So, the LVRs are back with us. Now we will find out whether they will 'work' against the newly white-hot housing market.

First up, I must just say that in my first, quickly-put-together, opine on the return of the limits on high loan to value ratio (LVR) lending last week I now realise I somewhat gracelessly skipped past the fact that it was a good thing on the part of the Reserve Bank to put the limits back, u-turn or not.

It's a move I certainly wanted to see, so, well, good to see it.

However, and there's always a however, isn't there, I'm not sure whether the balance of the LVRs rules is going to be quite right in the face of the super hot market that will greet their reintroduction.

It may seem odd to say that, given that the rules will be the same as they were at the time the LVRs were removed by the RBNZ from May 1. I will explain my reasoning as we go on.

But first, to refresh memories, these are the rules as explained on the RBNZ's website:

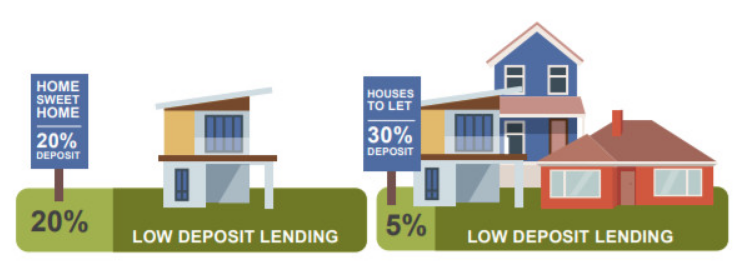

Owner-occupier loans – 20 /20

This is borrowing secured with a mortgage against residential properties that the borrower lives in or uses as a holiday house. High-LVR loans are defined as those loans that are more than 80% of the property’s value (20% deposit). High-LVR loans can make up no more than 20% of a bank’s total new lending in this category.

Investor loans – 30 / 5

LVR lending restrictions are tighter for loans secured by investment property, in response to the growing housing market risks in that area. High-LVR loans in this category are those loans that are more than 70% of the property’s value (30% deposit). High-LVR loans can make up no more than 5% of a bank’s total new lending in this category.

It's worth remembering that those are the rules as they were at the time the LVRs were removed in May. There's been a few iterations along the way since these things were originally introduced.

At the very beginning of the LVR regime in 2013 the rule was applied across the board; banks were restricted to just 10% (known as the 'speed limit') of new lending on loans that were more than 80% of the property's value.

House prices did moderate considerably in the 2013-14 period. But I don't think it should be forgotten that in addition to the impact of the LVRs, there was also the not trivial matter that between March and July 2014 the RBNZ hiked the Official Cash Rate from 2.5% to 3.5%. As we see in 2020 with such incredibly low interest rates, it's interest rate levels that really make all the difference in the housing market. Low rates are catnip. Rate hikes are a cold shower.

So, anyway, by May 2015, with house prices in Auckland very much on the rampage again the RBNZ made a substantial tweak to the LVRs. It introduced a 30% deposit rule specifically for investors in Auckland. In Auckland the 'speed limit' was retained at 10% for owner-occupiers. However outside of Auckland the 'speed limit' was actually loosened, whether you were an investor or not, to 15%.

I might say, I thought these moves were great at the time - but they turned out to be the opposite of great. Oh yes. In reality the voracious Auckland investors started marauding the countryside outside of the Auckland region for new investments. The upshot was the market in Auckland kept bubbling away anyway, but now the rest of the country started coming to the boil as well.

So, then we had what looked at the time like a desperate move. In mid-2016 the RBNZ took out the blunderbuss and aimed it at all investors throughout the country. A 40% deposit rule. That's it. No arguments.

As I say, this one I thought was desperate. This one worked.

And it allowed the RBNZ to gradually ease the restrictions from 2018 onwards to the point where we finished up with the settings that were in place early this year.

My point of contention then is; will a 30% deposit rule on investors rein in a heated market?

It's hot out there

The reality is there were plenty of signs the housing market was really starting to heat again early this year just before everything went Covid crazy - although it is true that at that point the investors were not strongly re-emerging from their slumber.

However, since the February/March period and the lockdown both fixed and floating rates on new mortgages are anything from 0.75 percentage points to over a percentage point lower. And they were already low.

As cannot be stressed enough, such super low interest rates apply a push-pull dynamic to housing investment. Investors get rubbish returns on deposits at the bank so they are 'pushed' into housing investment where the yields will be (they hope) better. And, of course, super low rates for borrowed money make it that much easier to buy a house. So, this 'pulls' them into the housing market. The result is the investors are on the rampage again.

Which is all my way of saying that while a 30% deposit requirement on investors may have seemed okay at the time the LVR limits were removed, it might well not be enough to dampen the ardour once the LVRs return.

