By Jenée Tibshraeny

2020 has been a year of reassessing our values.

Nature has reminded us humans are not at the top of Earth’s pecking order. We have a new-found appreciation for being able to spend time with loved ones - in person, and we’ve come to plan for changes of plan.

But there’s one area we’re yet to move on: property.

Too big to fail

The message from the Government and Reserve Bank (RBNZ) is effectively, the residential property market is too big to fail.

With housing equity accounting for two-thirds of households’ net wealth, both Prime Minister Jacinda Ardern and Finance Minister Grant Robertson have commented New Zealanders can “expect” house prices to keep climbing - ideally at a more moderate rate than at present.

No Members of Parliament have committed "political suicide" and called for a moderate or controlled decline in house prices.

The Labour Government is too scared of even exploring the counterfactual to its unsubstantiated policy of house price growth, even though its decision to pursue this goal is worth 10s of billions of dollars in the immediate-term and will affect generations to come.

House price growth is the unchallenged status quo that’s possibly been the only thing immune to reassessment in 2020.

The Government has of course been stuck between a rock and a hard place, as the RBNZ has been slashing interest rates, in part to support the wider economy via the property market. Neither it nor Treasury earlier in the year expected house prices to sky-rocket.

Nonetheless, the RBNZ's been open from the start, it would rather risk over-cooking than under-cooking its response.

While the likes of former investment banker, Raf Manji, called it earlier, this writer has been urging Robertson from at least June to start considering policies that take into account the fact, historically, cheap new money has seen asset prices balloon to the benefit of the wealthy.

Early in the new year Robertson will reveal the advice he’s received from Treasury on what to do to cool demand for housing.

A policy mix aimed at a controlled decline in house prices shouldn’t automatically be written off as an option.

So, what would actually happen if the country’s median house price fell by 18.5% to where it was a year ago at $632,000?

1. Someone wishing to make a 20% deposit would have to save $23,400 less.

If a buyer paid 4% interest over 30 years, their monthly repayments would be $447 lower than what they’d be now.

The total value of their principal and interest would be reduced by $160,920.

Lower house prices would help more people into homeownership, giving them stability, security and social connectedness.

It would also reduce the transfer of inequality between generations, as poor and middle-class kids wouldn’t have to risk changing schools and then struggle to buy a house without access to a ‘Bank of Mum and Dad’.

2. Rents would likely stabilise.

The need for rents to become more affordable is acute. Boosting wages won’t do enough.

There are 3,653 transitional housing places, like motel rooms, for people in urgent need of temporary accommodation.

Separately, 2,853 households received an Emergency Housing Grant in the week to December 11.

There are 70,889 households in public housing and 21,415 households on the waitlist - a 44% increase from a year ago.

The Government is working towards building 6,000 public homes and 2,000 transitional places. This won’t be enough.

There are a whopping 372,235 households receiving an Accommodation Supplement - a weekly payment to help cover rent or mortgage payments. There has been an 18.3% increase in the number of households receiving this support year-on-year.

According to Statistics New Zealand, renters are about twice as likely as homeowners to spend 40% or more of their household incomes on housing costs.

In the June 2019 year, just over a quarter of renting households spent 40% or more of their household incomes on rent and other housing costs, compared to about 1 in 8 people who owned, or partly owned their home.

Lower rents would also support younger people, who have been most affected by Covid-19 job losses, yet haven't benefited directly from the RBNZ's stimulus lowering debt servicing costs and boosting asset values.

3. Homeowners would feel less wealthy.

RBNZ research done pre-Covid suggests on average people spend an extra 3 cents each time the value of their house goes up a dollar.

So, the $117,000 increase in the median house price over the past year should’ve been accompanied by a $3,510 increase in spending on consumer goods and services.

However, it would appear currently those who aren’t buying property and/or shares are putting their money in the bank.

Households put an additional $17.8 billion in the bank over the past year - a 9.7% increase from this time last year.

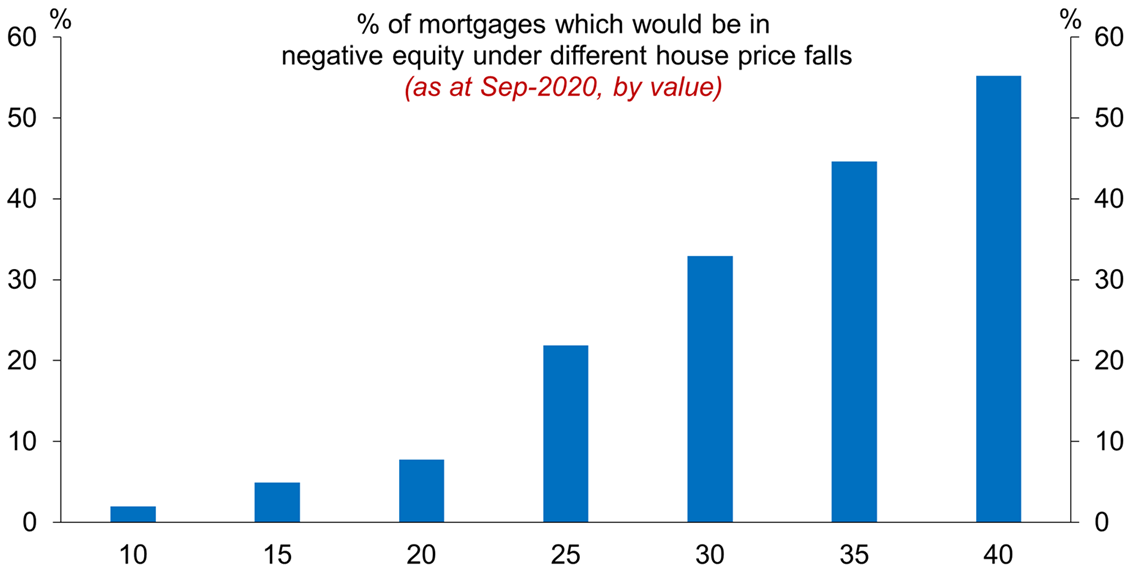

4. A 20% fall in house prices would put 7.7% of mortgage debt ($22.3 billion) in negative equity, according to the RBNZ.

Negative equity occurs when the value of a property falls below the outstanding balance on the mortgage used to purchase that property.

This would become a problem if a mortgage holder had to sell before the market had time to recover and they couldn’t afford to pay the outstanding amount on their loan.

If house prices fell by 30%, the portion of mortgage debt in negative equity would jump to 33% ($95.6 billion).

5. Businesses - particularly small ones - with loans secured against residential property would get nervous, threatening people’s jobs.

There is $5 billion of business debt completely secured against residential property. This is equivalent to 1.7% of all the country’s mortgage debt.

The RBNZ doesn’t collect data on business loans only partially secured against residential property.

Both the RBNZ and Government have rightly and successfully prioritised keeping people employed in their economic responses to Covid-19.

6. Business confidence would take a knock, with a question mark over the degree to which this would stymie investment.

Business confidence in December hit its highest level since before Labour came into government in 2017, according to the latest ANZ Business Outlook Survey.

This is despite Covid-19 continuing to plague the world, disrupt supply chains and cause job losses.

The resilience of the housing market is bound to have influenced this reading.

It’s worth noting low business confidence didn’t translate to high unemployment pre-Covid.

Conclusion

New Zealand’s economy and financial system are precariously built on the housing market. It is for this reason policymakers would rather protect than risk damaging this market.

But what we need to realise is taking a block off the top of the game of Jenga that is the housing market, and sliding it back into the foundation, is possibly lower risk than taking another piece out from the bottom to keep building an increasingly shaky tower.

More research needs to be done around the trade-offs surrounding changes in house prices from inflated levels.

2021 needs to be the year of challenging the narrative that house prices must always keep going up.

227 Comments

Minimum wage is going be $20 a hr.

House price fall?

for NZ, it would only fall when people stops migrating to NZ for some reason in the next 30 years.

