By Jarrod Kerr*

“Don't look so worried you know, There ain't no hurry, 'Cause life's supposed to ebb and flow” Shihad.

- Financial markets, globally, have been pacified by copious amounts of QE. And fiscal policy has joined the fray. Few do it better than NZ.

- Extraordinary measures are designed to boost asset values, including equities. But the risks remain heavily titled to the downside.

- We lower our interest rate forecasts and tweak our currency call. We expect the RBNZ to eventually double their QE program. And term lending to banks is the next (best) policy off the shelf.

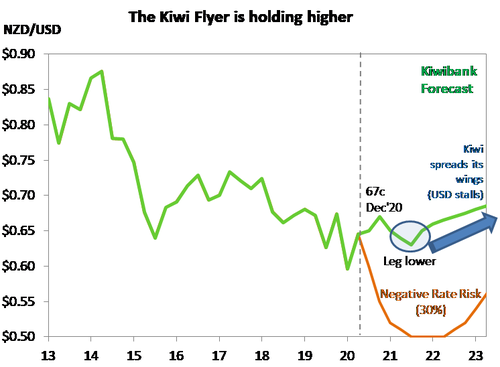

The pandemic is accelerating offshore. The economic cost of the covid crisis is climbing. And New Zealand is a small, seemingly pristine, Oasis of elimination. Although our nation remains vulnerable to imported cases. Our relative success, and resurgence in activity out of lockdown enabled us to upgrade our economic forecasts – see “Icy Climb”. Our current forecast of 67c for the NZD by year-end, remains unchanged. And we suspect the Kiwi flyer will have another bumpy ride over 2021. Interest rates are likely to remain at, or below, record lows into 2022. The ‘whatever it takes’ monetary policy mantra, and growing fiscal urgency, are powerful backstops for businesses and markets.

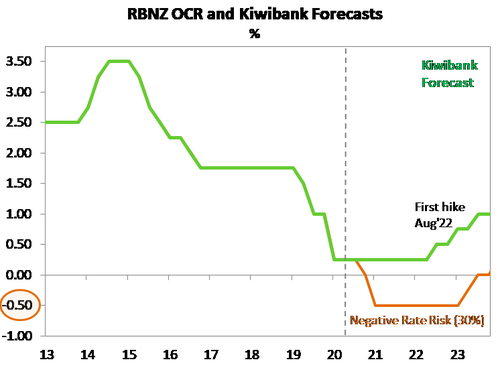

As economists we’re forced to make some pretty big assumptions. We’re assuming our bubble of 5 million remains Covid-free. We’re also assuming our borders remain closed until the middle of next year. Both assumptions are optimistic. Under our baseline assumptions the RBNZ will keep the cash rate unchanged well into 2022, as the local and global economy takes time to heel, and eventually recover. The risks to our assumptions are simply to the downside.

The message for businesses facing interest rate and currency risk is expect volatility in the currency, but much lower for much longer interest rates. Cash available for debt servicing is important in determining a businesses’ ability to leverage. The sharp decline in interest rates in recent years (and decades) has significantly reduced debt servicing costs for business and households. The RBNZ will keep it that way.

My Mandate’s Sedate: QEIII

“You gotta deal with it” Shihad.

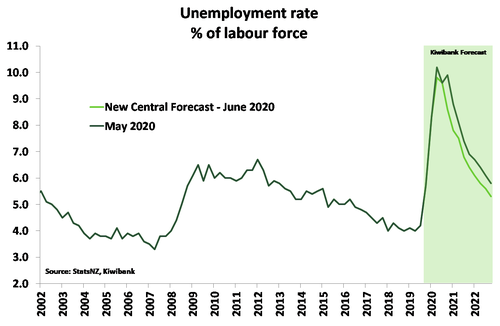

The RBNZ’s mandate is to “maintain stability in the general level of prices over the medium-term, and support maximum sustainable employment.” Based on our forecasts, the return to full employment and stable inflation (around 2%) will take at least two years to achieve. And that’s without any further shocks. As a consequence of the damage caused by the lockdown, and prolonged closure of the borders, the housing market is likely to correct by ~9% as well. The nature of the global shock means a swift full recovery is highly unlikely. There’s still a very long and bumpy road ahead, with plenty of risks from offshore – including a return of the virus itself, weaker trading partner growth, trade disputes, and the fact our borders will remain closed well into 2021. With both mandates unlikely to be met in the next two years, the RBNZ has more work to do to ensure the recovery is sustained.

