By David Hargreaves

The development of the worrying situation that is the current Auckland housing market can be measured through the Prime Minister's denials.

Last year John Key denied existence of a housing 'crisis' - whatever that actually is supposed to be anyway. And he's continued to do so.

Now he's denying existence of an Auckland housing bubble. I leave it to readers to decide whether they think a 'crisis' or a 'bubble' is worse, though for my money the 'b'-word is far more scary.

Of course, denials only serve to put the subject being denied more and more into the public domain. If the Prime Minister's denying something, there must be a problem.

It is a standard management technique to attempt to handle a problem by denying its very existence.

With all this in mind, I was intrigued to read research by academics Peter C B Phillips, of Yale, and Auckland University's Ryan Greenaway-McGrevy (Sunday Star-Times, business section, page D10).

This said, unequivocally, that the whole of the NZ housing market was in a bubble from 2003-04 to 2008, while Auckland re-entered the bubble zone in 2013 and has remained there since.

Yep, take note Mr PM, the sums have been done and Auckland's a bubble, all right.

The academics say there's no ongoing evidence the "contagion" from "the latest Auckland bubble" has made it to other centres.

This provides further evidence of the Auckland-as-an-island emerging theme.

In his weekend column Bernard Hickey referred to Auckland having "officially disembarked from the rest of the country".

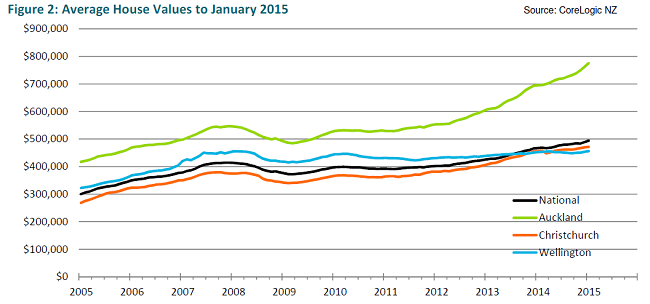

They say that a picture (or perhaps a graph) is worth a thousand words. I was absolutely riveted in reading the latest MBIE Housing and Construction Quarterly by one graph in particular, which I include below.

If anything demonstrates just how Auckland's house market has disconnected itself from the rest of the country - in a way not seen, certainly in recent history - then surely this is it.

As can be seen, during the previous housing boom, the rises and falls of the Auckland market were matched (albeit at a lower price level) by mirror movements in other parts of the country.

But since about 2013 - when the academics say the Auckland bubble started inflating - our largest city's house market has completely disconnected itself from 'the rest' and is now heading for goodness knows where.

So, of course with such a problem visibly manifesting itself by the week, politicians - and this is including local government ones - are doing what politicians do best, and are talking up a storm.

But amid all the chatter, what I'm not hearing is any concrete proposals to give the naughty Auckland market a kick up the Khyber Pass.

All we are hearing is about supply and what's being done there, through such strategies as the Auckland Housing Accord.

Supply, supply, supply

In his Radio NZ interview the PM banged on and on about what the Government is doing to help supply.

There's two issues here: One, it will take years not months to ramp up the supply of Auckland housing. Two, the Government and other politicians can happily talk and talk and talk about supply because it's essentially a positive thing to talk about. We'll build houses, and we'll create jobs and people will have places to live. Marvellous.

But, dear politicians, there's another side to this and it's the side you don't want a bar of because if you are seen to be doing anything about this, well, then it would be negative.

Yes, I'm talking about demand.

Demand? What demand?

Reserve Bank Governor Graeme Wheeler recently suggested that about 40% of houses in Auckland were being bought by investors. Now, whatever you want to say about Auckland's perceived housing supply shortage, if 40% of the available houses are being bought as investments then clearly there's a hell of a demand issue as well.

But what's the Government doing about that?

They could immediately do something about about the high levels of immigration that have seen a net 55,000 people arrive in New Zealand - about 25,000 of them in Auckland - in the past 12 months.