OCR down, LVR gone, FLP, QE 100billions, taken roughly of 20% from the 100billion part, what will happen to that 20% housing price increases? if the QE is just 80billions?, 60billions? - XMW, is super correct. The current dented influx of cheap overseas money/labour being replaced temporarily by printing money, worldwide consensus to repay it back is by squeezing more blood/taxes & the very unpopular 'austerity'. BUT hear hear hear world, NZ found the solution: once the natural disaster/pandemic etc. past - the pay back is to be done by the new capital in=people movement in.. that is for sure. Trust me rarely people move their big capital to one place, without them move to that place. It's a trade. NZ is ideal place for seasonal worker, students, wannabe migrants, cheap labour.. this is a golden shine of hidden plan specially by right wing govt. - left is just hands off.

The obvious trigger for a big drop in house prices in NZ is a significant overseas event i.e a major correction in the financial markets which is quite likely give just how stetched valuations are in many industry sectors. Furthermore the economic outlook for many major economies is looking challenging to say the least. e.g www.nzinitiative.org.nz/reports-and-media/opinion/the-coming-monetary-c…

It's a silly Article. The property economy will never, ever fall.

The NZ Government and RBNZ 100% categorically guarantee its on going inflation.

Quite simply put, it's no longer a bubble - it's our economy.

Wayyyyy to big to fail.

NUTS!

100% correct, bugger!

It is our only economy. Once those borders are opened, it’s going to be open slather on immigration, it’s the only way to keep this thing alive. Come one, come all...

if you don’t get into the market by mid-21, you never ever will. It’s appalling, but there it is....

At one point, I thought these prices gains were humbug, but now I am starting to believe the following (owing to mass immigration once the borders re-open:

The leafy suburbs and central water fronts, will continue to be in their stratospheric ranges and stagnant at best for the next 5 years;

There will be a change in demographics in the mediocre suburbs and shite holes, which will start to get new influx of working people (I see a lot of selling in Otara, Manurewa and Papakura).

Most of the development seems to be going south and places like Pokeno, Pukekohe, Tuakau and Bombay seem to be the next safe bets.

As for the north-west, places like Hobsonville and beyond are already out of reach (cookie cutter town-house crap is selling for over a million off the plans with a 7% deposit).

What NZ actually needs is much more of the cookie cutter houses that are of a high build quality. All this got to have a bespoke home BS just makes building more expensive. Like it matters if your house is the same as next door, if it was $50K cheaper and better quality than your one off design, wouldn't you buy one ? You just personalise the inside.

Dumb article, what if they fell 40% 50%, what if they went up 50% on a year blah blah

Sorry Luke but I think Jennée's "what if" article is an interesting talking point which needs to be addressed

I agree. It's an excellent, thought provoking piece on the various pros and cons of a booming housing market versus one that corrects.

There's too much binary thinking on this site, that lacks nuance.

... what I'd like to see is the media spending more time on articles about Kiwi business successes , such as Xero , A2 Milk , F&P Healthcare ....

A broad based healthy economy is built upon a vibrant business sector ... not on a vastly inflated residential house price bubble . ..

Why are you sorry, I think it's stupid article, you don't, that's fine, end of story.

I agree Luke, I'm not sorry, I was just trying to soften my stance. So happy to disagree with you without being sorry

Yea of course, people are allowed different views, merry Christmas

Well, thanks for clarifying that...

What made you read it (presumably) and comment on it? The internet's a big place, you can ignore the stuff you don't want to read.

I found the article far more useful than your contribution - a few useful numbers about what is a quite conceivable future - 20% drops in housing markets around the world are fairly common.

43 upticks Yvil ... you are popular today

Hmmm worrisome, I may have to re-evaluate my post, lol

I agree Yvil

Hey we agree! lol. Merry Christmas mate, catch you in 2021

I've just popped a graph in, provided by the RBNZ, that shows what portions of mortgage debt would be in negative equity if prices fell by more than 30%.

Thanks, great graph which shows my point made below at 9:16 that whilst a 20% drop in prices will most likely not be too problematic, a further slide to 25%, 30 % would become very difficult to handle by many.

If about 65% of NZ population into gambling? do you think the authority such as govt & RBNZ will sit doing nothing? - you've just high lighted, if it's becoming very difficult for many, then the intervention will be there for them, bail them out for example. Human have learned in the past how Tulip mania/bubble being disrupted by Bubonic plague, so in similar case in today's modern world.. the weapon for it is govt & CB interventions, this interventions designed to be as a 'buffer' until the next cycle pick up, the interventions is at the future cost. The issue is how prolong is the mania can be supported with interventions?, the pandemic may still be on going, but the interventions can be diverted/distorted by different reasoning eg. climate change/try to be carbon neutral/bailing out the insurance for coastal erosion/flood prone risk zone.. The most feared worldwide phenomenon that govt & CB afraid of.. is just that.. 'public/world confidence' - when their decisions impacting too much in consistent/unfair result.

Fritz, my reply of last may have come too late for your to read, so here it is again:

by Yvil | 22nd Dec 20, 9:07pm

I'm actually happy to make another prediction on which you can hold me accountable (Fritz). In 6 months time, there will be no more house price increases (HPI figures for June released in July) UNLESS there is another significant drop in interest rates to below 2%

Thanks Yvil. I don't actually really care anymore what anyone's predictions are, or whether they are accurate or not.

But for what it's worth I would tend to agree.

Hi Yvil,

excellent article by Jenee. Astute forecast by you about prices stopping rising if interest rates not cut further.

Underlining the point that prices rose due to rates falling, plus shortage of good stock and desire of many to escape urban crowding + fact that they became convinced (unlike prev 2 years) that they would get more than CV in Auckland especially.

When inflation starts its (not to me!) unexpected rise, bank will come under pressure to raise rates. Which of course they will not. But won't cut further.

Do not expect more cuts, except maybe .25 in March and only then if world economy in severe mess.

However, if CB does cut by .25, I do not think high street banks will follow.

Hi yvil , can I ask why the change of heart on your prediction? Before your opinion was that house prices will only keep going up . Please share your thoughts :)

Starr

That is not correct and at best obtuse but more in fact a very weak and pathetic post which has no value.

Yvil has always commented on the market outlook and in fact posted that he sold in the expectation of the market peaking. In the long term 5 to 10 years one can expect the market to show growth but those with experience - such as Yvil - know from experience that the market fluctuates. Yvil will have experience a number of such negative fluctuations.

Care needs to be taken that there are some who assume that there are two very distinct camps on this site - those who maintain that property always increases and those who claim bubble burst.

There is a third group - those who call what they see as the future of the market based on the changes in the wider environment and economy - and that is not flip flopping but being astute.

In response to your request to share one’s thoughts - Starr, you need to start ensuring that your posts show a bit more intelligence.

Printer8, I didn’t realise you were Yvils personal assistant. Judging by your uptight post, you must be fun at parties. Chill out mate, it’s Xmas :)

Starr

Thanks for your suggestion re Christmas. I can assure you I’m enjoying Christmas with family and friends.

In return for you: a New Year’s resolution to make improved constructive posts is much needed. :)

Cheers

Hi Starr, I have said that if one can afford it, it's best to buy a house asap because no one can accurately time the market. Many misrepresent this as me thinking the RE market can only ever go up, I have never said such a thing.

To answer your question, IMO the current strength is due to lower interest rates and removal of the LVR's. As per this article, the benefits of lower interest rates have been exhausted and LVR's are being re-instated. We are also building more houses and immigration has stopped due to CV. These are the reasons I believe the market will stop rising in 6 months time (June 2021) UNLESS of course interest fall further, typically below 2%

Hi Yvil, apologies if I mis understood your posts previously. I agree with you about market stability next year. Maybe that’s why government is not looking for any effective measures to intervene, they may also know it will most likely run out of steam. Thanks for answering my post without getting too offended :)

No problem at all Starr

7. Boomers would vote for National next election

There might not be many left next election, particularly if C19 gets around. They are quilckly being replaced by Gen Z.

