Summary of key points: -

- Pullback in the US dollar value expected to be short-lived

- No surprises expected from this Wednesday’s inflation numbers

- Lack of skilled immigrants hurting the NZ economy

Pullback in the US dollar value expected to be short-lived

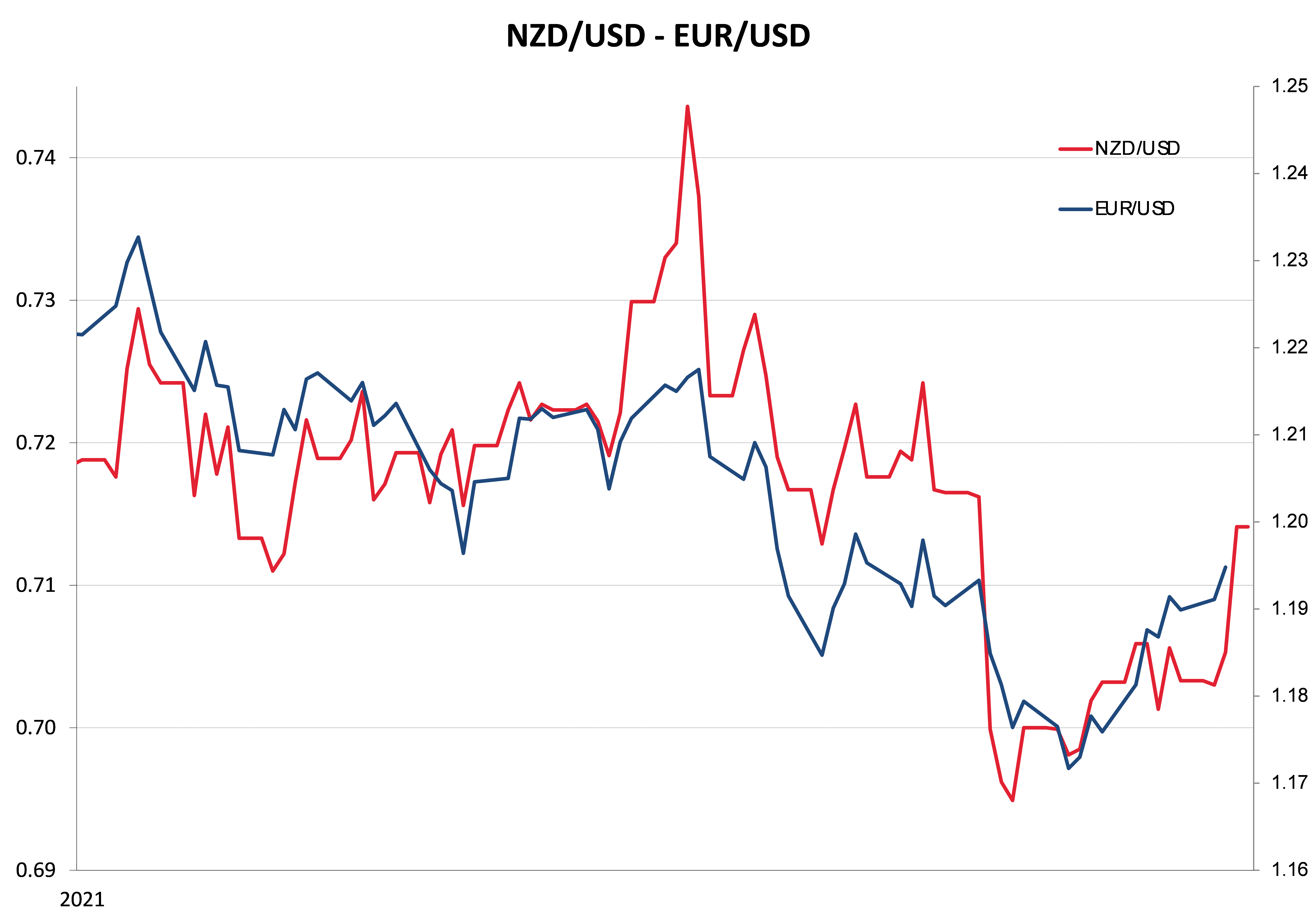

Until a week ago, the expected trend of a stronger US dollar against the Euro on global FX markets was very much on-track with increasingly stronger US economic data propelling the EUR/USD rate from $1.2300 in January to $1.1720 on 30 March.

The pullback in the USD to $1.1980 over this last week does not represent a fair or accurate reflection of the current economic performance of the US compared to Europe.

As anticipated, all US economic data has printed on the stronger side with March numbers for retail sales, manufacturing, employment, consumer confidence and housing all well above prior forecasts.

Listed companies’ earnings reports have all been stronger on Wall Street as well, underpinning and evidencing the impressive recovery in the US economy at this time. Whilst some business confidence measures in Europe have improved, March and April economic activity is again suppressed by partial Covid lockdowns.