They could do something to limit the numbers of offshore-based investors buying properties by introducing a rule that any overseas buyer of a house has to come and actually live in the house, or alternatively that offshore investors must build new houses.

They could introduce capital gains tax on investment properties.

They won't.

Why not?

Because these things would be unpopular.

It's much easier to talk about building new houses than any measures that might discourage investors from pumping more and more money into the inflated Auckland market.

Just keep talking

So, we'll keep talking and talking and talking about supply. And who knows, if enough people believe the mantra then maybe there really will be a whole lot more houses built in Auckland eventually - possibly just in time to coincide with a global event that sees our 40% of investor-buyers take fright of the housing market and disappear overnight.

And that's what really concerns me. Investors might burn their fingers somewhat. But if (when) there is a serious correction in the Auckland market the people who will really stand to get hurt are the people who have bought houses to live in that they've had to pay too much for because they've been bidding against investors.

The only talk about houses that will be worth listening to this week is when the Reserve Bank Deputy Governor Grant Spencer (who crucially doubles as the central bank's Head of Financial Stability - housing being a financial stability issue) will make a speech in Rotorua - er, about housing.

It's unlikely that Mr Spencer will be discussing the outcome of TVNZ's "Our First Home" or the benefits of building a deck. He may of course give some hints - or perhaps even more - about what the RBNZ proposes to do about the Auckland situation.

So, all eyes will be on the RBNZ, trying to do the Government's job for it.

And if whatever the RBNZ comes up with happens to be as unpopular as its restrictions on high loan to value lending, then you can count on the Government to distance itself, shrug its shoulders and say, well, the RBNZ is independent...

Nothing to do with us...

70 Comments

He's just hoping the bubble doesn't burst before he sells up and vacates to Hawaii.

Talking about bubbles.....I am still staggered that this property sold for $840k in the weekend...... http://www.barfoot.co.nz/540813

Unreal.

lol, the median rent for a 2 bedroom house in that area is $480 pw according to the DBH

If that there does not PROVE there is a bubble I don't know what does...

Absolutely ridiculous and re-affirms my decision to leave the rotten-to-the-core city.

and, to think that Bernard Hickey sold his Epsom house for just a touch more

A bubble on a bubble. Aucklanders are like sheep to the slaughter. Everyone will be shocked at how fast greed turns into fear... Might be a good idea to invest in a few bars me thinks.

That seems quite reasonable for the area. Assuming it's not leashold.

How about this one selling for 1.35M? http://www.remax.co.nz/12417043

There is an old saying "Never believe anything in politics unti it is officially denied"

John Key is a member of the church of the squiggly line - whose belief is (if you look at that pretty chart) the Auckland line is an abberation and is unsustainable and will eventually revert back to the norm in keeping with the other lines

What might be news to him is there is another possibility:- the other lines just might in fact kick up in tandem with, and catch up to Auckland.

That is not as fanciful as you might think, if you only look at pretty pictures of squiggly lines

I can't imagine foreign investors competing to buy in Palmerston North. Gen X and Y might give up on Auckland though, and try to front-run the baby boomers.

David, you say bring in a capital gains tax.(CGT)

Please explain to me and your readers just what a CGT will do to slow down demand?

Indeed, name me one tax that has decreased the price of anything in the market

Sorry but a CGT will not only not work but as it won't apply to home owners who make up the bulk of the market so it will have no effect on prices whatsoever.

A CGT will be passed onto buyers and merely increase prices, and will be made worse by people not selling to avoid the tax hence raising prices through squeezing the market further.

I repeat: Name one tax that has decreased the price of anything.

It will be funny, they bring in a CGT just before the bubble bursts, then everyone books massive losses and nobody pays any taxes for the next 20 years. Thats probably my main issue with using a CGT to lower prices.

Labour's CGT is 15% tax rate to "allow for losses", ie you cannot book any, so not a problem.