Gen X is next in line

Why didn't they vote for them this year?

Maybe a govt backed fund to lend to small businesses at 3% might take the pressure off mortgage lending on houses?

A beneficiary can borrow 300k on a first home while a startup business owner can’t borrow $10k.

Start up businesses have a high failure rate, while houses only ever go up.

...when they are not going down.

Great article, Jenee. It’s a complex issue and you’ve captured the nuance well. The Jenga reference sums it up!

. . except for a minor fall during the GFC , the NZ property market has been on a bull run for 20 years ... 2 entire decades . . A whole generation of investors have been lulled into the mindset that house prices only ever go up ...

I think the term 'lulled' is too soft a description. They have had it pounded into their brains that the housing market will never ever by allowed to drop. The RBNZ grabbed them by the throat and slapped them across the face left and right whilst screaming "House prices will only ever go up!!!"

I would add a 7th point Jenée and I think that's what the Government and the RBNZ are really scared of, if house prices fall 20% there could well be the reverse effect of FOMO, where buyers disappear and many people start to panic and put their houses on the market to sell "almost at any price". This could then lead to falls much bigger than 20% and real trouble for NZ's economy and employment.

(For what it's worth I don't believe house prices will fall 20%)

You're correct about that Yvil though the effect is primarily felt with investors rather than owner-occupiers. Investors are more likely to sell to avoid negative equity whereas owner-occupiers (as long as they still have their job) tend to just pay it through.

RBNZ and other economists worldwide have done research on this. The basic takeaway is that economies with a large proportion of their housing market in investment properties tend to experience larger downturns in responsive to economic shocks (particularly those that have their origin in the financial sector) and take a longer time to recover.

With regards to this opposite of 'FOMO' idea, I think this is one of the most dangerous things about the govt and RBNZ essentially telling the public that property is guaranteed. It makes people think there isn't any risk (there is, historically and internationally housing markets tend to be less risky than sharemarkets, but not by as much as you'd think). So they FOMO in and they buy property they can't afford and they don't do the downside calculations in the event things go wrong because they think house prices always go up. But that's simply not how financial assets work. That's speculative bubble behaviour. Eventually you get the Minsky moment and people realize the asset they hold has risk attached to it.

Great comment

Well said. They haven't even been shy about this guarantee, they have been quite open about their stance on this, and on purpose. Unbelievable.

Excellent comment with great points. Well articulated.

Been buying and selling here since 1979. I recall periods of no/little growth in house prices but I can't recall any widespread market decline (not even with the '87 sharemarket crash), which was coupled with a statistically significant higher number of mortgagee sales. Many a time there was a 'window' where good buys could be had (usually from elderly folks who had already started building their downsize new home) - but generally never all that much panic in NZ markets.

Even Q'town at the moment still isn't a panic market.

Motu claims that between April 2007 and April 2011 the real house price (the amount paid for a house adjusted for inflation) in New Zealand fell by 15.3%. I know two people in my circle of friends / acquaintances in Auckland who were caught out by a fall nearer 20 per cent after the GFC — one had to sell at a mortgagee sale and another had to offload several rental properties from his portfolio because the bank demanded he pay back some of his mortgages to restore his equity position to one that was acceptable to it.

A home owner doesn't have to be in negative equity before the bank can decide to demand the owner's equity position be raised.

Yes it's often forgotten that prices fell on average about 10-12% after the GFC, but some people saw declines of circa 15-20%

For houses, real prices don't matter. Your mortgage is nominal, that's what matters.

Depends if all you want is same return of ‘nominal mortgage interest rate on your so-called investment.... then you are correct.

What’s the point in ‘locking away expedenture now for only receiving same buying power in x years

Indeed Kate

But what were the ownership ratios re owner V investor back then? The house market has become a speculative financial asset and we should now expect it to behave like one.

Those in Queenstown must believe we are at the end of the pandemic. Seems to me it is only getting started.

Agree, this was certainly a very concerning aspect of the government and RBNZ signalling that property investment is a guaranteed, supported investment.

That, and as one of the reporters was quick to ask, "If I buy shares am I entitled to expect that they can only go up?"

We have a bit of a moral problem in society with this approach of transferring wealth to keep property values inflating.

Another superb analysis, Jenée. And the analogy to Jenga is perfect.

Which is why I am hoping that TSY looks at a rent control mechanism to solve 2. in a way that doesn't result in a rapid price shock/adjustment.

the inability to pay could be the issue, both mortgage or rent. Somewhere down the line someone has to make the first dollar, thats where the risk is, you can create debt but paying the interest requires making/mining/ growing stuff.

Give up on the rent control, Kate.

It is categorically the worst possible response to the issue.

It is categorically the worst possible response to the issue.

Really? After WWII, there was such a shortage of housing in cities like Tokyo and Osaka, people with the means would pay 6 months rent as a 'gift' to the landlord to put a roof over their heads. The practice became ingrained and was still being asked for until quite recently.

In response to oppressive rents, the govt build public housing where rents were calculated based on income.

But why did the Japanese govt interfere in the housing market in the first place? Quite simple. They wanted to build a world-beating economy that was inclusive. That means everyone had a role to play, from the CEOs to the people who deliver noodles. This required removing feudalistic structures that NZ seems to want to build.

Thank-you!

What are you thanking him for ? His post boils down to " Japan did a good job in this space , without rent controls".

You can argue about whether Japanese approach would work here - but certainly their experience does not support a case for rent controls.

You can argue about whether Japanese approach would work here

Right. But what Kate is suggesting 'can' work. It's within the ruling elite's capabilities. Regardless, I think you also missed some of the point where we can learn from Japan: Affordable housing for all was a part of the foundation in their economic goals. Housing and related services was not the be-all-and-end-all of the economy.

And in particular, as you pointed out it was a policy initiative intended to be inclusive. Perhaps that is why their urban centers remain vibrant.

Interesting take on rent control. We already have public housing with rent based on income. Most people would know these as "State Houses" As far as I am aware Japan did not control rents in the private market.

Secondly, "gifts" are actually more common under rent controls... Can't get more in rent, add in a levy/fee/service charge, or just take cash/gifts/koha/payments in kind either at the start, periodically, or at the end of the tenancy (Common one I have seen is Tenant signing away the bond).

Yes, and large concentrations of public housing come with all the problems detailed in the US city-centric article link to above.

'Gifts' only happen when one limits rent controls to only certain properties. That is why you have to go universal with a price discovery mechanism that is publicly available (i.e., the formula based on RV). Every person renting could simply look up and calculate the weekly rent maxima on any property. And the point is, higher end properties already charge no more than the market for those properties can pay. It is the lower/middle end of the rent rack that needs controls - otherwise, we taxpayers simply keep upping the government assistance by way of Accommodation Supplements to meet these unaffordable rental costs.

"The more you try to control the economy the more that things will not turn out as expected" its a quote but I can't remember who by. It sums up your proposition nicely though

FH - Human nature is to assert some regulation into the random wild west world. Not much differ for control measure within other addiction industries. Sure, you can negate one part of suggestion. But borrowing from your quote above, it's clearly have been done by Govt & CB the past 9months.. what need to be seen in 2021 onward if their lever control keep being shifted to the same direction? or.. Not. Imagine this; you just a passenger in airplane controlled by pilot & co-pilot (Govt & RBNZ), their both combined binary decisions will only yield 4 results. Now, let's just hope that miracle in Hudson river to be repeated for NZ economy, both pilots agreed for choosing the 0-0 (downing the plane on river),.. now, try their last 3 options; 1-0, 0-1, 1-1. I'm not saying that the rest of options are false, you 'can choose the narrative of survival scenario' that suited for the other 3 options..moral of the story is the same, No control? or some sort of?