Extending the QE program, call it QEIII, is inevitable. QEI was the initial $30b (actually make it $33b) commitment, in March. QEI was swiftly followed by QEII in May, doubling the program to $60b over 12 months to May 2021. QEIII, to be announced in August, will likely push the limit towards $100b, over a longer time frame into 2022. The program could then be extended to $120b into 2023. Extending QE in both duration and size is the (inevitable) next step for the RBNZ.

The expansion will enable the RBNZ to take down ~50% of (existing and incoming) Government debt issuance. LSAPs are limited to 50% of the total NZGBs on issue, with $139b total in 2021, $179bn in 2022, $198b in 2023, and $213b in 2024. The RBNZ could front load incoming issuance, but would need to expand the pool of assets purchased in our view. The RBNZ will continue to purchase LFGA debt and may consider buying other council (namely Auckland) and Housing NZ debt also. There’s still plenty of ammunition in the most preferred tool. But, beyond the $120bn to 2023, the program becomes more limited without a further increase in Government bonds. Therefore, if required, any further moves would involve the RBNZ pushing out the risk spectrum themselves, into all council, then corporate and bank bonds.

So, what about the other measures?

Term Lending to banks would be instant

The next best policy tool would be a term funding facility for banks. Cheap term funding will lower all bank rates (deposit and lending) immediately. We’ve seen a sharp decline in wholesale and retail rates already. A term lending facility would provide even cheaper, term funding to banks. Such a facility would reduce bank dependence on both retail and wholesale markets. All borrowing and lending rates would fall as a result. The spreads between the cash rate (OIS strip), swap rates, and all lending and deposit rates would naturally compress as banks tap the RBNZ, not the market, for cheap funding. The RBA provides a facility to the Australian banks. And lending and deposit rates are significantly lower across the ditch. It’s an effective, and proven, tool.

FX intervention is useful, but success may be limited

The RBNZ can sell unlimited, freshy minted, Kiwi dollars. The currency must be deemed “exceptionally high” and “unjustified” by economic fundamentals. Action must be “consistent with the PTA” (not hard), and at an “opportune” time to allow “a reasonable chance of success” (very hard). The first 3 criteria can be easy to meet. But the ‘opportune’ time for success is difficult. If global investors are piling into Kiwi dollars, because the rest of the world looks a lot worse, it’s difficult to stop. The Swiss tried a peg (trench warfare), but ultimately stepped away on 15th Jan 2015 (causing havoc). The RBNZ would have to engage in Guerrilla warfare. But it could be done. The RB could at least clean out a few positions and open up the market to downside risks.

Negative rates are debatable at best

If New Zealand enters a dreaded double dip recession, or W shaped disaster, then negative rates may go from being possible to probable. But negative interest rates are still up for debate. And we are far from convinced. Evidence shows negative rates cause a perverse increase in savings and lowers inflation expectations. We believe the drastic step is a last resort, and the last tool to be used. But there is a growing call for negative rates, and rates that are well below the negative rates seen in some parts of the world. Our work on the demographic influence on interest rates suggests New Zealand’s ageing population may push interest rates negative – as seen offshore. 75% of the decline in global interest rates can be attributed to ageing populations (increased savings and decreased investment). And negative rates may come to be seen as intergenerational wealth transfer… Talk of negative interest rates, however, has caused financial markets to persistently price in the risk, and the currency has traded lower (at times) as a result. Continued “jawboning” may help push the currency lower, and keep downward pressure on rates. But we don’t expect a negative OCR in this cycle. Although negative rates cannot be ruled out. Policy makers will do whatever they deem necessary in a recession.

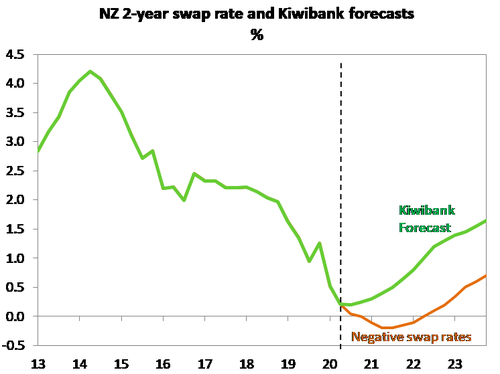

Sitting at a spread above the NZGBs, wholesale swap rates would also delve into the negative, just not as much. We would expect to see the 2-year swap rate trade down towards -25bps if the OCR hit -50bps, for example. Given 2-year fixed mortgages rates are hedged off the 2-year swap rate, such a move would cause a large downshift in mortgage and business lending rates. Deposit rates would follow suit.