Ollie .... sorry , my bad ... ummm ... " Big Daddy " .... I think that David just threw in the CGT as one means of curbing the property speculation ... one means amongst several ...

... but , of course , CGT is only effective where it's comprehensive .... no exemptions ... but it's way too politically unpalatable to include the family home .... you ain't gonna get onto the gold-plated seats in parliament if you offer up a comprehesive CGT to the electorate ...

So , we're left with the one tax that no one is talking about .... well , Bernard Hickey has been , 'cos he's championed this excellent anti-speculation measure for several years now ...

... a land tax ! .... simple to apply , comprehensive , raises bucket loads of dosh for the government , and takes the wind out of the rampant land speculation we're currently witnessing in Auckland city ....

Good on ya , Bernard !

land tax just gets passed on to consumers

Not necessarily. Rents are determined by supply and demand, it's not cost plus.

when it hits across the whole market then yes it gets passed on. That's what stops Libertarian utopias from realising the promised cheap prices they predict, as they leavy costs across everything there is no alternatives pressure to keep prices down. So levy rates inflate prices rather than taxes, but it is usually considered "fair" because it hits everyone and participation isn't theoretically mandatory.

... if you accept the premis that if you want to retard anything , or to destroy it , you slap enough tax onto it ... then a land-tax subdues the expectations of speculators of gigantic swathes of free money flowing to them from increased land prices , dairy farm prices , house sections , whatever ...

The flip-side is that you off-set the other side of the government's accounts by decreasing personal income taxes and company profits tax by the same amount as you collect from the land tax ....

... the net effect being more money in the pockets of non-land owning workers ... and more incentive to establish your own business ....

What has libertarianism to do with this? Where does libertarianism promise cheap prices or levy costs across everything?

LVT local government rates are better than capital value rates because.

- They are unavoidable, unlike labour or capital, land cannot migrate away.

- It incentives the productive use of land.

- Those doing nothing or very little with land pay the same LVT rates as those who are more productive. Land bankers and speculators hate them.

- The marginal cost of more intensive development is zero.

- Thus they actually enhance agglomeration economic efficiencies in urban environments. Not like urban growth boundaries -there ineffectual replacement.

Years ago local government got soft hearted and transferred from LVT to total capital rates. They wanted to tax wealth like their big brother -central government rather than properly regulate land development, which is their actual function.

The turning point of Councils losing control of affordable urban development may have been when Councils started to think like Central government and tax wealth rather than focusing on a taxation and planning system that enhances the affordable development of land.

As posted earlier, it makes ppl not invest and causes prices to reset.

http://www.zerohedge.com/news/2013-12-04/its-payback-time-foreign-uk-ho… and http://www.zerohedge.com/news/2015-04-12/uk-housing-bubble-bursts-sales…

nice little gem in the first article

60% of all home purchases are "all cash" - best of luck controlling that Graeme Wheeler

....does a proposed tax (or closing of tax loopholes) count Big daddy?

Labour's plans to change rules allowing wealthy foreigners to lower their tax bills is causing London property deals to fall through and homeowners to sell up, estate agents have claimed

When demand is over supply, the buyers pay CGT. When supply outstrip demand, the vendors pay CGT. It is that simple.

40% of house purchasers are investors. How does that square with the near 50% home ownership levels in Auckland? If only 50% of Aucklanders own their own home, and that has fallen from over 70% surely over 50% of house purchases have to have been by investors.

Trusts?

Exactly. More than 50% of the houses are being bought by speculators. It's not a rational market driven by fundamentals like living costs.

If any of you think that the Auckland market is a bubble, check house prices in small Asian cities ( China , South East Asia, India) with poor infrastructure) and then come back to me

Not to mention that in China, at least, you don't get to own the land underneath, so is anyone really surprised that people not able to own land in their own country are so desperate to own some wherever they can. I believe it is this money that is distorting the market more than anything else

you want to bring the house prices down?

