates want everything NOW and like petulant spoilt children scream and throw a tantrum when you don't get it. Ever heard of the Hare and Tortoise fable?? Thinking of which.. heard of Cryptopia? Their clients aren't laughing too much.

Strawman.

No, just my honest opinion of Brando's tone

Oh really? Look at your comment "the problem is you and your digitally focussed mates want everything NOW'.

What does that mean? That somehow older generations posess great powers of patience and that the millennials should just suck it up and take on ridiculous debt levels to buy assets from the boomers?

Why would they do that when there are potentially other asset classes better suited to their digital worlds that don't require the same level of debt and manipulation?

No JC, what it means is the older generations knew/know that you work your way up in measured incremental steps and they are resigned to that reality and have an end goal many years down the track. They didn't buy a house costing 10x their gross salary and moan about the payments. They bought a modest home @ 3-5X salary (often needing improvements) and then used that to advance up the value scale, bit by bit, home by home. The mere fact that Brando is advocating Bitcoin (< 1/2 it's value of 12-18 mnths ago) Gold (at peak value currently) and "selected equities" (hmmm I wonder which ones} shows me an underlying tone of short termism and has nothing to do with digitalisation

No JC, what it means is the older generations knew/know that you work your way up in measured incremental steps and they are resigned to that reality and have an end goal many years down the track.

OK, so you suggest that the older generations know that buying instruments such as ETFs on a regular basis will meet some goal. It's some kind of universal truth. Well that may be so, but it might not be so. The experience of the boomers doesn't necessarily represent the future nor are the current monetary / financal systems some kind of fixed paradigm.

The mere fact that Brando is advocating Bitcoin (< 1/2 it's value of 12-18 mnths ago) Gold (at peak value currently) and "selected equities"

Once again, what does that mean? That you know something about the future that millennials / yonger generations don't?

has nothing to do with digitalisation

That depends on what you understand as 'digitalization'. IMO, it has everything to do with Bitcoin as it exists within the digital world and is the application of 'digital' technology into society.

Maate.. where did I mention ETF's? I was specifically referring to houses. As far as the Bitcoin statement goes it was about short termism. In fact buying Bitcoin (or any other crypto) doesn't require any sense of digitalisation at all.. just a trading account and a desire to speculate. Gold is hardly a digital asset nor are "selected equities", again just a trading account and a desire to speculate is all that is required. Remember Mr Brando lumped them all in together not me. If he'd said "mining" crypto then that would be different but he didn't.

Maate.. where did I mention ETF's? I was specifically referring to houses. As far as the Bitcoin statement goes it was about short termism. In fact buying Bitcoin (or any other crypto) doesn't require any sense of digitalisation at all.. just a trading account and a desire to speculate. Gold is hardly a digital asset nor are "selected equities", again just a trading account and a desire to speculate is all that is required. Remember Mr Brando lumped them all in together not me. If he'd said "mining" crypto then that would be different but he didn't..

Looks one big troll post to me.

There are no homes at 3-4x salary, that’s the whole f’ing point. There are no regular raises. It’s a different world.

Sounds all well and good until you look at some stats mate.

1990 average house price - $115k, average income - $29,393. House/income ratio 3.9 (source:stats NZ)

2020 average house price - $620k, average income - $53,040. House/income ratio 11.7 (source:statsNZ + REINZ)

Rug has well and truly been pulled out under the younger generations and acting like it isn't an issue is ignorant and exacerbates the problem.

As Simon Bridges termed in a moment of startling lack of self awareness (in fairness, not that startling): "mortgaging our children and grandchildren's future" to live up large now. Generational self-absorption.

There are some really important factors you are ignoring. It might be a good strategy to buy a home that (say) is not really suitable for a family if you are in your 20's and have the time to work your way up before having kids, and you expect salary progression. But push the timeline back 5-10 years (which a combination of lots of jobs with good salaries requiring degrees which they didn't in the past, student loans to payback, and higher deposits to save), then that no longer makes much sense. And if you are (say) 35 when you are buying your first house, large increases in salary are unlikely - the most rapid salary increases tend to happen in the early parts of your career. If you are 35 and are buying a house that will suit for the next five years (which is sensible, as it costs money to move), and you're unlikely to be earning a lot more in future, then it's not sensible to buy something that you will need to 'trade up' from. You are also unlikely to be able to afford much in the way of improvements, given that a two salary family who wants kids is likely to spend a significant amount of time in the next five years as a one salary family.

What incentives are in place for millennials to work hard? Wages are relatively low in NZ and our housing is by any measure some of the most expensive in the world.