That's a really good discussion. But again, all of the issues raised in the US scenarios relate to non-universal rent control schemes, where only some rental accommodation is regulated/controlled. And yes, just like our state housing market (where rents are controlled) people will stay in them forever if allowed to. And that most certainly needs to be avoided. So the control has to have some bearing on market prices/fundamentals.

My idea of rent control would be universal - meaning, it would apply to every rental accommodation unit - based on a formula set around (RV/1000) +/- x% - with the 'x' variable dependent on the triannual RV review cycle and targeting 'x' to bring the lower income quartile (i.e., RVs in the bottom 25% of properties) in line with a 30% of median household income weekly rent maxima.

The Stockholm example might be more akin to a universal rent-control scheme. And that is really interesting. I also really get what the interviewees are also saying about the US 'sun-belt' having less restrictive planning rules allowing for those cities to grow and hence accommodation markets are affordable. And we have seen some of that in terms of our CHCH market. But CHCH had the space to grow out - Wellngton City for example doesn't and any undeveloped space there may be left are complicated engineering projects - hence they type of intensification going on in the Hutt Valley.

Lots to think about, thanks for the link.

*facepalm

I've realised you must really love bureaucracy and market distortions and really hate renters.

Economics has this great concept of welfare. It is not maximised by constraining markets arbitrarily.

Neither is it maximised by unfettered capitalism as recent decades have shown us.

She’s a socialist.... of course she’s into ‘control’

Imagine the world without some sort of 'control'

Drop by 20%? I'd buy a small 3 bedroom brick and tile unit in Warkworth. Freehold....and would become again a parasitic landlord...

The thing is when housing price drops by 20%, you don't know how much more it continue to drop. Would you buy it if it's gonna be another 10% drop? That's why people buy assets when asset price goes up, people sell assets when asset price drops.

.. yes , its the opposite of the " baked beans theorem " . ..that you buy more when the price is discounted...

How many investors rushed into the NZX to buy shares in March when the Covid-19 collapse crashed share markets world wide .. .. very few ... just when the buying opportunity of a decade fronted up .... investors were scared witless of further falls ...

If house prices fell 20% then;

- Homeowners could go outside, walk around the house and find that it is exactly the same house, and

- Investors already have that rent locked in.

The reality is that home ownership is a long term investment (bright line test for investors especially important) so like any short term investments volatility is not an issue.

Bought an investment property in 2006, saw RV go 10% below what I paid in GFC but sold in 2016 for good capital gain.

Home owners and investors have more to fear than price fluctuations- for homeowner it is servicing the mortgage (risks of job security and personal shocks such as sickness, accidents, marital issues) and for landlords it is about reliable tenants.

Yes, a fall in house prices of 20% is a possibility but that property owners need to be really worried is simply scaremongering.

There are to many other things to worry about in life. Checked under the bed lately . . . . ?

Maybe not letting houses get back into 'stupidly unaffordable' territory again is kind of the point.

As pointed out in the article, when house prices fall people tend to spend less. Whether this is rational behaviour or not is up for debate, but it happens, and has impacts on the wider economy.

The whole "heads down, tails up" approach of just continuing to faithfully make mortgage payments while you wait for the inevitable house price recovery only works if you have a job to go to.

P8... I am so confused and have no idea of the chances that property will drop by 20% but feel the odds are way higher than most think. But I do think if prices came back 20% the chance of further drops of ANOTHER 20%+ could be around 50/50 or even higher (as a complete guess). If the Govt, the RB and the banks have information which shows this to be feasible or even likely, it would explain why they are so worried about any sort of meaningful drop.

We have never seen huge falls in NZ property but does that really mean we never will? As someone famous said "only a fool thinks 8000M mountains do not exist just because he has never seen one".

Karl

There is no certainty as to the market. The 20% scenario discussed in this article is simply one of “what if?”.

Not sure what you refer to as RB and government having information as to what fall is feasible. About a year ago RB carried out modelling to stress-tests banks for a variety of scenarios from about 20% to 40% (from memory) fall in house prices. RB made it clear that this was not about likelihoods but simply that - a test simply to determine what would happen if it did occur. (They did indicate banks could handle that.)

What is your rationale for a 20% fall, and why then a likelihood of 40% fall other than a guess.

P8...I have no idea what will happen but a 20%+ drop could be caused by:- A. interest rates rising B. more sensible immigration C.income to price ratio DCovid 19 problems E. Global economic problems F: a number of others we have not even thought of.

It is a guess that they have info that they are not making public but it would be surprising and remiss of them to have not done very in depth modelling and studies that go far further than a simple stress test. My main point was that IF prices did fall a little (say 10 to 20%) it would be logical to assume that the probability that they would continue to fall, maybe much much further than 20% is a likelihood that they would be aware of. After all, although they do not inspire confidence (in most financially literate people anyway) we do need to give them (and their research team and advisors) some credit. A good analogy may be that once you slide 20M down a snow covered mountain, halting the slide may prove much harder than many expect, unless of course they have personally slid down a mountain before.

Karl, if house prices dropped 20% the government and the RBNZ would act drastically to support house prices from falling further, they have made no secret about this

Yvil, I think if investors lose confidence in the market, no amount of intervention by government and RB will prop up the market. The interest rates are already low, I guess they can only remove LVRs if that was to happen. 20% drop still very unlikely but probably will happen in CBD only at this stage

... that's my concern too ... the " housing put " to underpin prices ... further strengthening the Kiwi mindset that property is guaranteed to only ever go up ...

Agree, and then the question would be, could they stop it.

There's no doubt the government and RB can stop a hypothetical house price slide, just imagine negative interest rates where you get paid to take out a mortgage, that a would get people borrowing! I hear you say "but that can't happen", that's not true, we never thought printing $100 Billion was possible, 5 years ago we never thought an OCR of 0.25% was possible, now we're talking about a negative OCR. We have to be more open minded of what is possible

The OCR can go negative but bank lending rates obviously cannot go negative. The bank is never going to pay you to borrow money, they make their money in the difference between the rate of them borrowing and lending. Orr just want negative OCR rates to try and push the interest rates to near zero. The whole monetary system is just a farce when you think about it, its a confidence based system and if that confidence ends its all over.

"The bank is never going to pay you to borrow money, they make their money in the difference between the rate of them borrowing and lending" If house prices were to tank the RB drops the OCR to -3%, the banks pay the borrower 1% et voilà. Not likely but possible, open your mind Carlos

I don't think the government and the RBNZ can do much to prevent house prices from falling further. That's why they are so scared and not doing anything about it at the moment. So when house prices drops, both of them want be blamed. And they can find excuses like "Oh it's a free market, what do you expect? It was your own choice to invest, not us."

COH - that’s a good point , I too think government is taking a back seat so they don’t get blamed for what could come next year

As I have said a couple of times recently, as a country we need to move on from the historic concept that we are a property-owning democracy. That has been destroyed over the last 20 years and won't come back. Even a 20% house price decline will make minimal positive difference now to home ownership rates and will come with plenty of costs.

The best thing we can do is get the rental market functioning better. The new tenancy laws are a good start. We also need to keep building lots of townhouses and apartments.

In this new reality - if you accept it - investors actually need to be embraced. I would like to see policy that incentivizes investors to buy new property rather than existing.

Disagree - new tenancy laws simply tip the balance even more in favour of tenants and will have unintended but predictable consequences. Anything less than equal responsibilities for both parties to a rental agreement will produce more problems and state housing demand will grow exponentially and supply will not keep up with demand and the taxpayer will effectively fund the costs including those caused by bad tenants.

Don't agree.

But I don't think the law should go any further in favour of tenants, that could certainly generate unintended consequences.

If the tenancy laws are so bad for landlords, why then have so many investors been buying up over the last 12 months?