Make it law that all houses SHALL be brought up to current code before purchase and sale agreement is settled.

No more passing the buck to the unsuspecting or following generations.

Full insulation, modern wiring, proper earths, no condensate or dodgy pipes, no drains that are too small or back flow on to the property.

Because new houses _already_ meet compliance, and they set the top bound of pricing already.

So when second hand property suddenly has to comply to the same rules, it's value becomes....

And this goes for council compliance too. No more slipping it through before it's on the LIM.

Mandatory inspection at sale date, fix or council gets certification of compliance that declares it as a brownfield knock down.

put that one in yah boots...

That's just plain cowboy. Buyer is the one coming in with a vision - as is where is.

I'd like to hear you tell my Gran she has to do up her house to someone else's standard on her pension before selling - she will have something to say

Then your gran would have to do a deal with the incoming tenant to contract the repairs.

She's had a while to bring the place up to code, or she brought it knowing she was getting a disount deal in that it wouldn't have to brought up to modern standards.

This falls on the tail on how previous generations could get "start-out" discounts, yet modern and low-income people aren't allowed that "no frills" discount that many of the older generation had. Now those new generation have to pay modern prices or are forced to "buy new" with all the bells and whistles.

Your gran, she'd be upset that she's not getting the huge "capital gain" that others received because she'd have to do a bunch of work to have the house up to code? Then perhaps that "capital gain" vs the "new house price" is an accumulation of "no frills privilege" and "differed maintanence". Since it's the new house alternative that sets the top bound, and those not able to pay that premium price must settle for overpaying for what is really...as you have pointed out (with your grans costs of updating)...really a house of much lower _value_. The demand pushing the price up is solo from the cost of new alternatives. (hence the "tiny house movement" too).

It's not that I think that such a thing _should_ be introduced...although after dealing with the bad design inherited in my recent purchase (all storm water drains are very poor design, and most drain back into the section).... it is clear that once again the wealthy are taking advantage of the young and poor in order to pay their leveraging debts... (rather than keep to a proper standard)

This article is great. It belongs in the mainstream media.

ha ha..you just pointed out why it is not in MM!

Is it really a bubble when viewed globally? Another article shows commercial property sales at record levels to foriegn buyers at 57%. NZ probably looks pretty good for investors from other countries economically, also politcally with low coruption and environmentally with low population numbers and a clean green image. It looks to me as though the property 'bubble' could expand for sometime yet. Even demographically if we have a large number of baby boomers holding assets and selling these to fund retirement the additional supply could easily be soaked up by the much larger numbers of rich foriegners.

The rents havent risen yet but are starting to climb and by some accounts it is hard to find rental accomodation, it can be like applying for a job.

It is hard to see with so many agendas and interlinking statistics but I think the boom will continue and may acclerate as China comes off the boil and more people pull their money from there and put it here.

Yes it is a bubble when viewed globally. By most metrics you care to choose. Rental yields, prices relative to incomes, prices relative to long term averages.

Your post alludes to the problem. The only thing propping up this entire steaming pile is the Chinese. Take them out of the equation and watch the greed turn to fear overnight.

The Chinese are probably a particular case where they will tend to think in terms of their domestic values and are then led by a ring through their collective noses to buy in Auckland led by local based Chinese agents themselves using questionable ethics.

It all helps to destroy the NZ ethic of fairness that helped us to the top of the world in lack of corruption. Then again our current Government is showing a drift in a similar direction.

The chinese seldom sell except out of real need. They seem to be culturally leaning towards never releasing land. (can't blame them, its the smart call).

Just look at all the forestry land they own, both in trees and out.

Yes it is a bubble. So by your argument lemmings jumping off a cliff to their deaths en mass is a perfectly sound decision?