And if millennials are 'self centred' as you put it, I question where they learned that behaviour from? They obviously just didn't make it up as children usually observe/copy their parents behaviour/s.

Well IO, it's just my theory but the rise in self entitled behaviour seemed to coincide with the rise in social media use by said generation. It also coincided with the parenting practices undertaken where children were treated not as children but as "miniature adults" with all the rights but none of the responsibilities.There also seemed to be few boundaries and even fewer ramifications if those boundaries were breached. When I was a child if I wanted something I worked and saved for it and thus valued the item. An ethos that seems lost on some of our current crop of 20-30 yr olds

Good points - but again what about the incentives for them? Many I have had work for me are much more proficient than those the generations above them - especially when it comes to technology! They worked smarter, not harder. Often they're lacking leadership from the generations before them in my view. Responsibility for them is saving the world from global warming or any other 'making a difference' type cause - which appears to grind with the generations above them who often are even in denial to some of the preceding issues.

If you lead them well they're great - but if you bully them/abuse them/belittle what is to them important, or put them down (per you comment) they turn into exactly what you're describing. Walking the higher path and setting the example seems to work well with them. Just my experience...

All true IO. They are good at Tech no doubt about that, however, when it comes to non tech jobs they can be very averse to putting in a fair days graft. Not all it is true, but a fair percentage nevertheless. In my field (Heavy Industry Control Systems) many of them need a good swift revup. Often the "working smarter" actually translates to doing as little as possible to "tick the box"and then being affronted and feeling aggrieved when they get the aforementioned rev.

To be fair though Mr Brando did touch a nerve so perhaps I was a little reactive

Can certainly understand where you’re coming from and have had some similar experiences - perhaps more so Gen Z though as opposed to millennials. But also with a few experiences implementing tech projects, the young 20’s something we’re often 5x more proficient (no jokes as we measured the KPI’s) than some of those 45+ doing the same coding/software interface type work. They made the older guys/girls look quite incompetent and unemployable. So I guess I’d be cautious in calling one generation lazy/unproductive as another as I’ve witnessed the opposite in areas. Times are changing and what is useful into the world we’re heading into could look very different to the past.

Yeah. in your line of business I'm sure the younger guys/gals run rings around the more "mature" ones. You're quite right in saying times are changing and that is natural progression. I think what's been lost in this discourse is I said "typical" not "all". My mistake was couching the "typical" as a stereotype when in fact I meant the individual "typical". Mr Brando, in my humble opinion, fitted the latter

Completely agree with IO. 'Work smarter, not harder'. Hook- we value our time and want to enjoy all the enriching experiences in life during our precious free time. I'm not going to sit there for 5 hours when I can automate the job in 1 hour and use my free time for learning... Just because something is tradition, doesnt mean you shouldnt question the WHY.

I work in wealth management and the productivity rate of young millennials compared to their older counter parts is far higher. Hence why I've seen a lot of redundancies in this area, a lot of the older ones seem to come from exisiting connections whereas now, there seems less nepotism in this industry. Sink or swim..

Millennials have had to wait and continue to wait much longer than either Boomer or Gen X had to to buy a house, they will have to wait much longer to retire. Its a bitter, nasty myth that millennials are impatient. Millennials even have a higher saving rate than boomers ever did.

Millennials have no great reason to wait to purchase RE. It's their desire to buy in the "right" neighborhood/development that holds them back. There are many places within a 45-60 min drive from most main centres (about the same as you'd spend on a gridlocked motorway) that are easily attainable nowadays with the various express ways & RoNs. This is a truth in pretty much any area of the country. It is true though that they'll be waiting a bit longer to retire but then again maybe not. Some commentators are saying the age must go up, but others are saying NZS is totally sustainable through to 2050 and beyond.

I'm sorry but this is not what the data shows. It's another myth that millennial's won't buy entry level properties. They would and they do. It still takes them longer to raise the deposit because of their comparatively lower wages and the comparatively higher house prices than either Gen X of Boomers experienced at the same age.

And lower interest rate on saving for a deposit

This is absolute nonsense. Check out the average wage of the younger cohorts, and explain how exactly they're going to buy a 'doer-upper' in Manurewa or whatever you're imagining. Explain what budgeting magic trick they're going to pull off. 70% of FHBs need help from their parents to buy a place. Generational class mobility is dead.

Dp

"I rent. I have no interest in buying property in NZ at the current prices given the properties on offer... here in ChCh."

WTF? Where's TM2 when you need him to respond to that statement

He's probably busy doing more overtime to try and counter his property losses.