I hope the RBNZ will keep its options open in terms of raising that deposit requirement quite quickly if there are not reasonably quick signs of the housing market cooling somewhat.

Bring on the DTIs

I think it is also well overdue that the LVRs had some more 'friends' in the RBNZ 'macro-prudential toolkit' - well at least one more friend anyway. It is high time the RBNZ had the option of some kind of debt-to-income control measure.

We know that in this country our debt to income levels on house buying are getting pretty elevated.

In fairness, I thought the latest (September) quarterly DTI data produced by the RBNZ suggested that New Zealand's most stratospheric DTI ratios - in Auckland - were at least plateauing if not falling slightly. Is this borrowers reaching their own limits? Or is it the banks applying some handbrakes? Either way, I thought there was some encouragement in the latest figures, given that they were figures compiled amid a very fast rising market.

Still though, some further measure of control for housing lending for the RBNZ could only be good. So, here's hoping this Government is amenable to the idea of at least having DTI controls available for the RBNZ.

This leads me to a final thought that should be stressed, but probably isn't stressed enough.

Not my job

It is not the RBNZ's job to control house prices. Or to ensure that young first home buyers can 'get on the ladder'.

The RBNZ is there to preserve financial stability. To very much simplify the position: The RBNZ wants to avoid a situation where too many people take too many financial risks with their house purchases and get themselves into trouble. And the trouble forces them to sell (or forfeit) their property. Which means a lot of property goes on the market at once. Which means prices go down sharply. Which means the banks start to look at making big losses on their loans. Which leads the banks to start sharply reining back on credit. Which leads to disorder...

That's kind of roughly what the RBNZ is trying to avoid. You being able to afford a house is not down to the central bank.

Ultimately the New Zealand love affair with housing and the whole question of whether those who want to buy houses are ever able to do so is down to the Government.

Hopefully the reintroduction of LVRs will get some sense of order back into the housing market next year.

But any long term fix to the ongoing housing problem in this country is going to have to come from this Government and future governments.

44 Comments

The fact is that Jacinda does not want to alienate property investors vote block. She will do all the hand waving but not tackle the housing problem head on. period.

The sad part is, while landlords think they win, but in long run, they do not. Housing is a big driver of brain drain from NZ and a downward pull for NZ economy.

Cue land tax, wealth tax, inheritance tax, and/or (shock, gasp!) capital gains tax...

Median household income in June 2019 was $102,613.

Median house price in Oct 2020 was $725,000.

Property to price ratio was : 7.

There are still room for the ratio increasing to 10 nationally (1 million houses) and 20 (2 million houses) in population centres.

Keep buying guys.

Income to house price ratio will never reach 20. I would guess 12 or 13 is the absolute max and we are almost there in Akld. People who borrow heavily will be in a sticky position if Govt decides to inflate away its debt causing interest rates to rise with inflation. Seems unwise to currently take on debt that you couldn't service if rates were 5 or 6%, unless you are happy to take a real gamble for a lot of money.

Karl, "never" is a very long time. What if retail interest rates reached 0% ? It would be perfectly fine to have a DTI (which I have always said is a flawed measure) of 20, 50 or 100.

Of course you will reply that retail rates will never reach 0%, just like the OCR could never go below 4% or the RBNZ would never print money or numerous other examples many thought would never happen.

Agree if retail rates reached 0% it could happen. Even at 1% or lower it's possible. But as you said I would say, it is a pretty big if.

But this is the era of financial repression. I wouldn't be surprised if we see 10% pa real inflation with official inflation below 2%. Borrow borrow borrow (for hard assets).

Great article David, in my opinion housing investment should be banned altogether until we reach levels of affordability compared to what we used to have 20-30 years ago. As long as there's a single Kiwi that cannot afford a healthy home, investment in first necessity assets such as housing should be considered as what it is, something good to have if economy allows, but not in this context.

Hi b21

Not a problem at all if you are happy to have all those potential tenants in need of a home in your place . . . or they could harden-up and go live under the bridge. ;)

Rental accommodation is needed to house people and there is currently a shortage.

Totally not my point. BTW we do not need to rely on the good will of investors to provide the rental properties we need to the market.

I guess you're waiting for the 100'000 affordable homes form the government huh?

I guess you are waiting for the same number affordable homes from private investors? We have already seen where that goes.

Private individuals have built far more houses than the government lately, B21. In 2019, 37,000 consents for houses were issued, of those 2-3k were Kainga Ora and a few hundred were build by kiwibuild.

I am totally aware of this, and this is exactly my point to where the problem is.

How would you propose that work?

Sounds a lot like communism which never ends well.