Just consider for a moment that any time profit on an asset is based on its capital gain and not its income its over-priced and heading into bubble territory. Now that doesnt mean ppl cant make money, but now you are gambling and you need to know the timing to exit, but greed gets in the way, think tulips. The Q then is who takes the loss. If as per expectation the losses go back to the lender ie the bank(s) and its expected our Govn bails the bankrupt bank(s) out then in effect I the tax payer who acted sensibly and didnt participate carries some or much of the loss. Now if I was getting an insurance levy then I suppose my Govn acting on my behalf is a willing participant in the "deal" but I still object to it as the levy is priced to low.. Besides which the banks wont pay insurance so should not be bailed out.

Rents are not following the rise in asset values (ie as fast) from what I can see. On top of that the areas rising fastest are not rental areas but high end? I'll agree on $s being hidden here the faster a CGT comes in the better IMHO.

"need to know the timing to exit"... First, steven, I'm surprised you're lecturing anyone about timing housing markets; you've got it horribly wrong for years now.

Second, rents are catching up, see today's headline for the latest example.

"profit on a asset"... in a QE and ZIRP world return on captial is lower, it's a new normal, that includes rents and that includes rents on Auckland houses. Your antiquated metrics also ignore accumulated weatlh.

And most important... you and I both know you've been posting this nonsense for years now and getting it horribly wrong, in the time I've been reading your doom posts the Auckland market has sky-rocketed.

I am not lecturing on timing, I didnt say it was easy in fact it isnt which was my point. Just remember what you have is an asset that may or may not be cashable for the amount you think its worth. My assets were sold early, sure but I have the cash.

Returns on capital is indeed lower, that isnt a normal nor acceptable, when the risk is bigger its a sign things are not well and market players are deluded. In terms of doom posts actually I have been pointing out that when event(s) occur then the housing market will be in severe difficulty it comes back to timing.

Auckland, yes indeed its only in Auckland really, so it is a gamble, good luck with that.

This Government is in complete denial that there is a housing crisis in Auckland because they and their backers are so heavilly involved in rental properties.

This is similar to a pyramid game where money must come in from underneath to sustain the bubble.

It started with the world being flooded with cheap money which went into assets instead of production and jobs. Now because prices are going up everyone in NZ and overseas want a bit of the action and are putting their money into houses to rent.

It reminds me of the same scenario with the sharemarket before 1987 when everyone was advised to put their money in the sharemarket to get higher returns than the bank and they could not go wrong because of the demand for shares.

Then came forrestry syndication followed by finance companies.

Now we have rental properties.

They all follow the same pattern, the frenzy feeds on itself until it becomes unsustainable and collapses.

Many people who have bought investment properties over the last 4 years are going to be badly hurt and all their life savings tied up in property will be wiped out. History repeats itself.

Why should this property bubble be any different from the above ???

Pyramid schemes are only under-written by new comers, Auckland property is under-written by land, building and other hard tangible assets that have had value to humans for thousands of years.

Your just trying to draw parallels to something with negative connotations despite the fact that there is little in common.

I agree partly with you but at the moment houses are being used not for the purpose they were built for but are now being used by many only as an investment vehicle to make money.

This is not a normal property boom cycle. I am retired, have seen many property boom and busts, have studied economics and I know this boom will end in tears, not for the professional investor but "mum and dad" investors who think they have done the right thing for their retirement.

Believe real estate agents, banks and the Government at your peril,!!

The boom in Auckland is being driven by supply shortage so we have to ask ourselves, how long will it take to correct said shortage.... At the rate that we're building houses today it will take years to catch up with the under-supply and that's assuming Auckland's population stands still. But Aucklands population is not standing still, it's rocketing ahead at a stratospheric rate and the unitary plan has declared we are going up not out. I could go on and on about factors pushing the market up.

Believe the doomsters at your own peril ! ! !

My guess, Auckland's average price will hit 1m before it slows down.

If you believe the housing bubble is as a result of a housing shortage in Auckland, then tell me why house prices in ALL major cities have inflated by as much or more than in Auckland?

ie, look at Sydney and London, to name two.

It has only happened since Governments have introduced quantative easing.