Then the complication begins. The decline in retail deposit rates towards (but not through) zero, is likely to induce a higher level of savings – as experienced offshore. Because savers realise they need to save at a harder and faster rate to achieve their goals, or maintain the same standard of living (if retired). The removal of interest on Government bonds also adds stress to all the forced local fixed income investors. Added stress to the financial system at a time when policymakers are trying to rebuild, is a risk not taken lightly.

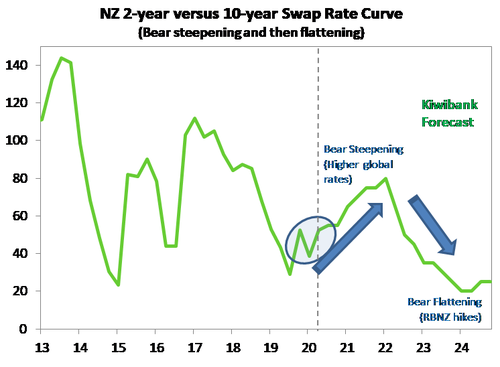

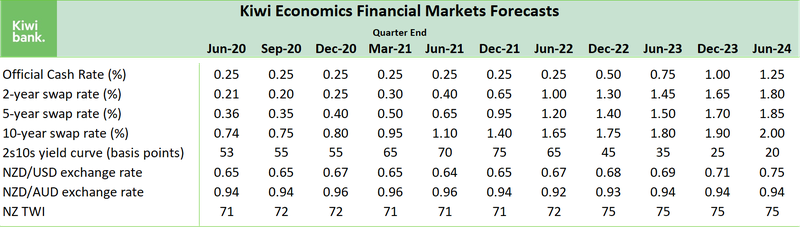

The outlook for rates in 2021 is either ‘on hold, at record low levels’, or ‘going negative, to record breaking levels’. Interest rate risk to the upside, is a risk for another year. From 2022, we see a very gradual lift in rates as the recovery continues and the RBNZ potentially moves to a tightening bias. We have pencilled in a gradual normalisation of policy from August 2022, all going well. We believe the normalisation process would include a long pause in QE (holding the RBNZ’s balance sheet unchanged) followed by an eventual evaporation of QE (or QT, Quantitative Tightening), allowing the curve to lift and bear steepen. The RBNZ would also embark on a very light lifting of the OCR back towards 2%, but no more, by 2026. That’s a very protracted ‘normalisation’ of policy. Even in our optimistic scenario, we struggle to see a sharp increase in interest rates over the medium term.

Low and flat interest rates over 2021, should mean the action will (again) be in currencies. And the Kiwi is the most volatile of the world’s top traded currencies. Hold onto your seats. Unlike the beauty of interest rates, that can all fall together, currencies are a different beast. Currencies are a relative price, and can’t all fall together. In the Covid world, the Kiwi is relatively attractive. Our pretty bird looks gorgeous compared to the dodos offshore. And investors are piling in.

Home again: the Kiwi flyer pushes higher as Kiwis return

“So sit and wait. And bend and break. You rise and fall. Just you, that's all. I'm here, you're there. It don't mean I don't care” Shihad

Success in eliminating the virus and moving out of lockdown earlier, makes New Zealand the envy of the world. Kiwis are flying home in droves. It’s the place to be, if you can get here. And the sharp bounce in spending and activity out of lockdown, has us growing in confidence. Our currency is reflecting the relative optimism, and has risen sharply towards 66c. The recent low of 55c seems like a lifetime ago.

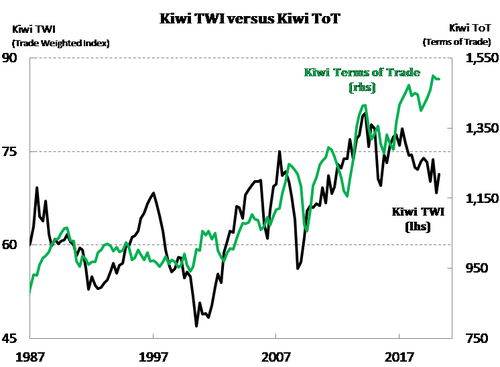

The strength of the Kiwi flyer has been supported by a strong terms of trade (for now). Our export prices have held up relatively well, and our imported prices (including oil) have eased. The elevated terms of trade is supportive during our time of need, especially on the export side. But the rising currency can quickly undermine the terms of trade boost.