Over coming months with the rapid vaccine roll-out in the US allowing inter-state travel and family vacations for the first time in a year, the leisure, hospitality, hotel and gaming industries will be dramatically rebounding in terms of economic activity. In turn, that means large increases in re-employment in the lower-end jobs that were laid-off when the Covid pandemic struck last year. Watch out for the Non-Farm Payrolls jobs increase for the month of April to be a “whopper” when the data is released in the first week of May.

What caused the USD selling against the Europe that drove the rate up from $1.1800 to $1.1980 last week was a downward correction in US 10-year Treasury Bond yields.

The 10-year yields reducing from above 1.75% to 1.55% and therefore reducing the margin over the European bond yields and making the USD relatively less attractive. The dramatic increases in US bond yields this year being the main reason why the US dollar has been stronger against the Euro.

The Federal Reserve was partially responsible for causing the reversal back to 1.55% in bond yields as they reiterated their commitment to keep their monetary stimulus at current levels for a considerable further time yet.

That was hardly fresh news for the bond market, however after the steep climb in yields from 0.90% in early January to 1.75% at the end of March, the market was overdue for a correction on profit taking (by those that had short-sold bonds).

In the author’s view, nothing more should be read into this decrease in US bond yields other than a natural market correction following very large and rapid movement. Already the 10-year bond yield has lifted to 1.59% and further increases over coming weeks/months look likely as upcoming economic data releases confirm to speed and strength of the US recovery.

The recent reversal in bond yields is therefore expected to be short-lived, and thus the reversal in the EUR/USD rate to $1.1980 is also expected to be not that long lasting. There is considerable technical/chart resistance at the $1.2000 level that should hold.

The consequential conclusion from this analysis is that the spike upwards in the NZD/USD exchange rate last week to 0.7175 will also be very short-lived. A return of the EUR/USD rate to $1.1700 would see the NZD/USD reverse from the current spot rate of 0.7150 to 0.6950. Importers in USD should be taking advantage of this temporary blip and exporters can afford to be patient and stick with their orders to sell USD/buy NZD from 0.6950 downwards.

No surprises expected from this Wednesday’s inflation numbers

Do not expect any fireworks in the local financial markets from Wednesday’s CPI inflation numbers for the March quarter.

The price increases occurring across the economy have been well signposted and are expected. Inflation is forecast to increase by 0.80% over the quarter, however the annual inflation rate will remain stable at 1.50% as a large 0.80% increase recorded in the March 2020 quarter drops out of the figures.

Supply chain disruptions and increased freight costs will be behind the price increases in consumer goods, whilst electricity, rents, rates and commodity prices are all increasing.

The RBNZ are forecasting a 1.00% increase for the March quarter, a result below that may well be interpreted by the financial markets as slightly negative for the Kiwi dollar.

Whist there is no debate about what is causing the current increase in the inflation rate, the real debate is whether the price increases are merely caused by temporary factors (the RBNZ’s view) or whether they will be more permanent. Higher costs and prices feeding on themselves become permanent when the economy is strong, and demand outweighs supply.

For a variety of reasons the NZ economy is about to experience a double-dip recession following the Covid shock 12 months ago.

As we have stated previously, the export sector saved the NZ economy last year, however exporters are currently facing several business challenges that do not suggest continuing increases in production and investment.

Shortages of containers to ship the goods and shortages of skilled labour to produce the goods being the large and obvious impediments for our exporters. Local consumers had their splurge last year and this winter they will be spending their money on Australia holidays.

For these reasons, the near-term outlook for the NZ economy has turned decisively more negative, and thus the RBNZ may prove to be correct with their temporary inflation view as demand wanes. Therefore, the 26 May RBNZ monetary policy statement is expected to be more on the dovish side on the economic outlook than the neutral tone delivered by Governor Orr last week. The RBNZ will not be delivering to their employment growth target requirement if the economy is going backwards.

Lack of skilled immigrants hurting the NZ economy

It has become increasingly obvious over recent months that the current Labour Government is not up to the task of delivering/executing economic policy initiatives to invigorate the economy in the post-Covid era. There is a growing realisation that New Zealand is now rapidly falling behind other countries on the vaccine roll-out, opening its borders and returning the economy to a sustainable growth trajectory. The contrast between the current US and New Zealand economic trends is stark, worrying and negative for the NZ dollar.

What has become very evident over recent months is how dependent the NZ economy is on skilled immigrant labour.

The strong immigrant inflows over the years before Covid was due to New Zealand businesses demanding skilled people from offshore as they were not available locally.

The Labour Government had a policy to reduce immigrant inflows, which would have hurt the manufacturing and primary industry export sectors. Today, the Government displays absolutely no urgency in getting the nation vaccinated as soon as possible so the borders can re-open, and our export industries can maximise their potential with full workforces. Local technology companies like Vend and Seequent which were recently sold for extraordinary figures would not have grown their software solutions/products and global businesses if they did not have access to skilled and talented immigrant workers.

It is a sad indictment on the NZ economy when the outlook is negative despite the milk price being near to record highs above $7/kg milk solids for dairy farmers.