I do not believe for a moment it is only as a result of a major housing shortage.

Only a very small part of it comes from a housing shortage.

Chinese money is mostly "hot" money which will go to wherever the best return is. As soon as there is a perceived downturn in Auckland's property market, it will go offshore.

Calgary, Edmonton, Winnipeg, Atlanta, Richmond, Austin, Houston, Dallas, Tokyo

Bigger, faster growing, cheaper than Auckland

Housing shortage is just part of the perfect storm; the underlying cause of house price inflation across the developed world is debt and growth based economies that create systemic inflation in all things, most of all in life's essentials like housing. House price inflation didn't start with QE, it started in the 17th century when debt and fractional reserve banking were created. Saying "it's the foreigners" is a weak excuse for a problem that is very much created by Kiwi's, if there is any investment at all in NZ housing it's because we are perceived to be following the debt/growth handbook by the letter and hence ensuring a safe, profitable, inflationary place for people to park their money. I tend to post what I think will happen not necessarily what I want to happen, and I have been getting it right for years now. And regarding your comment about the Chinese, "it will go offshore"... you clearly don't know any Chinese investors, I do, and they are not going anywhere. There investment in Auckland housing is accelerating and levels I could never imagined, if only you could see the things I see you would be thinking my 1m average price prediction is modest.

... you gotta stop watching the " Keiser Report " , dude .... that guy is nearly as big a gloomsteriser as Bernard " Chicken Little " Hickey ...

It'll all be hunkadory , right after we print off another coupla trillion ( insert currency of your choice ) ...

.., then you'll be happy .... promise !

I was thinking about you the other day GBH; as I watched reports of the Aussie economy stumbling further and further and asking myself, what's the right time to buy into the ASX.... Care to comment....

The ASX is one of the few markets in the world below long-term average based on CAPE. That and the fact we are at a one in a generation high against their dollar means I have been buying for the last few months and will continue to do so.

Thanks Kiwi; I'm on the sidlines now, I want to wait for their OCR to bottom out first. Have you bought any mining stock?

I buy the whole index as I prefer not to fail at picking winners. Mining stocks are about 15% of capitalisation.

... Mr kiwimm has nailed it , Happy123 ... the Aussie ASX indices are still way below their all time highs , the $A has fallen sharply against the Greenback ...

And the hickeysterical gloomsterisers across the Tasman are bellowing that the end is nigh , the resources boom has ended , all is lost ... blithely ignoring the massive boost to exporting SME's that the Aussie dollar's fall has granted ...

... seems to me that the time is right , just now , particularly with the extraordinary high $Kiwi to the $A ... jump in , fill your boots , hock off grannie's false teeth if needs be , to get some of the Aussie action ...

But , as they always say : DYOR !!! .... although what the hell desperate Yugoslavian overstayers & refugees have to do with investing totally eludes me ...

Are you buying mining stocks?

... miners are worth a dabble , at these depressed levels .... got a little gold , oil and gas .. mining service companies ... go for the ones with little debt on their balance sheets ...

Biotechs are my pick currently ... Australia has screeds of tech sector companies ... the healthcare and biotechs are particularly cheap .... also software firms , internet retail portals and the like ...

... but remember , Gummy has such an appalling record of picking stocks that I'm occassionally mistaken for being a stockbroker !

Irrationality says it will proabably go to $1m then promptly to $500k

You'll see (and I think since the election last year we are now seeing it) a last surge higher in prices in speculative markets as 'joe blogs' finally catches on that auckland prices are skyrocketting and they want a piece of the action.

If you look at a bell shaped curve distribution of people, the 'joe blogs' type person doesnt go on websites like this, or talk to people who crunch numbers, or can even do basic math. They cant calculate a yield and dont know what a price to income P/E multiple is. They watch TV shows 'my first home'. Unfortunately, numbers wise, they make up the bulk of the population. Thats why to informed observers we think its madness, but we are merely projecting our own mindsets onto people who think completely differently. The market is a voting machine not a weighing machine Ben Graham once said. Popularity is a funny thing for the majority of people.