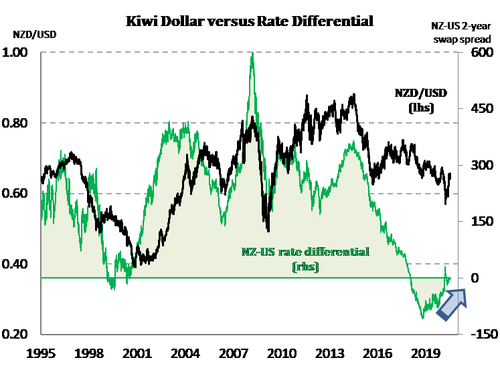

The other major driver of the Kiwi flyer is interest rate differentials. The Kiwi currency is also being supported by more advantageous interest rate differentials. We talk of RBNZ action, but other central banks are forced to do more.

We forecast the Kiwi flyer to end the year higher. Our NZD/USD forecasts have barely changed from early in the year, but the complexities around the forecasts have changed substantially. The Kiwi should remain relatively well bid into year end. But we suspect a drop back into the low 60s in 2021. Further policy action from the RBNZ will assist the Kiwi’s decline. At 66c today, the risk is asymmetrically lower. Our year end forecast of 67c offers little in the way of upside. As the world eventually (hopefully) recovers into 2022, we expect the Kiwi to outperform once again. ,Risk assets will gather momentum. And with a rise in risk appetite, the Kiwi flyer surges higher.

If you’re an exporter, hedging exposures to a rising currency can assist. You will hopefully get your turn to play in the low 60s.

If you’re an importer, 67c is within sight, and there may be a push towards 70c temporarily. Beware of negative press, central bank jawboning and downside scenarios.

*Jarrod Kerr is Kiwibank's chief economist. This report is used with permission.

48 Comments

*Boomer comment warning. Typos detract from the message.

More cheap money is good , just buy some F&P shares

In short to stay afloat more and more money has to be printed and distributed - asset class has to be inflated and keep it artifically inflated till times to come as that is the only economy.

Exactly.

For there actually is a cost to digitally printing trillions to bail out all the predatory parasites of financialization. Put simply, every dollar that's digitally printed that isn't matched by an increase in the productive capacity of the economy, i.e. the means to generate goods and services with less capital and fewer hours of labor, is nothing but a hidden reduction in the purchasing power of every existing dollar.Link

Central Banks Are Rate Followers, Not Rate Setters

Thus, the decline of interest rates to zero corresponds with a monetary imbalance in favor of deflation, if at least an abundance of deflationary pressures. This is something that Milton Friedman also talked about, particularly in 1998 with regard to Japan. He called it the interest rate fallacy, meaning that low nominal interest rates signify "tight" money conditions, or what would be consistent with significant deflationary pressure. It is and remains a fallacy because economists like those at every central bank around the world have decided instead that low rates are only "stimulus."

To correct this view, Friedman pointed out the basic, non-trivial distinction between a liquidity effect and an income effect. Low rates can be stimulative in the short run (the liquidity effect), but over the long run their persistence means something far different. A yield curve is supposed to be upward sloping given the core time value of money and investing. That arises from opportunity cost, meaning the more plentiful the opportunities the greater the time value and the steeper the curve (the income effect). Yield and/or money curves (the eurodollar curve and even the history of the OIS curve) that collapse and remain that way unambiguously demonstrate that "stimulus" deserves only the quotation marks. Link

The way I first put it in 2013 with my revision of the quantity theory of money is that Central Banks may have some control over peaks and troughs they don't control the trend. Yes they follow not lead.

Interest is afterall the price of money, if no one wants it the price will be low. It relates to affordability also, once tapped out on debt the only way to make it manageable is to keep lowering the interest rate.

Question is how is money making it into circulation to prop up asset prices?

Banks lending..

Ultimately there must be a reality check to cap them from rising into stratosphere?!

Taxation deletes currency, that is its purpose. Savings also remove money from circulation. The vast bulk of QE money just sits in the reserve accounts of the banks and so doesn't do anything.