Zack, it is all fine to be all digital, fact is that NZ is one of the most boring countries to live in for young people and post-Covid it is going to be akin to a deserted island in the eyes of anyone under 35. Better invest in an exit-strategy fast or forever (yes, forever) hold your peace.

If households want to repair balance sheets and are cautious then government needs to spend to fill the spending gap. Not rocket science.

Saving is what we need to do. Stop buying c##p and create a pool of savings which can the be lent to the productive sector. Not spend and print.

There is no guarantee that an increase in household savings will result in an investment boom. Far from it. Increased savings translates into a loss of income for firms. When sales drop businesses do not invest. They see inventories build (the bad form of investment) and become pessimistic. Savings and Investment equate only in that sense. Conversely when businesses encounter a booming economy short on labour and burgeoning sales they invest in capital which provides income which eventually leaks out as new savings. The investment creates the income from which savings are made. There is no scarcity of money for the productive sector due to poor saving by households. Loans create new deposits. There is a lack of demand for investment due to depressed aggregate demand. Why would you invest if households were no longer going to buy your products due to their desired saving?

Covid has made many rethink their ways of life, lifestyle, saving and spending habits. The breather given by the lockdown has given many the chance to see more money in their bank accounts and the possibility of living a happy life without spending every cent they earn immediately. And that those designer coffees for $7 a cup is totally a waste of money and time. Don't mention the avo on toast, that can die a silent death.

So spending is not going to happen at a massive scale immediately. The uncertainty surrounding a resolution for Covid in the longer term and the September Elections in the short term will propel people to hold their money horses. Banks will be the beneficiaries of more cheap money to lend and pocket a good interest margin. And some share trading platforms too.

Very prophetic and completely salient

I could cut back on the avocado toast or expensive morning coffees, but they only exist as tedious stereotypes foisted upon young people by the generation which crippled the state and imported population pressures to enrich themselves at the expense of everyone else.

The reality is, most young people who have a chance of saving and buying a house are already cutting things back by default. Employment scares won't make them save any more, they're already having to stretch to make huge deposits. If you want to talk about symbols of boomer excess (New Mustangs, shiny new white New Balances and verging-on-problematic drinking habits); that's where the real spending contractions will probably happen. While it's fun to dunk of boomers for their archaic views and walking-ten-miles-to-school-barefoot-in-the-snow-uphill-both-ways crapola, there's no getting away from the fact we need them to be spending now just as much as they need us to buy their overpriced houses to finance their retirements.

None of it will work if no one has a job or an income.

I think the so called Boomers are the wise people, they know the value of money, know how to make money, hoard it, and also spend and invest it wisely. They are also adept at influencing policies to protect themselves and their wealth.

They will know when to cut back as well their excesses and say good bye to Mustangs and say hello to Tesla at 30k.

All hard won lessons Contrarian.. don't know about swapping the Mussy for a Tesla though, gotta have some fun after all and the Mussy sounds a shipload better than a Tesla, although personally I'd go for a Camaro (looks better) or a 'vette (faster)

The annual insurance on a Mussy or a Vette scares me to death, Hook.

Hence, I am sticking to my Toyota Wish. Takes me from Place A to B smoothly.

Hmmm you have a point.. AGAIN!! I too will stick with my '08 Pathfinder. Cheap and solid. Good Boomer stuff.. LOL

Yeah, Corvettes can do 30 in a 30 zone, 40 in a 40 zone, 50 in a 50 zone and up to 110 in a 110 zone....and will get you from A to B at a price of about 100 times that of a SIMPLE CAR......So Gassing about it is something one may have to learn, as you get older. But what the hell, it took years for me to learn that. I used to have Gas Guzzlers too....but ....what the heck...It is all childs' play and a work in progress....

But then sometimes it ain't.

Buy electric, get a Tesla, richest non profit maker in the business......I could explain...but being a Rich Ppppp-erson is being a dick if you have to gloat.

Get on yer bike......by Hook or Buy Crook........keep the money in a safe place and get Fit....Live long and prosper.....retire early...have fun...Bye.

"They are also adept at influencing policies to protect themselves and their wealth."

Purely the benefit of forming the largest demographic in society the world has ever known. Make no mistake, Boomers influencing policies to hoard wealth is not due to some massive group consensus or any planning/strategic ability, its individual greed and fear manifesting itself on a grand scale, and materializing in the voting ballet.

Not quite sure which generation you're referring to GV re:"foisting" Who do you mean?