Actually putting in place laws such as exist in Germany seem to do a lot of good for societal stability and increasing landlord professionalism:

https://www.interest.co.nz/property/75809/getting-renters-rights-german…

We've seen bad renters TV programs in UK, OZ, NZ.. the difference so far? you can see the Slum landlord part in UK - apparently, they don't exist in OZ or NZ? - need more expose on this, so a real balance can be observed, 'not the balance view' from the so called bias towards both side. Tip toward who? and why more property investors buying? sitting empty? or rent to family? or..

Fritz I disagree the tenancy rules a good start, they are an appalling set of regulations that distort the relationship between parties even more so expect unexpected but predictable consequences. Typical of a Govt with no real experience of life outside bureaucracy and unprovable academic theory and a lack of common sense of peoples reactions. Tenancy rules that depart from equality of responsibilities and enforceable should negotiation fail will result in unnecessary disputes and unhappiness both which lead to more unintended consequences.

Here's one key takeaway: Tax payers money is being used to fund property investors in the form of the accommodation supplement to the tune of 372235 households. That needs to stop. Investors of property already have the privilege of more than one house, if rent is unaffordable, LOWER IT. My tax contribution is not available for landlords to collect. Solid regulation of rental prices at their current rate and ability to raise in future is an obvious place to start.

New Zealand needs to phase out the Accommodation Supplement - it hasn't done what it was meant to do - which is help low-income renters. Instead because of the power imbalance between landlords and tenants they have just used it to increase rents. Unfortunately because of the power imbalance if the Accommodation Supplement is suddenly cut the cost will be carried by tenants not landlords.

The way out is to start a massive public housing build programme - KiwiBuild for renters - 10,000 houses a year - properly funded - say $2billion a year (the same as we pay for the Accommodation Supplement). Not a few thousand highly subsidised state houses targeting the most destitute beneficiaries. Lots different sort of schemes targeting different parts of the low-income end of the housing continuum, using the Community Housing Sector. It wouldn't just provide affordable rentals for beneficiaries it would target low-income workers too.

Also NZ should set up public housing schemes like they have in Austria where if the tenant contributes 5% equity after 10 years they have the right to buy their home. In Austria they are allowed to use their government subsidised saving account. In NZ we could let renters use KiwiSaver.

In a decade NZ will have increased its social housing stock from 70,000 to 170,000 houses , in two decades 270,000 houses.

At some point - after a decade or two - the Accommodation Supplement would not be necessary and could be phased out.

r-mc & Brendon - the fundamental cause is insufficient net income due to excessive Govt expenditure and lack of real productivity growth over decades masked by immigration and debt creation - this is not going to end well in fact it will be very ugly.NZ has just voted for more of the same so do not expect improvement.

That doesn't make much sense to me. Do you have a logical explanation for your conclusions or maybe some comparative data?

Correct in part, but the more economic digging you do? the more you can find those intertwined debt binge all over in NZ, as a major get rich 'quick' scheme. The past decades or so NZ tend to flip-flop voting in 9yrs cycles - ideally, this should create some sort of balance walk, between left & right foot - but now, they no longer walk in circle left, circle right, .. it's zigzagging all drunk binge on properties, soon it will be ended up in ED.

Brendon, my view has changed on the government building affordable as well as social housing. The social housing waiting list is so long that that needs to be their main focus - the truly destitute must always be a government's biggest priority. Even getting on top of that will require a massive ramping up of house building.

Hence, we need the private sector to do the heavy lifting in terms of the (non-social) rental market.

Fritz I could be convinced to change some of the focus. Actually I would want there to be a Independent Housing Commissioner and they should have the ability and resources to assess what type of social houses are needed, as well as where and when they are needed, to meet the goal that rent should be no more than 30% of income. I certainly have no problem with the government very, very quickly building long-term housing for the 6000 households living in motel units - that should be the highest priority. I also have no problem with ramping up the state house programme -but the Income Related Rent Subsidy which funds it is really expensive - tenants only pay 1/3 of the costs and IRRS pays 2/3.

A major reason that the public housing waiting list is ballooning is because rents are too high and they are inflating faster than wages.

A bigger public house build programme covering a wider part of the low-income housing continuum will bring down rents in the wider market faster.

Also a wider spectrum of public housing types is easier to integrate into developments so the housing is indistinguishable with general market housing - important to avoid slums etc.

Our government is ideologically opposed to building very high density housing as state housing. Something about becoming a ghetto (like Singapore’s low cost HDB units)

I reckon up to 6 stories around rapid transit would be very popular with the whole housing continuum ( including different types of social housing) if a variety housing sizes and types were provided. In this sort of more 'urban' as opposed to 'suburban' environment a mixture of socio-economic groups would more easily fit in - at least that is the experience in Europe.

Fritz do you have any thoughts how the private sector can be encouraged to undertake more build-to-rents?

Not really but I would have thought that tax incentives could be an option.

At least theoretically the model sounds good. A return of at least 5% is doable.

I understand that they need scale ie. the developments need to comprise at least 30-40 dwellings. In this respect, the NPS-UD should help facilitate more development of this scale on suburban sites.

Fritz

Overseas this has been achieved via strategies such as halving the tax on rental income or having a fixed rental income tax rate of 10% ish. This causes every man and his dog to want to become property investors which in turn makes all the developers scramble to cash in on the wave of demand. This ultimately leads to an oversupply of rental accomodation available and a corresponding drop in rents. All paid for by those who can afford to buy investment properties.

The problem is that to the short sighted it will look like a gift to property investors.

Good points

I prefer the Austrian model. Various capital incentives to build if you are a registered limited-profit affordable rental provider.

I think NZ has had enough of giving property investors subsidies with no guarantee it will not be capitalised into higher house and rent prices.

My fear with community housing in NZ is that we simply aren't big enough to get any scale in the sector.

Austria seems to have managed and their population is just under 9m, so not that much bigger than NZ.

NZ has some pretty big community providers already because Councils restructured their housing into independent community housing trusts. Some well capitalised iwi might also be interested in supporting the model. Churches often have land... some of them may be interested.

It might also be possible to allow KiwiSaver providers to go into non-controlling interest partnership with community housing providers...

I agree scale is important. But so is competition - even in a non-profit business model environment.

Well that's getting close to double our population, so it's a fairly significant difference.

I am not saying it can't be done here, but I think scale is a big challenge for us.

"New Zealand needs to phase out the Accommodation Supplement"

Absolutely

Its just a market distorion of epic proportions

subsidising people to live in over priced cities and hand landlords a capital gains bonanza

Agree - #rentcontrolnow.

Technically speaking there is no such thing as taxpayers money as taxation only cancels money. Only the government and the banks have the authority to create money and anything else would be classed as counterfeiting.

Great article. Good statistical digging. The housing crisis root cause is politics. IMO if our political decision makers are choosing not to allow house prices to fall because the housing market is too big to fail then they/we have a duty to care for those losing out from that outcome. Primarily that is renters paying too much rent but it also FHB who face a difficult choice of paying high rent for insecure accommodation or mortgage slavery because they over paid for housing. Given these poor options it is not surprising that so many confident, talented, hard-working... kiwis leave NZ.

Housing in the Silicon Valley is phenomenally expensive, talent does not leave the valley because of it. The main reason talent leaves is over taxation of a very small pool of net tax payers and a shallow capital pool caused by that same taxation. You need lower taxation to enable more capital accumulation (greater inequality) to facilitate innovation and development as well as a lower minimum wage to enable our products to be competitive.

At present the top strategy in NZ is to accumulate capital via real estate and then use that capital to start small businesses. Once your business reaches a certain size you switch to being an American company with manufacturing based in China.

Essentially we need inequality to drive productivity, not just via making the extra effort worth a bit more relative to the status quo, but also via facilitating private capital growth which can be invested into productivity.

People leave for a host of reasons, but high taxation generally isn't one of them. Our taxation isn't even that high.

There is massive migration of people from high housing prices in California to low housing prices in Texas.