Instead of recognising the restrictions on our export industries and doing something pragmatic about it, the Ardern Government is sticking to their political ideology of redistributing the pie (instead of growing the pie) and running interference/intervention (Grant Robertson’s letter to Air New Zealand).

Global investors and traders will be recognising the lack of action and urgency by the NZ Government and in the short to medium-term this adds to the weaker Kiwi dollar outlook.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

11 Comments

As usual, excellent analysis from Roger Kerr. Wish he were Finance Minister.

Can't agree, I'm very, very happy he's not.

Roger,

1) Both Phizer and Moderna have a full book for this year. No other vaccines cut the mustard. The Govt could speed things up by buying some AstraZeneca but would you recommend that?

2) Given that the strong immigration flows of prior years led neither to solving the labour shortage nor to creating significant increases in per capita inflation-adjusted GDP, it that really the path forward?

KeithW

Importing skilled labour has had the sole effect of suppressing middle class wages. In that regard it has been a huge success.

Worth noting the Productivity Commission has found the average migrant is less skilled than the average person here already. And that even the genuinely skilled usually come with a contingent of extras to dilute the net worth of such a migrant.

Not from the migrant labour I have seen.

I see highly qualified people with excellent education and skills, and often better language and comprehension skills, who are also more ready to work.

Perhaps if you widen it to ALL migrants, including families, students and refugees, then it might be a truer statement. That could be managed by restricting the "contingent of extras" though, while getting the skills we need.

It's misleading to use the success of Seequent and Vend to justify using immigration to fill the shortage of workers for manufacturing and primary sectors. They are very different types of employees. Roles that pay above a threshold (2x median wage, ~106k/year) are prioritised and from people I know in those positions are still making their way through at a good rate.

The struggle to fill tech worker positions is less about strict immigration, and more about NZ companies just not having competitive compensation. Software Engineers in the US will typically make >4x what they will make in NZ. Good luck trying to get them to move here.

There's a huge difference between a software engineer and a service station attendant/security guard/fruit picker/courier (insert unskilled labour here). I'm sick of reading news stories about dodgy employers rorting the system here and in Australia exploiting the newly arrived compatriots from their original home countries. If you are highly skilled - let's say Master's degree or higher AND there is no one available in NZ who is available, then yes, a Work Visa is available as an option to a domestic employer. Too often, it appears there are too many shonky employers taking advantage of the lax policies of the Immigration Department. Not enough prevention, and prosecution of these chancers.

We need skilled workers in the building industry for work available right now, and could probably have done with container crane operators in the last 12 months too. Mind you, the global shipping crisis will probably put paid to many of those jobs as the materials won't get to NZ, even if AKL Port finally get their act together

Pick a city and you'll find either a skill gap, or a shortage of labour generally.

Dunedin, its hard to find skills or workers even for process work, multiple companies looking for workers.

Wellington - everyone's working for the government.....

Auckland, lots of CV's, only a few of acceptable standards

As for those taking advantage of low skilled migrants, that's a whole different story.

Throw the book at 'em, and don't let them employ in the future.

Our vaccine rollout may not be lightening fast but it's not as urgent as other countries with populations over 100 million and that are still in various levels of lockdown. We're enjoying a level of freedom unprecedented in most parts of the world.

Vaccinations are also not a 100% guarantee that travelers don't bring COVID-19 to our shores, so I'm happy with the current border controls. But then, I'm not working in an industry that relies on overseas visitors, although my pessimistic expectation is that the Trans-Tasman Bubble will bring along some community transmissions and another round of lockdowns, but not limited to Auckland this time.

As for the migrant workers, well that can be placed fully in the lap of the employers who refuse to pay a wage high enough to attract unemployed Kiwis, and in the lap of those same Kiwis who refuse to work for migrant wages. If those 2 groups got their act together, we wouldn't have a need for seasonal migrant workers and instead they would be a bonus when they're available.

The downside to increased tourism, as I see it, is that prices will creep back up to international levels and domestic tourists will be avoiding those high-priced places just as they did pre-COVID. Hopefully the difference can be made up from all the Australians coming to visit, but historically it was the Asians who were the big spenders.

That's where you've fallen into the trap of believing the Government. They claim this is all part of a grand plan. Australia are at least as good at preventing and managing COVID as NZ, their failings have been the same as ours.

Vaccines are preventative, our moat and border closure can't last. We need high levels of vaccination before we can enter the world again. A likely 2023 completion would be a disaster. Then again, its not like the government achieves any target they set, so better to drift along claiming victory.

The fruit picking industry had myriad incentives but kiwis didn't work, much fruit rotting on the trees, and wine industry doing pruning over many months rather than at the correct time. NZ exports will take a hit and our local fruit prices will skyrocket. Overseas income lost.

We're about to enter a recession, this time not rescued by pent up demand. The government are spending their time adding costs to employers and hate actions against landlords for PR gains. I'm picking them to spend wildly as the economy stumbles, but not spending that builds economic capability. Tourism is a 7 day business, kiwis visit in the weekend and school holidays. Overseas tourists balance the rest of the time to keep the industry afloat.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.