Who is the boss :, Mr Orr

AND

Boss is interested in price rise so Screw everyone

AS

Boss is always right specially when supported by PM

Good article David, as you point out interest rate is a major driver of house prices, therefore the answer to your question whether LVR of 30% will be enough, depends on whether the FLP, which has the explicit purpose of further reducing interest rates, will be exempt for lending to buy existing houses. If the FLP can be used to lend to buy existing housing, the LVR's will have very limited effect

FHB: I want affordable housing!

National: No

Labour: No #aroha *love heart* *rainbow flag*

People need to get over the fact that bank deposits are unlikely to return as a source of stable income for quite a while. How long are the shades of the late 80s stock market crash going to haunt us? Get over it people and invest in proper places. A place to live is all anyone needs.

Buy inflation proof assets people because hyperinflation is coming

Buy Bitcoin.

Theoretically your right. But you can't borrow 80+% of your bit coin investment to leverage. Plus you'll be taxed on your sales of bit coins.

actually you can apply leverage on most of the major exchanges, some up to 100x. No paperwork etc as they have your BTC as collateral. Tax is another issue

???? I know little of Bitcoin, but one of the few things I know about it is that you can leverage Bitcoin.

Actually, you can leverage on virtually every asset class under the sky, even pork bellies.

Housing speculators that claim that residential property is the only asset class where you can leverage only demonstrate that they don't know how investment markets work outside the real estate market. I have seen this theme recurring in interest.co.nz, and it is time to dispel with myth once and for all.

Regarding taxation, cryptocurrencies follow the same philosophy as a few other asset classes: the profit derived from acquiring cryptoassets for the purpose of disposal as a "trader" is taxed, like shares, but this is not necessarily the case if they are treated as an "investment".

- re garding non FHB. Park them for the moment.

With most deposits come from revaluation & redraw from existing (but other upwardly valued) property assets. Are the higher ups happy they have thought this through?

Thinking about funding of FHB lots come via Bank of Mum & Dad, are at least share a dep. Acc balance.

# is anyone putting actual cash in?

Q. How effective will a 30% LVR be for investors??

A. Minimal to absolutely none.

A little story that with modification of figures is applicable anywhere.

My son lives in Gisborne.

He bough his first home under three years ago.

A few months back he bought a rental property. I offered to go shares - he ended up saying "nah Dad".

Why?

It wasn't because he hates me.

Lets look at why?

Like most if not all investors he leverage of his existing property.

He bought three years ago for $300k with $60k equity (no need for help from the bank of Dad then). His home is now considered by bank to be worth $500k (actually up 34% just in past year) so his equity is now $260k.

The rental he bought this year was $350k without having to to put in any significant extra money .

(I know you Aucklanders will be either in disbelief or spitting tacks - housing is a tremendous cost if you choose to live in Auckland).

Total value of both properties $850k - his equity of $260k gives close to 30% equity in both properties.

So it was "nah Dad, I don't need you".

Yeah, yeah, Gisborne region had record national growth this past year so a selective biased example.

However, apply it even to Auckland but consider a longer timeframe.

The reality is that most home owners who purchased properties prior to 2014/5 will be able to leverage of their existing home to meet LVR deposit requirements - Auckland median prices up 16% past year.

The reality is that these same home owners have not only done well out of CG on property, but have also seen their mortgage repayment costs most likely halve since they purchased.

Well, so what? They have the ability to leverage of their property, have more than a few hundred dollars a fortnight a week in their pockets due to lower mortgage payments, have had a positive property experience, can't spend the money taking the kids to Disneyland . . . why not that rental and any 30% LVR isn't going to be a handicap and with that extra money they will have little problem meeting any bank stress test or DTI ration. Happy for an Aucklander to do the maths.

Yeah, yeah; "bubble burst, bubble burst" - been hearing that for the last five plus years.

Well maybe make the 30% deposit needed in cash. That may be a little more challenging.

That’s easy to get around. Draw down one an existing property and then get the cash and then buy with a different bank. This is exactly how I bought my second house but not for the reasons above.

Is using a loan as deposit for a mortgage legal?

CourtJester

Yes it is certainly legal and such leveraging is common and usual practice amongst investors.

That is how investors finance multiple properties. The situation for a first home is not likely to be the case - it is all about one’s equity and not simply “cash”.

In the past I was active in investment properties; other than my first home not once did I buy a property using cash sitting dormant in the bank.

Njay

What you suggest is not in touch with reality.

Technically it is cash. The bank provides is cash on the existing property - simply increasing that mortgage - and that cash is seamlessly used as the deposit or equity in the new property.

Hi P8. I enjoy your posts by the way. I think you are missing my point. My point is that instead of being able to leverage against an existing property to raise the deposit, you have to raise the cash deposit by some other means. Leverage to start up a business and create jobs would be a great idea and save a deposit for that next property if you wish. I know this goes against convention but we need radical thinking. I know everyone will say that oh well, who is going to supply all the rentals, well maybe that's the job of the government, yes, it will take time but the housing bubble wasn't created overnight and I don't think can be solved overnight. We have to start somewhere. I know that would upset all investors but something radical has to be done or this will just keep going which I don't think is good for our country long term.