Texas also has relatively high property taxes and aggressively effective planning legislation. The US is a fascinating place to watch the effects of individuals states legislation.

House Bill 2439

HB 2439 prohibits cities from directly or indirectly restricting building materials. Any material that is recognized by one of the three national building codes within the last three code cycles can be used in construction.

The intent of this legislation is to keep construction prices down in order to provide more affordable housing.

House Bill 3167

Also known as the ‘Shot Clock’ bill, HB 3167 will have a huge impact on development. Cities (and counties) now have 30 days to approve, approve with conditions, or deny a preliminary plat, general plan, final plat, replat, development plan, subdivision construction plan, site plan, or land development application. If the City does not meet this timeframe, the plan is automatically approved.

Very interesting. I like the concept of automatic approval if council does not make a decision within 30 days.

That would certainly force councils to develop much more efficient processes.

It might also mean that they decline more, but that is not necessarily a bad thing.

True about the CalExit, but multiple causes, Brendon:

- Decades of green gubmint with high taxes, failing infrastructure and dashed hopes (e.g. high-speed rail to nowhere)

- Sanctuary state (especially to Mexicans and homeless) attracted by State largesse causing massive immigration with the inevitable cultural changes and resultant discomfort

- Sensible (by comparison) State gubmints in most neighbours, so a constant pull eastwards by comparison with the nuttiness (e.g. San Franpoopsco) so evident on the streets

Man, you are a real 'gubmint' hater!

Your point 2 - so why then have many migrated to Texas which has it's own high Mexican population?

I didn't pick that vibe - just seemed to be stating the facts.

Mexicans are mainly illegal immigrants ie they are Mexican nationals. Hispanics could be US citizens or Mexican citizens. California now gives shelter to illegals, whereas other states still require immigrants to legally apply for residency, or will arrest them if they enter without approval. However, in most states, the private sector welcomes the cheap labour regardless.

The high immigration from Cal. to Texas for both business and families, is because of the price of land which means cheaper commercial development, cheaper housing. Businesses can be more competitive in price and can if needed pay their employees more. Either way the employees have more disposable income due to affordable housing.

This article shows how much more a reduction in house prices would give homeowners in the hand, money which can go for more important uses rather than paying a nonexistent amenity benefit on their property. Approx. 1/3 to 1/2 of the value of a NZ property is non-value added due to uncompetitive rentier policies.

Cheap Mexican labour is a factor in Texas's lower construction costs.

As I said, the cheap Mexican labour is welcomed in all States. Who do you think harvests Californias Vege crops?

Last person I know who headed to the midwest from LA did so because of water shortages and wildfires. Nothing to do with Mexicans, taxes or nutters - they exist everywhere in the US!

You don't need inequality to drive productivity, you need Research and Development spending to drive productivity.

There are so many countries around the world where small elites control the power structures of their nation, take all the existing resources and use those resources badly. Russia, most of Africa, most of South America are examples of high inequality driving low productivity.

Silicon Valley is a nexus of US defense driven research dollars, university talent and enterprise capital. Inequality comes after the tech elites make their money not before.

But its only the higher echelon of the tech elite that own a property there - the rank and file are living on the streets (literally);

https://www.bloomberg.com/news/features/2019-05-21/silicon-valley-s-sha…

https://www.kqed.org/news/11751183/what-its-like-to-live-in-an-rv-and-w…

https://www.topic.com/life-inside-the-rvs-of-silicon-valley

https://www.businessinsider.com.au/inside-the-silicon-valley-van-dwelle…

We always welcome good grades Kiwi healthcare pro/new graduate, to join/contribute their productivity... in the location where everything still feasible & makes senses (OZ). Ensure to do the due diligence first, plenty consideration for sure.. but don't wait too long, NZ isn't worth it for the young healthcare workers (doctors, nurses, specialist, pharmacist, dentist, physiotherapist etc.)

What of the other dimensions?

You say resilience, not resilience more a symptom, the result, the derived outcome of massive flooding of bank reserves & liquidity, leading to further increasing availability of credit.

There is a lenders strike against productive borrowers, farmers & small & private business.

There is great over regulation coming in upon agriculture, fundamentally wrecking the industries ethos (and measures of value).

There is the destruction of tourism businesses & gutting of export education.

The regulation & policy settings encouraging banks to create funds against residential property.

If the above were adequately addressed, enabling jobs, rising productivity & incomes, the house market symptoms would be lesser.

The funniest thing is that the Ardern governments should enable the housing mess, as it is diametrically opposite & opposed to every policy inclination they & Helen C ever had.

They are all impostors, if it was ever a real thing.

Excellent article, Jenée. Love the jenga analogy.

Playful, but incorrect.

The article assumes its only the borrower, the little guy that cops it.

Look at Iceland, they let the banks go, not the borrowers.

Look at Rural Bank crisis here, the borrowers were bailed out.

The narrative that its the borrower at fault its the borrowers failure.

It is just a narrative.

History shows banks have always failed, why should now suddenly be different?

I struggle to imagine our politicians emulating those in Iceland rather than those in Cyprus or Greece. The banks will threaten and the politicians cave.

Austerity RS? like Greece.. C'mon, we're talking NZ here.. with the majority of Red band at the helm. Our current shine solution is proven (for now), just keep printing it.. at will/when you need so.

On the topic of promoting renting as a better option, it will be interesting to see if much progress is made in the next year or two on 'build to rent' initiatives. Shamubeel Eaqub seems big on it.

Disposable Income = Wages - (Taxes + Cost of Living)

Employers pay for the cost of property prices rises. It's in the wages they have to pay to attract employees. If Wages become ( more) uncompetitive in a Global World, the jobs exit stage right, overseas. (China is finding this out as jobs head off to Vietnam etc. Why have they had to increase their wages base? The Price of Property there).

The biggest factor in the above equation? "Cost of Living". And the biggest component of that? Housing/Property Cost.

New Zealand, amongst many countries, in the process of pricing itself out of business.

Lower property prices allow Employers to provide an increased Disposable Income; remain globally competitive and employ more workers.

Employees are able to better allocate/diversify Disposable Income as it increases, instead of having to channel it evermore into one category.

Lower property prices are in the interest of Employers, Employees and the Country as a whole.

I agree NZ housing market atm is a train wreck. It is bad for productive businesses. It discourages productive workers. It is ripping apart the social fabric of the country.

Affordable housing should be a public service that government ensures is delivered one way or the other. It is as important a right as free education for children and superannuation pensions for the elderly.

Yes, #rentcontrolnow.

If there is a mass exodus from landlords - no prob - government can buy up the dwellings to add to the state stock (provided no FHB wants the property) - and gee, they can do that via social credit, i.e., no new taxes needed at all.

Where is Mike Kirk to trot out some cherry picked numbers and tell us the 20% drop is already happening?!?

Bit silly. My numbers are usually for sales in Auckland.

Prices in Auckland, as Yvil has intimated above, will not stop rising til rates stop falling.

That is when end game begins.

2011 - 2020, rates come down and down. Can that continue? I doubt it and certainly not at same impact, as zero approaches.

5m mania is cooling and will cease in mid February

He mainly reports on volumes and pace of transactions and provides good data.

You want a hand picked number?

Google "fed global money supply last 20 years"

Then "all time nz house price index (same period, median prices will do).

Compare the two graphs.. And have a really really good think.

The minute interest rates and money production slows down, all Capital assets will start to contract, or at best plateau for a long time. Shares, housing. All the same.

In nz our tax laws and policy benefit housing as a first choice investment. But its all just one big global asset bubble. housing is just our drug of choice (same as Early 2000s usa re sub prime risk)

But the key point is its not just out little bubble. We are but a drop in the bucket of Global finances. One thing that always amazes me is most kiwis attitude that we are the centre of the world. In reality financially speaking we are feathers in the globalised wind.

Global finances are stable only via massive QE programs, we already carry too much household debt.