Essentially, at later stages of these things, the mid to late adaptors who get there info from bbqs and TV shows pile in, numbers wise they are the biggest group, hence the late surge in price, but once they have all been 'converted' to bulls, there is no one left, and thats when you see a top. Cant be too far away now in the auck market, another year or so.

Prices wont crash unless something external triggers it. You will see sales vols remain very low for a number of years and prices flatline for a number of years, once sentiment goes it can be hard to get back (look at all other housing markets in NZ past decade). My pick is for 7+ years of flat lined prices in auck as rents and income, and regional house prices, play catch up. Nothing to worry about unless you just bought a rental that 15k negatively geared p.a meaning 105k cash down the drain over the next 7 years if cap gains do hault just at the wrong time.

I think it's possible to have a crash without an external trigger if enough people are negatively geared. I haven't seen stats on that - have you? Sentiment is a powerful force and topping up an "investment" each month becomes very unattractive when capital gains look unlikely.

Such jumps normally come in threes.

the value investors picking up the old, reinventing the new. prices step a short distance.

a few drop out for own reasons (low resources, over exposed, better deals elsewhere)

then the hike, investors see value and start buying, some wait to see if it's a trend so they tend to keep it rising. the sell-outs fingerjoint into the new buy-ins. Money starts to see a rise coming, many jump in, several jump out early having hit their mark. the rush falters (which is the GFC).

then the latecomers come in.

if it's overseas money in first phase we're going to see a steady trend and more lifts.

if it's home investors, grabbing super-heated last minute deals we'll see a short burst and then the dropping off cycle as it comes off the local peak.

If the last cycle isn't brief, then more folks will see it as a trend or bubble. smart money wll get ready for the pieces, and the mum & pops will be looking to lose their lives savings (again)

Only my opinion'but it seems to me that the bubble is slowly making it's way to the northern suburbs of Hamilton especially at the top end of the market.

I hope so, NG, I need a million to retire on eventually, cannot wait?..Yippie, Hawaii here I come.

"nequivocally, that the whole of the NZ housing market was in a bubble from 2003-04 to 2008" - that was a great time to buy an Auckland house. My friends that sold or avoided buying in that bubble are pretty upset about it now.

So we're doing this again are we interest.co.nz... Is it 2011 again? Is this an article by BH? We all know how that 'bubble' prediction turned out don't we....

I could list 10 reasons why Auckland is not in a bubble and why prices will keep increasing, just like I did back in 2011. But what's the point, no one wants to understand why prices are going up and why their so called metrics arn't working anymore; they just want to complain about it and scream "bubble".

Agreed, a bubble suggests burst. I dont think the house prices will crash. The world is awash with cheap money, this is a nice safe country to invest and there are lots of Chinese owners who would never sell at a loss.

Perhaps a levelling in prices once supply catches up with demand but no crash.

Ok Happy, since you endlessly claim to be the guru of all things Auckland property, why don't you offer to write an article on this website presenting your argument?

Put your mouth where your money is.

My money is where my mouth is... I'm neck deep in the Auckland market, that's the difference between me and the average commonpotator. This is what I do, I would never offer commentary on what ever it is you do, because I know little about it, it's odd that so many people who clearly know nothing about Aucklands market feel fit to comment.

Write an article... conflict of interest, a conflict of my own interests, the most important interests.

Auckland house prices are dictated by events overseas. As long as the world economy stays stable then Auckland House prices are OK. If any major crisis occurs overseas or a change in path by central banks then this will decide the direction on Auckland house prices. Suppy and Demand are only relevant when markets are stable and no serious event. The US federal reserve has a bigger influence on Auckland house prices and other central banks and they will decide when the Auckland House prices growth will come to an end.

Excellent article. There is so much talk and huffing and puffing from all sides of the political spectrum, and a whole lot of nothing being done.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.