Adrian Orr = Reverse Robin Hood

With all the kiwis returning for the medium term, NZs COVID-free status, primary exports continuing, older kiwis upspending locally instead of international travel, - how can house prices drop 9%? Seems there’s a miniboom going on in the economy atm.

Agree, currently there's a boom in housing market despite all the future predection, which may or may not come true.

It won't be 9%. That's just the highest single figure that won't frighten the horses.

In reality, all of the above adds up to one thing - The State is going to control the workings of the economy and not the Private Sector to the degree that it has.

The solution seems to be obvious - Control all of the economy until such times as it can be returned to the Private Sector. That means (1) a Fixed Exchange Rate (2) Capital Controls (3) Trade Controls and (4) Population Controls

Trying to manage all of the above with Interest rate and Liquidity targetting is pointless. The leaks will be too many to manage.

It's already done elsewhere; even in our trading partners, so why are we going to try to compete or survive on an unequal playing field?

In all likelihood, everyone will have to go this route, so Going Early and Going Hard might be better yet again?

Governments must take the lead

For this to happen there will need to be bold leadership and a willingness to do things differently.

First, we need a shared platform for coordinating the development of a collaborative market-shaping strategy. It will probably be temporary and would be best developed by the state, extending the excellent work already being undertaken

https://theconversation.com/the-market-is-not-our-master-only-state-led…

Interesting to see a government handing back all the control and power back to private sector. All the moochers easy to win votes from.

One trick pony economy

Can you call it an economy?

Very disappointed that QE is not reaching the common man. Where is the Helicopter money in my bank account ?

I saw someone else's comment on another thread to the effect we did helicopter money - targeted helicopter money - they called it the wage subsidy. It targeted affected businesses. I quite liked that.

Helicopter money runs the risk of inflation wrecking the plans of the asset inflating banks. QE causes deflation despite what economists claim. Helicopter money will not work anyway as people will save it or pay down debt.

A prezzie card with 5k on it given to everyone so it must be used for goods and services will certainly boost economic activity. But some inflation will wreck the banks capital ratios so will not happen.

I reckon there'd be a good market in Prezzie Cards at $4,000 cash for each one with a face value of that $5,000! (Discounting 'retailer' just banks the voucher with their daily takings)

The $4,000 then heads off down that 'saving and debt repayment' road.

(Luncheon Vouchers in the UK years back were the same. They came 'free' with your salary and you just cashed them in at the local sandwich shop)

A black market in prezzie cards would appear overnight - cash them in for $2000 cash

Or buy $2000 sell $3000

I promise to spend it wisely, on a trip to Queenstown. Please show me the money.

I tire of the 'Kiwis returning' narrative. Overblown.

Massively overblown.

It helps to support the narrative in favour of housing boom

Yes, it assumes they are all coming back cashed up, and/or walking into secure good paying jobs. Whats the odds most of those returning were those that hadn't been overseas long enough to become established and accrue significant assets.

What I have noticed over the years is that economists are generally awful at looking at the more nuanced aspects of trends. Far too many seem to rely far too heavily on aggregate data.

Yeah. Anecdotally (media stories, acquaintances) a large number of the people returning are young ones who went overseas not long before the lockdown, and lost jobs overseas. Also as I and others have said before, lots of kiwis overseas are perfectly happy there and never want to come back, or at least not come back for quite a while. Also, of course, many kiwis based overseas are in relationships with non-kiwis, and the partner may have no desire to live in NZ.

Kiwis often overrate the appeal of this country.

Yes Fritz, you don't have to look too far below the surface to see how NZ could be heading towards Columbia: a one-trick-pony income producer (but in our case exporting milk powder, not oil), and awash with violent drug-gangs (in our case importing and distributing illegal drugs rather than producing and exporting them).

Our only hope is to head towards Denmark:

https://www.youtube.com/watch?v=J5_I6noG0ps&feature=youtu.be

This was an interesting piece. It didn't just repeat the desired narrative but looked at the data: "Since March the number of people leaving this country has exceeded those arriving by a substantial margin", David Chaston, 6 July 2020, https://www.interest.co.nz/property/105905/march-number-people-leaving-…

Fritz - 'I tire of the 'Kiwis returning' narrative. Overblown' ???? Why do you say that ? There are 14,000 Kiwi's returning every month that looks set to continue for some time. Yes it will effect the housing market in the short term, then when the borders open 12-18 months ? there will be a massive surge in immigration for good reason, people wanting to live in a country that puts people's health before money. Jacinta has done a huge marketing exercise NZ. Those are facts why deny them.