And we respond to this risk by taking out even bigger mortgages.

Just a bit of anecdotal evidence to support the reality of housing mania out there. My mate listed his 4 bedroom, 850m2 property located in GreenBay last week. Received 19 offers in 7 days and sold to a family today. He didn't even take the highest offer either.

it's like the Lockdown when people were fighting over toilet paper, now it's houses.

I tried to convince my bank to let me use my existing stock of toilet paper as a deposit to borrow money so I could buy more toilet paper in hopes that I could sell it later for a tax free profit. Weirdly they said no.

We sure were quick to see stores limit purchases of toilet paper when it became necessary, so that everyone had access to a basic necessity, rather than outright allowing people to purchase up big and profit by selling it back at insane prices to those who could afford them. They'd have rented it out too if they could.

It was only a limit per transaction. No limit on total ownership.

Ha! my partner and I put in one of those 19 offers. The ninth house we’ve lost since June. Trying to buy a home in Auckland is truly one of the worst experiences of my life.

We bought off plans a couple of years back. Not without risk, but it was certainly nice not having to deal with auctions and tenders.

I feel for you. And I'm curious as to what keeps you in Auckland?

My partner’s family is here and with her parents getting older and our desire to have children, and have them be near grandparents, we are really adamant about staying. We are in a relatively fortunate position compared to many and I am sure we will eventually get something. It is mad though that we have been priced out of suburbs that until six months ago we could have easily afforded and which have been working/middle class areas for decades, such as New Lynn.

All the best - what we've always found is that the one you get is the one that was meant to be.

I am in a similar situation. Wellington is soon to become a million dollar area city, joining Auckland and Queenstown. So not only have our generation been saddled with huge student loans and user pays, we now also have houses that cost multiple times of our income more and previous decade. A new house in my area is essentially a million dollars + now, and this isn't Auckland. The older generations will likely end up paying with increased costs as this could lead to massive inflation in the future. People in the property game don't see any problems and claim this is all normal and homeownership percentages haven't changed from historic numbers, and they seem to be pushing for things not to change. But something has to change. The best thing IMO would be the actual state houses are build, and first home buyers can buy them cheaply.

In any ponzi, by very nature it is hard for anyone to think that house price rise will stop, hence this is a hypothetical question today but could be reality in future.

And what lets people play is the availability of credit, ever increasing, driving bank valuations & lending amounts up up & away.

Remember we have had housing booms at double digit interest rates too - credit supply was as much as you want).

Another wishful thinking and distraction.

Everybody goes down if house crashes.

Big correction will happen 20% but price will shoot up 50% first...

If house prices have risen 20% this year, then if they drop 20%, I can't see how banks would be affected much. It would likely only only affect those who have purchased most recently who may end up in negative equity, which I would think s only a very small percentage of loans. Plus banks should be requiring 20% deposits anyway, s they should still be in positive equity if people were forced to sell. Or am I missing something. I think the worry is that they will drop 30% +.

Lack of supply and record low interest rates, and media hysteria over FOMO are almost solely driving these dramatic rises. THis mixed with peopel not being able to travel overseas, so they may have a bit more money.

Yeah the stress tests make little sense in that context.

Where are the positive results of prices rising 20%? And shouldn't they to some extent offset the potential for future falls? Why isn't the windfall being used proactively?

It just seems a bizarro world in which we require as of right, 10%+ annual house price increases, but if any of that increase is reversed, we're all doomed.

House prices would have to fall 67% before I got into negative equity. But even if they did I'm not worried- I plan to live here a long time. Sure, if circumstances changed I might be in trouble, but then again, so would everyone else - the banks wouldn't want to foreclose on too many people because it could lead to prices falling even more, increasing their losses.

So I figure the missing part of the analysis is what proportion of people in a recession would usually have to move outside their area (and therefore into a different market)? Then we would have an idea how big the negative equity problem actually is, not how many people would have a paper-negative equity.

Prices wont fall

Interest rates can only going one way

the system cant unleverage; instead we must add more debt & leverage

we need to keep raiding the balance sheet to fake income

But at some point soon, the whole charade will snap because of producers going bust

So its a matter of how long the system can tolerate insolvent producers

I agree Ham n eggs, what people need to focus on is the trigger to the end on the financial system we have been running with since 1971. You would have thought that where were were in the cycle combined with a Pandemic that is still far from over, would signal a crash, but the government jumped in and saved the day. The big "Some point soon" question is exactly when ? I think we need to ask the question, can this just not go on forever ? The money doesn't really exist does it ? in fact it is available in unlimited supply.

yes the money is unlimited supply

but the (annual) output from the world economy is basically fixed

so all this new money chasing the same old output ... its a recipe of inflation (somewhere in the system; read Asset prices) but comes with the kicker that real incomes are losing spending power

ie a haves and have nots situation and ultimately low prices for commodities (on the back of low affordability for the stranded masses) - see lamb prices / beef prices / oil prices (at the producer level...

Do we just keep printing more and more to support more and more people over time? And without negative effect?

We're basically increasing the proportion of people on welfare. We push massive welfare into property investment currently through this, effectively putting the load on those who follow behind. This reduces those following folk's ability to save for retirement over and above paying for their house, as they don't get the free money that those who bought earlier have received through our inflation of assets.

Or do we just keep devaluing money, somehow without consequence? Presumably at some point we have to generate some wealth with which to power this? We may have a magic money tree currently but do we have a magic wealth wand?

Nice article. Now do one if house prices rise another 20%, which is much more likely to happen.

Here is basis for my forecast of 18th February being the crucial inflection point for housing market.

It is mid summer and no foreign tourist money coming in, at same time that government stimulus is not repeated and mortgage support going to be withdrawn altogether, + no likely further cuts to interest rate. Plus LVRs fully reintroduced in March.

https://www.stuff.co.nz/business/123792654/outgoing-tourism-new-zealand…

What basis do you have to suggest that stimulus will not be repeated and mortgage support withdrawn?

Yep my prediction is if things are still looking a bit shaky, the stimulus will just be extended. Really this is all just a sign that we have got your back so just go out and spend. Americans just got another USD$600 handout, really there is no end to it, just extend and pretend it could go on like this for years.

Trump says he won't sign that package unless they up the helicopter drop to $2,000 per taxpayer.

11858 households missed mortgage payments in the week ended 11 December.

2.73 bln of Mortgages remain on full deferral. Approx 11,000 households at the average of stated weekly averages. More deferrals being granted each week.162 in week ending 11/12.

Will RBNZ kick the can again in March or allow some households to be placed into forced sale situation. A few thousand forced sales could push the market south. Combine that with excess of new builds coming to market in Auckland with Zero population growth. Double dip

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Statistics/tables/c6…

RBNZ + Banks will allow those deferrals to go on as long as needed for the household to either quietly sell the house (not as a mortgagee sale) or earn income sufficient to resume payments. Banks don't even have to report these deferrals as non-performing loans, so they aren't required to hold additional capital against them. That's how little they care about the scenario you are describing.

How do these stats compare to pre covid times? In my town, any new land is quickly being snapped up, but hardly anything is actually being built, and there seems to be a lack of builders. It is now just as cheap to build as to buy an existing house in my area. Infact some older 10 years houses work out at a higher sqm rate than it costs to build new. But the problem is lack of good quality builders.

If you were self-employed why would you re-start a deferred mortgage payment - would it not be better to perhaps reinvest more profits (i.e., upgrade plant/machinery/vehicles etc.) so the books remain at not much better than break-even and/or still below the pre-COVID earnings threshold?

In other words, I just wonder how many of those deferrals are from households that lost an income through redundancy and are finding it difficult to become re-employed. That's the worst-case scenario for a homeowner.

They will extend mortgage support. I'll bet my non-existent house on it.

The business model of most landlording needs capital gain. So many would exit if that was not going to happen. Why would you stay?

More home ownership results, which would be a great thing.