We have a media that acts like millennials are on a near-constant bender of avocado on toast rampages, only stopping to take a selfie or to order Uber Eats sixty three times a week, despite as noted, millennials having better savings rates and drinking less than their forebears. It seems to be particularly popular amongst the NewstalkZB/NZ Herald crowds.

Hopefully society at large now has the wisdom to understand all generations' fates are inexorably linked - the idea that we are extremely dependent on each other fulfilling certain economic roles is inconvenient for those who want to pay lesser wages but still want to sell their house for higher and higher prices, or talkback radio hosts who think angrying up the blood is the only for of engagement their listeners care for.

I wasn't alive but I hear 1966 was a good year for NZ radio.

I really have been a provocateur today. "Nothing is so provoking as the truth."

~Zack Brando 2020~

Generations are inexorably linked yes, but circumstances can and do lead to some generations being luckier than others. Boomers lived, probably in a once in a 200 year fluke of growth luck. A series of geopolitical, demographic and technological factors combined. Post war technology and rebuild led to the biggest surge of wealth (and wealth equality) that has perhaps ever happened in all of human history. They benefited from growth rates in bonds, property and shares that might never happen again, return on capital might never again achieve what was achieved over their lives (well not until the next fluke factor lands), they benefited from unprecedented workers rights, job security and protections. They were the first generation where they could often build wealth on two incomes or still afford to have one of them stay at home with the kids, before house prices became so high that it would henceforth require two incomes and necessitate children in childcare facilities.

My boomer parents don't deny this, they admit to all this and acknowledge the fluke of their wealth. And its not that they didn't work hard, they did, but their hard work paid off in a way that my hard work never can because the economy changed. My Mum is horrified by how hard I work, how few holidays I take, how frugal I am. She will say "it wasn't this hard to be a Mum in my era" and she does what she can to help.

I have no problem with a generation who just happened to have good luck. And who can acknowledge that. But i do have a problem when they rub their wealth in the noses of later generations, claim that they worked harder and somehow came by their wealth exclusively via their own efforts. And worse still, point at younger generations and their struggle to achieve a home or financial security and troll them with false accusations of frivolousness and laziness. The data simply does not bear that out.

There are social trends within generations and there are also repeating patterns. But we are always just the same human beings with the same human nature, responding to slightly different circumstance. Boomers born in the 80s and 90s would have been just as millennial and millennials born in the 50s would have been just as boomer! If we keep trying to feed on intergenerational hate/blame it might escalate into something very ugly. Newstalk/NZherald are irresponsible to fan these flames, we all need each other and we need to come to a way to support each generation fairly.

Nice post

I have no problem with a generation who just happened to have good luck. And who can acknowledge that. But i do have a problem when they rub their wealth in the noses of later generations, claim that they worked harder and somehow came by their wealth exclusively via their own efforts. And worse still, point at younger generations and their struggle to achieve a home or financial security and troll them with false accusations of frivolousness and laziness. The data simply does not bear that out.

Hear, hear.

As well as: vociferously resist policies that benefited them in their younger years being extended to following generations - e.g. government efforts to boost housing supply, the effects of land tax on creating more affordable access for more Kiwis to portions of land. Instead younger folk get their incomes redistributed as welfare that props up house prices and rental yields, for generations who received free education and cheap housing through the efforts of others.

Just remember , the market gets things right about 99% of the time .

The fact that ordinary players like you and me in the market are saving , means there is low confidence and fear is influencing spending decisions .

One could surmise that saving and not spending will result in as self-fulfilling prophecy of a consumer - led recession due to wallets being firmly shut .

Either way , its better to err on the side of caution right now and deal with the fallout later .

For me , I am saving and NOT spending on anything I dont actually need, and I am sure I am not the only one.

Stay lean, stay liquid? Sounds good to me.

However it has prompted me to do a bunch of deferred maintenance on things like cars and the house in case I decide I want/need to turn them into cash in a hurry.

I wonder how much of that home furniture spend was equipment for new "work from home" offices...?

I was interested to speak to a 23 year old made redundant from a hotel business about her perspective. Her and all her hotel and airline hostie and ground crew mates all got fulltime jobs by the end of the lockdown. Some are still in hospo where the restaurants and bars seem to be packed, doing as brisk a trade as ever. Others got jobs at post centers. Theirs is the highest risk group of unemployment in terms of industry and age.

Every single one of them got re-employed full-time and her perspective is people are still out partying, spending and she feels nothing has really changed.

I think she got the pulse of the people and their attitude correctly. "Go spend". YOLO.

I myself splashed out on 3 pairs of new Nike shoes in the last 4 months.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.