Multifactorial failure, RBNZ and Govt are saying it is a supply issue, and an environment of raising prices helps to bring more supply into the market, and supports the wider real estate industry (construction supply chain and also the business of selling existing houses employs a lot of people). But it takes time, and with the current favourable tax treatment over other asset classes and the familiarity of housing to people with money that is looking for a return it looks like we are well and truly off to the races with the demand, and the lever to balance supply and demand is price, and the cost of the transaction.

My thoughts would be adding more things to junk up the transaction, agreed anything done quickly is going to be a mess, but why don't try a few things that reduce the attractiveness of existing property as an investment? ideas like a)removing the ability of using businesses to buy existing houses. b) only tax residents can purchase, or hold nz property. c) housing must have a building warrant of fitness (this would require a lot of work) d) stamp duty that goes to the local council ( get that money in the coffers AC :-))

Additionally, I would be thinking about looking at what investments this money can actually go into, a covid bond or infrastructure bonds that have a good return, and also looking at the investments that ACC retirement fund etc are making. They are making direct investments into private companies like Les Mills International, and Bayleys etc, instead of them having some public offering that creates a viable option to invest in well run businesses.

Any other ideas?

Orr's approach is simple: give more alcohol to the alcoholic.

"The RBNZ is there to preserve financial stability. To very much simplify the position: The RBNZ wants to avoid a situation where too many people take too many financial risks with their house purchases and get themselves into trouble. And the trouble forces them to sell (or forfeit) their property. Which means a lot of property goes on the market at once. Which means prices go down sharply. Which means the banks start to look at making big losses on their loans. Which leads the banks to start sharply reining back on credit. Which leads to disorder...

That's kind of roughly what the RBNZ is trying to avoid. You being able to afford a house is not down to the central bank."

Exactly....the Government (of any stripe) has the obligation and tools to mitigate...that they they havnt is on them. The RBNZ have two concerns, bank stability and a competitive currency (does anyone believe a marginal diffence to the employment rate trumps either of those?)...let them do their job and berate the Government for house prices

100% correct...

"It is not the RBNZ's job to control house prices. Or to ensure that young first home buyers can 'get on the ladder'. The RBNZ is there to preserve financial stability."

If we want to reign housing prices in, then I quite like the idea of DTI's, LVR's as well as changes to immigration policies and housing benefits which typically now go indirectly to supporting high rents

Most deposits are loans based on property revaluations.

# cash less

The problem is not investors buying houses. It’s the Mums and Dads buying and selling their own homes knowing it’s guaranteed tax free profits. It is very common for home buyers to buy and sell within a year or two to grab the profit and bank the bulk of it. What should be done is extend the bright line test to homeowners who sell for a profit but do not invest all the proceeds into their next home. Exemptions would apply to those retiring or going into rest homes or serious genuine reasons. I know of one family who paid $10M for home, did some light weight redecoration and sold for $20M all within 3 years. They are now looking for another $10M home to repeat the exercise. Nice work if you can get it.

In principle fine. In practice it's administratively heavy, so impractical.

Problem is no one wants to own the problem. Low interest rates are causing a house price explosion. Adern says low interest rates are not her fault - it is the reserve bank who decides that. Orr says rising house prices is not his problem either. History will judge both poorly.

Neo-Lib ideas penetrated pretty much like cancer cells itself, the removal will be much more pain to do. So? just let it be ...turn into corps of zombie.

Housing inflation, hikes the rates! really? if that the case? put housing out of CPI reporting. Cunning eh? - Employment issues, increases! really? if that the case? put it to RBNZ - Soon NZ will be swamped by multiple earthquakes, tsunamis, more pandemic, for 3-5yrs, not a prob. sit safely at home.. subsidy from RBNZ printing money soon distributed by the govt, clever apart from cunning too. You name it, the so called leave it to the natural market? everything will be done to distort it, if it's going pear shaped.... NZ economy is like a terminally ill patient, refuse the verdict.. until.

Leave it running, the faster, the hotter.. the better. Any prudent regulatory measures means just that, a jealousy.

NZ is not a nanny state, we don't need this idea. NZ is not yet achieving ideal ratio of housing price inflation.

The economy will be on steady growth, once we can achieve the housing doubling price for every 2-3 years.

Current Lab govt. is on the way to achieve this, let's hope they can deliver. If not? Opposition will steal the march.

Complicated problems can only be solved by complicated responses. Simple is good but tends to create unfairness.

I would order that all lending to property investors on their businesses of "people farming" be charged at commercial rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.