So long as the rent covers the interest costs of your mortgage, you're better off landlording than not.

Landlording, eh. Here are a couple of better terms, imho, for that, "people farming" and "economic cannibalism"

RBNZ ought to do something about interest-only residential mortgages - ban perhaps?

Absolutely agree. That is stroke of the pen stuff that would make a huge difference to owner occupiers families and FHBs everywhere. If they won't do it, we know for sure that the fix is in.

Yes.

Pretty incredible that we do nothing to address this, yet at the same time we shovel welfare money through to support rental yields.

Maybe think of what is causing the friction that is withholding such action addressing, and consider the energy that propels the shoveling.

Government removed the option of interest only loans in horticulture related mortgages (kiwifruit orchards at least) around 5 years ago on grounds of financial stability. I recall ANZ pushing clients back onto interest plus principal payments. So there is a precedent to do the same in NZ housing sector - at a minimum in respect of investment properties and non-owner occupied properties.

I reckon they will extend until NZ is vaccinated.

There is a language thing here. "Market fail" is not a negative thing. Falling prices would be great for those seeking houses to live in.

Falling house prices should be called "market success"

Just saying

Excellent writeup Jenee.

Thank you for the marvellous work this year.

You are a star of informative journalism.

Merry Christmas to you and yours.

it wouldn't matter if there is a drop of 20%... prices are still too incredibly and excessively high, which is stupid if the aim is to encourage the young to remain in NZ and promote a fairer society for all. Im telling everyone I know-mostly young professionals...get your arses over here PRONTO. NZ is in the social mess it is currently in, due to the greed of the wealthy- treating property as investments to make them more money, as opposed to the push for homes for all. Like a domino effect, not having a home leads to a road of poverty, renting and inabilty to get ahead. Now property being out of reach of the majority, the future professionals and trades (that would be the future of a society- future leaders, essential workers, tax payers) have to go to foreign shores to be able to do well. Come to Perth- get double the wages and half the living costs. Buy a new home for $320 k...NZ- Nose is cut, spite the face...

That's a great plan, except you're in the @rse end of nowhere with the cultural depth of a puddle and an economy based on digging dust out of the ground and shipping it to China. You will be stranded there, an analog city in a digital world. Margaret River is nice however.

Thats absolutely wrong. You dont know what you are talking about re: Perth. Ive lived in both countries and I can say with great certainty, that Perth is waaaaayyyy better than what I experienced in NZ. Its a beautiful city, with the best beaches in the World- huge wages and our family are financially much better off than the terrible experience I had in NZ. And that not including the absolute concerning racism that we faced. I do agree with you-that Margaret River is awesome- looking forward to heading down there over the holidays! Lastly Te Kooti- you are detracting from the actual issue- the push of the younger generation that are faced with poverty in NZ, or opportunity elsewhere.

Good points. I lived in Adelaide, another city kiwis and sometimes Aussies deride. It's a great place, it has everything you need in a city whether it's the arts, sports, or food and wine.

Much lower cost of living than Auckland.

The only real downside of Adelaide is it's economy is a bit sluggish and job opportunities a bit limited.

Fritz- re job opportunities... Its about to BOOM in Perth. If you are in construction or mining (or similar roles)- try Perth! Iron ore is at a nose bleed price of $175 US per tonne... We cant get enough workers...

B2P I didn't say Perth didn't have nice beaches, I said it was in the middle of nowhere with a coal/iron ore based economy. You may be very happy there - but all that glitters is not gold including not being able to vote or receive a state pension etc. You will always be a second class citizen.

Also, if wages are higher and houses are a lot cheaper - how is that possible? Australia builds a lot of subdivisions a long way out with expensive toll roads into the CBD - that's why. You will find houses in desirable places to live are way more expensive than NZ - Sydney Eastern Suburbs, Byron Bay etc.

I personally find NZ a far more beautiful country, a greater variety of topography. However I see where you are coming from and I'm sure NZ is the poorer for your leaving.

Construction costs are much cheaper in Aus, that's a key reason why the housing is cheaper.

Australia is a beautiful country, in different ways to NZ.

Te Kooti- the issues that you raise are very, very minimal compared to the significant issue here. Real issue- We are forced to go overseas because we CANT STAY IN NZ. Our family is lucky in that the place we live in- Perth, is an incredibly fantastic place, where the Government (who are flush with money) look after you and there are plenty of jobs. Iron ore is at Boom levels- $175 US per tonne. Get over here young NZers! They love us. Talking about second (or third) class citizens- try being a Maori in a rural town in NZ. My wife couldnt believe the amount of racism were we stayed. It was F@#ken disgusting. In Perth we are treated as NZers. NZers are celebrated as great workers. I love being treated as a normal citizen.

Maybe it wasn't clear, but I'm in your corner. Many Maori do well in Australia and part of that is getting away from the crap in NZ, were you in the South Island? I refuse to visit the place - in fact I'd happily cut it free.

The point I was making is that houses can be cheaper in Australia, but not in the more desirable parts and often expensive commutes are inbuilt.

Unfortunately it was in the Nth Island...a well known red neck community! I've had my fair share of being chased by skinheads in Chch on a Unversity trip back in the 90s... so I agree with you.

Being Maori in Australia is amazing...we are really treasured here. Culturally and our reputation as hard workers...I know many that have flourishing businesses in Perth.

Houses- we are currently looking at Eglinton in Perth. It has a train station being built 5 mins walking distance...45 mins into Perth city where I work. You can get houses 5 yrs old for $300-380k. Huge houses. The beach is 5 mins walking distance. Everything is dirt cheap... our family of 5 eat like kings for $270 a week. We fill our car on tues for $1 per ltr ...$43 to fill our car up! And this is what is to be the downfall of NZ- the younger generation are forced overseas because greed has priced us out of the market...

Good luck and Meri Kirihimete!!

Meri kirihimete kia koe hoki Te Kooti!

40% of the world's Li comes from two modest holes in the ground (Greenbushes and Mt Cattlin/Ravensthorpe), with Perth as the service town for the former and Esperance for the latter.

Depending on who you listen to, Li has a Yuge future.......

yes...worked in the Pilbara mine site mining lithium for 1 year. Prices have been dropping for a period, but is on the rebound. With electric cars in the mix, possibly a good time to invest in lithium....

Good summary. I would note that there would be a substantial difference between building our way out and a crash. If you built more housing (e.g. if government changed the way land was allocated for development and reformed the RMA) it would likely tend towards reinflation of our economy, so wages would rise and so would rates. In the event of another crash RBNZ would have to jump into more QE and we would continue a deflationary trend. Whatever we do or don't do we have made a choice about the future of New Zealand.

My advice to young people is to look towards countries where they will have a better quality of life. Australia is probably back on the path to economic growth, many European countries are projecting declining populations due to low birth rates and looking to attract young people, Canada and the US are easy if because they speak English. Just don't sit around waiting for change that is not comming. Best of luck!

Yeah if you are a middle income person / household then places like Aus and Canada can offer a much better quality of life.

It’ll be like October 1987. A bunch of divinely entitled people will pack meetings in community halls and whine about how “this bluddy guv’mint has gotta do something about it”.

Happened more recently too - recall those pensioner meetings regarding Blue Chip.

The fact is that house prices do fall. There are also booms and busts, these things go in cycles. We only have to look at history. But people quickly forget. The US had their subprime housing crisis less than 15years ago. The problem is that the government has allowed prices to increase too much too quickly after the covid lockdown, causing a bubble, which is more likely to pop, and cause prices to drop significantly. Just needs an external shock like unemployment rising caused by covid around the world. Is the government going to print money and pay everyone a living wage if they own a house and lose their job? If people buy other asset classes, like shares, do they only expect they will go up, and never down. Imagine if the government said that people always expect shares to increase in price at a modest amount, and had policies to prevent them going down, then everyone would be buying shares in NZ companies rather than houses.