Those are not facts. Those are opinions or even speculation. We don't know how many people will come back. That depends on a large range of factors, including how many jobs are available here (probably not that many).

Have you actually thought about who might be coming back? It seems like it's a lot of young kiwis who had been travelling, or lost jobs overseas. Do you really think that will be a big boost for housing? Tell me how?

It's all very well to dream up a dream of lots of kiwis coming home, landing well paying jobs, boosting the economy and the housing markets. As a housing spruiker, of course that narrative would appeal to you.

But it's speculation that is full of holes.

Why would kiwis overseas want to move to an overpriced parochial prison island where travel is prohibited?

To claim the benefit while the Australian economy recovers and then head right back over..... why else?

These people don't seem to fit the profile of well heeled property buyers.

If you look at the Customs figures you'll see that twicw as many are leaving as arriving, and no-one knows who either group is comprised of. Just because it was on Seven Sharp doesn't make it true.

or the returning international students narrative,if harvard can go online so can we and they dont have a reason to come.

They study so they can stay. Why not just sell citizenship instead.

Nothing to worry about here...

“If I’m going to be forced into equities, which is what the Fed’s clearly doing, I’m going to own the equities that I feel the best about and large-cap tech has become a safe-haven play.”

(Apple and Microsoft currently yield 0.86% per share and 0.96%, respectively. The 10-year Treasury note, meanwhile, has a yield of around 0.6%.)

https://www.cnbc.com/2020/07/10/big-tech-went-from-growth-stocks-to-wal…

Are at the point where the likes of Dalio think we’re in for a lost decade on stocks (so no capital growth) and the index yield is near enough equal to a 10 year treasury - so even though central banks are ‘encouraging‘ investment in the stocks the question could become, why would you when the risk/return just doesn’t justify it. I think this is why the likes of Buffett are more or less just sitting on a pile of cash.

The chart showing rates increasing was a nice piece of comedy.

Like any Central Bank, anywhere, has any intention or the first idea about how they are going to be able to pull back from loose policy.

They weren't able to do it when we had the most amazing economic conditions of all time, so what makes anyone think they are capable of ever tightening?

They've irreparably broken the system.

It gives the illusion they have a plan

quarantine and play - standard or luxury? gateway to the pacific. isolation cruises. minimum stay.

Oz news but relevant here. It shows how fake the economy is right now.

"JobSeeker payment: Pandemic sparked wage loss but rise in bank deposits"

https://www.news.com.au/finance/economy/jobseeker-payment-pandemic-spar…

I'm less optimistic than the kiwibank economists. In my opinion the virus will make it's way to NZ shores, at which point lock-down 2.0 will see NZ fall far behind all the other developed economies who've adopted more pragmatic and sustainable approaches. The massive fiscal spending (19->53% govt-debt:GDP) will largely be wasted on quarantine hotel stays and other fruitless endeavors. While other economies are retooling for increased output and productivity. (10 billion euros in Germany for Green energy production. Germany strengthens foreign direct investment scrutiny.) I wonder if all the NZ bankrupted companies will be purchased by foreigners for pennies on the dollar in several years time.

QE infinity! At this point, they basically don't have a choice, having painted themselves into a corner. They can't let asset prices drop, it would mean disaster for the economy and the housing market.

So money will be pumped to ever larger degrees... at what point does money become worthless? Which will mean your buying power with your saved funds now will be higher than it ever will be in the future. So why not use it to buy something now?

And with interest rates this low and the government likely to bail out any property downturn, why not just buy lots of houses? We have been so disconnected from sensible valuations for so long, the government won't have a choice but to bail out all owners of property. And I am increasingly convinced that our population is simple enough to accept it.

Righto, off to buy some more assets

"Extending the QE program, call it QEIII, is inevitable. QEI was the initial $30b (actually make it $33b) commitment, in March. QEI was swiftly followed by QEII in May, doubling the program to $60b over 12 months to May 2021. QEIII, to be announced in August, will likely push the limit towards $100b, over a longer time frame into 2022. The program could then be extended to $120b into 2023. Extending QE in both duration and size is the (inevitable) next step for the RBNZ."

Good bye NZD.

Good bye NZD.

And hello civil unrest?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.